Good morning!

It looks like we are going to have one last day without too much news, before things get back to normal tomorrow.

12:30: all done, see you tomorrow for some more interesting announcements!

Spreadsheet accompanying this report (updated to 3/1/2025).

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Gulf Marine Services (LON:GMS) (£164m) | Debt refinancing | Debt refinancing completed, reducing cost of debt & allowing higher dividends. | GREEN (Roland) |

Trufin (LON:TRU) (£92m) | TU | FY24 adj PBT expected to be “significantly ahead of market expectations” leading to maiden FY profit of >£0.5m. | AMBER (Roland) |

Hercules Site Services (LON:HERC) (£33m) | Strategic Update | Plans to sell “Suction Excavator” business, including its debt, which will raise HERC’s PBT & EPS. | AMBER (Graham) |

Smarttech247 (LON:S247) (£10m) | FY update | Results for y/e 31 Jul 24 expected later in Jan. Revenue exps “in excess” €13m, +8%. Adj op profit exps over €750k. | AMBER/RED (Graham) |

Summaries

Trufin (LON:TRU) - up 4% to 91p (£96m) - FY trading update - Roland - AMBER

2024 profits are expected to be “significantly ahead of expectations” after a very strong performance from the group’s games business in December. Trufin now expects to report its maiden annual profit one year earlier than planned. I can see attractions in the group’s payment businesses, too. But with management warning that 2025 could be a year of consolidation, I think the share price may be up with events for now.

Hercules Site Services (LON:HERC) - up 2% to 42.9p (£33m) - Strategic Update - Graham - AMBER

I’m upgrading this construction recruitment firm to AMBER as I always appreciate a sensible divestment, and HERC’s proposed disposal of its vehicle rental business sounds reasonable to me. Hopefully we will start to see material profits here before too long, perhaps with the help of some small acquisitions. Existing broker forecasts are for adj. PBT of £1.3m in the current financial year (FY Sep 2025), rising to £1.5m the following year.

Short Sections

Gulf Marine Services (LON:GMS)

15.4p (£164m) (pre-market) - Debt refinancing completed - Roland - GREEN

This offshore support vessel operator completed its debt refinancing on 30 December, as first announced in August. It should be good news for shareholders as debt costs will fall, freeing up cash for debt reduction and – potentially – dividends or share buybacks. According to broker Zeus (many thanks), this will be possible when net debt/EBITDA falls below 1.5x.

Checking back to the August RNS, the new debt package includes a $250m, five-year loan and a $50m working capital facility. GMS will need to repay 16% of the loan each year, with a 20% final payment at the end of the term.

I estimate the new package could result in a c.0.6% reduction in the interest rate being paid by GMS today, with a further reduction when leverage drops below 2x EBITDA. That could save c.$1.3m per year in debt costs, based on the last reported net debt of $234m. That's a useful saving for a company expected to report a net profit of c.$48m in 2025

I’m happy to stay GREEN on GMS ahead of the company’s full-year results, given recent strong trading and the stock’s substantial discount to book value.

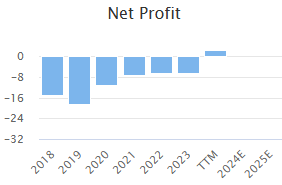

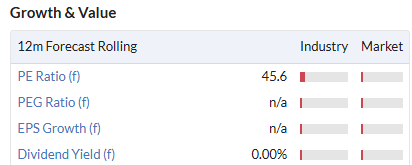

Smarttech247 (LON:S247)

Up 16% to 9.8p (£12m) - FY trading update - Graham - AMBER/RED

Smarttech247 (AIM: S247), a multi-award-winning provider of AI-enhanced cybersecurity services providing automated managed detection and response for a portfolio of international clients, announces an update regarding the Company's results for the year ended 31 July 2024 ("FY2024").

This one listed in Dec 2022 and was mentioned by Paul twice - April 29th and April 30th.

With such a small market cap and with most of that held by the Chairman, the free float is only worth a few million pounds.

The company still hasn’t published its results to July 2024 and says that it will do so “in the second half of January 2025”.

