Good morning! Let's see what's in store for us today.

11:30: wrapping this up here, thanks everyone! Another clean sweep!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| BP (LON:BP.) (£69bn) | None | Noted activist investor Elliott Management has built a stake in BP, according to press reports. | AMBER/GREEN (Roland) |

Porvair (LON:PRV) (£316m) | Final Results | Revenue +9% to £192.6m, op profit +8% to £22.8m. Trading mixed, 2025 outlook optimistic. | AMBER/GREEN (Graham) Not too much has changed since my last review. Underlying sales growth is now positive and a new CEO will take charge in 2025. A nice company, valuation somewhat full. |

Filtronic (LON:FTC) (£203m) | Further contract win with SpaceX | £16.8m contract for FY25 and FY26. Both years now expected to exceed current market exps. | AMBER (Roland) |

Likewise (LON:LIKE) (£48m) | TU & Acquisition of Logistics Centre | Positive start to 2025, revenue +8.4%. £1.2m acquisition near Plymouth completes UK coverage. | AMBER (Roland) |

EnSilica (LON:ENSI) (£47m) | Interim Results | “Solid” H1? Rev fell slightly (£9.3m) and negative EBITDA (£0.2m). H2 weighting expected | AMBER/RED (Graham) I'm not RED on this because I presume that ENSI's customers would not be awarding contracts and funding to a supplier that was in danger of going bust. |

Zinc Media (LON:ZIN) (£15m) | TU | Rev below exps, but adj. EBITDA +50% to £1.5m, in line. Excellent momentum into the new year. | AMBER/RED (Graham) Taking a more lenient view on this as it does not seem to be distressed currently, but the net cash balance is thin and the long-term financial track record is terrible. |

| LifeSafe Holdings (LON:LIFS) (£3.5m) | Business Outlook | The fire safety tech business is hoping for an €800k order in “coming months” and £800k contract over next two years. But no certainty of either yet. | RED (Roland) [no section below]. Shares down 90% since 2022 float. Appears subscale and loss-making. Some hope of a transformative deal but looks speculative and risky to me. |

| Supply@Me Capital (LON:SYME) (£2m) | Funding Update | “Given the cash flow pressure…the Board is actively exploring alternative funding options”. Waiting on related party loan funds from CEO’s other company which itself needs restructuring. | RED (Graham) [no section below] |

Graham's Section

Porvair (LON:PRV)

Up 2% to 692p (£322m) - Full Year Results - Graham - AMBER/GREEN

Porvair plc ("Porvair" or the "Group"), the specialist filtration, laboratory and environmental technology group, announces its results for the year ended 30 November 2024.

This looks a solid set of results from PRV. The headlines:

Rev +9% to £193m, +13% at constant currencies.

Adj. op profit +8% to £24.5m.

Op profit +8% to £22.8m

The adjustments to the profit figures are reassuringly light.

Even statutory PBT comes out at £20.9m, not far off the adj. PBT figure.

I think these results are slightly above consensus estimates, although the announcement does not confirm this.

Please note that acquisitions have boosted performance and so none of these figures are organic or “underlying”.

As we saw the last time I covered PRV, the company doesn’t mention underlying sales growth in its headlines.

You have to get into the footnotes of today’s report to find PRV’s underlying revenue at constant currencies. It turns out that growth according to this metric is just below 4% (£166.5m vs. £160.3m last year).

So once again I have to observe that underlying sales growth was limited. The company emphasises that trading conditions were “mixed” with “some end-market inconsistency”.

Then again, if the company can afford to make acquisitions and if growth is more attractive as long as those acquisitions are included in the results, should investors really care about weak organic growth? Perhaps not! But I think it’s good to understand where the headline growth is really coming from.

Final dividend gets a small increase to 4.2p, total dividend for the year 6.3p.

CEO comment:

"Trading conditions were mixed, with strength in aerospace and petrochemical markets offsetting weakness in laboratory and industrial consumables. The Group's strategy, unchanged since 2004, continues to deliver consistent results despite some end-market inconsistency. The Group focuses on markets with long-term secular growth drivers: tightening environmental regulation; the growth of analytical science; the need for clean water; the development of carbon-efficient transportation; the replacement of plastic and steel by aluminium; and the drive for manufacturing process quality and efficiency.

