How to Make Smarter Stock Selling Decisions

Selling investments is one of the most difficult decisions investors face. Many of us know the feeling — reluctant to sell, even when logic suggests we should. In this article series, we explore why selling is so hard, the psychological biases at play, and some strategies to improve decision-making.

By reading this series, your key learning outcomes will be:

You will understand why we are so reluctant to sell a stock, to gain clarity and discipline when analysing your portfolio.

You will learn systematic approaches to selling based on rules, with a unique framework to simplify the selling process.

You will learn discretionary approaches to selling, by considering more carefully the reasons why we bought in the first place.

You will learn to keep a cool head during significant market events, by knowing exactly what to do after profit warnings, accountancy irregularities and takeover bids.

You’ll know how and when to rebalance your portfolio to minimise your risk.

And finally, you'll understand the principles behind stop losses, how they should vary based on risk and why you should cut your losses before it is too late.

Why Are We Reluctant to Sell?

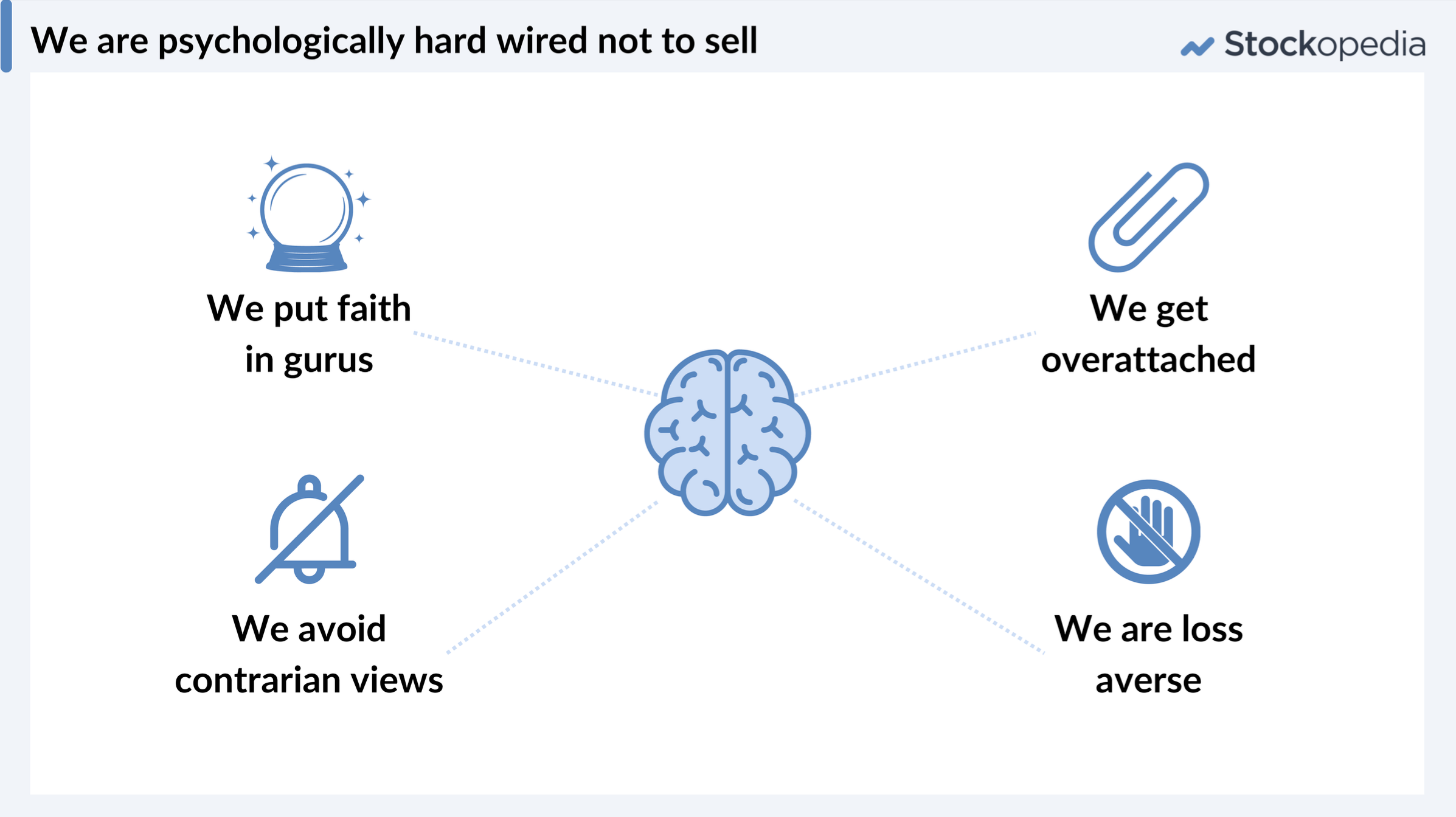

The reluctance to sell is a common issue for investors. Some of it stems from mindset and behavioural biases.

For example, many investors develop attachment bias: we research a stock thoroughly, buy into its story, and grow emotionally attached. Selling often feels like admitting defeat on a promising stock, or letting a winner go too early, even if the circumstances change.

