Good morning! Graham here, back after taking some time off. Let's see what companies we have reporting on the first business day of the new year!

Recent articles on Stockopedia:

- SIF Folio 2024 review & changes for 2025 by Roland

- 12 Stocks of Christmas: IG Design by Mark

- 12 Stocks of Christmas: Billington by Mark

11.15am: Roland and Megan have covered a few stories and I think I'll end the report there due to the limited amount of news to cover today. Hopefully we'll have more to cover tomorrow! Cheers.

Spreadsheet accompanying this report: records from 5/11/2024 (format: Google Sheet). Updated to 19/12/2024.

Companies Reporting

Unfortunately there is almost nothing of interest today:

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Mission (LON:TMG) (£22m) | Disposal and capital allocation update | Mission has sold a subsidiary for £17.4m, proceeds will repay debt. | AMBER/RED (Roland) |

Backlog

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Ricardo (LON:RCDO) (£261m) - 17 Dec 24 | Sale of Ricardo Defense & Acquisition of E3 Advisory | The UK engineering consultancy group is exiting defence and doubling down on its focus on the environment and energy transition. | AMBER (Roland) |

Summaries

Mission (LON:TMG) - Up 20% to 29p (£27m) - Disposal and Capital Allocation Update - Roland - AMBER/RED

Mission has sold a US-focused subsidiary for up to £17.4m. This deal should repair the group’s balance sheet and provide some protection for the company’s equity. However, I think there’s a risk the company may have sold one of its more profitable units in order to achieve this goal, so I’d like to see updated guidance from the company before considering a more positive stance.

Ricardo (LON:RCDO) - unch. at 419p (£261m) - Ricardo Defense sale & Acquisition of E3 Advisory - Roland - AMBER

Recent corporate activity will see Ricardo exit the defence sector and expand its focus on the environment and energy transition markets. I take a look at these recent transactions and consider the resulting fall in near-term profit expectations. While the strategy makes sense to me and both deals may turn out to be reasonably priced, I think it makes sense to stay neutral for now.

Short Sections

Poolbeg Pharma (LON:POLB)

Down 34% to 4.7p (£35m) - Reverse merger with US company - Megan - RED

I have been reading some rather depressing statistics this morning about the number of companies that delisted from London’s main market in 2024 - 88 of them in total, compared to just 18 new entrants. This marked the worst year for UK stock market outflows since 2009 in the wake of the financial crisis.

News this morning that Poolbeg Pharma (LON:POLB) is reversing into Nasdaq-listed Hookipa Pharma (NAQ:HOOK), in a deal which seems to value the UK company at about £25m less than its pre-announcement market capitalisation, adds more negativity.

Poolbeg is a spin out of hVIVO (previously Open Orphan) which has had its fair share of ups and downs since it listed on Aim in 2012. Poolbeg was listed as its own entity (with the same chairman as the former parent) in 2021 in the wake of the Covid-19 pandemic, to focus on clinical candidates in the antiviral and vaccine space.

Hookipa is a specialist in immunotherapy with drug candidates in both the oncology and infectious disease space. Like both Poolbeg and its former parent hVIVO all of its drugs and vaccines are in the early stages of human trials. All three companies are aiming to sell their drug candidates to larger pharmaceutical companies before they reach the expensive late stage trial phase.

It’s not a bad model. Big pharma tends to struggle to move quickly enough to take drugs from the pre-clinical stage of development all the way through to commercial launch, while smaller companies don’t have the financing or commercial expertise to take them all the way through to market.

The trouble is that for now Poolbeg hasn’t managed to hook any of those big partners. In September, chief executive Jeremy Skillington commented that the value and attractiveness of one of the company’s drug’s candidates had been “greatly enhanced following the independent confirmation of a potential market opportunity”. But that is definitely more of a hopeful comment than anything concrete.

Megan’s view:

Poolbeg, hVIVO and Hookipa are all ‘wait and see’ kind of investments. They’re high risk because there is no guarantee of any deal coming to fruition, but could be high reward if a clinical candidate does get snapped up by a big pharma group.

They also absorb a lot of capital which is perhaps why the merger with a Nasdaq-listed company is sensible. In September Poolbeg had £10m of cash on its balance sheet and under its new parent, it’s hoping to raise $30m from Nasdaq investors.

Shareholders will definitely suffer some dilution in this deal, but Nasdaq does (for now) seem like a better home for Poolbeg. There are good clinical synergies between the two companies as well. Plus the fact that the US is a better market for pharmaceuticals.

I’m RED on the company as a whole and I don’t like the way Aim-shareholders have been treated in this situation, but I can see why the deal makes sense.

Mission (LON:TMG)

Up 20% to 29p (£27m) - Disposal and Capital Allocation Update - Roland - AMBER/RED

This small-cap marketing group has announced the £17.4m disposal of its April Six subsidiary today – a material amount, given Mission’s £22m market cap (pre-open).

We’ve regularly covered Mission in this daily report, often with mixed feelings. For much of last year we maintained a RED view on Mission due to its weak balance sheet.

In May 2024, Graham discussed a (rejected) bid by rival Brave Bison to buy Mission that might have addressed this issue.

In June, Graham reviewed Mission’s trading and warned that its “large debt balance and slim profitability” could require an equity fundraising.

As it turned out, Mission didn’t carry out an equity raise – and perhaps we now know why. The company has opted instead to sell what appears to be a sizeable subsidiary.

Let’s take a closer look at today’s news.

April Six sale: Mission has agreed to sell its April Six business (April Six Limited & April Six Inc) to US firm Marketbridge Inc for a total gross consideration of up to £17.4m.

This will comprise an initial cash payment of £10.5m and an earnout of up to £4.2m. As these figures only total £14.7m, I guess Marketbridge will also assume some debt/working capital liabilities.

The total consolidation of £17.4m appears to be equivalent to c.1.5x April Six’s revenue, but the company has not provided a 2024 profit-based valuation multiple for the sale. The only clue we have is that the earn-out target is calculated based on a 7x EBITDA multiple.

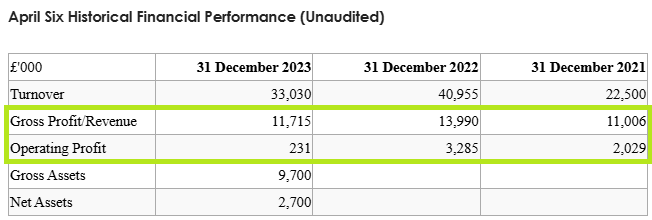

April Six’s client base is said to be heavily skewed to the US tech sector. As a result its profits slumped in 2023 as tech spending slowed. But we can see from the historical numbers provided today that April Six has generated significant profits in the past.

I’ve highlighted the relevant lines for adjusted revenue (excluding pass-through) and adjusted operating profit:

We don’t have 2024 figures, of course. But averaging the three years above gives £1.85m of operating profit on £12.2m of revenue, equivalent to a margin of 15%.

If we view these figures as a normalised level of performance for April Six, then today’s transaction appears to offer the buyer an earnings yield (op profit/EV) of nearly 11%, which does not seem too expensive to me.

One other interesting point from today’s announcement is that the founder and CEO of April Six, Fiona Shephard, seems to have played a key role in arranging this transaction.

Mission says Ms Shephard will remain with April Six and will receive a £360k payment “for sourcing the buyer”, as part of a wider £860k “incentive payment” to members of April Six’s management team.

Impact on TMG balance sheet: initial cash proceeds of £10.5m are expected to reduce net bank debt from £17m on 30 December 204 to £6.5m following receipt of the proceeds.

A further reduction is expected if the earn-out consideration is received.

TMG says the disposal will improve its net debt/EBITDA and interest cover ratios. This is expected to result in improved borrowing terms from lender NatWest.

Looking ahead, Mission’s management are targeting medium-term leverage between net cash and 1x headline EBITDA.

Dividends are expected to return in 2026.

However, the company is sufficiently confident to declare a £1.5m share buyback today, beginning immediately.

Impact on TMG earnings & outlook: The profit figures for April Six in the table above suggest to me that this subsidiary generated around 25% of TMG’s 2021 operating profit, rising to nearly 38% in 2022.

In 2023, TMG’s headline operating profit fell by £2.3m to £6.5m, while April Six’s operating profit fell by c.£3m to just £231k. So it seems that TMG’s profit slump last year was probably caused by April Six, partially offset by gains or savings elsewhere.

House broker Canaccord Genuity has left its 2024 forecasts unchanged today ahead of TMG’s expected FY24 trading update on 20 January 2025.

Current forecasts suggest Mission shares could be trading on c.4.4x 2025 forecast earnings, after this morning’s rise. But I would prefer to have some idea of the likely impact on profits before relying too heavily on these estimates.

£5m cost saving plan completed: the company says that the disposal of April Six means it has now achieved its target of £5m of annualised operating cost savings in 2024.

Of course, it’s easy to reduce operating costs by carving out a big part of the business. The question now is what impact this may have on future earnings.

Roland’s view

Today’s deal seems a reasonable approach to solving Mission’s debt problem. The company has historically generated more than 80% of its operating income in the UK, so selling a US-focused business may be logical.

Assuming that 2025 earnings bear some resemblance to current forecasts, then I think it’s fair to say the overall position has improved for equity investors today.

However, while April Six performed poorly in 2023, its performance in 2021 and 2022 suggests to me that it’s capable of generating high-margin earnings. I wonder if the other parts of Mission’s business are as profitable.

Until we see the 2024 accounts and receive updated guidance on profits and growth expectations, I think it makes sense to retain a cautious view. I’m going to upgrade our view by one notch to AMBER/RED.

Ricardo (LON:RCDO)

Unch. at 419p (£261m) - Ricardo Defense sale & Acquisition of E3 Advisory - Roland - AMBER

This is a backlog piece covering news from 17th Dec 2024. As it’s quiet today, I thought it might be interesting to take a look at this engineering consultancy business, which is currently reshaping its operations.

On 17 December, Ricardo announced the sale of its Defense unit for £67.5m and the acquisition of Australian infrastructure consultancy business, E3 Advisory, for £51m.

The planned sale of Defense had been flagged up in October’s strategy update as part of a move to focus more closely on “engineering consultancy in environmental and energy transition”.

As Graham commented at the time, Defense was a key profit contributor with higher margins than the group’s other operations. So the exit valuation would be important, as would the company’s plans for the proceeds – unlike TMG above, debt levels were not a concern.

Ricardo Defense sale: the sale of the defense business was agreed to a private equity consortium for $85m (£67.5m).

For context, Defense contributed £123.4m of revenue and £23.5m of adjusted operating profit in the 23/24 financial year. Those figures represent 26% of revenue and 60% of underlying operating profit for FY24.

At first glance, the valuation of the sale appears to be very reasonable (for the buyers!) at less than three times trailing operating profit.

However, the picture is complicated slightly by the outlook for a significant drop in sales of a key programme supplying updated Antilock Braking Systems for US Army vehicles. Activity is expected to peak and start falling from 24/25 onwards, meaning future profits could be lower than those seen recently.

The company says this means the timing of the sale is “optimal to maximise the value of Ricardo Defense”.

However, unless the ABS programme is truly exceptional, my feeling is that this valuation also implies a relatively cautious view on future sales. I don’t know whether this might be justified by sector expectations and the Defense order book.

E3 Advisory acquisition: on the same day as the Defense sale, Ricardo announced the acquisition of Australian firm E3 Advisory for £51m (funded entirely with proceeds from the Defense sale).

Given their similar size, shareholders might have expected these transactions to broadly offset one another in terms of profit contribution. But that’s not the case. At least, not initially.

Ricardo’s acquisition price for E3 is 7.7 times the company’s FY24 operating profit of AUD13.2m (£6.6m) – a much higher multiple than the Defense sale.

Management appears to be counting on E3 to continue delivering high-margin growth, in a way that perhaps the Defense business would not.

In fairness, the summary accounting information provided for E3 Advisory does seem to suggest this could be an attractive business. Revenue rose by 15.7% in FY24 and profits were generated with an underlying operating margin of 28.5%.

Updated outlook: the inescapable reality is that Ricardo is selling a business that generated £23.5m of profit last year and replacing it with one that generated less than £7m of profit last year.

The company admits this will be “dilutive to the Group’s earnings per share in the near term”...

With thanks to broker Panmure Liberum, we can get an idea of the scale of this dilution:

FY25 earnings forecasts cut by 47% to 21.4p per share

FY26 earnings forecasts cut by 27% to 33.5p per share

Panmure’s FY25 forecast in particular appears to be more pessimistic than the consensus forecasts shown on the StockReport – this may mean that some of the estimates used to compile consensus have not yet been updated:

Panmure Liberum’s estimates price Ricardo on a FY25 P/E of 19.6, falling to a FY26 P/E of 12.5.

Roland’s view

If E3 Advisory can maintain its recent growth rate and profitability, then I think it’s fair to say that the purchase price may prove reasonable.

Whether the Defense sale price is attractive for Ricardo shareholders is harder to ascertain. Realistically, we are unlikely to have any visibility on the subsequent performance of this business once it is divested.

If profits slump for a few years then Ricardo’s sale may indeed have been “optimal”. Personally, I’m not entirely convinced this will be the case, given the positive macro backdrop for defense spending and Ricardo’s seemingly positive relationship with the US DoD.

For prospective and existing shareholders in Ricardo I think this pair of transactions justifies a fresh look at the business. As Graham commented, a more focused strategy can often be attractive from an investment perspective.

On the other hand, the loss of the Defense unit means this will be a somewhat different business, going forward.

Looking ahead to FY26, my feeling is that a valuation of c.12x earnings would not be unreasonable.

However, my feeling is that the earnings outlook for the next 12-18 months could be somewhat uncertain, until both transactions have completed and we see some evidence of the contribution that’s being made by E3 Advisory.

I’m staying neutral for now - AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.