Good morning! We've finished this report at 1am, cheers!

US Federal Reserve/Interest Rate news

The FTSE 100 is lower by 1% this morning, and AIM is down similarly after a “hawkish cut” by the Federal Reserve. The Dow Jones is down by 1,100 points or 2.5%.

The rate cut to 4.25% - 4.5% was anticipated, but it was accompanied by hawkish language and forecasts.

Below I have given the “dot plots” published by the Fed’s decision-making committee. These show where members believe the federal fund rates should be in 2025.

First we have the situation back in September. The plot goes from 2% at the bottom to 5% at the top, with each dark line representing a 1% change.

You can see that only one member thought that the federal funds rates should be over 4% in 2025, and two thought it should be less than 3%:

Yesterday, this was updated and became:

Now there are four members who think it should be over 4%, and none think it should be less than 3%. Most members now believe that the rate should be just below 4%.

The result is that markets are now pricing in only two rate cuts in 2025, for a total cut of 0.5%.

Markets were previously expecting four rate cuts, for a total cut of 1%.

It seems that PCE (the Fed’s preferred inflation measure) remains a concern for committee members. Its most recent reading was a 2.3% year-on-year increase, and its next reading is forecast to be a 2.5% year-on-year increase.

The committee might also be concerned by the unknown potential impact of President-elect Trump’s policies on inflation, and prefer to take a cautious stance given that uncertainty.

Equity markets move together and are priced against each other, and since US equities account for about 60% of total global equities, the Fed’s thinking affects all markets. But most companies we cover here will not be affected by US rates staying a little higher for longer. If Mr. Market is a little more depressed today than he was yesterday, I’d consider buying something from him!

Explanatory notes

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day. We usually avoid the smallest, and most speculative companies, although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We have a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Add your own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing. Links:

Daily Stock Market Report: records from 5/11/2024 (format: Google Sheet). Updated to 13/12/2024.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Serco (LON:SRP) (£1.42b) | TU | 2024 revenue in line. Adj. op. profit £270m. 2025 outlook: similar revenue, adj. op profit c. £260m. | AMBER (Graham) |

Henry Boot (LON:BOOT) (£314m ) | Acquisition | Acquires 100% of curr. 50% JV | GREEN (Mark) |

Avation (LON:AVAP) (£116m) | AGM Statement | Confident in ability to place remaining aircraft in orderbook. Bought back 10.45% of shares. | AMBER/GREEN (Mark) |

National World (LON:NWOR) (£59m) | Final Rec. Offer | 23p in Cash | PINK (Mark) |

Time Finance (LON:TIME) (56m) | TU | H1 revenue +16%, PBT +44% (£3.9m). Full-year performance to be at least in line with guidance. | AMBER/GREEN (Graham) |

Intelligent Ultrasound (LON:IUG) (£36m) | Recommended Cash Acquisition | 13p in cash, 16.9% premium to last night’s close. 47.5% of IUG shares have pledged to support. | PINK (Graham) |

FIH (LON:FIH) (£30m) | HY Results | £5.9m loss due to issues with an MOD construction project. | AMBER/RED (Mark) |

Insig Ai (LON:INSG) (£18m) | Interim Results | EBITDA loss (£0.4m). Cash £0.2m plus £0.3m R&D refund. Material uncertainty re: going concern. | RED (Graham) |

Summaries

Time Finance (LON:TIME) - unch. at 60.2p (£53m) - Half-Year Trading Update - Graham - AMBER/GREEN

Good news continues to flow from TIME and Cavendish believe that the company has a good chance of beating their recently upgraded forecasts (PBT £7.2m in FY May 2025). The stock trades at a hefty (35%) premium to tangible NAV but with a single-digit PER and strong momentum I’m happy to maintain our mildly positive stance for the time being.

Insig Ai (LON:INSG) - down 4% to 14.3p (£17m) - Interim Results - Graham - RED

This is a slam-dunk RED due to a weak balance sheet, a “material uncertainty” warning re: its ability to continue as a going concern, low-value contract wins, and potential overvaluation due to its association with the bubble in AI.

Avation (LON:AVAP) - down 3% to 152p - AGM Statement - Mark (I hold) - AMBER/GREEN

A large discount to TBV remains, and this AGM statement gives some confidence that asset values are reasonable, with demand for the ATR 72 planes that Avation prefer remaining strong. Their ability to sell a newly delivered plane for a $5m profit adds further evidence to this. The company has also managed to buy back a significant chunk of shares - 10.75% at 150p - which further increases the discount to book value. Some holders will be disappointed that recent takeover speculation is not mentioned, and the earnings remain depressed due to higher interest charges. This is too cheap, but an AMBER/GREEN until there is some tangible progress on either a sale or refinancing.

