Good morning! Let's see what Thursday has in store for us.

The Agenda is complete.

We are finished for today, thank you!

Companies Reporting

RNS | Summary | Our view (Author) | |

|---|---|---|---|

| Unilever (LON:ULVR) (£120bn) | Trading Statement | 2025 outlook reconfirmed with 3-5% underlying sales growth, modest improvement in margin. | |

| Relx (LON:REL) (£72.8bn) | AGM Trading Update | Full year outlook unchanged. Positive momentum, strong underlying revenue growth especially in the Risk business. Adjusted operating profit growth is expected to exceed revenue growth in all four operating divisions. | GREEN (Megan - I hold) [No section below] The word ‘continues’ appears no fewer than 15 times in this morning’s short update from Relx. That’s a good thing because it means that the trends which make this an attractive high quality growth stock remain on track. It’s the risk business (34% of sales) where the most growth is on offer. Relx has won new clients in the period as demand for financial crime and fraud solutions increases. It’s still an expensive stock (Trump tariff problems barely caused a scratch to the share price), but this isn’t a stock to wait for an attractive entry point. For investors after long-term high quality growth, I can’t see many better candidates in the UK. |

| Anglo American (LON:AAL) (£28bn) | Production Report Q1 2025 | Copper and iron ore in line with guidance. Platinum expected to demerge from 31st May. | |

| Weir (LON:WEIR) (£5.7bn) | Trading Update | Full year guidance reiterated. Q1 original equipment and aftermarket orders both +5%. | |

| St James's Place (LON:STJ) (£4.9bn) | Q1 New Business Inflows and FUM | Net inflows £1.7bn. FUM £188.6bn (Dec 2024: £190.2bn). Good levels of activity so far in April. | |

| Hikma Pharmaceuticals (LON:HIK) (£4.2bn) | Trading Statement | