Good morning!

The latest set of US tariffs came into effect overnight. I believe that a 104% Chinese tariff came into effect in the last few hours. However, it looks like we might have a relatively quiet day in terms of political headlines. The FTSE is expected to open down 2%, while the S&P is down 1.6% overnight. Compared to what we've witnessed over the past week, these are rather gentle market movements!

12.40pm: it has been another tough day with the FTSE down 3.6% so it is now down by over 11% for the week. The S&P has already retreated c. 11% this week, and is currently set to open down by a further 1.3% today. The reality of tariffs, including a 104% Chinese tariff, is kicking in. We conclude the report here for now!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Assura (LON:AGR) (£1.5bn) | Statement re. possible offer from Primary Health Properties (LON:PHP) & recommended offer from KKR | Rejects the PHP proposal which was 0.3848 new PHP shares and 9.08p cash (worth c. 46.2p). AGR has issued a second RNS with details of a recommended cash offer from KKR of 49.4p per share. | PINK (Roland) [no section below] |

Pagegroup (LON:PAGE) (£844m) | TU |

SP down 2% | AMBER/RED (Graham) |

Oxford BioMedica (LON:OXB) (£271m) | Full Year Results | EBITDA loss £15m in line. Guidance reaffirmed: pivot to profitability in FY 2025. | |

Saga (LON:SAGA) (£180m) | Full Year Results | FY26 to be a year of transition. Adj. PBT to fall before growing thereafter. Net debt to reduce. | RED (Graham) More of the same with terrible unadjusted numbers, a balance sheet with negative net worth and an unappealing debt position. High speculative upside but it's a definite RED from me due to the high risk, complexity and what I perceive as very poor quality from an investment point of view. |

Gulf Marine Services (LON:GMS) (£180m) | Full Year Results | Adj. EBITDA guidance $100 - 108m, utilisation 96%. Continued improvement on day rates. | GREEN (Roland) GMS is doing exactly what it’s promised, repaying debt against a backdrop of cyclical growth in day rates. Equity value is rising as a result. One day the company will probably have to address either falling rates or fleet replacement costs, but that time is not here yet. At a 40% discount to NAV, GMS continues to look decent value to me, with the added potential catalyst of shareholder returns going forward. |

Tristel (LON:TSTL) (£129m) | US update | SP up 4% | AMBER/GREEN (Graham) [no section below] I see no reason to move from the AMBER/GREEN stance held by Roland in February. In addition to the positive news surrounding the Mayo Clinic trial, today’s update also informs that Tristel’s disinfectant foam will see “no adverse impact on our pricing or sales performance in North America”, as it is already manufactured in the United States. Tristel has a long and successful track record and much of the air has come out of its valuation since 2021 and again since mid-2024. PER now c. 15x. |

Epwin (LON:EPWN) (£123m) | Full Year Results | Rev -6%, adj PBT +5.5% to £19m, “marginally ahead” of expectations. Improved margins. Outlook in line, with Q1 trading ahead of prior year. Forecasts unchanged today, suggesting mid-single digit EPS growth in 2025. | GREEN (Roland - I hold) [no section below] Today’s results from this building materials group look solid enough to me, with modest leverage and improved margins vs 2023. While the outlook remains uncertain, I think it’s fair to assume the potential for a cyclical recovery in demand at some point. On this basis, the shares look reasonably priced to me, especially as the 6% yield remains well covered. Epwin is currently a SIF stock and I think it’s worth considering as a way to play a recovery on housing. |

Audioboom (LON:BOOM) (£71m) | Full Year Results & Q1 TU | Rev +13%, adj EBITDA $3.4m ahead of exps. Q1 adj EBITDA $0.7m, outlook “at least” in line. | AMBER/RED (Graham) Keeping our moderately negative stance here as the financial figures for 2024 and the 2025 forecasts leave me underwhelmed. It does have some interesting speculative potential. |

Churchill China (LON:CHH) (£54m) | Full Year Results | In line. Rev -5%, EPS -17.5% to 57.9p. Dividend increased, £10m net cash. Outlook mixed. | GREEN (Roland - I hold) For investors with a long-term view, I think this market leader in hospitality tableware looks good value at current levels. Today’s results highlight balance sheet strength and investment in productivity gains. However, the near-term outlook remains uncertain and it’s still possible that further downgrades might be needed. |