Henry Boot (LON:BOOT) - flat at 234p - Acquiring 100% of Stonebridge Homes - Mark - GREEN

I am underwhelmed by a further move into housebuilding by buying out their JV partner, even if this is a strong growth area. Smaller housebuilders tend to have mixed success. The good news is that the payment is structured over a long period of time and is dependent on performance. Hence this doesn’t impact the core reason for holding Henry Boot - a big discount to a tangible book value, where the accounts almost certainly undervalue their assets. Hence, the GREEN rating is retained.

FIH (LON:FIH) - Down 8% to 220p - Interim Results - Mark - AMBER/RED

Poor results from this rather strange mix of Falklands and UK businesses. It seems an issue with a construction contract in the FI has led them to restate the percentage completion of a housebuilding project for the MOD, leading to a large loss. The issues here are likely to continue into H2. Even excluding this, only one part of their business - the Portsmouth Harbour Ferry - appears to generate a decent return on equity. With the majority of the business being low-quality and facing issues, this is an AMBER/RED for me, despite a decent discount to TBV.

Short Sections

Intelligent Ultrasound (LON:IUG)

11.1p (pre-market) (£36m) - Recommended cash acquisition - Graham - PINK

This has been a special situation where IUG made a large disposal (£40.5m) during the summer, and was left with a smaller and financially limited subsidiary. As I noted in August, the remaining business (providing ultrasound simulation) generated H1 revenues of only £4.5m, and an operating loss of £1.4m.

Up until today, it looked like IUG was planning to make a large return of capital to shareholders. Indeed, it had taken the necessary legal procedures to enable a reduction of capital. But instead, it today announces an agreed sale at 13p for share. The buyer is from the industry: a Swedish company “Surgical Science” that provides medical simulation training.

I was neutral on this stock at 10p in August; I am now pleasantly surprised by IUG’s ability to find a trade buyer for the simulation business and protect its shareholders from the ongoing losses that it would be likely to generate as a standalone business. Hopefully this business will strengthen as part of a larger group.

The deal values IUG at £45.2m and should go ahead without difficulty as nearly half of shares are already pledged to vote for it. I would vote for it if I held IUG shares, as I would prefer to get paid a few million pounds for the simulation business instead of continuing to fund its losses.

National World (LON:NWOR)

22.2p (pre-market) - Recommended Final Cash Offer - Mark (I hold) - PINK

There was considerable uncertainty as to whether this potential offer was going to become a recommended one. I wrote about how shareholders could model such situations here. The biggest impediment was likely the agreement of Executive Chair David Montgomery, who was the driving force behind this media roll-up. After the company acquired the assets of Johnston Press in 2021, the shares touched 40p. In light of this, selling out at 23p may have been viewed as a failure. Perhaps the fact that he was in his 70s meant that he didn’t have the desire for a fight that looked like it was becoming acrimonious.

The premium offered seems reasonable:

53.3 per cent. to the closing price of 15.0 pence per National World share on 21 November 2024 (being the last Business Day before the commencement of the Offer Period);

However, this forgets that there was a recent overhang from Downing and concerns about poor shareholder communication depressing the price. Likewise, the multiple quoted at 4.6x adjusted EBITDA may be reasonable for a business expected to be a melting ice cube. However, it ignores that EPS was growing in very challenging advertising markets.

Mark's view

This has been sold cheap, but shareholders (such as myself) are probably just pleased to have the cash to deploy to other opportunities at the moment. When I modelled this, the presence of some severe downside scenarios meant that getting a recommended offer at 23p is definitely good news in the short term. It looks like shareholders may only be able to get between 21 and 22p in the market for their shares at the moment. Even at 22p it is a pretty certain 4.5% return. If we assume it will take around two months to receive the 23p cash, this is an annualised return of over 30%, and I see no point in selling in the market now.

Serco (LON:SRP)

Up 8% to 149.6p (£1.5bn) - Trading Statement - Graham - AMBER

It's an ahead-of-expectations update from the support services group Serco. There was a much improved order intake in H2, giving a book-to-bill ratio for the full year of c. 100%. Checking the half-year report I see this was only 82% in H1.

