Good morning!

To start off the week, I'd like to mention Stockopedia's new podcast that has been produced by our colleague Lawrence - Companies and Markets Weekly.

The first episode features Roland, Lawrence and myself as we discussed the financial stories that we found most interesting last week. It's available on Spotify and Apple Podcasts.

Huge thanks to Lawrence for spearheading this - and I hope you like it!

12pm: this report is finished for today.

Explanatory notes

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day. We usually avoid the smallest, and most speculative companies, although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We have a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Add your own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing. Links:

Daily Stock Market Report: records from 5/11/2024 (format: Google Sheet). Updated to 10/12/2024.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Ricardo (LON:RCDO) (£250m) | Acquisition & divestment. | Ricardo is spending £51m on an advisory firm and is divesting its Defense unit. | |

Videndum (LON:VID) (£245m) | TU | Profit warning? 2024 rev £280m (StockReport: £315m). Dec 2024 banking covenants amended. | RED (Graham) |

Tristel (LON:TSTL) (£187m) | AGM Statement | In line. Expecting to hit or exceed three-year revenue growth target of 10-15% by June 2024. | GREEN (Roland) |

| Saga (LON:SAGA) (£177m) | Saga and Ageas insurance partnership | Saga selling underwriting unit (£65m). Will outsource home/motor, cons. up to £140m | AMBER (Roland) |

Filtronic (LON:FTC) (£158m) | TU | H1 25 results to be ahead of expectations. Reports pull-forward of orders. | AMBER (Roland) |

Duke Capital (LON:DUKE) (£124m) | Interim Results | Cash rev down 4% to £13.5m, free cash flow down 26% due to fewer exits. “Positive outlook”. | AMBER/GREEN (Graham) |

| Concurrent Technologies (LON:CNC) (£117m) | $3.3m contract win | Order for standard computer boards from existing US customer. No change to guidance. | |

| XLMedia (LON:XLM) (£33m) | Update on distribution of capital | Proposes £16m ($20m) tender offer, half of potential total cash available following disposables. | AMBER (Graham) |

Cirata (LON:CRTA) (£31m) | Contract wins & FY24 guidance | New contract with IBM, but FY24 bookings guidance withdrawn due to pipeline delays. |

Summaries

Filtronic (LON:FTC) -up 4% to 75p (£163m) - Trading update - Roland - AMBER

The electronics group has upgraded its guidance for FY25 as existing orders are pulled forward. I’m positive, but I wonder if this could have a negative impact on FY26 trading. Broker forecasts suggest some risk of a profit drop next year. I’m broadly positive, but I reckon the shares are up with events.

Duke Capital (LON:DUKE) - up 3% to 30p (£153m, 510 million shares outstanding) - Interim Results - Graham - AMBER/GREEN

The interim results show little change with a mild increase in recurring revenue and a flat dividend. More interesting is the change in strategy as Duke moves away from the UK equity market as its primary fundraising tool. It’s now looking for managed accounts or joint ventures that would deliver fee-based revenue. I think the change makes sense and could see Duke evolve into a unique type of fund manager.

Saga (LON:SAGA) - up 6% to 131p (£187m) - Saga and Ageas agree new insurance partnership - Roland - AMBER

The over-50s travel and insurance group has confirmed a partnership with insurer Ageas to complete the transition of Saga’s insurance operations to a capital-light, marketing-only model. Substantial cash inflows are expected, but seem unlikely to accelerate the group’s deleveraging. The shares could be cheap, but I think risks remain. I’m staying neutral for now.

XLMedia (LON:XLM) - down 24% to 9.45p (£25m / $32m) - Update on distributions to shareholders - Graham - AMBER

Proceeds from XLM’s disposals that are likely to make their way to shareholders’ pockets turns out to be lower than hoped for. Only up to $5m is anticipated from earn-outs (out of a maximum $15m) and shutting-down costs could cost up to $13m. Hopefully this is the last disappointment from XLM before it leaves the market.

