Good morning all, the Agenda is there now!

1pm: we're all done for today.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Ashtead (LON:AHT) (£20.1bn) | 9M Results | Q3 rev -3%, adj. PBT -6%. Nine-month figures more positive. Full year results to be in line. | |

Intertek (LON:ITRK) (£8.3bn) | Final Results | Rev +6.6% at constant FX. 2025: mid-single digit growth, margin to grow to 18.5%+ (2024: 17.4%). | |

Beazley (LON:BEZ) (£5.7bn) | Final Results | PBT +13% to $1,423m. Net tangible assets per share 545.9p. Share buyback for $500m. | |

Fresnillo (LON:FRES) (£5.6bn) | Final Results | Rev +26.9% ($3.6bn). $550m divi. 2025 production might be lower: 49-56 moz silver, gold 525-580koz. | |

Direct Line Insurance (LON:DLG) (£3.6bn) | Final Results | Ongoing operating profit £205m (2023: loss £190m). | PINK. Under offer. |

Abrdn (LON:ABDN) (£3.0bn) | Final Results | New 2026 targets: adj. operating profit >£300m (2024: £255m), net capital generation >£300m. | GREEN (Graham) Lovely news that they are changing their name back to the pleasant "Aberdeen". The 2026 targets are also encouraging, as are the improved net flows. Adjusted profits for 2024 have slightly beaten expectations. Shareholders can look forward to a constant dividend payout for now, until it's coverage has improved. All in all, it's a picture of improving health and positivity. |

Inchcape (LON:INCH) (£2.7bn) | Final Results | New med-term CAGR targets (compound growth rates). EPS >10% p.a. Volume +3%-5% p.a. | |

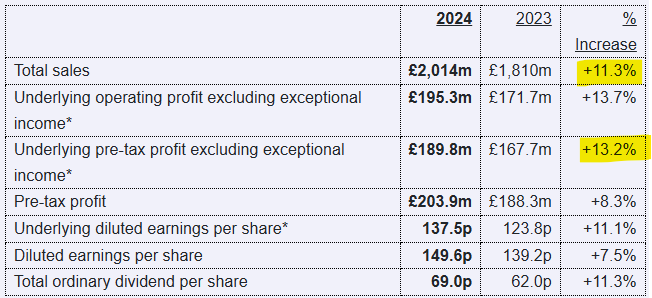

Greggs (LON:GRG) (£2.1bn) | Final Results | Sales +11.3%, adj. PBT +13.2%. LfL sales +1.7% in first nine weeks of 2025. Challenging Jan weather. | AMBER/GREEN (Graham) This is a risky decision but I'm leaving our stance unchanged despite another sharp fall on the back of declining short-term sales growth. Management assert that their expectations for the year are unchanged and still plan to hit their long-term sales growth next year. |

International Workplace (LON:IWG) (£2.0bn) | Final Results | Outlook: cautious. FY25 EBITDA $580-620m. Leverage to fall, BBB credit rating to be maintained. | |

Spirent Communications (LON:SPT) (£1.1bn) | Final Results | Rev -3%. Challenging market conditions, but a growing orderbook. Well-placed for 2025. | PINK. Under offer. |

Keller (LON:KLR) (£940m) | Final Results | Rev +4%, adj. op profit +22% at constant FX. Significant deleveraging. Multi-year buyback. | AMBER/GREEN [no section below] (Roland) |

Bakkavor (LON:BAKK) (£895m) | Final Results | LfL revenue +5.1%, adj. op profit +20.5%. 2025 rev to be “broadly” in line, adj. op profit to be in line. | |

Supermarket Income REIT (LON:SUPR) (£869m) | Proposed Mgt Internalisation | Using sale proceeds to insource mgt team for £19.7m. Exp £4m ann. savings; 19% yield on cost. | |