2025 outlook: flat revenues of c. £4.8 billion despite the loss of major immigration contracts in UK/Australia worth 7% of revenue. The underlying operating profit forecast for 2025 is c. £260m, vs. £270m expected for 2024. These annual profit figures are both about £5m ahead of expectations according to Thomson Reuters.

Graham’s view: the addition of c. £5m to annual underlying profit has helped to boost the market cap today by over £100m but the most impressive feature of this statement is the way the group has bounced back from the loss of major contracts, to produce a good result for the year along with a positive outlook for 2025. The new business pipeline is ending the year “at highest level in more than a decade”.

Serco believes that it is under-leveraged with debt ending the year at £145m and a leverage multiple well below its target range of 1-2x. This gives scope for another potential catalyst that could help the share price to recover further, e.g. in the form of a new buyback. In the short-term I do think the Serco share price can recover further but ultimately I would not want to pay an earnings multiple significantly above the current level of c. 9x.

Graham's Section

Time Finance (LON:TIME)

Unch. At 60.2p (£53m) - Half-Year Trading Update - Graham - AMBER/GREEN

Roland covered this SME lender in September and then I gave it a brief review in November, when it upgraded expectations for FY May 2025.

The company was previously known as 1pm and traded under the ticker OPM.

Today’s H1 update confirms continued excellent progress:

H1 revenue +16% to £18m

PTB +44% to £3.9m (PBT margin improves to 21%)

Net tangible assets increase to £41.5m.

I’ve noted before that the company trades at a substantial premium to tangible NAV. We currently have a £53m market cap vs. £41.5m TNAV, for a premium of 28%.

This effectively puts a limit on how bullish I can be, as I prefer buying quality financial stocks at or below TNAV.

But for a high-performing lender, a premium valuation can be a fair valuation. TIME’s lending activities are doing well:

Lending book up 11% year-on-year to £209m

Net arrears stable at 5% (last year: 6%)

Bad debt write-offs unchanged at 1%

The outlook is therefore at least in line with recently upgraded guidance.

The strategic focus now is on invoice finance and “hard” asset finance (vehicles, machinery, and equipment), “as they are, typically, both larger in average loan size and more secure”. These categories now account for 85% of new deal volume.

CEO comment (excerpt):

The Board are very encouraged by the performance in the first half of the current financial year. In line with our strategy, we have continued to increase the size of our lending book and, crucially, have done so without compromising on credit quality. This is borne out by the stable nature of both our arrears and our write-offs… We have real confidence that the Group is well placed to continue on this growth trajectory, building long-term value for our shareholders…

Estimates: Cavendish says that TIME has “a good chance of outperforming our recently upgraded FY25E PBT of £7.2m”. PBT is forecast to grow further to £8.1m by FY May 2026.

Graham’s view

Although I said that I could not be too bullish on this one, due to its valuation, I can still retain our mildly positive AMBER/GREEN. The shares are only a little higher than last time I covered this one (57.8p) and they do still (just) trade at a single-digit PE ratio:

Note that there is still no dividend here, and there is no indication that management wants to do anything with the company’s available cash other than investing for further growth.

I’m wary of this one becoming overheated but for now I think the price is fair for a growing SME lender with strong momentum and I’m happy to stay AMBER/GREEN.

Insig Ai (LON:INSG)

Down 4% to 14.3p (£17m) - Interim Results - Graham - RED

I looked at this one two years ago (share price at the time: 16.5p) and concluded it was very high risk. Funding it seemed to be a challenge.

Hopes that it would become cash flow positive did not materialise, as full-year results for FY March 2024 showed a £300k outflow from operating activities, plus another £800k outflow from investing activities.

The company provides “AI and Machine Learning Data Solutions” and “Machine-readable ESG Data” (for use by AI) to the asset management industry.

Today’s interim results show an EBITDA loss of £04.m, and an operating loss of £1.4m.

CEO comment:

"I am pleased to report that since the period end, we have seen year on year revenue growth, a dramatic increase in our sales pipeline, broadening engagement with regulators and incoming requests for proposals to meet business needs as a result of a strategic business development shift. Alongside structural tailwinds within the markets we address, we can look forward to 2025 with confidence.

The sales pipeline is now worth £2.5m.

The company finished the period to September with cash of £0.2m, plus another £0.3m in an R&D tax refund received since then.

Balance sheet: negative tangible net worth of £2.7m. There’s £1.6m outstanding in convertible loan notes, owed to two individuals including the CEO. The company is paying 6% interest to the CEO and 12% interest to the other individual.

