Good morning!

At 7am today we have the UK unemployment rate, which is expected to come in at 4.3%, same as last time. [Update: unemployment remains at 4.3%, as expected.]

It’s a remarkable feature of the economy that unemployment has been at a level that many would consider to be “full employment”, at the same time as consumers have felt as if they are being squeezed.

According to the economics I learned, full employment happened when the unemployment rate was around 4%, which is more or less where the UK has been for the last several years:

A concern that often accompanies this discussion is that there are too many people outside of the workforce, i.e. that the total employment rate is too low.

However, the employment rate has risen over the past 10 years, and is nearly flat over the past 3 years.

The economy might have problems, but too many people out of work isn’t one of them!

Then this afternoon at 13:30, we’ll have US retail sales which are expected to grow by 0.5% month-on-month, a slight improvement on the 0.4% growth rate recorded last month. These figures are seasonally adjusted.

A level of growth of this size tends to be reported as “solid” or “steady” and is considered to be consistent with consumer-driven GDP growth.

The most recent US GDP estimate (for Q3) was a year-on-year growth rate of 2.8%. Donald Trump takes office again in less than 5 weeks, with a mission to boost the economy. As this is his second time at the wheel, perhaps there won't be too many surprises?

12.15pm. We've wrapped up the report for today! Cheers.

Explanatory notes

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day. We usually avoid the smallest, and most speculative companies, although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We have a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Add your own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing. Links:

Daily Stock Market Report: records from 5/11/2024 (format: Google Sheet). Updated to 10/12/2024.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Bunzl (LON:BNZL) (£11.9bn) | Trading Statement | 2024 rev exps +3% at const currency. Op margin “strong” and above 2023. | |

Chemring (LON:CHG) (£985m) | Final Results | FY24 adj op profit +3% to £71.1m. Margins lower and order intake -11% to £672.8m. FY25 in line. | AMBER (Graham) |

Hollywood Bowl (LON:BOWL) (£572m) | Final Results | Adj. EBITDA ahead of exps. PBT falls due to impairment. 2025 has started well, positive outlook. | AMBER/GREEN (Graham) |

Goodwin (LON:GDWN) (£507m) | Half-year Report | “Trading profit” up over 50% to £17.1m. Similar level of activity expected for H2. Net debt £39m. | AMBER (Roland) |

Frp Advisory (LON:FRP) (£396m) | Half-year Report | Revs up 32% to £77.6m, PBT +55% to £17.8m. Outlook positive, FY25 trading in line. | GREEN (Graham) |

Capita (LON:CPI) (£295m) | Trading and Operating update | 2024 profit guidance unchanged. YTD adj rev -8%, but £140m of cost savings achieved. | AMBER/GREEN (Roland) |

Netcall (LON:NET) (£168m) | AGM statement | FY25 trading is in line. | |

Gulf Marine Services (LON:GMS) (£162m) | Update to 2024 and 2025 EBITDA guidance | Guidance upgraded: 2024 EBITDA “at upper end”, 2025 EBITDA now exp. $100-108m | GREEN (Roland) |

Journeo (LON:JNEO) (£46m) | Contract Extension | 4-year extension with Edinburgh Council. £1.5m/year. No reference to impact on earnings exps. | |

GSTechnologies (LON:GST) (£37m) | Interim Results | Revenue up 760% to $2.23m, losses reduced. “Well positioned” for future. | |

Sutton Harbour (LON:SUH) (£11m) | Half-year Report | GP down 18% to £1.3m due to fish auction closure. NAVps stable at 37.3p but gearing higher at 51%. |

Summaries

Gulf Marine Services (LON:GMS) - up 3.8% to 15.6p (£168m) - Update to 24/25 EBITDA guidance - Roland - GREEN

Today’s update from this offshore support vessel operator confirms that recent contract awards have fed through to upgraded adjusted EBITDA guidance for 2024 and 2025. While I can see risks in the medium-term, the near-term outlook and valuation continue to look positive to me.