Videndum (LON:VID) - down 18% to 210p (£197m) - Pre-Close Trading Update - Graham - RED

Detailed forecasts are unavailable to me but the new revenue estimate looks very poor at just £280m. The company is trying to boost margin but at the same time it announces a £25m impairment that will hit both stock and intangibles. Prior management gets blamed for what has happened here, even though the Hollywood strikes and weak demand in the content creation market provided ready-made excuses. With the company requiring very loose covenants from its banking syndicate, it’s an automatic RED from me.

Short Sections

Broadcom (NSQ:AVGO)

Up 24% on Friday ($1.05trn) - Q4 results - Megan - AMBER

A 24% share price leap to take the company’s market capitalisation into $1trn territory, was enough to make Broadcom (NSQ:AVGO) one of the most popular shares on our site over the weekend. It’s rare for our community to be so interested in the StockReport of a non-UK share, but AI companies tend to buck the trend. Broadcom seems to be giving lots of investors Nvidia vibes.

Both semiconductor companies have very exciting exposure to the artificial intelligence industry. Nvidia specialises in a unique piece of hardware known as a graphics processing unit (GPU). Broadcom has both the hardware and software products, but it's the software solutions that are really benefiting from the surging demand from AI customers.

In the fourth quarter of the 2024 financial year (to November), revenue was up 51% to $14.5bn. In the year as a whole, AI revenues were up 220%.

In the company’s earnings call, its chief executive Hock Tan fuelled the excitement which has propped up companies with AI exposure (and the US markets as a whole) with his outlook for the coming years. He told investors that the addressable AI market for Broadcom is expected to rise from $20bn currently to between $60bn and $90bn by 2027.

Megan’s view:

It’s good to see another semiconductor truly joining the AI party, which Nvidia has attended on its own for most of the year. Broadcom’s share price has doubled in the year to date, which is still some way behind its larger peer, but nonetheless impressive.

The problem with Broadcom is that sales growth is far less consistent than that of Nvidia. While the larger company manages to deliver consistent growth on a quarterly basis, Broadcom’s growth is coming in surges.

Its earnings momentum also isn’t quite as impressive as that of its larger peer and margins aren’t growing, which is surprising given the market opportunity.

That said, I can’t see the US market turning away from Broadcom in 2025. For momentum investors happy to ride the wave of positive sentiment towards AI companies, this could keep delivering. For those looking for more fundamental value, Nvidia looks like a far better pick. AMBER.

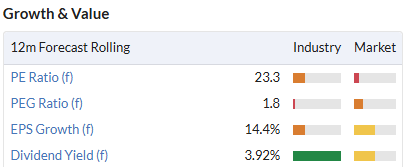

Tristel (LON:TSTL)

Down 2.6% to 380p (£181m) - AGM Statement - Roland - GREEN

This infection control business has issued an AGM statement today confirming that the company is trading in line with expectations.

Tristel also confirms that it expects to “hit, if not exceed” its existing three-year target of 10%-15% revenue growth by 30 June 2025 (the end of its current financial year).

This business has a strong share in the UK healthcare market and a long history of growth, supported by its proprietary disinfectant formula. Tristel is now hoping to gain a foothold in the US market, having gained FDA approval for some of its core products.

Megan took a closer look at Tristel in the latest Week Ahead article, which is worth reading for a broader view on this interesting business. She highlights the scale of the opportunity and the challenges involved in US expansion for small UK companies. Today’s AGM Statement alludes to this, warning that US sales growth has been below expectations:

This is primarily due to the stringent purchasing bureaucracy of signing up new healthcare accounts, alongside the time taken to train sales reps with the Company's longstanding partner Parker Laboratories.

On a more positive note, US customer feedback is said to be “encouraging” and the company’s sales pipeline “remains robust”.

Tristel will publish its interim results on 24 February 2025, when I imagine more detailed information on trading may be provided.

Roland’s view

If Tristel’s US expansion is successful, this business could be worth significantly more in the future. Unfortunately, I don’t see any way to predict how likely this might be.