Fundraising: new equity was raised in April, May and June.

Going concern warning: given the low cash balance, it’s unsurprising to find a “material uncertainty” warning, re: the company’s ability to continue as a going concern..

Graham’s view: it’s inadequately funded in my view and will need to continuously raise fresh equity. I have to be RED on this.

Do the company’s solutions have commercial value? That might very well be the case, but I’m instinctively cautious whenever looking at an “AI” or “machine learning” stock (INSG is both), due to the obvious bubble associated with AI.

A recent RNS from INSG trumpeted a contract win with a value of £80k. Even for a company with a sub-£20m market cap, I don’t see how this moves the needle. So I have zero doubt that RED is the right choice for this one: extremely risky, and I think there’s a very good chance that it’s overvalued.

Mark's Section

Avation (LON:AVAP)

Down 3% to 152p - AGM Statement - Mark (I hold) - AMBER/GREEN

On an asset basis, Avation remains one of the cheapest stocks on the UK market:

However, the book value is the difference between two large figures:

The debt is largely fixed in value, so this is highly sensitive to the value of the assets. So it is good news that they open today’s AGM update by saying:

Market values and lease rates for commercial aircraft continue to be supported by constrained deliveries of new aircraft due to continuing supply chain issues. Avation believes that values of popular new narrowbody aircraft types have increased by around 5% over the last year.

There is evidence that the demand for their preferred type of plane, the ATR 72, is in high demand too:

In November 2024 the Company sold a new ATR 72-600 on delivery from the manufacturer, generating net cash proceeds for around US$ 5 million. The net proceeds from sale have been deployed to fund pre-delivery payments on Avation's orderbook for additional ATR aircraft.

This is good business. Avation has agreed to buy new aircraft from manufacturers at fixed prices far in the future. These are known as slots. While they can’t sell on the slots, they can take delivery of the aircraft and immediately sell it on. This is what they have done here, generating around $5m of profit. It is worth noting that this can be a risk as well as an opportunity. The demand for this specific aircraft may not always be as buoyant, so they are also taking a risk that prices go against them.

It seems selling this was a one-off, and future deliveries have agreed to be leased:

The Company has two new ATR72-600 aircraft being delivered in 2025. For the first aircraft, the Company signed a twelve-year lease agreement with a Japanese airline. This aircraft is currently scheduled for delivery from the manufacturer in October 2025. The second aircraft has been placed with an airline in Korea. Both of the two new aircraft have been placed with two new airline customers. The next available new aircraft scheduled for delivery is in 2026.

As have returning aircraft:

The Company has three leased aircraft being returned in 2025. All three aircraft have been placed with three new airline lessees for subsequent operation. There are no further lease aircraft being returned until 2026.

Unfortunately, they do not mention the rates obtained for these. If the market for this type of aircraft is indeed tight, it should be reflected in the lease rates. However, we are not given any information on this.

While the discount to NAV seems compelling, the other value metrics are not as good. Their broker, Zeus, is forecasting 9.1c of EPS for FY25, putting them on a P/E of 21.9. It's not exactly bargain territory. There are three reasons for this. The first is that depreciation is a big charge for planes. Secondly, they still have some money owed from COVID times. However, the most significant is the interest they pay on the debt:

Avation currently has US$ 336.8 million secured bank loans outstanding which bear interest at an average interest rate of 4.86%.

Avation also has US$ 331.6 million outstanding 9.00%/8.25% Senior PIK Toggle Notes which have a maturity of October 2026.

Perhaps the biggest news here was actually announced yesterday:

The Company repurchased on the 17th of December 2024 a total of 7,800,000 shares representing 10.45% of the outstanding shares for 150p each. These repurchased shares will be held in treasury. The Company had a view that the most undervalued security was the ordinary shares and that this repurchase was the most value accretive.

It is this that actually caused me to buy some Avation for the first time yesterday. Although some of these may be used to offset the large number of options outstanding here, buying back significant chunks of shares at half TBV is highly accretive to that TBV per share. The shares appear to have come from Rangely Capital, as the only independent holder capable of supplying that quantity. Strangely, they don’t appear in the data from Refinitive but other sources had them at 25.75%. This means they are down to around 15% minus any they have been selling in the market. This may still represent a significant overhang. But equally, assuming the buyback mandate is renewed at today’s AGM, it may give an opportunity for Avation to enhance the discount to TBV further.

The shares are down a couple of per cent today. Presumably, because the company makes no mention of the recent takeover rumours. One of the impediments may be the previous statement from the CEO saying they won’t sell below TBV. Hopefully, this is just a negotiating tactic, as the share price is clearly telling the board that shareholders would be happy to receive a small discount to TBV for an exit. The rationale for a takeover by a larger leasor seems compelling, too. The acquirer gets to refinance the debt at the lower rates enjoyed by larger more diversified companies, plus access to aircraft and slots in a tightening market for less than their book value. However, balancing this, we have to ask why Rangely Capital would be such keen sellers if such a deal was imminent?

Mark’s view

When Paul looked at this in May, he rated it AMBER/GREEN. Since then, the discount to TBV has improved due to the recent large share buyback, and there have been takeover rumours. The rationale for a takeover seems compelling, and it is tempting to update this to GREEN on that basis. However, experience tells me that the timing of offers tends to be almost entirely random to those outside the process. Outside of an offer being made, unless they can pay down or refinance their expensive PIK notes then their earnings will not reflect the market value of the assets. Hence, I retain the AMBER/GREEN until there are signs that they have made progress on this, or a potential acquirer starts stakebuilding.

Henry Boot (LON:BOOT)

Unch. at 234p - Acquiring 100% of Stonebridge Homes - Mark - GREEN

Henry Boot describes themselves as “one of the UK's leading land, property development, home building and construction businesses.” Their specialism is navigating the planning approval process and getting plots approved for housing. However, they also have a construction arm and Joint Ventures in housing. This morning’s announcement is about them buying out their JV partner in Stonebridge Homes. The rationale is that this is a business which they can grow:

Stonebridge is a high growth U.K. multi regional housebuilder which is currently focussed on delivering premium homes in Yorkshire and the North-East. The business has grown significantly since it was founded in 2010, increasing output by an average 25% p.a. over the past ten years. In addition, in the five years ending 31 December 2023, both revenue and operating profit more than doubled, reaching £94.4m and £5.9m, respectively. In 2023 Stonebridge completed 251 homes and has a medium term target of delivering up to 600 new homes annually.

However, housebuilding is a hugely cyclical, low-margin business, and as we have seen with Vistry recently, things can go wrong quickly if costs are underestimated. One of the major costs is land, and perhaps controlling the full value chain is an advantage. Although perhaps no more than having a JV.

The good news is that they are not paying much upfront for this:

The Transaction will be undertaken in three tranches over the next five years, with anticipated fixed payments totalling £30m and additional payments linked to Stonebridge's performance as follows:

· The first tranche is expected to be completed in January 2025, and will see the group acquiring 12.5% of Stonebridge for a fixed price of £10m, resulting in a majority shareholding of 62.5% of Stonebridge;

· A second tranche to acquire a further 12.5% is expected to complete in January 2026, with consideration payable in FY26 and FY27; and

· A third and final tranche to acquire the remaining 25% is expected to complete in January 2030, with consideration payable in FY30 and FY31.

Despite this, the core reason for holding Henry Boot remains, which is a discount to TBV:

It is worth noting that the company only marks up the book value of their plots when they are sold, not when planning consent is achieved, which means that the stated book value almost certainly understates the market value of the land they own. In their announcement last week, they say things here are accelerating:

Hallam has seen noticeable improvements in the planning system since the change in Government during the summer. In the year to date, Hallam has secured consents on a total of 2,870 plots (2023: 1,014 plots), of which 2,056 have been achieved since the beginning of September. In addition, Hallam has appeals lodged on 2,189 plots across seven sites and in total has 11,191 plots in the planning system.

Not only that, but a further 10,000 plots are expected to be submitted to the planning system over the next 12 months. In 2023, they submitted just 2185 plots for planning. This is likely to result in a further uplift to TBV.

Mark’s view

Graham rated this GREEN in March. Since then, the shares have gained almost 30%. While I am not convinced about the rationale for increasing their exposure to housebuilding directly, the terms of the deal mean they are not taking much risk on the amount paid. The core reason for holding Henry Boot remains, which is a significant discount to TBV, with the current balance sheet almost certainly understating the market value of those assets. Hence, I retain the GREEN rating.