Apax Global Alpha (LON:APAX) (£660m) | Final Results | NAV -4.6% to €1.23bn/208pps. Decrease mainly due to PE portfolio. €69m of s’holder returns. | |

Johnson Service (LON:JSG) (£547m) | Final Results | FY24 in line. Outlook: £30m buyback, improved margins in FY25. Possible Main Market move. | AMBER/GREEN (Graham) [no section below] |

| Warehouse Reit (LON:WHR) (£360m) | Stmt re Possible Offer | Blackstone offered 110.5pps for WHR, its 4th proposal. Board has rejected. Sept ‘24 NAV 127.5p. | PINK (AMBER/GREEN) [no section below] (Roland) |

Reach (LON:RCH) (£275m) | Final Results | Rev -5%, but adj op profit +6% ahead of exps. Digital returned to growth. FY25 outlook in line. | GREEN (Graham) [no section below] This cigar butt stock keeps puffing out impressive profits (£102m adj. op profit, +6%) and cash flow (£107m adj. op cash flow). The dividend is maintained with a yield of over 8%. I also note £59m of contributions into pension schemes - these contributions “will materially step down… to around £15m in 2028”. My estimate of c. £200m of future pension contributions still seems about right (see January report). Non-pension net debt is only £14m. Total enterprise value including pension commitments is c. £500m or 5x adj. op profit. Like-for-like group revenue fell by a modest 4.2% in 2024. This continues to intrigue. |

Origin Enterprises (LON:OGN) (£261m) | Interim Results | H1 op profit +2.2% to €14.9m. Net debt €270.1m. “Too early to issue guidance for the full year”. | |

Kitwave (LON:KITW) (£223m) | Final Results | FY24 in line with exp. Rev +10% to £664m, adj op profit +6.3% to £34m. FY25 “started well” | AMBER/GREEN (Roland) |

Aquis Exchange (LON:AQX) (£194m) | FY24 TU | Profit warning. Heightened credit risk in respect of two clients. FY24 to be £3.7m below exps. | PINK. Takeover remains expected to complete in Q2. |

Synectics (LON:SNX) (£64m) | Final Results | FY24 results ahead of exps with adj PBT of £4.7m versus exp of £4.3m. FY25 estimates upgraded. | AMBER/GREEN (Roland - I hold) |

PCI- PAL (LON:PCIP) (£44m) | Interim Results | H1 revenue +26% to £10.6m. ARR +21% to £16.8m. H1 adj PBT of £0.2m in line with mgt exps. | |

Blackbird (LON:BIRD) (£23m) | Final Results | Rev -17% to £1.6m with adj EBITDA of £492k. Cash outflow of £3.8m. Net cash of £3.8m. | |

Tekmar (LON:TGP) (£9m) | Final Results | FY24 results in line with exps. FY25 EBITDA to be “consistent with FY24”, with H2 weighting. |

Graham's Section

Greggs (LON:GRG)

Down 11% to 1844p (£1.9bn) - Preliminary Results - Graham - AMBER/GREEN

Before getting into the bad news, we have very nice headline growth rates from Greggs this morning, for 2024:

The company points out - with evidence, if it was needed - that consumer confidence in 2024 was low, and that the food-to-go market wasn’t growing.

Despite the difficult circumstances, they can point to various growth achievements during the year:

Estate: the estate has increased to 2,618 shops with a net 145 openings during the year. Similar net openings are targeted in the current year, as they “continue to see clear opportunity for significantly more than 3,000 UK shops over longer term”.

App: The Greggs App scanned 20% of their company-managed shop transactions (up from 12.5% in 2023).

Delivery: delivery sales grew by 30%+ in 2024, from a low base.

Evening trade: post-4pm is the fastest-growing part of the day and is now 9% of company-managed shop sales.