It’s a paradox that I see so often: small companies take an age to get their audits done and their results out, while large international companies have little difficulty getting results out promptly. Shouldn't it be the other way around?

Management at S247 seem happy with progress in FY July 2024, reporting a 50% increase in ARR (now 60% of total revenues), revenues up 8% to €13m, and an adj. operating profit of over €750k.

I don’t have a strong view on this business but with a free float so low I reckon that AMBER/RED is appropriate, purely as a warning to everyone re: illiquidity. Getting involved with companies at this size and with such a small free float brings a different set of risks compared to mid-caps and big-caps, with the main risk being that at some point the company decides it's no longer worth being listed. Hopefully that doesn't happen here, but I just think it's crucial to be aware of this factor.

On the subject of illiquidity and delisting risk, I note in passing that the owner of a quirky bookshop Scholium (LON:SCHO) has left AIM today. This stock spent years trading at a deep discount to its tangible book value. I looked at it several times, but thankfully never bought it. Delisting risk is not something I put up with these days - I've decided that life's too short to hold "deep value" stocks that are too small to have a stock market listing!

Graham's Section

Hercules Site Services (LON:HERC)

Up 2% to 42.9p (£33m) - Strategic Update - Graham - AMBER

An interesting little announcement from HERC as it now intends to sell its “Suction Excavator” business, as it considers it to be “non-core”.

Offloading debt

Suction Excavator Services is said to be responsible for only 5% of HERC’s overall revenues, but 88% of its debt.

It’s is a vehicle rental business, so it’s natural enough that it would use some debt.

It would have been helpful to get an indication of what the debt number is, but I can try guessing at a ballpark figure using the interim results, when HERC’s gross borrowings were £6m. So I would guess that the Suction Excavator business probably has debts in the region of £6m - hopefully this can be confirmed soon..

As we discussed back in October, HERC raised £8m of fresh equity recently, in order to strengthen its balance sheet and give it the firepower for acquisitions. So its balance sheet should already be quite strong, even before going ahead with this disposal.

Concentrating, not diversifying

The proposed sale will allow greater resources to be dedicated to HERC’s core labour supply activities, and will “reinforce the Group’s market positioning” in this area.

In other words, HERC will be more easily recognised by customers as a construction recruitment business, not as a group offering a mix of construction-related services.

As an aside, I’d like to note that when companies do the opposite of HERC and diversify their operations, they rarely acknowledge that it will dilute their market positioning - even though that’s probably true in a lot of cases!

Financially, the planned disposal by HERC “is expected to contribute to higher profit before tax, improved earnings per share, and enhanced returns for shareholders in the near future”.

I’m wondering how that can be true, unless Suction Excavator Services is currently loss-making?

Checking the 2023 Annual Report, I see that Suction Excavators generated an operating profit of £600k for the year (2022: £1.0m).

And things seemed to be going ok for this segment in 2024, when the interim report was published. There was only a small hint that profits might be under pressure:

Demand is strong but the key is focusing on profitable work, and so a number of changes relating to the way we select jobs have been made to ensure we are as efficient as possible.

I wonder if trading has been tougher in recent months. Perhaps the operating profit from Suction Excavator Services is not enough to cover its interest bill.

As this business is now up for sale, it will be reported separately by HERC in the “discontinued operations” section of its 2024 results.

Graham’s view

Divestments can be a great source of investment ideas. In general, I like proposals that reinforce a company’s strengths, improve its balance sheet, and help management to focus on where they can have the greatest success.

However, I must add a few caveats here.

Firstly, there is no guarantee that any disposal will be achieved. Full-year results will be reported on the basis that HERC intends to make this disposal happen, but we can’t know for sure that it will.

And on a related point, what might the Suction Excavator business be worth? The sale price might not be very impressive given that it's a leveraged business model and that current trading might not be very strong (otherwise, how would the disposal result in higher profits for HERC?).

In October, I was AMBER/RED on HERC. I’m inclined to raise this to AMBER now on the basis that the balance sheet should be strong already (given £8m raised previously), and could get even stronger if the proposed disposal goes ahead. With management armed to make relevant acquisitions, hopefully they can start to generate some value for shareholders.