Frp Advisory (LON:FRP) - down 3% to 150p (£385m) - Half-year Report - Graham - GREEN

FRP are confident of achieving market expectations which is not surprising not given that they have already achieved well over 50% of the full-year estimates. However, H1 benefited from the administration of The Body Shop plus another large project, so H2 might be quieter. I remain positive on this one due to strong organic growth and an acquisition strategy that appears to be working.

Capita (LON:CPI) - down 8% to 16p (£274m) - Trading and operating update - Roland - AMBER/GREEN

Today’s update from this outsourcing company appears to be a mild downgrade. However, Capita does appear to be making tangible progress with its AI-led strategy and its shares could be cheap. Given this year’s improvement to the balance sheet, I’m prepared to take a mildly positive view ahead of the company’s next set of results.

Goodwin (LON:GDWN) - up 9.5% to 7,408p (£555m) - Half-year Report - Roland - AMBER

Strong results from this high-tech British engineering group have provided a boost to the share price. Profit margins and cash generation have both improved and the outlook appears positive. However, the steep valuation and lack of forecasts mean this complex business needs further research, in my view.

Hollywood Bowl (LON:BOWL) - down 7.5% to 308.6p (£531m) - Final Results - Graham - AMBER/GREEN

Another good set of results with the company keeping prices low and still generating a chunky profit (both on an adjusted and a statutory basis). The roll-out continues and I still have a positive overall impression of BOWL, but I do take our stance down a notch due to weak like-for-likes.

Short Sections

Chemring (LON:CHG) - down 11% to 323p (£880m) - Results for the year ended October 2024 - Graham - AMBER

I don’t think I’m the only one who is surprised to see the Chemring share price down by over 10% today, when the outlook for 2025 is clearly stated to be in line with market expectations. The simplest post hoc explanation is that the share was rated too highly at 18x forecast earnings - above what might typically be expected in the defence sector - and that investor hopes were therefore a little higher than official forecast.

There is not much wrong with the headline numbers: revenue +9% (£510m), underlying operating profit +4% (£71m), and statutory operating profit +28% (£58m). The company does now carry some net debt (£53m) but it’s much less than 1x EBITDA and therefore should be easily manageable. Order intake fell by c. 10% but new orders were still strong enough to push the order book over the symbolic £1 billion milestone.

If I was nitpicking, I would highlight that the FY25 revenue forecast is only 77% covered by the order book (last year: 79%), despite the much larger order book. So perhaps there is a slightly higher risk of FY25 revenue failing to hit the £535m forecast. On top of that, the company has guided for another heavy H2 weighting in FY25 (H2 of FY24 generated 56% of full-year revenues and over 60% of full-year underlying EBITDA).

Market conditions provide a tailwind as “the threat environment remains increasingly complex, with heightened geopolitical tension and risks of global conflict”. Chemring’s wide variety of products - including sensors, countermeasures, signals intelligence systems, and decoys - seems certain to remain in high demand. However, the shares may have got ahead of themselves at this high PER, given that performance here is rarely smooth.

Graham's Section

Frp Advisory (LON:FRP)

Down 3% to 150p (£385m) - Half-year Report - Graham - GREEN

FRP Advisory Group plc, a leading national specialist business advisory firm, announces its half year results for the six months ended 31 October 2024 ("H1 2025").

Today’s results table from FRP is full of excellent growth rates:

Impressively, 23% of the revenue growth is organic, while only 9% was acquired. We mentioned this at the time of the H1 trading update in November.

But watch out: a few large projects helped to boost organic growth, including The Body Shop, and so we might not be able to rely on projects of this size repeating:

Organic growth was driven by confidential advisory mandates (not formal appointments), and complex restructuring projects. It also included a strong contribution from the Body Shop and a large Corporate Finance project.

Net cash only grows by a few million pounds to £13m. I presume that acquisition spending prevented it from growing any faster than this - and the cash flow statement quickly confirms this, with £10.6m spent on acquisitions during H1.

Each of the FRP’s “pillars” seems busy: Restructuring, Corporate Finance (including Debt Advisory), Forensic Services and Financial Advisory.

Strangely, in Restructuring, FRP’s market share of administrations has fallen from 15% to 12%. But they say that colleague utilisation is up due to all the work they are doing on confidential advisory projects rather than formal appointments.

Outlook: in line.