We also have a trading update and this is where the shine starts to come off the announcement:

Like-for-like sales in company-managed shops increased by 1.7% year-on-year in the first nine weeks of 2025. Challenging weather conditions in January followed by improved trading in February

Confident that Greggs can manage inflationary headwinds and deliver another year of progress in 2025

The CEO’s report says that management expectations for 2025 are unchanged despite the above.

Roisin Currie elaborates on the outlook; I’ve tried to pick out the key points here.

Looking ahead to 2025, the macroeconomic landscape remains tough. Inflation remains elevated, and many of our customers continue to worry about the cost of living…

Despite a challenging food-to-go market, Greggs has demonstrated its ability to make positive progress and we remain confident that Greggs can and will continue to grow. The five-year strategic plan that we set out in 2021 is proving successful…

Increases in employment taxes will significantly increase our wage bill, and that of other retailers, in 2025, but we have dealt with significant cost inflation effectively over recent years and remain confident in our ability to manage the impact of cost inflation on the business. We are relentlessly focused on improving efficiencies which supports our position as a value-led brand. To the extent that we cannot mitigate cost inflation through savings, we recover it through careful pricing activity, which we strive to keep to an absolute minimum to ensure that we protect our reputation for offering great value.

I note that under the 5-year plan, the company planned to double sales by 2026, which I think means hitting £2.4bn. Consensus forecasts suggest that this will be achieved (£2.0bn in 2024, £2.2bn in 2025, and then £2.4bn in 2026).

Graham’s view

It’s clear that the slow growth figure for early 2025 has rattled confidence this morning.

I note that Megan covered this in January and reported on a clear, declining trend in like-for-like sales: from 7.4% growth in H1 2024, to 5% in Q3, to 2.5% in Q4.

And now it’s just 1.7% in early 2025.

It appears that Greggs is not immune to the economic climate, even if it does offer better value than most of its competitors. The entire food-to-go sector has slowed down and brought Greggs with it.

Perhaps I should downgrade our stance on this from Megan’s AMBER/GREEN. It’s a tough call as we haven’t had a clear profit warning today - management expectations for 2025 are unchanged, officially.

However, we have had a noteworthy drop in the share price this morning, and this follows another sharp fall in January. Don’t they say profit warnings come in threes?

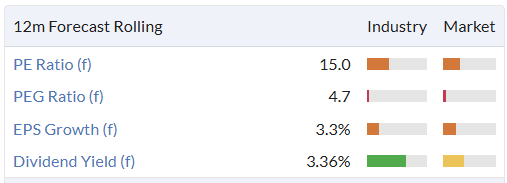

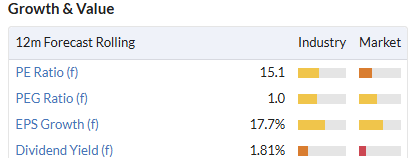

Valuation has been moderate, which makes it easy to take a positive stance on it as one of the most likely long-term High Street winners.

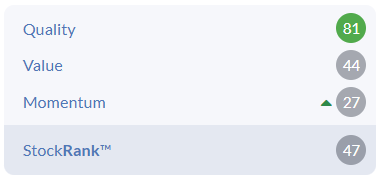

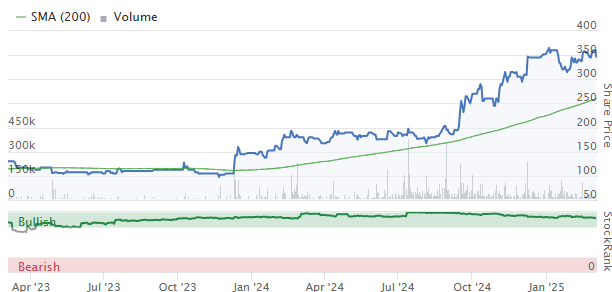

But the StockRank is neutral, mostly due to the weak momentum offsetting its high quality:

I’m unsure but on balance I’d like to leave our AMBER/GREEN stance unchanged. If you scroll out, the share price is back below the levels it first reached in 2019-2020. Sales were only £1.2bn in 2019, and the company could well double that figure next year.