Flowtech Fluidpower (LON:FLO) (£31m) | Full Year Results | Revenue -4.5%, operating loss increases to £(25.2m) after a large goodwill impairment. Orderbook +5% vs Dec 23. | AMBER/RED (Graham) [no section below] I've been patient on this, giving it an AMBER while hoping that it could make a recovery. However, recovery seems further away than ever with the company today posting a full-year underlying operating profit of only £2.7m, which implies that it made a small underlying operating loss in H2. Together with a large unadjusted operating loss and a weak outlook statement, I'm afraid this warrants a downgrade to AMBER/RED. |

Graham's Section

TPFG interview

To kick us off this morning, here are the notes from my interview with Property Franchise (LON:TPFG) management yesterday - CEO Gareth Samples and CFO Ben Dodds.

As usual, these are paraphrased comments from my notes, not direct quotes.

Q1. Firstly I’d be very interested in your view on the housing market. Do you worry that transactions may slow down this year?

A. January, February and March were very strong. Whenever there is a stamp duty holiday rush, there is a likely to be a lull immediately after that. We think the normal number of sales per year is 1.1 million and this year we are tracking ahead of that. Maybe this year there could be 1.15 million sales. Both sales and financial services are having better than normal years.

Q2. How about the rental market, how is sentiment among landlords?

A. Landlords are exiting due to increased regulations. What we are seeing however is that some landlords are getting bigger as they buy properties from the landlords that are exiting.

Q3. Mortgage Advice Bureau (Holdings) (LON:MAB1) is a stock we like to cover at Stockopedia. Can you give us any insight into your relationship with them?

A. It’s a very close and very deep relationship - we are MAB’s biggest customer! We meet Peter (Brodnicki) or his team once a month and talk together about how to improve processes. Michelle Brook at Brook Financial has been working with MAB for many, many years.

Q4. Now that you are carrying some net debt, do you intend to return to net cash as soon as possible? Forecasts suggest you will return to net cash next year.

A. We do plan to return to net cash although it depends on acquisitions (particularly in financial services) that we might be interested in.

Q5. Isn’t your licensing division (Fine & Country, Guild of Property Professionals) very similar in nature to your franchising division, as both are fee-based?

A. There are fundamental differences. In licensing there is a fixed yearly fee. In franchising there is a variable amount paid over five years. So there are different strategies to grow each division and it’s important to report them separately. With licensing at Fine & Country, TPFG gets paid more at first because the amount paid is calculated as a function of the addressable market that the licensee has access to. With franchising TPFG gets paid more later as it’s a function of actual revenues.

Q6. Ewemove reported 17% revenue growth but your other activities have taken all of the headlines this year. Can investors still be excited about prospects at Ewemove?

A. Ewemove has had its best year ever, busier than ever and selling 15-25 territories as usual. It is more mature now and so high % growth rates are more difficult to achieve. But our experience at Ewemove has also helped to inform developments at other brands. Some very successful Ewemove agents are opening physical stores, while conventional estate agents can now also copy the hybrid model - see Hunter’s Personal Agents.

Conclusion - many thanks again to TPFG for taking the time to talk with me. I continue to rate the quality of this business very highly - see my coverage of the full year results yesterday.

Audioboom (LON:BOOM)

Down 7% to 406p (£68m / $87m) - Final Results & Q1 Trading Update - Graham - AMBER/RED

I see that Roland was AMBER/RED on this podcast platform in December. I’ve also generally been a sceptic when it comes to this share.

Today brings a double-whammy of announcements so let’s look at it with flesh eyes and see what these results are telling us.

Firstly, the results for 2024:

Revenue +13% to $73.4m, capturing market share in the US and UK.

Adjusted EBITDA $3.4m, vs. an adjusted EBITDA loss of $0.4m in 2024. The forecast for this was upgraded something like four times during the year.

Q4 Adjusted EBITDA of $2.1m - interesting that the majority of adj. EBITDA was generated in the last three months.

Revenue at Showcase (Audioboom’s tech-based advertising hub) of $23.1m, up 56%.

Downloads and video views are down significantly. It doesn’t sound like a very meaningful reduction as Apple have “reduced and rebased download reporting”. There were changes to how Apple’s podcasting app downloaded content. This impacted revenues linked to the official download numbers.

Ended the year as 4th largest podcast publisher in the United States with high rankings also in Australia, Canada, New Zealand and Latin America.

Cash of $3.9m and there’s $3m available in an overdraft.