Roland's Section

Trufin (LON:TRU)

Up 4% to 91p (£96m) - FY trading update - Roland - AMBER

Checking back in the archives, Graham last covered this technology and finance group just one month ago, when Trufin said 2024 results would be significantly ahead of expectations.

Today, we have another upgrade:

TruFin is pleased to announce that it expects its adjusted profit before tax ("PBT") to be significantly ahead of market expectations resulting in its first full year profit - a year earlier than forecast.

The company now expects to report revenue of approximately £54m – a 197% increase on FY23. This is expected to translate into an adjusted pre-tax profit of “more than £0.5m”, versus a loss of £6.6m in FY23.

As a result, Trufin expects to report its first ever (adjusted) full-year profit one year earlier than previously expected.

For context, Trufin’s guidance on 6 December 2024 was for full-year revenue of £46m and a pre-tax loss of £1.5m. So performance during the final month of the year must have been pretty outstanding – a good example of the way a big hit can transform results for games producers.

Today’s upgrade is said to have been driven by “exceptional year-end performances” from games Balatro and Abiotic Factor, both published by the company’s Playstack subsidiary.

Balatro is said to have won several industry awards in December, which helped to “significantly boost sales of the game” during the month.

Playstack is one of Trufin’s three operating subsidiaries. The other two can be classed as financial/payments businesses. Today’s update also includes an update on the 2024 performance of each of these.

Oxygen Finance Group: this business provides an early payments service that lets organisations pay their suppliers more quickly. It’s focused on the public sector.

Revenues rose by 21% to “no less than £7.5m” during 2024. EBITDA rose by 65% to no less than £2.1m (FY23: £1.3m).

Oxygen signed up four new early payment clients (EP) in 2024 and all four renewals due signed up for further five year terms. The business ended the year with a record 62 EP clients and says 82% of the next five years’ EP revenues are already contracted.

In his comments, Trufin CEO James van den Bergh commends Oxygen’s newish CEO and notes this is the first year the business has been able to benefit from its “inherent operational gearing”.

Satago Financial Solutions: this invoice factoring business lost a major contract with Lloyds Bank in July. This is said to have been “an enormous shock”.

Satago has since “aggressively realigned its cost base” and is in “advanced talks” with other potential Tier One bank customers.

As a result of the contract loss, 2024 revenue is expected to fall by 37% to “no less than” £2.4m, with a pre-tax loss of no more than £4.9m (FY23: £(4.2m)). The company expects to be able to bounce back from this setback over the next 18 months:

Satago has a fully costed and funded plan to achieve cash flow breakeven in the next 18 months.

Cash: Trufin expects to report a year-end gross cash position of at least £14m, including £12.5m of unrestricted cash. Panmure notes that this is double their previous estimate of £7m.

Outlook: today’s update does not include any new guidance for 2025, other than this somewhat cautious sounding statement:

Although we expect 2025 to be a year of consolidation, we will maintain our disciplined approach to allocating internal resources and expect the Group to grow all the profitability lines in 2025 and beyond.

House broker Panmure Liberum (many thanks) has updated its FY24 forecasts today to suggest earnings of 1.2p per share for 2024.

FY25 and FY26 forecasts have been left unchanged at 1.9p and 4.6p per share, respectively.

Roland’s view

With Trufin shares trading at 90p as I write, broker forecasts price this stock on a lofty 75x 2024 earnings, falling to 47x in FY25 and 20x in FY26.

Playstack’s performance last year also seems impressive. But as we’ve seen with numerous other listed games companies over the last couple of years, results can be volatile and are dependent on a regular supply of successful new games.

However, I can see the potential for the Oxygen Finance business to deliver a lasting improvement in group profitability and cash generation if it can continue to add new clients.

One further attraction for me is Trufin’s net cash position. In addition to providing some protection for equity holders, this should allow the company to invest for growth on favourable terms.

Trufin seems to be performing well, but my feeling is that there’s already plenty of progress priced in. At this stage, I’m happy to retain our neutral view – AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.