Closely related to this is confirmation bias. We tend to seek out positive news and analysis about the stocks we already own, while dismissing or overlooking negative signals. This imbalance in analysis clouds judgment when it comes to selling.

Human beings are also loss averse, meaning we feel the pain of our losses doubly as much as the joy from our winners. As a result, we are 50% more likely to sell our winners than our losers

We also badly from “authority bias”. Analyst and broker recommendations play a real role here, as we tend to trust experts. Across the London Stock Exchange, there is a huge bias toward “buy” and “strong buy” recommendations.

Very few analysts recommend selling, partly due to conflicts of interest, media narratives, and PR pressures. As a result, investors constantly hear bullish cases, making it harder to step back and sell objectively.

Selling can seem hard, but by recognising we are prone to attachment and confirmation biases and the influence of analyst recommendations, we can make more rational and effective decisions.

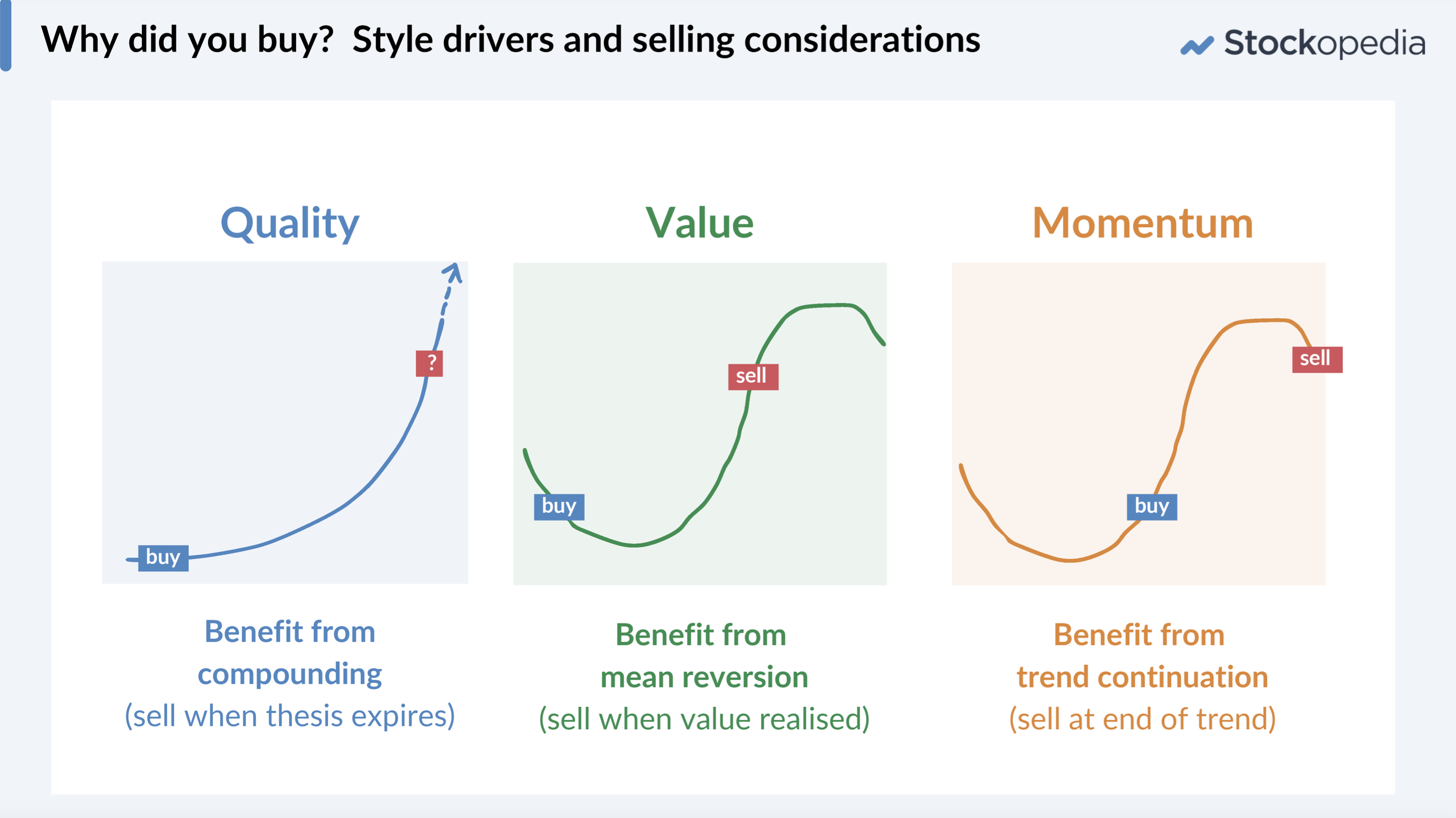

Selling is easy, if you know why you bought

The most crucial, basic truth behind selling is that selling is easy, if you know why you bought.

If you buy a stock based on its quality - then you may be aiming for it to reinvest its profits and compound its growth. When that reality changes, it’s time to part ways.

If you see value in a stock - then you should aim to sell once the true price, or a typical valuation is realised.

If you are buying due to earnings or price momentum - then selling at the end of that trend’s period will see the best results.

Selling is made all the simpler if you know why you bought.

Our first article will take you through a few systematic approaches to analysing a stock based on this framework.