Good morning! It has been a busy week for updates, let's see what's in store for us today.

And we'll kick things off with a backlog section from Mark on AVAP.

Spreadsheet that accompanies this report: updated to 14/2/2025.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

London Stock Exchange (LON:LSEG) (£61.3bn) | Final Results | Total rev +5.7%, adj EPS +12.2%. Equity FCF of £2.2bn. 2025 exps for >£2.4bn FCF, higher margins. | |

CRH (LON:CRH) (£54.6bn) | Final Results | Rev +2%, net income +15% with higher margins. 2025 outlook +ve, w/ “supportive underlying trends”. | |

Rolls-Royce Holdings (LON:RR.) (£53.6bn) | Final Results | Adj op profit +54% to £2.5bn, FCF of £2.4bn. Net cash £475m. 2025 guidance for £2.7-£2.9bn FCF. | AMBER (Roland) [no section below] |

HALEON (LON:HLN) (£35.8bn) | Final Results | Org rev growth +5%, adj op profit +9.8%. FCF of £1.9bn. 2025 outlook for org revenue +4%-6%. | |

Aviva (LON:AV.) (£14.1bn) | Final Results | GWP +11.9% to £12.2bn, adj op profit +20% to £1,767m. Dividend +6.9% to 35.7pps. | |

WPP (LON:WPP) (£8.3bn) | Prelim Results | Underlying rev -1% LFL. Adj op profit +2% LFL, margin 15.0%. Divi held. 2025 outlook H2 weighted. | |

St James's Place (LON:STJ) (£6.2bn) | Final Results | Adj net profit +14% to £447.2m, net inflows £4.3bn, y/e FUM £190.2bn. Dividend -25% to 18p. | |

Howden Joinery (LON:HWDN) (£4.6n) | Final Results | Rev +0.5% to £2,322m, op profit -0.3% to £339m. 2025 outlook “challenging”. Targeting mkt share. | |

Taylor Wimpey (LON:TW.) (£4.1bn) | Final Results | 2024 new homes -2.3% to 10,593, op profit -11.5%. ASP -1.5%. 2025 outlook in line with market exps. | AMBER/GREEN (Roland) [no section below] TW delivered an improved sales rate from a reduced number of sites last year but now seems to be positioning for a return to growth. The order book at 23 Feb was 8,021 homes, up from 7,402 last year and pricing is now said to be flat YoY. Net cash of £565m is reassuring, but is being used to subsidise the uncovered dividend. With the shares trading slightly below NTAV of 124p, I’m cautiously positive despite subdued profitability. |

Hiscox (LON:HSX) (£3.8bn) | Final Results | GWP +3.7%, PBT +9.5% to $685m. ROE 19.8% (2023: 21.8%). 2025 outlook positive. | |

Ocado (LON:OCDO) (£2.8bn) | Final Results | Group rev +14.1%, adj EBITDA +197% to £153.3m. £224m cash outflow, exp +ve cashflow in FY26. | |

Man (LON:EMG) (£2.6bn) | Final Results | AUM +0.7% $168.6bn. Inv perf +1.0%. Net outflows $3.3bn. NTAV $867m. EPS +29% to 25.1 cents. | |

Shaftesbury Capital (LON:SHC) (£2.5bn) | Final Results | EPRA NTAV +5.2% to 200.2pps/£3.7bn. Portfolio +4.5% LFL. Adj EPS +16.2% to 4.0p. | |

Greencoat UK Wind (LON:UKW) (£2.5bn) | Final Results & £100m buyback | NAV -10% to £3.4bn/151.2pps. Dividend held at 10p. Targeting 10.35p for FY25, £100m buyback. | |

Drax (LON:DRX) (£2.3bn) | Final Results | PBT -5.4% to £753m. DPS +12.6% to 26p. FY25 adj EBITDA outlook in line with consensus. | |

Derwent London (LON:DLN) (£2.2bn) | Final Results | EPRA NTAV +0.6% to 3,149pps. Total return 3.2%. Div +1.3% to 80.5p. FY25: 3-6% rental growth. | |

Serco (LON:SRP) (£1.3bn) | Final Results | Rev £4.8bn, adj op profit +10% to £274m. 2024 guidance for flat revenue, efficiency gains. | |

Genus (LON:GNS) (£1.2bn) | Half-Year Results | H1 rev +1%, op profit +22%. Mkt stable. FY25 outlook in line with recently upgraded expectations. | |

Cairn Homes (LON:CRN) (£1.1bn) | Final Results | Rev +29%, op profit +32% to €150m. ROE 15.1% (LY: 11.3%). 2025 to be another strong year. | |