Outlook: There is more than $63m of contracted revenue (advertising sales) already booked for 2025.

The Board is confident that the business is well placed to deliver upon expectations for record revenues and adjusted EBITDA profitability across 2025, and is fully primed for further future growth beyond this year.

Estimates: Cavendish have published a helpful note this morning which reiterates 2025 forecasts for revenues of £ 80m and adj. EBITDA of £4.5m.

Q1 trading update

Some key points:

Q1 2025 adj. EBITDA is $0.7m, much higher than Q1 last year but lower than the previous quarter (Q4 2024). Q1 is “historically the seasonal low point”.

Year-on-year revenue growth only 1% as Audioboom “continues to focus on high-quality revenue generation, relinquishing and replacing low performing contracts with higher quality revenue”.

Revenue per 1000 downloads (RPM) $60.83, up 17% year-on-year.

Reported download growth to increase in future quarters, as Q1 is the last one where year-on-year growth is impacted by Apple’s app update.

Kudos to the company for giving us a tariff update: they expect “minimal impact” as a direct result, “due to the production and sale of its inventory being within specific territories”. I guess this makes sense when we are talking about advertisers who tend to be country-specific?

Also, most of Audioboom’s employees are in the United States, so higher NICs aren’t relevant.

Graham’s view

I continue to find this company’s reporting style overly promotional.

For example, they trumpet (putting in bold) the fact that they increased their Q1 adjusted EBITDA by 10x.

If adj. EBITDA had increased from $1m to $10m, or from $0.5m to $5m, I could maybe, sort of, understand it.

But it actually increased from $0.07m (i.e. $70k) to $0.7m. In my book this is an increase from breakeven to $0.7m, not a 10x increase!

Also, the adj. EBITDA numbers are dubious at best. For 2024 they excluded:

Share-based payments (management bonuses by another name) of $1.4m

Lease-related costs $200k

Contract-related costs $550k

The actual operating profit number is $1m and that seems to me to be much closer to a real profit figure than adjusted EBITDA. It is a big improvement on the corresponding figure for 2023, but a far cry from their adj. EBITDA.

Some other small points:

I note that $1.1m of receivables are past due out of the total customer receivables of $16.5m.

1.7m share options were outstanding at the end of 2024 (current share count: 16.4m).

Minimum revenue guarantees to podcast partners - amounts that Audioboom must pay to content providers - are reducing gradually but are still $29m as of the end of 2024.

I’m inclined to maintain our AMBER/RED on this share. I do think it has some interesting potential and that the new business model - including its high-tech advertising marketplace - sounds quite a better than the old one. So I am warming to the investment case at Audioboom.

Against that, I have to acknowledge that real profits remain quite small for now. The adj. EBITDA numbers aren’t real to my eyes, and the prospects for growth over the next few years are pretty good but not outstanding (e.g. 9% revenue growth is pencilled in for each of the next two years).

In an ideal world we would see operational leverage kick in from here, and the profit figures would really take off. That is arguably happening now but only at the adj. EBITDA level. I’m not sure if we are going to see meaningful, unadjusted bottom-line profits here in the foreseeable future.

The cash balance is also a little small considering the investments that might be needed and the risk of future cash burn. Barely any cash was generated in 2024.

For these reasons I think a moderately negative stance remains valid.

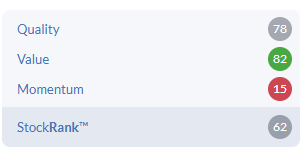

This is consistent with the StockRanks which view it as a “Momentum Trap”, i.e. offering little in terms of Quality or Value.

Let me emphasise again in closing that I do think this has some interesting potential - a successful podcasting platform with a high-tech advertising marketplace could be a fabulous business in theory. So this could be an interesting high-risk/high-reward investment. For now, however, based on the financials, it’s a thumbs down from me

Saga (LON:SAGA)

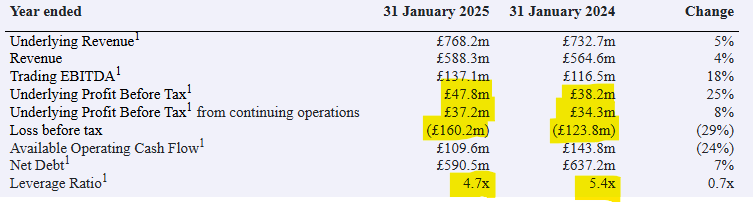

Up 1% to 126.5p (£181m) - Final Results - Graham - RED

Saga plc (Saga or the Group), the UK's specialist in products and services for people over 50, announces its unaudited preliminary results for the year ended 31 January 2025.