Another point in its favour is £125m of net cash (before leases)..

The accounts are clean with few adjustments.

Quality metrics are very attractive, as reflected in the StockRank above.

I am therefore going to leave the AMBER/GREEN stance unchanged, while acknowledging that negative momentum could continue to hurt the share price in the short-term. We’ve had two sharp falls on RNS statements now, and the trend in terms of sales growth is negative. Hopefully we can see this turn around before too long!

Abrdn (LON:ABDN)

Up 11% to 179.4p (£3.3bn) - Final Results - Graham - GREEN

Abrdn have published a 7-part RNS with far too much detail for me to cover. But let’s just get a helicopter view of this investment giant - to help inform us when we might look at the smaller ones.

The big picture is that AUMA (assets under management and administration) are down by 6%, and adjusted net operating revenue is similarly down by 6%.

More positively, the net flows in 2024 were much better than in 2023. Net outflows were only £1.1bn, which is almost a rounding error when you have over £500 billion in AUMA (admittedly some of the improvement for the year relates to flows into low-margin liquidity funds).

Another positive is that the company made a small improvement (+2%) in adj. operating profit, despite lower revenues. It’s no surprise that cost management played a role: “This was driven by cost discipline, better markets and a strong performance by interactive investor.”

And the accounts are clean, with £251m in statutory pre-tax profit, almost matching the adjusted operating profit figure (£255m).

According to Refinitiv the consensus forecast was for £249m of adj. operating profit, so the company has beaten forecasts today.

But the best news is that they are changing their name! This must be why the share price is up over 10%, as they will no longer be a target of ridicule in the City:

"This is a Group to be proud of, with a promising future. We will deliver by looking forward with confidence and removing distractions. To that end, we are changing our name to aberdeen group plc. This is a pragmatic decision marking a new phase for the organisation, as we focus on delivering for our customers, people and shareholders."

Unfortunately, I doubt that they will get a refund from brand consultancy Wolff Olins.

And it’s a sharp U-turn by CEO Jason Windsor who said only in January, as we reported here, “the name (Abrdn) is the name and we will be continuing with it”.

Outlook: falling interest rates will reduce cash margins at Interactive Investor and in the Advisor side of the business. But cash balances and trading activity are expected to grow, offsetting that.

In the Investments division, there will be “a slight reduction in revenue margins”.

It’s a measured statement:

Looking beyond 2025, we continue to see long-term structural growth in the UK savings and wealth industry, which we are well-positioned to capture. In addition, while market conditions are expected to remain challenging for active asset managers generally, we see a number of areas of attractive opportunities that our Investments business is well-placed to serve.

New targets: for FY26 they are targeting adjusted operating profit of £300m and net capital generation of the same amounts.

Graham’s view

I was GREEN on this last time and I am GREEN on nearly all fund managers.

With the name fiasco getting put behind it and with flows having improved significantly, I’m very happy to stay GREEN on this today.

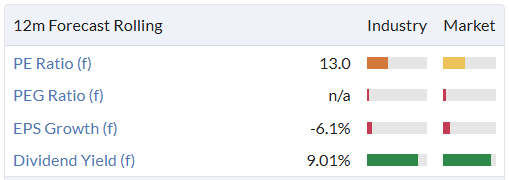

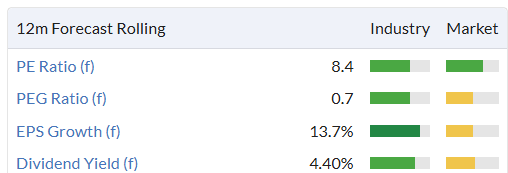

The StockRank is close to perfect:

And it offers an incredible yield:

The full-year dividend for 2024 is 14.6p, vs. adjusted diluted earnings per share of 15p. It’s not easy for them to pay this level of dividend and so their intention is to leave it at this level until it is covered 1.5x by the capital they generate. It’s currently covered 1.2x.