CVS (LON:CVSG) (£758m) | Interim Results | LfL sales growth -1.1%. Leverage 1.66x. Outlook: in line. Prioritising Australia until CMA finishes work. | AMBER/GREEN (Roland) [no section below] |

Metro Bank Holdings (LON:MTRO) (£658m) | Final Results | Net income £42.5m, includes tax gain. Underlying profit in H2 beats guidance of profitability in Q4. | |

PPHE Hotel (LON:PPH) (£547m) | Final Results | Like-for-like rev +3.3%. PBT £30.6m (LY: £28.8m). Occupancy 74.5%. NRV per share £27.51. | GREEN (Graham) [no section below] Still trading at only 50% of its official NRV (net realisable value) per share. The question is whether this value is meaningful. Nice upward trend in occupancy although there is a lack of progress in terms of RevPAR (revenue per available room). Four new hotels have opened with another due in March 2025 and as these mature we should see this reflected in future EBITDA/PBT growth and hopefully in the NRV, too. The new hotels negatively impacted 2024 results which is considered normal for the pre-opening phase. I still find this very interesting. Net debt of £750m needs to be managed. |

Serica Energy (LON:SQZ) (£489m) | OFAC Licence Renewal | OFAC license & assurance relating to Rhum field is renewed to Feb 2027. | |

Jupiter Fund Management (LON:JUP) (£439m) | Final Results | “Resilient”. PBT £97.5m (LY: £105.2m). Net outflows £10bn+. AUM down 13% to £45bn. | GREEN (Graham) Excellent profit margins despite awful sentiment, and a market cap that’s mostly covered by balance sheet strength. I feel obliged to keep my contrarian stance alive. |

Brooks Macdonald (LON:BRK) (£236m) | Half-Year Results | H1 “solid”. Anticipates full year performance in line with expectations. | |

Macfarlane (LON:MACF) (£172m) | Final Results | Rev -4% (£270m), PBT +3% (£20.9m). 2025 to be challenging, positioned for profitable growth. | GREEN (Roland) |

hVIVO (LON:HVO) (£108m) | Acquisition | £3.2m acq. of storage solutions provider (bio & clinical materials). £2.7m cash, £0.5m equity. | |

Winking Studios (LON:WKS) (£75m) | Prelim Results | Rev +8.9% ($31.9m). Adj net profit -10% ($3.4m). Outlook: strong project pipeline. $20m acquisition. | |

K3 Business Technology (LON:KBT) (£45m) | Final Results | In line. Reduction in revenue was expected. ARR -1% to £16.7m. Cash breakeven from March. | |

Polarean Imaging (LON:POLX) (£16m) | FY TU | Rev $3.0-3.1m, exceeding upper end of guidance. Cash $12.1m, giving runway through Q1 FY26. | |

ITIM (LON:ITIM) (£13m) | TU | Revs up to £17.9m, EBITDA and cash significantly ahead of exps at £2.5m and £3.8m respectively. |

Backlog

Avation (LON:AVAP)

140p (£94m) - HY Results - Mark (I hold) - AMBER/GREEN

Everything seems to be going in the right direction here:

· Revenue and other income increased to US$55.4 million (2023: US$46.3 million) displaying continued business momentum;

· EBITDA increased to US$55.6 million (2023: US$38.3 million) demonstrating enhanced cash generation;

However, the rise appears to be largely due to how maintenance is accounted for:

We adjust our forecasts to account for non-cash movements, as well as incorporating the additional revenues and costs from the A320 purchased. As a result, our revenue expectation in FY25E increases to $102.3m (from $94.8m), this also reflecting maintenance reserve revenues, leading to PBT of $0.9m (from $7.4m) after non-cash movements, with our net debt forecast increasing to $624.4m, reflecting the acquisition of the A320, partly offset by the strong cash performance. For FY26E, we look for revenue of $99.7m (from $95.8m), leading to PBT of $8.4m (from $8.1m).

All of this makes it perhaps more important to focus on cash flow rather than accounting earnings, and here things look better:

Given the debt, we really need to be looking on an EV basis. Annualising the OCF works out to be 6.7x EV/OCF after taxes & financing, so this appears to be good value on that basis. There is also the potential for the finance expense to reduce over time. Earlier this month, the company said that refinancing $85m of debt would lead to $4.8m of improved annual cash flow. Any additional refinancing could be material and will not be in forecasts.

Despite the strong cash flow, the dividend paid to shareholders is very low, with the money instead spent on debt reduction and further building their fleet. In light of this, the acquisition announced today was perhaps not the one shareholders wanted (many AVAP shareholders would prefer to read about the sale of the company to a larger aircraft lessor):

…it has entered into an agreement to acquire an Airbus A320 on lease to Etihad Airlines. This secondary market transaction adds a high credit quality airline to Avation's customer list and further enhances Avation's narrow-body aircraft fleet.