I was RED on this in January which I admitted may have been a little harsh. But the structure and makeup of this group has never made much sense to me, and its results have been atrocious for many years.

Let’s see if I can find any reasons for optimism in today’s full-year results.

Once again there is a huge discrepancy between the adjusted numbers and the actual numbers.

There is “underlying PBT” of £47.8m vs. an actual loss of £160m. This is even worse than the previous year. There are huge goodwill impairments along with restructuring costs:

Net debt remains enormous at £590m but there is at least a reduction in the leverage multiple. However, 4.7x is still too high. In my view, Saga can afford to have a lower leverage multiple than other businesses, as leverage is calculated on the basis of EBITDA which excludes some very high charges, e.g. depreciation of £35m.

Let’s listen to some management commentary on the performance. Here’s the CEO:

From a trading perspective, we delivered a strong performance, with total underlying profit before tax up 25% and ahead of previous guidance. This was driven by the strength of our Travel businesses, with especially high levels of customer demand for our differentiated ocean and river cruise offers.

In addition, we took the significant strategic action necessary to reposition the Group for future growth. We completed our strategic review, successfully signed a new 20-year Insurance Broking partnership with wholly owned UK subsidiaries of Ageas SA/NV and agreed the sale of our Insurance Underwriting business. These achievements materially reduce the risk and complexity of the Insurance business going forward and, when combined with our continued strong trading performance, meant that we were able to complete the refinancing of our long-term corporate debt, replacing our 2026 debt maturities with new long-term credit facilities…

The sale of the insurance underwriting business is expected to complete in Q2. Ageas will take on most of the financial risk while Saga focuses on “marketing, brand management and customer insight”.

Outlook: this year they are expecting more growth in the Travel business, but also “a material increase in financing costs”, so that underlying PBT will fall. Net debt to reduce further although perhaps not by much, “with the reduction expected to accelerate thereafter”.

There is a 5-year plan that involves underlying PBT of £100m and leverage below 2x.

Graham’s view

This is another RED from me - I view this as a horrible investment with still too much complexity, no competitive advantage that I can discern, a group structure that makes little sense, carrying too much expensive debt and producing consistently awful numbers.

Let’s take a moment to reflect on the refinancing that Saga recently announced.

Saga has had to turn to HPS Investment Partners - a private equity/private credit firm - for the refinancing. This is the type of firm that will be well-prepared if Saga enters financial distress at some point in the future.

The new facilities include a £335m term loan, a £100m delayed term loan, and a £50m RCF.

The first two of these facilities charge 6.75% over the base rate, and reduce if/when the company de-levers.

The Sterling base rate is currently 4.46%. So Saga are paying 11% on these facilities.

I would be happy to earn 11% on my equity portfolio, let alone on a fixed income investment!

There is no “going concern” warning in today’s statement, and I do not think that Saga is currently in financial distress. However, I do think that their lenders are going to suck most of the cash flow out of them.

I also observe that even after the enormous goodwill write-offs, the company’s balance sheet is still stacked with goodwill and has a negative tangible net worth in the region of £180m.

This is another one with high speculative upside, but for me it’s a definite RED at almost any price, due to the high risk. Saga’s market cap is modest at £180m, confirming that the shares are trading only as option counters on its debt load.

Roland's Section

Gulf Marine Services (LON:GMS)

Down 3% to 15.6p (£179m) - Final Results - Roland - GREEN

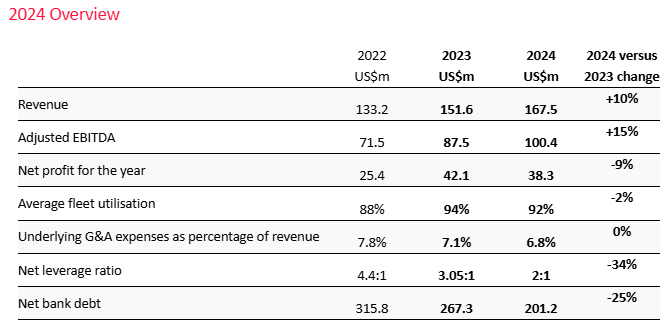

Average day rates increased to US$ 33.1k (2023: US$ 30.3k) with improvements across all vessel classes.