Can we read across from this to other fund managers, that their performance should also be expected to start improving soon? I think we might be able to start to think more optimistically about the sector.

At Aberdeen’s Investments division, net outflows were only £4bn, vs. £19bn the prior year.

£4bn is only around 1% of the AUM in this division.

Let’s see if the smaller fund managers can follow suit with less dramatic outflows.

Roland's Section

Synectics (LON:SNX)

Down 7% to 335p (£60m) - Final Results - Roland - AMBER/GREEN

At the time of publication, Roland has a long position in SNX.

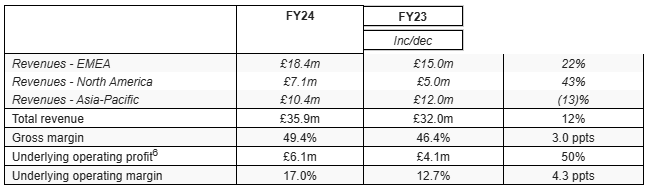

Synectics plc (AIM: SNX), a leader in advanced security and surveillance solutions, announces its audited final results for the year ended 30 November 2024 ("FY24").

Synectics’s full-year adjusted profits have beaten market expectations today, but the shares are still trading lower at the time of writing.

This stock is a member of my Stock in Focus portfolio and my personal holdings. So I’m keen to see if today’s results suggest recent momentum can be maintained – or if the rate of growth may be slowing.

2024 results summary: at face value these results seem excellent, with adjusted pre-tax profit of £4.7m coming in comfortably ahead of the £4.3m consensus estimate:

Revenue up 14% to £55.8m

Adj pre-tax profit up 59% to £4.7m

Reported pre-tax profit up 57% to £4.2m

Adj earnings up 52% to 21.6p per share

Net cash of £9.6m (FY23: £4.6m)

Order book at 30 Nov 24: £38.5m (Nov 23: £29.2m)

Full-year dividend up 50% to 4.5p per share

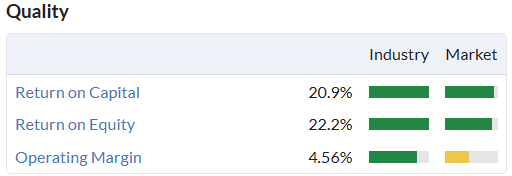

Drilling down a little further into the numbers, I can see evidence of improved profitability – a point I’ve flagged up previously. These figures are still fairly average in my view (using reported profits), but are moving in the right direction:

Op margin 7.6% (FY23: 5.6%)

ROCE 9.6% (FY23: 6.5%)

Cash generation has been skewed by some big movements in working capital. An updated note from Shore Capital today suggests Synectics has received cash upfront for revenue not yet booked, boosting its cash position.

Stripping out working capital movements gives me an underlying free cash flow estimate of £3.4m. This represents an excellent 107% conversion from reported net profit of £3.2m.

I don’t have any concerns about Synectics’ finances. Let’s see what the company has to say about trading.

Trading commentary: Synectics reports its results under two segments, reflecting its split between solutions that are sold through systems integrators and partners (Synectics Systems) and those it sells directly (Ocular).

Synectics Systems: this part of the business generates the majority of profit, selling software and hardware solutions (primarily) to the gaming and oil and gas markets.

Synectics has a long heritage of providing surveillance systems to Casinos and this remains one of the most important parts of the business.

Although Asia-Pacific revenue fell last year, the company also won a $13.2m contract during the year in this region:

the upgrade and expansion of one of the world's most successful and highest-profile gaming resorts in South-East Asia. Synectic Systems has been working with this customer since 2014,

Elsewhere, the company won a series of contracts in North American casinos and said it’s starting to target the tribal gaming market – casinos located on reservation land.