I note that the CEO is retiring this year; he has been in this position since 1998! But true to form, PRV is well set up with a “Chief Executive Designate” who has already joined the Board. The Designate’s most recent role is COO at Hill & Smith (LON:HILS).

In a review of the past 20 years, the retiring CEO highlights PRV’s achievements including compound growth in EPS of 13% and growth in the share count of less than 1% p.a.

It doesn’t happen often enough that companies use low growth in their share count as a metric of success! A stable or declining share count is one of the first things I look for when I’m making an initial assessment of any company. Bravo to PRV for keeping its share count stable over the long-term and for pointing this out.

Net cash: finishes the year very slightly lower than last year, just below £14m.

Checking the cash flow statement to confirm PRV’s explanation for the lack of growth in net cash, I see the following items:

£10m spent on acquisitions

£5m on capex (my impression is that this is mostly replacement capex, not growth capex)

£3m on dividends

£2m on pensions

It seems to me that most of these items could be classified as voluntary, except for the capex, so I would see true cash generation as c. £15m.

Contributions to the pension scheme are temporary, as the deficit is v. low at around £6m.

Also, the company's cash balance was held back by a large (£7m) growth in receivables - perhaps this might reverse in 2025?

Outlook: the CEO reiterates his belief in the company’s long-term strategy, and has this to say about the current year:

In the nearer term there is much to look forward to in 2025: new product introductions in aerospace, Seal Analytical and Kbiosystems; the installation of a new manufacturing line for aluminium filtration; industrial demand recovery in the US; and increased Laboratory in-house manufacturing through Hungary.

Graham’s view

I was AMBER/GREEN on this last July at a share price of 676p.

At 692p today, I think I can leave my stance unchanged.

I do admire PRV’s consistency and its stable share count over the long term.

It has an admirable track record of paying progressive dividends for many years.

The strategy of focusing on particular filtration/environmental markets has worked and continues to work.

Given all of its positive characteristics, I’m inclined to keep my positive stance on the share. However, I have to dock it some points for a) the limited organic growth, and b) the fact that the valuation does a good job of reflecting its past success.

Perhaps if its end-markets can recover, we could finally see it breaking higher out of this 500p-700p range?

Zinc Media (LON:ZIN)

Up 7% to 66.25p (£16m) - Trading Update - Graham - AMBER/RED

Zinc Media Group plc (AIM: ZIN), the award-winning television, brand and audio production group, is pleased to announce a trading update for the period ending December 2024, subject to audit.

We very rarely cover this one. Paul gave it a scathing review last year on the basis that the messaging from management simply didn’t match up with reality.

It has a long history which goes back to Ten Alps (TAL), co-founded by Bob Geldof, that produced shows like Panorama and Dispatches.

Today we learn that 2024 EBITDA is £1.5m, in line with expectations.

However, revenue has apparently missed expectations at £32m, vs. £40m last year and a Singers forecast for £34m.

The fall in revenues reflects a disposal, business closures and “some opportunities moving into the new financial year which have now been commissioned”.

There is gross cash of £6.3m and net cash of £1.3m. The net cash figure is very slightly below forecast (£1.5m). Most of the debt seems to be in the form of shareholder loans, without covenants.

CEO comment:

The Group has undergone an exceptional transformation in recent years… focused the Group on its higher margin television and content production, whilst broadening its offering in this sector; positioning the Group for further growth.

The start of the new financial year has been excellent, with a slew of new, high-profile commissions and launches including the BBC documentary Israel and the Palestinians and a new multimillion pound primetime quiz show, The Inner Circle, hosted by Amanda Holden. Forward bookings for the current year are well ahead of the same time last year, and we have a strong pipeline for the year ahead…

Outlook: ZIN has won £16m of work in the last five months, and has £21m of revenue secured for FY25, up 24% compared to last year.

Graham’s view

Checking the forecasts again (with thanks to Singers), I see that adj. PBT for 2024 is expected to come in close to breakeven (£0.2m), so it’s only marginally profitable in real terms.

For 2025, adj. PBT is expected at less than £1m, which in my book is still not a meaningful level of profitability for a listed company.

And this is a concern because if it does generate £40m+ of revenues, as forecast, then I’d like to think that some of this might be left over for shareholders after all costs. Especially if the company is now focused on “higher margin” work.

But TV production is a people business. ZIN’s staff must be paid for their efforts. I doubt that trying to save on staff costs in order to leave a profit for external shareholders would be a winning strategy.