However, a weak share price performance and the introduction of a more generous dividend policy have left this highly-profitable business looking more attractively valued than previously:

I think the current valuation is largely supported by the existing business, with the US offering potential long-term upside. On this basis, I’m happy to maintain Megan’s GREEN view.

Graham's Section

Duke Capital (LON:DUKE)

Up 3% to 30p (£153m, 510 million shares outstanding) - Interim Results - Graham - AMBER/GREEN

I downgraded my stance on this last month after the company raised funds at 27.5p, which I considered to be a disappointing price at which to raise new equity.

They had last raised at 35p in 2022.

Today’s interim results show 4% growth in H1 recurring cash revenue, up to £12.7m.

A dividend of 0.7p has been paid per quarter, entirely flat at this level since March 2022 and in truth this hasn’t changed much since early 2019 (0.67p).

With £15m of capital deployed in H1 into “follow-on” investments, Duke argues that there has been “an increase in the maturity and profitability of the underlying portfolio”, and that this will result in higher EBITDA multiples upon exit.

New funding strategy: Duke outlines a fundamentally new approach to its strategy.

Building on the strategic review we undertook in the last financial year, we have been developing a long-term funding strategy which is not reliant on raising equity via the UK public equity markets…

…the time is right to move towards a third-party capital model and as such, we intend to raise future additional capital via new Managed Account / Joint Venture structures. The clear benefits of this strategy will be to eliminate cash drag, deliver accretive fee-based revenue and reduce Duke's dependence on the UK public equity markets, thereby minimising dilution and enabling us to execute on strategic growth opportunities more rapidly and at scale. With this in mind, during the period, Duke engaged a placement agent to approach potential capital providers and, as previously announced, has received indicative term sheets from Tier-1 capital providers on potential new funding, with further term sheets expected.

Outlook: they maintain “a positive outlook for the months ahead, albeit we recognise the need for caution in relation to the UK economy”.

Graham’s view

Firstly in terms of valuation, the market cap at the new, higher share count I calculate to be £153m, which is not far off balance sheet equity of £162m.

The bigger question today is around the implications of the new strategy.

I’m impressed that the company has decided to stop relying on the UK equity market for funding. I always knew that they were ambitious to raise funds but it has been clear in recent years that the price at which funds might be available has not been very attractive, and the quantity of funds available has probably not been attractive either.

I give credit to them for saying that the decision to raise funds recently “was not taken lightly and reflected the near-term investment opportunities” within their existing portfolio. It’s clear now that raising equity at that sort of price is not the plan going forward.

If Duke evolves into a sort of private equity fund manager, largely managing 3rd party funds, this is something I could support. Readers will know that I like fund managers with a niche, and Duke’s mortgage-style funding product for medium-sized businesses could certainly be considered niche!

The new plan is still in its infancy, however. Term sheets are really just proposals and negotiating tools. We’ll have to see what comes of the term sheets received so far by Duke. But I do think that the new plan has some interesting potential, and I remain comfortable with a mildly positive stance on this one.

XLMedia (LON:XLM)

Down 24% to 9.45p (£25m / $32m) - Update on distributions to shareholders - Graham - AMBER

This is a special situation as cash is being distributed to shareholders with the only questions left being “how much?” and “when?”

In October I did some calculations and estimated that XLM would get a cash balance of at least $52.5m (£41m), before various costs and ongoing cash drain, and before discounting for certain risks. I suggested at the time that a c. $50m (£39.5m) market cap might be fair, and took a neutral stance.

Unfortunately, the company has announced today that it is only expecting to have about $40m (£32m) of available cash “after taking account of reasonably expected costs and liabilities and expected further receipts”, including deferred consideration and earn-outs from its disposals.

What has gone wrong? Firstly, cash at the end of October 2024 was only $17.7m.

This is despite the company starting with $19m at the end of June, and receiving $10m during October for its European disposal.

The only major payment I was expecting was a $4m outflow for a prior acquisition.

My conclusion is that the North American business must have been burning cash very rapidly in the period before it was sold, and/or that the costs of selling it must have snowballed.