The Board remains confident of achieving current market expectations for the full year*, assuming current activity levels continue.

Market expectations: revenue of £146.7m, adj. EBITDA £39.5m.

CEO comment:

We continue to strengthen the Group through acquisitions, with four completed across three of our service pillars. We also recently opened a new office in Belfast, Northern Ireland. Developing talent and managing succession is a key focus of the Group. In H1 we were pleased to promote seven colleagues to Partner, along with three more lateral hire Partners.

Graham’s view

I’ve been GREEN on this one, despite it being in a sector that I tend to avoid - professional services.

Going over some of the bull points I mentioned last time:

Valuation. It continues to trade at a PER of about 14x.

Balance sheet. This is still fine with tangible NAV of £59m and a positive net cash position.

There are a few items on the balance sheet that might be worth keeping an eye on. The value of receivables outstanding for more than 30 days has increased steadily and is now almost £5m. And the value of unbilled revenue - work done but not yet invoiced to the customer - has soared from £54m (April 2024) to £66m (Oct 2024).

These items can be expected to grow as the company grows, but they do tie up a lot of working capital. So it’s important that FRP continues to maintain a healthy net cash balance.

As I noted last time, FRP has already achieved more than 50% of its full-year expectations in H1. A note from Cavendish this morning suggests that 56% of the full-year EBITDA forecast has been made already.

However, both the company and Cavendish are leaving forecasts unchanged today. This may help to explain why the shares are a little lower, as some people might have pencilled in an upgrade.

With conditions remaining favourable for restructuring work, I’m optimistic that some more very large projects might fall into FRP’s lap, but I don’t think the investment case is totally reliant on that happening. Expectations for H2 are very modest so hopefully there is still a good chance of an earnings beat by year-end.

Hollywood Bowl (LON:BOWL)

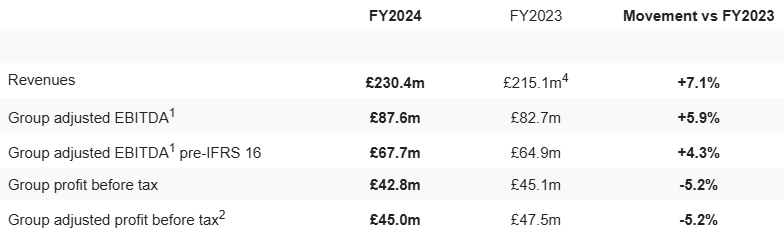

Down 7.5% to 308.6p (£531m) - Final Results - Graham - AMBER/GREEN

Revenues and EBITDA have moved in the right direction, but PBT has gone into reverse for “the UK and Canada’s largest ten-pin bowling operator”:

As noted by Paul last time, there isn’t much going on in terms of like-for-like revenue growth, which comes in at +0.2%.

Adjusted EBITDA of £67.7m is ahead of expectations: we knew from the corresponding trading update that this would be in excess of £65m.

Dividends for the year add up to 12.05p. Last year benefited from a special dividend, so that total dividends last year added up to 14.54p.

Estate - compared to last year, there are two new UK centres. UK total: 72. In Canada there are now 13 centres, an increase of 4 compared to last year.

The results “highlights” could be more helpful if they clearly outlined the net change to the estate, including closures.

Net cash finishes the year at £29m.

Higher NI contributions will cost £1.2m annually from April 2025.

Outlook

High demand for competitive socialising and strong appeal of bowling as a family-friendly activity with Hollywood Bowl the lowest cost option of the major UK ten-pin bowling operators

Group trading performance has started well in FY2025 and we remain positive about our future prospects

Maintaining our well-invested estate with ten refurbishments planned across the UK and Canada in FY2025

Expect to open at least four additional centres in the UK and two in Canada by the end of FY2025

On track to meet target of 130 centres by 2035

Graham’s view

I like BOWL’s position as the lowest-cost option among bowling operators - that must have been a great help during the economic conditions of the past years.

The average bowling price for an adult during FY24 was £7.15, or £6.21 for children. BOWL says that in real terms, their bowling price was cheaper in FY24 than it was in FY23.

The only problem with that from an investment point of view is the lack of LfL revenue growth and, in turn, the lack of PBT growth for the year.