Regardless of the strategic value of this move, I can’t help feeling that with a NAV per share of £2.94 vs a share price of £1.43, they would have been off buying back their own shares in the market. To be fair, they did buy back 10% of their shares in a single transaction at around 50% of NAV at the end of last year. However, the market would perhaps appreciate a more regular purchase schedule.

Mark’s view

While the assets are not particularly productive based on accounting earnings, and even less so following today’s downgrade, the operating cash flow is strong. There is also the catalyst that debt is being refinanced at lower rates that should drop through to the bottom line. When I looked at this in December, it just seemed too cheap on an asset basis, and I see nothing in these results that changes that. AMBER/GREEN

Graham's Section

Jupiter Fund Management (LON:JUP)

Down 4% to 77.5p (£423m) - Annual Financial Report - Graham - GREEN

I haven’t looked at this since July, although Roland and Mark have looked at it since then.

What’s striking to me about today’s results is the profitability that is achievable despite enormous outflows and dire sentiment in the sector.

This is why I’ve been positive on the conventional fund managers. Even in those times of extremely poor flows - surely the worst in the history of the UK asset management industry - they remain profitable, with profit margins far in excess of that which many other industries can achieve.

Today’s results from Jupiter highlight this point.

We have an underlying PBT of £97.5m, down by 7% from £105.2m the previous year.

We have statutory (i.e. unadjusted) PBT of £88m.

This has been achieved despite a horrendous net outflow of £10.3bn, about a fifth of the year’s starting (£52.2bn).

The company does acknowledge that its underlying profit margin has taken a hit, with a “cost: income ratio” of 78%, up from 73% the prior year.

Broadly speaking, if this gets to 100%, it means that administrative expenses are eating up all of the company’s net revenues.

Also, the net management fee margin has reduced from 70 basis points (0.7%) to 65 basis points (0.65%). Fee erosion is an important theme in the sector. As most active fund managers struggle to match, let alone beat, the performance of low-cost ETFs, there is a natural downward force on the fees they can charge.

But still, I go back to that enormous profit margin of £97.5m (underlying PBT) from net revenues of £364m. That’s a pre-tax margin of nearly 27%.

And as a rule, fund managers never have an issue converting their profits into cash. Customers are in no position not to pay, as their liquid assets are available to make immediate payment of fees.

What I'm looking for from fund managers in this environment is a drive for simplicity. The way I see things, one of the main problems with the industry is that there are too many funds. So simplicity is the way forward, I think.

Comment from CEO Matthew Beesley, whose overall strategic direction has been very good in my view:

We have made material progress to better position Jupiter for future success and have progressed in each of our strategic objectives… The actions we took during the last year, together with improving performance and encouraging early signs this year, give us confidence that we will see near-term growth in the majority of our investment capabilities.

We have again delivered on costs, demonstrating strong discipline in non-compensation costs and finishing the year with fewer than 500 FTEs, our fourth year of headcount reduction and lowest level since 2016.

Dividends: the proposed final dividend is 2.2p, so that total dividends for the year are 5.4p.

Total dividends last year were 9.8p, including a final dividend of 3.4p. So this is a significant reduction.

Was it necessary to cut the dividend so much?

Underlying earnings per share were 13.4p (previous year: 14.8p). Actual earnings per share on the income statement were 12.5p.

So in theory there was EPS available to pay a higher dividend than this. But their capital allocation policy is to pay out only 50% of underlying EPS (before performance fees).

Fortunately, the dividend is not their only use of surplus cash. They also announce a £13m share buyback which equates to a payment of 2.5p per share (I know that some readers will shudder when I equate a buyback to a dividend!).

In addition, there is £50m of debt that Jupiter is going to redeem early. It wasn’t set to mature until 2030.

Performance: sounds fine with 61% of mutual fund AUM outperforming its peer group over 3 years.

Graham’s view

This is a highly contrarian stance but I’m going to leave my GREEN unchanged.

The StockRanks concur:

The PER is 10x and that’s without making any adjustment for balance sheet strength. Today’s balance sheet shows equity of £834m of which tangible equity is £327m. This covers more than three quarters of the market cap.

Whether it stays alone or mergers with another fund manager to gain even more efficiency in terms of costs, I think this is a stock I have to remain positive on.

I concede that the share price has not cooperated with me yet. I’ve been positive on this for over two years now, and the stock has been unable to get out of this slump. If I’m wrong, this is a cigar with only a few puffs left.

Roland's Section

Macfarlane (LON:MACF)

Down 1.5% to 106p (£169m) - Annual Results - Roland - GREEN

We start 2025 with new-business momentum as customers increasingly recognise the added-value we can offer both on an environmental and cost-savings basis.