GMS has made regular appearances in these pages this year thanks to its habit of issuing an RNS (seemingly) each time it signs a new vessel hire contract. See yesterday. But underlying this, I’ve been fairly confident the group is trading well and benefiting from stronger oil and gas markets to repay debt, transferring value to equity holders.

Today’s results give us a chance to review progress in 2024. The headline numbers appear to be at the top end of expectations and the outlook commentary for 2025 seems positive.

2024 results summary: let’s start with a quick look at the main numbers. I’ve pasted this in from today’s results to avoid retyping:

A few comments on these numbers.

Revenue: GMS says revenue growth last year reflects a 9% increase in average day rates to $33.1k (2023: $30.3k), with improvements across all vessel classes.

Profit & margins: adjusted EBITDA rose by net profit fell by 9% to $38.3m. On closer inspection of today’s accounts, the main reason for this appears to be due to impairment charges.

In 2023 the company reported net impairment reversals (i.e. a credit to the P&L) of $33.4m.

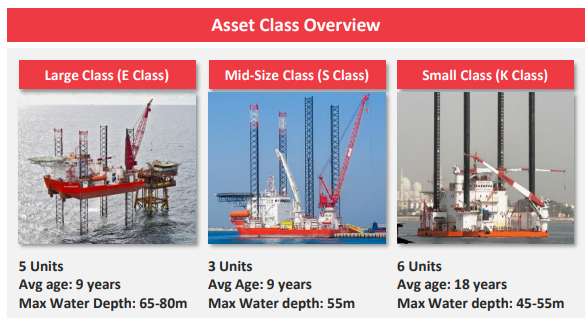

In 2024, this dropped to $9.3m as a reversal of $18.6m was partially offset by $9.4m of new impairment charges on its smaller K-class vessels. This is said to reflect expectations that day rates on these vessels will fall in outer years – they are among the oldest in the fleet (see below).

While we probably shouldn’t ignore impairment charges, these are non-cash and seem to be something of a moveable feast, changing each year depending on market conditions and management estimates of future day rates.

Stripping out impairment gives an idea of cash profitability, which can be useful. In this case, my sums suggest the group’s underlying operating profit rose from $54.8m to $63.4m last year. This implies a 2024 underlying operating margin of 37.8% (2023: 36.1%).

Net profit of $38.3m is somewhat lower due to substantial finance costs of $23.5m and some tax charges.

One other point worth watching is that expected credit losses rose by $2m to $4.2m last year. If I’ve understood the notes correctly, this represents the final tranche of receivables due from a customer that went into administration in 2023. Hopefully there won’t be any further losses – the majority of GMS’s customers are Gulf state national oil companies, which are presumably unlikely to default.

Free cash flow: my sums suggest 2024 free cash flow of $62.3m, giving an impressive 160% conversion from net profit of $38.3m. Of course, there are no free lunches here. The main difference between FCF and net profit is the depreciation charge on GMS’s owned fleet, which was $26.2m last year.

GMS doesn’t have a fleet replacement programme and has no apparent plans to buy additional ships or order newbuilds. Money that might be spent on vessel purchases can be used for debt repayment or shareholder returns (see below).

The average age of the fleet is currently 13 years, with an expected life of c.40 years. So there’s probably no rush to think about replacing the existing fleet:

However, demand and future day rate expectations appear to be strongest for the largest E Class vessels. Management recently leased an additional vessel to fulfill a contract extension, but I wonder if they may eventually be tempted to purchase additional vessels.

Middle East oil producers are expected to ramp up production over the coming years, while wind farms also appear to offer longer-term growth opportunities. GMS currently has one vessel (out of 14) operating in the North Sea wind market.

Profitability: GMS’s operating margins seem impressive, but this is because they are being earned on revenue from expensive capital assets with relatively low ongoing costs.

Looked at differently, last year’s results show a 6% return on assets and a 10% return on equity, according to my sums. This is a far more average level of profitability and reflects the high cost of assets needed to generate this level of revenue – the reported book value of GMS’s fleet is c.$600m.

As Mark commented recently, this level of profitability doesn’t really seem high enough to justify investment in new vessels. Fortunately, the company expects that day rates will continue to rise.