The CFO does note that adj. PBT, adding back impairments, was £50.3m which was a slight improvement on the previous year.

Actual PBT for FY24, without any adjustments, was £42.8m. The adjustments strike me as being reasonable.

My impression is that the company decided the level of PBT generated last year was “good enough” and that they could afford to keep prices low for customers in FY24 while still generating enough profits to fund their various refurbishments and expansion activities.

However, I would have liked to see low prices accompanied by stronger visitor numbers, so that LfL revenue might still have improved.

It might be a little harsh but I’m going to downgrade this to AMBER/GREEN primarily because of the lack of underlying growth. Hopefully my caution will be proven wrong by BOWL's continued successful expansion.

The share price has stalled this year as we wait to see the next phase of growth:

Roland's Section

Gulf Marine Services (LON:GMS)

Up 3.8% to 15.6p (£168m) - Update to 24/25 EBITDA guidance - Roland - GREEN

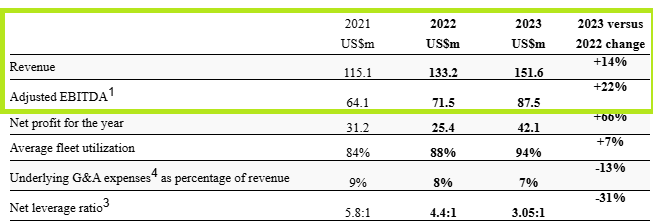

Recent weeks have seen GMS report a number of contract awards (e.g. here and here) for this offshore support vessel operator. This positive momentum now appears to be feeding through to profit guidance, as the company has updated its forecasts for 2024 and 2025 today, albeit only for adjusted EBITDA.

2024 adjusted EBITDA is now expected to be at the upper end of previous guidance of $98m - $100m. This is already a narrow range as I’d expect at this late stage in the year and represents an increase of c.14% from the $87.5m reported last year.

That’s a slightly reduced rate of growth compared to last year, but still extends a decent progression since 2021:

Today’s updated guidance for 2025 means this progress is now expected to continue for at least one further year.

For 2025, GMS expects adjusted EBITDA to reach USD 100-108 million, an increase from the previously forecasted 2025 EBITDA guidance of USD 92-100 million.

Trading summary: executive chairman Mansour Al Alami says GMS is seeing “strong demand” and that today’s upgraded forecasts are supported by “forecasted utilization rates and contracted daily charter rates”.

I assume this means these operational metrics are running ahead of previous expectations, extending the trend shown in the table above.

Outlook: adjusted EBITDA includes many real costs for a business of this kind, including depreciation of expensive capital assets and hefty interest payments.

Unfortunately GMS does not provide any pre-tax profit or earnings guidance. But an initiation note from Greenwood Capital Partners (many thanks) is available on Research Tree today.

Greenwood estimates 2024 earnings of 3 cents per share, rising to 3.7 cents per share in 2025.

Interestingly, this 2025 estimate is lower than the 4 cents per share consensus estimate currently shown on Stockopedia, which I believe is likely to have been derived from previous forecasts by Zeus and Panmure Liberum.

Roland’s view

It’s not clear to me if today’s upgraded adjusted EBITDA guidance will drop down to increase adjusted earnings and – most importantly – free cash flow. However, the GMS story remains on track as far as I can tell, with leverage falling and demand improving for the company’s assets.

I think the metrics in the table I’ve included above tell the story here – this is a cyclical story that’s still in a positive phase. At some point I’d expect conditions to turn, but I have no idea when this might be.

A secondary risk for me is that at some point, GMS may begin another fleet refresh/expansion spending cycle.

For now, GMS shares continue to trade at a discount of c.40% to book value, on a low single-digit earnings multiple.

With the balance sheet looking increasingly secure, I’m going to maintain my GREEN view of this stock ahead of a more detailed review when the 2024 results are published.

Capita (LON:CPI)

Down 8% to 16p (£274m) - Trading and operating update - Roland - AMBER/GREEN

Over the last decade, outsourcing and business process services group Capita has been a painful example of a turnaround that has refused to turn.