Inflows due after October:

$20m initial payment for North American business (already received)

April 2025: $7.5m deferred payment for European business

Earnouts: only $3-5m is now estimated in earnouts, out of a possible $15m. The amounts will be finalised in late Q1 2025 and payable in April 2025.

This gives a gross cash figure of $48-50m, before costs.

Today we get an estimate of winding-down costs and they are huge: $11-13m. The amount of tax due is yet to be finalised.

That leaves a range for cash available of $35-49m. XLM’s market cap has moved to 10% below the bottom of this range, which I think is reasonable.

Graham’s view: it turns out that I was too optimistic with my initial calculations, but I’m glad that I stuck with a neutral stance as voluntary liquidation events like this are unpredictable and I have noticed that I am often surprised by the amount of costs they incur while trying to sell down or shutter their businesses.

XLM shareholders can look forward to a £16m/$20m tender offer, and hopefully another one in the middle of next year. But there’s no getting away from the fact that the company has again failed to live up to investor expectations. Shareholders might be glad to see the back of this one at last.

Videndum (LON:VID)

Down 18% to 210p (£197m) - Pre-Close Trading Update - Graham - RED

I was RED on this in September due to concerns over its indebtedness.

That problem continues today with the following trading update:

The recovery in our markets continues to be slower than expected, but we are seeing some signs of gradual improvement, which we believe will benefit trading in H1 FY25.

FY24 Revenue: now forecast at £280m, this compares with £307m last year and a £315m forecast on the StockReport.

Profitability: breakeven in terms of adj. continuing operating profit, but that’s before the impact of several items including a £25m write-off (impairment) of stock and intangibles.

The write-off is described as “non-cash” but if the company is writing down stock then the impact on cash flow is pretty clear: the company expects to make a loss on inventories that it previously intended to sell for profit.

There’s also a £10m charge for restructuring costs associated with a savings programme.

Net debt is expected to close the year at £135m, of which £30m are leases.

This is a major deterioration compared to June 2024, when net debt was £117m including leases.

Covenants: the leverage covenant for Dec 2024 moves to 5.5x EBITDA. The interest covenant moves too, and the March 2025 tests are also relaxed.

I think 3.25x is the “normal” leverage covenant here.

When things were really stressed in early 2024, VID’s banking syndicate moved it up 4.25x.

If they are now moving it up to 5.5x, I doubt the banks are at all relaxed about this. This is far beyond a level that banks are typically comfortable with.

The interest covenant (EBITDA/net interest) has also moved to an extremely loose level. The company is only required to earn an EBITDA of 1.25x its interest bill.

These will be interesting discussions:

Our Revolving Credit Facility is set to expire in August 2026. We are actively working with our lending banks to secure an extension or a refinancing during H1 2025, in addition to addressing necessary amendments to the February and March 2025 covenants. An update will be provided in Q1 2025.

The Executive Chairman seems to blame former management even more than he blames market conditions:

Since assuming my expanded role, I have seen significant opportunities within the business. However, it has to be recognised that there are areas where management processes, cost discipline, and contractual and commercial acumen require strengthening. These challenges were exacerbated in some areas by challenging market conditions. The new management team has identified the issues and is addressing them at pace.

Graham’s view

VID is now doing what distressed companies do: reducing discretionary spend, merging divisions, and cutting costs wherever possible. And its prices are going up in an attempt to improve margins.

With the bank temporarily allowing the leverage covenant to go to 5.5x, as demand seems to be very soft, I have no choice whatsoever but to keep this on RED. I think this company needs to raise more equity and that they should have done it yesterday.

But they already raised £125m of fresh equity a year ago, at 267p, in a move that was supposed to fix the balance sheet. So I also can't blame shareholders if they are reluctant to pour any more money into this. A dire situation.

Roland's Section

Filtronic (LON:FTC)

Up 4% to 75p (£163m) - Trading update - Roland - AMBER

Today’s half-year trading update is short but sweet for shareholders in this electronics business, whose biggest customer is Elon Musk’s SpaceX (Filtronic provides radio equipment used to link Starlink ground stations with its low-earth orbit satellites):

the Board now expects to deliver stronger results for the full year than current market expectations

Filtronic shares have already tripled this year. As I’m writing shortly after 8am, the shares are up a further 4%.