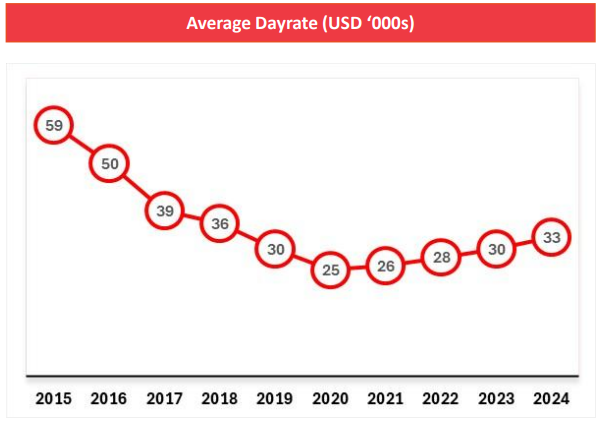

Historical pricing over the last decade certainly suggests rates are still some way below the last oil and gas boom, when GMS revenue reached $220m:

Leverage/Shareholder returns: If rates do continue to improve, debt repayment should accelerate, supporting shareholder returns.

Net debt fell to 2.0x EBITDA last year. While relatively high for a small cap, this is within a normal range. GMS has also recently completed a refinancing that should lower its cost of debt.

Management now plans to introduce a shareholder distribution of 20%-30% of adjusted net profit from 2025 onwards. This will be made through dividends and/or share buybacks. Using 2024 results as an example, I estimate this could give a yield of 4%-5% at current levels.

Outlook: GMS has rebuilt its backlog over the last couple of years and has already secured over 90% of 2025 revenue (based on consensus of $179m):

Management is targeting 96% utilisation for 2025 and says that secured day rates are already 6% 2024 actual levels.

The company’s 2025 guidance is unchanged today, with adjusted EBITDA expected to be $100m to $108m (2024 actual: $100.4m).

Estimates: consensus forecasts on Stockopedia prior to today showed 2025 earnings of $0.042 per share. This is supported by updated notes from brokers Panmure Liberum and Zeus today, which bracket this figure:

PanLib 2025E: $0.04

Zeus 2025E: $0.044

This puts GMS shares on a 2025E P/E of just under five.

Roland’s view

Today’s accounts show an equity value of $383m at the end of 2024 – a 16% increase from December 2023. The majority of this reflects the $48.5m reduction in net debt over the last year.

This transfer of value from lenders to shareholders is a big part of the investment case here.

An additional attraction is the stock’s discount to book value. I estimate a net asset value per share of around 26p using today’s accounts, so at 15p the discount is c.40%.

For anyone buying at current levels, the discount to book value improves the return on equity we might expect from the investment.

If this discount persists, I’d guess that GMS management might opt for buybacks rather than dividends when the time comes. Buying back shares at a discount to book value increases net asset value per share.

I can see some medium-term risks here relating to cyclical demand and eventual fleet upgrade costs. But I think it makes sense to remain positive at current levels, given the low valuation and reduced leverage.

I’m going to stay GREEN on GMS today, with the caveat that this is not a business I’d want to pay a high multiple for.

Churchill China (LON:CHH)

Up 20% to 590p (£65m) - Final Results - Roland - GREEN

(At the time of publication, Roland has a long position in CHH)

Churchill China plc (AIM: CHH), the manufacturer of innovative performance ceramic products serving hospitality markets worldwide, is pleased to announce its Final Results for the year ended 31 December 2024.

The headwinds facing the hospitality sector are well known and have a direct impact on suppliers to hotels and restaurants such as Churchill China. The company issued a big profit warning in November last year and its shares have suffered badly over the last year, despite today’s pop:

Today’s results don’t include any new guidance but do appear to be in line with expectations set in November.

2024 results summary: Churchill publishes lovely clean and simple accounts, with no adjustments:

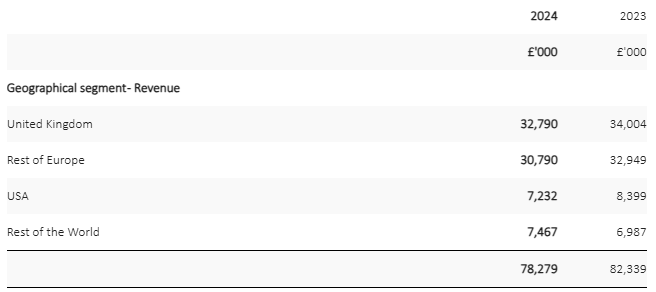

Revenue down 4.9% to £78.3m

Pre-tax profit down 21% to £8.5m

Earnings per share 17.5% to 57.9p

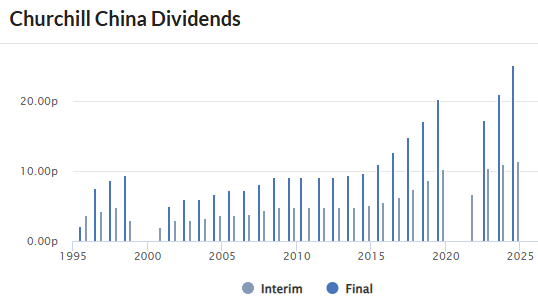

Dividend up 2.8% to 38p

Net cash down 27% to £10.1m

The dividend remained covered comfortably despite a slump in earnings – these shares now yield over 7% and boast an impressive dividend track record:

The reduction in net cash last year reflects higher inventories and year-end timing, which essentially reversed the more favourable position seen at the end of 2023:

Overall cash has decreased in the year by £3.8m driven primarily by increased stock of £1.4m and increased debtors of £1.2m. The debt position was primarily driven by the timing of the year end which resulted in a short month for collection and by a stronger position than usual at the end of 2023.

Underlying cash conversion is generally very strong in this business, which has no debt. Year-end net cash of £10m represents 15% of the market cap, providing a source of interest income and a big margin of safety.

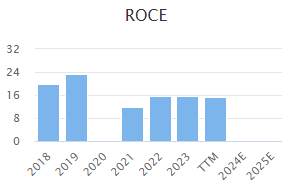

Profitability is also generally strong. Today’s accounts show an operating margin of 10.2% and return on capital employed (ROCE) of 11.8%. These are below prior year levels, but seem acceptable for what I believe is likely to be a low point for earnings:

Trading commentary: in short, Churchill says that people are still eating out leading to a continued healthy replacement business – crockery inevitably gets broken and needs regular replacement.

In the UK, the company has a strong position in with big pub chains (e.g. Wetherspoons, I think), which management says “tends to be less impacted by economic sentiment compared with independents”.

However, the company says its established customers have slowed plans to open new outlets and are suffering from “compressed” profitability. This is restricting the group’s overall sales growth.

The outlook in export markets is said to be stronger, however (installations are new openings).

… our current pipeline for installation business in our export markets remains strong.

Churchill sources most of its raw materials in the UK and manufactures its products here. The UK and Europe account for more than 80% of revenue, but there is some exposure to the USA that I assume may be affected by tariffs:

Over the last couple of years, Churchill has been investing in its manufacturing operations to improve efficiency and increase automation. Cash capex was £5.3m in 2023 and £3m last year.

The company says these investments are delivering results, allowing Churchill to maintain competitive pricing and protect its market share.

Outlook: perhaps understandably, Churchill has steered clear of any specific guidance for the year ahead today.

Replacement demand is expected to remain healthy, but new business is less certain. Management admits that the outlook may remain constrained, depending on economic conditions:

A more robust hospitality market is required for a step forward in our market penetration and profitability. We will continue to focus on improving efficiencies within the business and invest strategically to ensure we are in the best position to capitalise on future opportunities, as underlying macro conditions and consumer sentiment improves.

There are no broker notes available to me today, but consensus forecasts on Stockopedia show Churchill delivering broadly flat results this year, pricing the shares on a P/E of 9 with a 7% yield.

Roland’s view

I recently added the shares to my portfolio because I believe this is a good quality business at a very reasonable price. With hindsight, it’s clear I bought too soon – my shares are down by over 20%.

Personally, I’m confident that Churchill is likely to retain its position as a market leader. The company says the quality of its products and its ability to fulfil most orders within 48 hours differentiates the business.

Over time, my view is that demand is likely to recover and the company should benefit.

In the meantime, the stock’s dividend yield and strong balance sheet provide ongoing returns. This financial strength is also allowing the company to invest in its operations, improving efficiency and competitiveness.

The big risk here is that the current slowdown will last longer – and perhaps be deeper – than expected.

The StockRanks styled Churchill as a Contrarian stock ahead of today’s results, which I think is fair:

On that basis, I’m going to maintain my positive (long term) view today at GREEN.

However, I can see an argument for waiting until there’s concrete evidence of improving momentum before investing. This is especially relevant here as Churchill shares tend to trade with a huge spread and poor liquidity, making them unsuited for short-term trading.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.