And it’s not a strategy that they’ve tried before:

The company has raised new equity from time to time but at this stage it looks to have been a case of throwing good money after bad.

I’m toying between RED and AMBER/RED on this.

Why be RED:

A long history of unprofitability, and no meaningful profitability expected soon.

Doesn’t look like it owns any intellectual property. A people business.

A very thin net cash balance

Assuming that the net cash balance fluctuates from time to time, the company would be unable to repay its shareholder loans without finding another form of finance elsewhere. At least until profits and cash generation improve.

Why be AMBER/RED:

The new strategy is supposed to be more focused

The recent acquisition might improve performance possibly?

Revenues are supposed to increase 20%+ this year and the order book seems to support this.

Does not seem to be distressed currently.

I think I’ll go AMBER/RED on this, but it’s a really close call. I like to reserve RED for cases where there is current financial distress or a serious fundamental problem. It seems to me that ZIN is just a poor-quality business with a weak balance sheet. Maybe its performance can improve a little this year and it could give us a positive surprise at last. AMBER/RED it is.

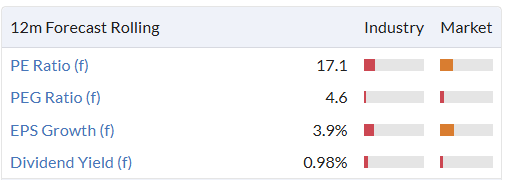

EnSilica (LON:ENSI)

Down 11% to 43.5p (£42m) - Unaudited Half Year Results - Graham - AMBER/RED

EnSilica (AIM: ENSI), a leading chip maker of mixed-signal ASICs (Application Specific Integrated Circuits), announce its unaudited results for the six months ended 30 November 2024…

We already looked at this a week ago, on a contract award, and it’s back today with interim results.

This is another stock I upgraded from RED to AMBER/RED, as I figured that ENSI’s customers (such as the UK Space Agency) must have done some due diligence on their supplier’s ability to execute contracts. Even though the company did not appear to be financially very strong to me, its customers must have faith.

Today’s interim results show revenues of just £9.3m (H1 last year: £9.6m) which leaves the company with a mountain to climb in order to hit full-year forecasts. Singers had previously pencilled in £30m of revenue for FY May 2025. They have today cut this forecast to £28.2m.

Similarly, the adj. EBITDA forecast gets a shave from £4.8m to £4.1m, and the adj. PBT forecast gets lowered from £2.5m to £1.8m.

The CEO describes H1 as a “solid start”, which I’m not sure I totally agree with. He points to progress on contracts and highlights the potential SpaceX opportunity:

"We have made a solid start to 2025, securing a further five design and supply ASICs contracts, and we remain confident of securing additional mandates across the remainder of the financial year. Our NRE and chip supply revenues from these new contracts alone are expected to generate a further £100 million of revenues over their lifetime, starting from 2027 onwards, further cementing our growing financial base…

Our ongoing progress has been further highlighted by the recently announced £10.4 million of funding from the UK Space Agency… This funding will enable our team to advance our position and competitiveness as a key supplier of silicon chips for user terminals across the various new satellite constellations, offering an alternative to SpaceX's Starlink service."

Chasing SpaceX contracts seems to be a good strategy for listed companies!

Net debt: the company doesn’t make its financial position obvious in the commentary, you have to get into the footnotes to find the details.

Net debt is £4.9m, up by about £1m year-on-year.

The value of loans outstanding is up by £2m, and this is not matched by an increase in cash. The lender is the Bank of Scotland.

So again it looks financially shaky to me. But its customers don’t seem to mind, and hopefully their funding will enable ENSI to carry on without interruption?

We get a going concern analysis, which concludes with the Directors (not the auditors) saying that they are happy with the company's ability to continue as a going concern. But I note that one of the reasons this give for this point of view is “the Company's history of being able to access capital markets as evidenced by the raising of £5.2 million gross equity in May 2024”. So I certainly wouldn’t rule out another equity fundraise.

Graham’s view

I was AMBER/RED on this very recently and I’m not inclined to change my view today, although make no mistake: this is a poor set of results and is effectively a profit warning. But I’ll stay AMBER/RED on ENSI for now.