We last covered this electronics group on 31 October when the company included an “in line” update with its AGM Statement. So I think it’s interesting to try to deduce what might have changed in the relatively short period since then.

Today’s statement is truly very short. Here are the main points:

H1 trading: “significant growth in revenue and profits” for the six months ended 30 November 2024.

H2 trading: the company says customer demand is robust, with “the second half benefitting from pull-forward of customer orders”. Results for the year ending May 25 are now expected to be ahead of current market expectations.

If H2 performance will benefit from orders being pulled forward, this raises the risk that the subsequent H1 could suffer unless Filtronic can secure significant new contracts. We’ve seen this with Solid State recently.

Outlook: no upgraded guidance is included in today’s trading update, but fortunately we have an updated note from house broker Cavendish - many thanks.

Cavendish’s analysts have upgraded their FY25 earnings forecasts by 25% to 4p per share, but have left FY26 forecasts unchanged at 3p per share.

These estimates seem to reflect the risk I’ve suggested above that Filtronics profits could fall next year, unless the company wins significant additional new business to offset the pull-forward of orders into the current year.

Based on a share price of 75p at the time of writing, these estimates put Filtronic on a FY25 P/E of 19, rising to a P/E of 25 next year.

Roland’s view

It’s still quite early in the company’s second half. Filtronic has shown strong momentum over the last year with some significant additional orders for power amplifier modules from SpaceX.

I would not rule out the possibility of the company maintaining this momentum to support further profit growth in FY26, but there’s no visibility on this at present.

I’m also encouraged by the evidence of operating leverage in the company’s financials as it’s grown over the last year - profitability has improved significantly:

I’m broadly positive on the medium-term outlook for this business. But I think it’s fair to say that a reasonable amount of growth is already in the price at current levels. I am going to maintain our AMBER stance on this high flyer.

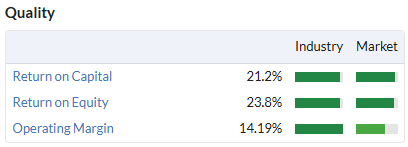

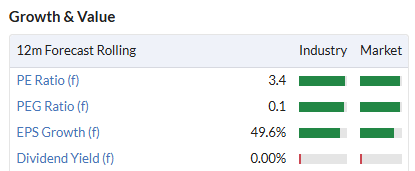

Saga (LON:SAGA)

Up 6% to 131p (£187m) - Saga and Ageas agree new insurance partnership - Roland - AMBER

Today we have confirmation of a partnership agreement between Saga and Belgian insurance group Ageas. This was first mooted back in October, when Paul covered the original announcement.

Saga shares have risen on today’s news, but we should probably remember that they were trading on an abnormally low forward P/E of 3.4 before the market opened.

Having read through the details of the partnership, my feeling is that shareholders should not necessarily expect any immediate benefit. While a lot of cash is changing hands, I don’t think it will leave Saga with any surplus distributable cash.

Partnership structure: today’s agreement applies to home and motor insurance. Saga will sell its underwriting business to Ageas and enter into “The Affinity Partnership” – a 20-year deal with Ageas to sell home and motor insurance.

Saga will retain responsibility for the brand and direct marketing, while Ageas will take on price comparison website distribution, pricing, underwriting, claims and customer service.

Financials

Saga appears to be in line to receive significant cash consideration, relative to its sub-£200m market cap.

Underwriting sale: Saga will receive £65m from the sale of its underwriting business (AICL) to Ageas, plus a further £2.5m when operational readiness is achieved = £67.5m

Partnership consideration: Saga will receive “upfront consideration” of £80 million in two tranches.

The company will also receive contingent consideration of up to £30m in 2026 and the same again in 2032, subject to certain volume and profitability targets being met.

Saga will also receive commission payments based on an undisclosed percentage of the Gross Written Premiums generated over the term of the partnership.