In oil and gas, the company reported a 5% increase in revenue and noted the dependence on economic conditions and geopolitical factors.

The final part of this market includes public spaces and infrastructure. Client wins last year included “a major UK utility provider”.

New opportunities flagged up include the UAE market, data centres and UK critical infrastructure.

Ocular: this business sells Synectics solutions and support directly to customers in the UK and Ireland. Key sectors are public spaces and transport infrastructure. It was previously known as Synectics Security but was rebranded in November to a name with no obvious meaning. Or as the company describes it:

This rebranding signifies a broader transformation programme designed to sharpen Ocular's focus on delivering cutting-edge security solutions and innovations across identifiable sectors, including public space, transport, and critical national infrastructure.

In any case, performance was solid last year, albeit at much lower margins than the channel business, perhaps reflecting the greater cost base required to work directly with end users:

The company says it’s “refining and developing Ocular’s go-to-market strategy”. with a “targeted approach to key sectors” where the company has a proven ability to deliver. A new Sales Director has been appointed and the company is investing in its sales team.

Operationally, growth was driven by “increased traction in transport sales”, while “security sales remained broadly flat”.

Transport growth is being driven by investment in infrastructure and a shift to the electrification of fleets (e.g. buses).

An ongoing framework agreement with National Grid delivered £6m of contracts during the year and Synectics now supports 32 NG sites.

Outlook & Estimates: 2025 trading is said to be in line with expectations, so far:

Following a good start to FY25, trading to date is in line with the Board's expectations, with our strong order book underpinning confidence in FY25 and beyond.

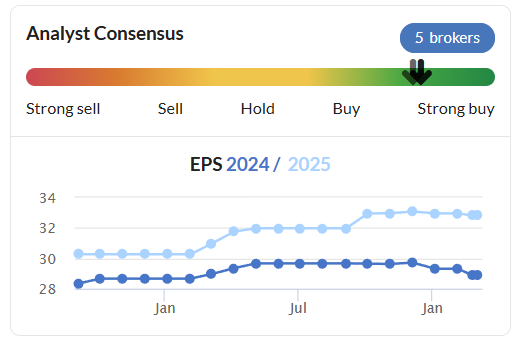

FY25 estimates from Synectics’ house broker Shore Capital have been upgraded today to bring them into line with the more positive outturn from FY24. Our thanks go for making this coverage available on Research Tree – without this it would be very difficult to track changing expectations:

FY25E revenue +5.3% to £65m

FY25E adj EPS +4.2% to 24.9p

For FY26, shore has edged up its revenue forecasts but left adj PBT unchanged to reflect higher spending on business development.

Roland’s view

Today’s upgraded FY25 estimates leave Synectics trading on a forecast P/E of 13.5 for the current year. That’s significantly below the level seen prior to today’s results and share price drop:

My impression from today’s results is that the business is performing well, but is investing more in business development in an effort to reach new markets to support further growth.

The year-end order book is equivalent to around seven months’ revenue, based on FY25 forecasts. This seems to provide decent support for FY25 trading at this stage in the year, but clearly still leaves some gaps to fill.

Optimistic investors will point to the opportunity to outperform during the year with new contract wins – and that’s certainly true.

However, I’d also want to consider the opposite risk – failure to secure a few more big wins could leave the outlook for FY25/26 looking a little weak.

On balance, I’m reassured by improving profitability and the strong balance sheet. I think it makes sense to maintain a cautiously positive view, while noting that the big gains may be in the price for now:

I’m going to maintain my previous view of AMBER/GREEN.

Investors can see a live presentation from Synectics on Investor Meet Company this morning at 11am.

Kitwave (LON:KITW)

Down 3% to 267p (£216m) - Final Results - Roland - AMBER/GREEN

Graham last commented on this food wholesaler and distributor in November, coming away with a positive impression. I’ve also been impressed by this business since its 2021 IPO.