Roland's Section

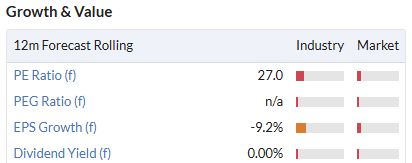

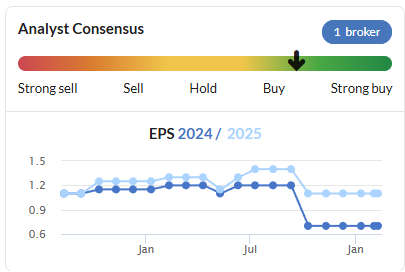

Filtronic (LON:FTC)

Up 11% to 103p (£225m) - Further Contract Win with SpaceX - Roland - AMBER

Results from this radio technology business have been transformed by its relationship with Elon Musk’s firm SpaceX. Today we have news of a further contract win and an upgrade to expectations.

Filtronic plc (AIM: FTC), the designer and manufacturer of products for the aerospace, defence, space and telecoms infrastructure markets, is pleased to announce a significant new contract win with SpaceX valued at $20.9m (£16.8m), to be fulfilled in both FY2025 and FY2026.

As a result, expectations are being upgraded for both FY2025 and FY2026:

the Board is now confident the business will exceed current market expectations for revenue and profit in both FY2025 and FY2026.

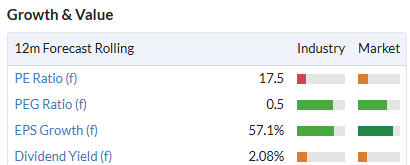

Estimates: Filtronic’s financial year ends on 31 May, so FY25 is around three quarters complete.

Reading the RNS, my initial thought was that adding £16.8m to the next 16 months would be a very significant upgrade for a business with annual revenue under £50m. However, I had to question whether any of today’s contract news might already have been factored into forecasts.

Filtronic has not provided any information on revised expectations today. However, investors with access to broker notes are able to get more insight. With thanks to Cavendish, updated forecasts are available today on Research Tree.

Cavendish’s analysts have increased revenue forecasts for FY25 and FY26 by 4.1% and 4.9% respectively. They’ve left their price target unchanged at 110p.

Forecasts for adjusted earnings per share have been increased as follows:

FY25E: 5.0p per share (+4.2% from 4.8p previously)

FY26E: 3.2p per share (+6.7% from 3.0p previously)

The shares have risen by 11% this morning at 08.30, meaning that Filtronics shares have become more expensive relative to expected earnings. I calculate a FY25E P/E of 21.5, rising to FY26E P/E of 32.

Roland’s view

Today’s news is certainly positive for Filtronic and its shareholders. But objectively it only appears to be a modest beat of existing forecasts.

My sums suggest the following revisions to Cavendish’s revenue forecasts today:

FY25E: £50.4m (previously £48.4m)

FY26E: £43.0m (previously £41.0m)

In total, this represents a £4m increase in forecast revenue. This seems to suggest that £12.8m (c.75%) of today’s contract award was already factored into analysts’ forecasts, prior to today.

Filtronic is undoubtedly trading well and boasts excellent quality metrics. But the concerns around forward visibility and customer concentration that I raised in my last comment (4 Feb 25) are unchanged for me.

This may be an unpopular choice, but I continue to think that the share price is largely up with events for now. I’m going to maintain my view at AMBER today.

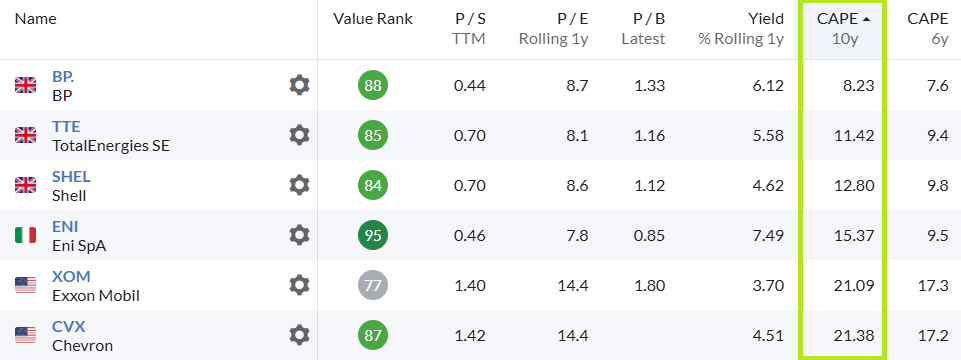

BP (LON:BP.)