Today’s trading update is written in positive language, but appears to include a cut to 2024 revenue guidance and (possibly) a downgrade to 2025 profit guidance.

2024: in August’s half-year results, Capita guided for adjusted revenue to fall by “low to mid-single digit percentage”.

Today’s update increases the scale of the expected fall to “high single digit adjusted revenue decline”. Both figures exclude the impact of disposals.

Revenue for the 11 months to 30 November fell by 8% on an adjusted basis, consistent with this new guidance. The drop in revenue appears to have been driven by a slowdown in the group’s Experience business (outsourced call centres) and its regulated services division, which includes closed book life insurance and pension administration.

Despite this, adjusted operating profit guidance for 2024 is unchanged, thanks to cost cutting. Capita says it has achieved £140m of annualised savings so far this year, from a target of £160m.

Checking back to last year’s results, Capita’s 2023 adjusted operating margin was 4%.

Guidance is for this rate to increase by 0.5% this year, so if I apply a rate of 4.5% to consensus revenue forecasts of £2,454m I can estimate an adjusted operating profit of £110m for 2024.

Comparing this to Capita’s enterprise value of £833m gives an EBIT/EV yield of 13%, which I would often see as cheap. However, I would take a cautious view on this adjusted figure, given that free cash flow is now expected to remain negative until late in 2025.

2025: Capita says that the increase in National Insurance costs next year will cost £16m, or £20m annualised. This is expected to be offset by further cost saving and management are now guiding for “modest profit growth” and “further margin improvement” next year.

Without access to broker notes, it’s hard for me to be certain if this represents a cut to guidance. However, I’m leading towards this view given that previous consensus estimates on Stockopedia were forecasting 32% earnings growth in 2025. I would not describe this as “modest”.

AI-driven cost savings?

Much of Capita’s business involves running outsourced call centres and similar services for local government customers. The company says that it’s having success rolling out AI services and sees “significant opportunities” to continue developing these.

The use of AI is already enabling us to deliver significant productivity and service quality improvements for our early adopting Contact Centre and Local Government customers, where those early clients have seen average handling time reductions of around 20%.

As a result of its experience so far, Capita now believes it can extend its cost savings target from £160m to £250m.

Much of this is being supported by a reduction in headcount. Remarkably (in my view), Capita says that “voluntary employee attrition” is running at around 21%. I’m not sure what this says about the experience of the company’s employees.

However, embedding these further cost savings won’t come cheaply. The cost saving programme is expected to have a cash cost of around £50m in both 2024 and 2025. This will delay the return of positive free cash flow until “the end of 2025”.

Roland’s view

Capita appears to believe the business has the scale and expertise to become a leading supplier of AI-driven services, and perhaps it can do this.

I believe we are in a transition period in terms of the commercial application of AI, and I expect to see some winners among companies who are able to provide scaled, quality solutions for clients.

As Paul reported in July, a disposal has strengthened Capita’s balance sheet, allowing the company to reduce its debt to a safer level.

If newish CEO Adolfo Hernandez can deliver on his expectations of “positive and consistent free cash flow from the end of 2025”, then I think that the stock’s forecast P/E of six could offer some opportunity.

However, I’m a little concerned that today’s update represents the latest in a series of nibbling downgrades that have seen profit expectations fall significantly this year:

On balance, I’m going to go AMBER/GREEN here, ahead of the 2024 results.

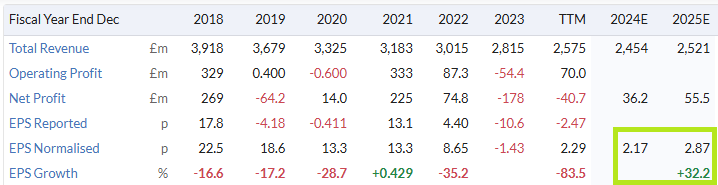

Goodwin (LON:GDWN)

Up 9.5% to 7,408p (£555m) - Half-year Report - Roland - AMBER

I am delighted to report that the "trading" pre-tax profit for the Group for the six-month period ending 31st October 2024 was £17.1 million, representing a 53% increase in profitability versus the same period last year.