FIH (LON:FIH)

Down 8% to 220p - Interim Results - Mark - AMBER/RED

FIH, formerly Falkland Island Holdings, joins my trio of stocks reporting today that are trading at a discount to TBV:

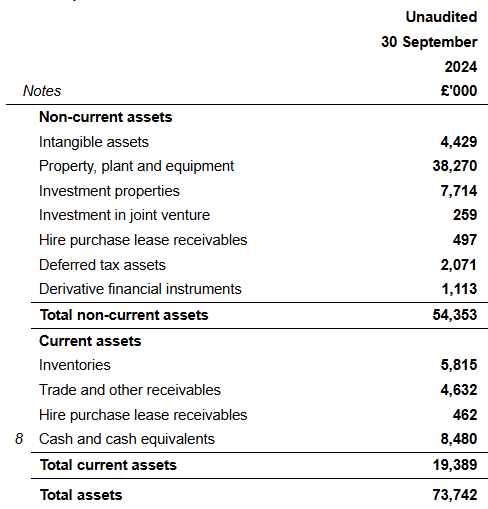

The good thing about analysing results versus a trading statement is that we get a (fairly) up-to-date look at what those assets are:

By far the largest amount is PP&E and investment properties. Offsetting these assets are £17.7m of debt and £9m of payables, plus a small pension deficit requiring about £0.3m a year in recovery payments.

There are lease liabilities too, as the company says:

Cash position of £8.5 million as at 30 September 2024 (2023: £9.2 million) within net debt before lease liabilities of £3.3 million (2023: £3.6 million).

However, these net off in the calculation of NAV. The problem is that these assets are hard to value. This is what the company does:

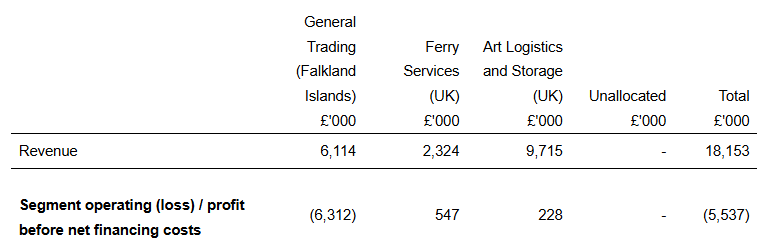

And here is the breakdown of trading:

And the balance sheet:

While a ferry, and logistics vehicles and warehousing may well have alternative use value, more than half of the net assets are in the Falklands. Unlike Avation or Henry Boot there is no easy way of realising these assets. This means we have to assess the business on the productivity of those assets. Looking at the figures above, only UK Ferry Services appear to be a decent business. The others don’t generate an acceptable return on assets or equity. Partly this is because the Falklands part of the business has had a challenging half-year:

The majority of this variance related to the contract to build a total of 70 houses for the Falkland Islands Government ("FIG") and the Ministry of Defence ("MOD"). The programme of works was changed to address the disruption caused by the lack of power on the MOD Mount Pleasant Complex ("MPC"). As a consequence, the assessment of percentage of completion of the project was amended, resulting in a reduction to revenue recognised in previous periods. In addition, there was an increase in the forecast contract completion costs due to a combination of adverse weather conditions and the departure of FBS management and the challenges in replacing them.

Other shortfalls in revenue in FBS were from a lack of work due to delayed and unsuccessful tenders.

I’m not close enough to this to know exactly what has gone wrong, but having to restate revenue recognition because a project was not as advanced as previously booked is a major worry. I can’t help feel that the location is major impediment to successful execution here. Both because of the weather and because getting staff with the right skills in the Falklands must be challenging. I’d only accept a job there if it was 100% WFH (in the UK!) There doesn’t appear to be an easy fix either:

Action plans are being progressed in FIC to address the challenges in FBS but these challenges are expected to continue to significantly impact the performance of the division for the remainder of the year, albeit within the Group's existing resources.

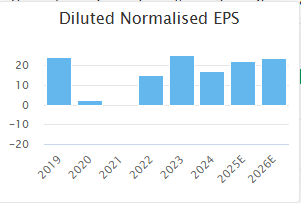

They are confident enough to maintain their interim dividend. However, an overall yield of around 3% doesn’t stand out in the current market. Following these results, and the outlook, I simply don’t believe these forecasts:

Indeed, after checking the updated Zeus note released today, I see they are only showing historical figures. Which means that they have withdrawn forecasts, and the ones on the StockReport are now stale.

Mark’s view

A reasonable discount to TBV is available here. However, those assets are mostly unproductive at the moment. Only the Ferry Services appears to be generating a decent return on equity. The rest of the business looks poor quality, and there is no sign of a short-term resolution to the issues they are facing. This is an AMBER/RED for me.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.