Up 8% to 468p (£75bn) - Elliott Management stake - Roland - AMBER/GREEN

Shares in FTSE 100 oil major BP are up by around 8% this morning, after press reports over the weekend revealed that well-known US activist investor Elliott Management has taken a stake in the business.

The size of the stake has not been disclosed, but a source quoted in Bloomberg suggested it was “significant”. Newswire items like this are available on the News tab of the StockReport - e.g. here.

There’s no official comment on Elliott’s objectives but it’s suggested that Elliott sees BP as “undervalued” and will urge the company to “consider transformative measures”.

BP’s challenges have been much discussed in the press recently, together with its potential to become a takeover target. Even The Guardian had a piece over the weekend.

Some analysts suggest the business is trading below its fair value, on a sum-of-the-parts business. A greater focus on the upstream division (oil and gas production) might improve both valuation and profitability.

The company’s 2024 results are due to be published tomorrow (11 Feb) and BP is hosting a Capital Markets Day on 26 February. This was postponed from the 11th to allow CEO Murray Auchincloss to recover from a planned medical procedure.

BP has already talked about the potential for further disposals – I imagine we’ll learn more on 26 February.

Roland’s view

BP’s share price has certainly underperformed key rivals over the last five years:

One metric I like to use with these large, cyclical companies is the CAPE ratio, or Price/10yr average earnings. This can be useful to see through the variability in profits from commodity production and gain a more objective view on valuation.

Stockopedia provides this measure in its Value table view. We can see that BP is trading at a significant discount to key rivals:

BP’s CAPE 10y of 8.7 (prior to today) suggests possible value, in my view.

However, the group’s falling profits and relatively high leverage have led some analysts to speculate that BP’s current share buyback and dividend programme might become unsustainable over the coming year.

BP is large and complex and faces the additional challenges of geopolitical risks and the energy transition. However, I would be inclined to share Elliott’s view that the company could be undervalued, given the underlying quality and profitability of its core units.

This isn’t a detailed review, but on balance my view is that BP shares are probably quite reasonably valued at current levels. AMBER/GREEN.

Likewise (LON:LIKE)

Unch. at 19.3p (£48m) - Trading Update & Acquisition of Logistics Centre - Roland - AMBER

This fast-growing flooring distributor has issued its second trading update in just over a month today. Graham covered January’s full-year update here. Today we learn that 2025 has got off to a relatively strong start:

Likewise has made a positive start to 2025, with total sales revenue increasing by 8.4% in January and Likewise Branded businesses increasing by 13.6%.

For context, total sales revenue rose by 7.5% in 2024.

Likewise has also completed its geographic coverage of the UK, with the acquisition of a new warehouse for £1.2m near Plymouth. This purchase was funded from internal cash resources.

The new Logistics Centre will both establish Likewise South West and also enable Valley Wholesale Carpets to develop business with customers in Devon and Cornwall.

This purchase takes the reported value of the group’s freehold property portfolio to £23.3m. A focus on freehold property is one factor CEO Tony Brewer appears to be determined to replicate from his former employer Headlam.

Likewise’s £23m property portfolio provides asset backing for half its market cap and just under one-third of its £75m enterprise value:

Outlook: 2025 forecasts are unchanged today, according to an updated note from house broker Zeus.

Revenue is expected to rise by 6.1% to £160m in 2025, supporting a 57% increase in net profit to £3m, or adjusted earnings of 1.1p per share.

In today’s update, the company says it has “extensive product launches planned for Q1 and Q2”. It’s aiming to “materially increase market presence in independent flooring retailers and contractors”.

CEO Tony Brewer continues to sound excited about the prospects for his business:

The momentum developed in H2 2024 has continued in the early part of 2025 providing the Group with confidence in an exciting future and further progress towards our medium term objectives

Roland’s view

Likewise is led by an ex-Headlam manager. His strategy appears to be to try and eat Headlam’s lunch. Recent share price action has certainly favoured the fast-growing upstart over the incumbent:

However, everything has its price. This sector is not exactly booming at the moment. I think it’s worth noting that Likewise’s Valley wholesale division – an established business it acquired – saw sales fall by 3% last year.

Low profit margins and (so far) very low returns on capital suggest to me that Likewise shares are probably up with events at current levels:

Graham took an AMBER view on Likewise in January. I see no reason to change this today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.