This buy-and-build packaging group features regularly in these pages. Today’s results may not be a vintage set of numbers, but they do not flag up any serious concerns for me.

The headline numbers for 2024 show improved profitability, despite a fall in sales:

Revenue down 4% to £270.4m

Operating margin: 8.7% (2023: 7.9%)

Pre-tax profit up 3% to £20.9m

EPS up 4% to 9.74p

Dividend up 2% to 3.66p

The company says that weak customer demand and selling price deflation affected both its distribution and manufacturing divisions. However, the distribution arm benefited from some new business and acquisitions:

Continued weak customer demand and selling price deflation have been partially offset by a strong new-business performance and the benefit of the acquisitions of Gottlieb in April 2023 and Allpack Direct in March 2024.

Improved operating margins were partly driven by changes in the fair value of deferred consideration due on acquisitions. But this seems a creditable performance to me, in terms of cost control.

Packaging distribution: In the larger distribution division, operating costs fell by 3% “through management action” and gross margin improved to 37.1% (2023: 35.7%).

Manufacturing: Macfarlane’s smaller (but higher margin) manufacturing business produces specialised packaging for industrial and other customers. It earned a gross margin of 43.2% last year (2023: 44.5%).

Although operating expenses rose by 14%, this was due to acquisitions. The company says underlying costs “are being well controlled”. I don’t see any reason to question this, given the group’s overall performance.

Balance sheet/cash flow: net bank debt stood at £1.9m at the end of December, after £15.0m of acquisitions and capital expenditure.

I estimate underlying free cash flow (excluding acquisitions) of £14.3m for 2024. This gives a very respectable 92% conversion from reported net profit of £15.5m.

Outlook: the company strikes a balanced note in its outlook statement, warning of cost pressures and a challenging environment, but also opportunities from new business.

The Group continues to invest in actions to grow sales both organically and through acquisitions. Despite the challenging market conditions the Group is well positioned to benefit from improvements in the macroeconomic outlook.

New Extended Producer Responsibility (EPR) legislation to improve packaging sustainability is expected to add cost. However, Macfarlane says it is working with its customers (in retail particularly) to help manage the impact of EPR.

I suspect EPR may be an opportunity for the company to demonstrate its value over smaller suppliers.

Estimates: with thanks to Shore Capital, we have updated earnings estimates for Macfarlane today:

FY25E EPS: 12.1p (previously 12.4p)

FY26E EPS: 12.3p (previously 12.6p)

These changes appear to be slight tweaks to underlying assumptions rather than an explicit downgrade - revenue expectations are almost unchanged.

Roland’s view

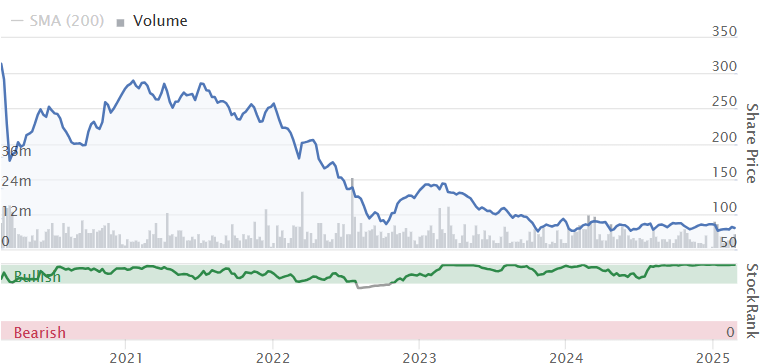

Macfarlane’s one-year chart looks poor:

But on a 10-year view, this is still an impressive growth story:

I don’t see any reason why this business can’t continue to progress well over the coming years.

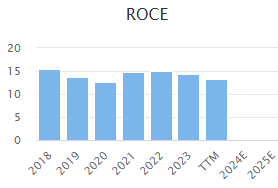

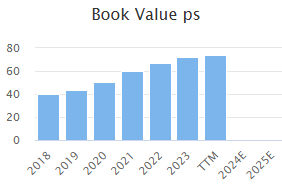

My sums suggest a return on capital employed of 13.7% for 2024. That’s consistent with prior years and high enough, in my view, to allow the group to self-fund growth and generate value for shareholders.

The two charts below show a picture I like to see – stable ROCE with rising book value per share, implying that a company is able to deploy new capital at stable rates of return:

Macfarlane also scores well with the StockRanks, in particular for quality and value:

The shares now trade on a FY25 forecast P/E of 9, with a useful 3.5% dividend yield. This looks a very reasonable valuation to me, underpinned by a well-run business and solid balance sheet.

I think Macfarlane remains attractive on a long-term view and am going to leave our previous GREEN view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.