Today’s results from this family-controlled FTSE 250 engineering group have received a warm reception from the market. A period of heavy capex appears to be starting to deliver results, supporting debt reduction and an increase in profits.

Half-year summary: Goodwin shuns broker forecasts and its market updates tend to be brief and mercifully free of PR fluff.

In today’s results, chairman T.J.W. Goodwin highlights reports that revenue rose by 9% to £106.4m, supporting a 45.6% increase in operating profit to £18.2m. This highlights a creditable increase in operating margins to 17.1% (HY 24: 12.8%).

Capex slowed to £5.3m during the half year (HY 24: £7m) and Goodwin says that cash generation improved, supporting a reduction in net debt to £38.8m (HY 24: £54.6m).

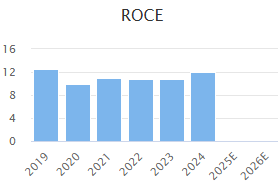

My sums suggest a trailing 12-month return on capital employed (ROCE) of 15.9%, a credible figure that shows continued improvement on performance in recent years:

Trading commentary: most of the company’s businesses appear to be trading well, with an order book of £296m on 16 December, up from £266m in December 2023. This compares to a figure of £175m in August 2022, highlighting continued progress.

Goodwin flags up a number of particular highlights from trading performance, including:

Nuclear: a contract to supply 29 tonne self shielding boxes has started to ramp up in the company’s foundry

Duvelco Ltd: a “significant milestone” has been reached with the industrial-scale production of polyimide resin in a new bespoke facility.

Easat Radar Systems: “long-promised future growth” is now coming to fruition with orders for radar systems to air force customers in Southeast Asia

Refractory Engineering: “a stable level of profitability” from core products with potential growth in newer areas including AVD, a “fire extinguishing agent for lithium ion battery fires”.

I think this sample of Goodwin’s activities provides an indication of the breadth and technical complexity of its product range and capabilities.

It’s beyond the scope of this report for me to try to evaluate the growth potential of such businesses, but I think it’s fair to say the group benefits from significant intellectual property and differentiated manufacturing capabilities.

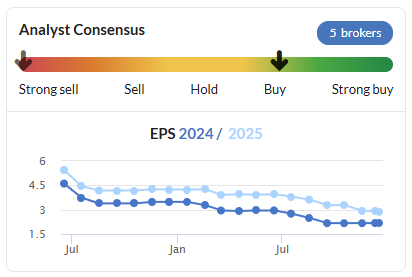

Outlook: although Goodwin is covered by broker Shore Capital, the company chooses not to provide forecasts to the market. So we do not have any earnings estimates for Goodwin.

Today’s results commentary indicates that “a similar level of activity for the Group” is expected for the second half of the current year, which ends on 30 April 2025.

If I assume that activity levels will be correlated with profits, then this might suggest full-year earnings of 300p per share (FY24: 224.5p).

Based on my guesstimate, Goodwin shares could be trading on a current year forecast P/E of c.25 after today’s gains, with a dividend yield just under 2%.

Roland’s view

Goodwin tends to score well on some of the quality and cash flow metrics I like to use and has often caught my eye.

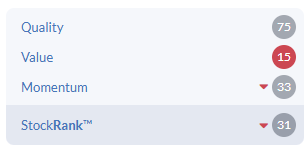

However, the seemingly full valuation has always been a sticking point for me. Paired with the lack of forecasts, this means that the shares also score poorly with the StockRanks:

I would guess that this StockRank score is likely to improve somewhat when Goodwin’s latest numbers are digested by Stockopedia’s algorithms.

It’s also worth noting that on a long-term view, Goodwin has created terrific value for shareholders.

Goodwin’s founding family own more than 50% of the company’s shares and are presumably unlikely to sell. So the company doesn’t need to spend too much time marketing its investment proposition to outside investors. Hence the lack of forecasts.

As a result, I’d argue this is only likely to be of interest to investors who are able to do in-depth research of their own to understand the valuation and outlook.

I suspect that this business could continue to generate attractive returns for long-term shareholders. But the lack of visibility and steep price tag means that I cannot be too positive after a brief review. On balance, I’m going to maintain our previous neutral stance of AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.