Let’s see if today’s 2024 results support a continued positive stance – the market has taken a slightly negative view, but in the current climate that’s not necessarily very significant!

The Company is pleased to announce financial results in line with market expectations.

The headline numbers suggest to me that Kitwave has delivered another solid year of progress:

Revenue up 10.2% to £663.7m

Adj operating profit up 6.3% to £34.0m

Reported operating profit down 2% to £28.8m

Earnings per share down 13% to 23.5p

Total dividend up 1% to 11.3p per share

The drop in earnings partly reflects some dilution from a £31.5m fundraising used to fund an acquisition in September. A more positive picture is expected to emerge when the new business makes a full-year contribution to profits.

Profitability/leverage: The reason for the limited dividend growth becomes apparent when we consider the sharp increase in leverage over the last year. This was required to fund three acquisitions, including September’s £70m deal:

Return on invested capital: 11% (FY23: 19%)

Return on net assets: 22% (FY23: 30%)

Leverage inc leases: 2.8x EBITDA (FY23: 1.4x)

Leverage exc leases: 1.9x EBITDA (FY23: 0.8x)

Net bank debt of £63.7m (FY23: £25.7m)

While I give full credit to Kitwave for actually reporting a return on capital KPI, these figures clearly require some explanation.

The company makes this comment on profitability, from which I infer ROIC and ROA should improve in 2025:

The discharging of acquisition consideration has increased the investment capital and net assets in the relevant measure, but the contribution from the related acquisition has only been taken into account effective from the date of the acquisitions. This calculation is the principal reason for the reduction in the return on capital measures compared to the prior year.

Similarly, with leverage, Kitwave says:

Accounting for an estimated full year run rate effect of the acquisitions made during the year, the Group's leverage (inc IFRS 16 debt) would be below our stated target of 2.5x.

The company says it remained in compliance with relevant bank covenants at 31 October 2024, but the fact this was mentioned makes me wonder if the safety margin may have been slimmer than usual.

Balance sheet: for me, the picture painted by today’s accounts is of leverage at the upper limit of my comfort zone for a business of this type.

While Kitwave has a track record of generating attractive returns on capital, it’s a low margin business that relies on managing c.£100m of payables and receivables to generate attractive returns. This model can work well, but in my view it’s better achieved with the flexibility provided by a strong balance sheet.

I’d hope to see the company focus on deleveraging over the current year, rather than further large acquisitions.

Outlook & Estimates: CEO Ben Maxted makes a fairly vague statement on the outlook for FY25, which started on 1 November 24:

Despite the implications of the UK Government's Budget as previously disclosed in the November 2024 trading update, the Group has started the new financial year well.

Fortunately we have updated estimates from house broker Canaccord Genuity to fill in the blanks:

FY25E EPS 32.5p (previously 33.0p)

FY26E EPS 34.5p (previously 37.6p)

Canaccord says its estimates are essentially unchanged, except for some minor changes to revenue and cost assumptions based on FY24 results.

The broker notes that Kitwave has made 15 acquisitions since 2011 and is “well-placed to drive further organic growth in FY25 and extract scale synergies from recent acquisitions.”

Roland’s view

These forecasts are broadly in line with consensus estimates on Stockopedia and put Kitwave on a potentially reasonable valuation:

Kitwave has been a rare success story from the doomed 2021 IPO crop:

I remain a fan of this business, which has generated strong quality metrics in the past:

However, I would argue that today’s results highlight not just the opportunity, but the need for a period of consolidation and deleveraging.

Assuming trading remains on track, my guess is that there could be some scope for broker upgrades over the coming year, as was the case last year:

My sums point to an EBIT/EV yield of nearly 10% following today’s results. I think the shares could be attractively priced at this point, but I’ll hope to see some improvement in the balance sheet as the year progresses.

I’m going to maintain Graham’s AMBER/GREEN view at this point, based on Kitwave’s valuation and the strength of its track record to date.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.