My sums suggest the total consideration received by Saga as a result of this transaction could be £207.5m, plus commission.

However, these payments will be subject to the company’s accounts achieving a clean auditor report in July 2025 and to Saga securing refinancing for its £250m July 2026 corporate bond and for the £85m loan facility held with chairman Roger De Haan, which matures in April 2026.

I think this is a useful reminder of the relatively leveraged nature of this business. Saga also has c.£375m of secured cruise ship loans, on which the company is currently benefiting from relaxed covenants and deferred payments.

Use of proceeds: Warren Buffett’s vast investment empire has been built with the help of the huge pool of ‘float’ generated by his insurance businesses. That is, premium payments received upfront, ahead of any possible claims or payments to underwriters.

Today we see the impact of this business model when it’s reversed (my bold):

“Proceeds from the Affinity Partnership will principally be used to offset the working capital impact associated with the transition to the Affinity Partnership. SSL has historically benefited from a favourable working capital profile. This arises from customers making largely annual payments at the start of their insurance policy, which in the case of motor and home are then remitted to panel underwriters between 30 and 90 days later.”

In other words, while Saga expects to receive up to £140m in partnership consideration payments, this inflow will broadly be offset by working capital outflows as the company will no longer receive premium payments.

Arguably, the only real upfront outlay being made by Ageas is the £65m spent on acquiring Saga’s underwriting unit, AICL.

Of this, Saga’s management plans to hand back £22m to Ageas to gain control of the “the Enbrook Park property”, which is currently owned by AICL. This 27-acre site is Saga’s former corporate headquarters. It closed last year but according to the internet, is now rumoured to be lined up for a housing development.

The remaining £43m from the AICL sale is expected to be used for debt reduction and other general corporate purposes.

Impact on earnings: while costs will fall as a result of the partnership, Saga’s future income from home and motor insurance sales will be limited to an undisclosed level of commission.

The company will also forgo the profit from the AICL underwriting business. This business made an after-tax loss of £9.6m last year, but recovered to a profit of £13.4m during the six months to 31 July 2024. Ageas appears to be buying AICL at a point where cyclical conditions are improving.

Finally, Saga also expects to incur “one-off transition costs” of c.£25m. I’d imagine most of these will be cash costs, so they could absorb around half the remaining £43m surplus from the AICL sales.

Outlook: I don’t have access to any broker updates, but the company has provided some updated guidance today:

As a result of the above changes to revenues and costs during the Transition Period, SSL's underlying profit before tax is expected to fall in 2025/26 and then partially recover in 2026/27, before recovering to or exceeding 2024/25 profitability in the first full financial year following achievement of SSL's run-rate cost base under the Affinity Partnership.

For comparison, consensus forecasts prior to today suggested the following progression of underlying earnings:

FY24 actual: 30p per share

FY25e: 26.6p per share

FY26e: 37.6p per share

We’ll have to see how these forecasts change over the coming days/weeks.

Roland’s view

Saga already sells travel insurance and private healthcare through partnership arrangements. Today’s deal will complete the transition of the group’s insurance business to a capital light, marketing-focused operation.

Alongside this, the group will continue to operate its cruise ship and travel business.

My feeling is that the overall financial impact of transactions announced today will be broadly neutral over the next few years.

In particular, I think it’s disappointing that there doesn’t seem to be any clear path for accelerated debt reduction.

Saga shares remain deeply depressed and could be trading at bargain levels, on a P/E of 4.

As far as I can see, the current consensus forecast for this year is likely to be underpinned by the cruise and travel business – this segment generated £54m of pre-tax profit over the 12 months to 31 July 2024.

However, I can’t ignore the debt risks here. Saga’s net financial debt was over £600m at the end of July 2024. H1 cash interest payments totalled £20m.

The completion of today’s transactions is also dependent on successful refinancing, perhaps a little earlier than might otherwise have been required.

On balance, I don’t feel I can take a strong view here without at least seeing Saga’s next full-year accounts and updated broker forecasts. I’m staying neutral for now. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.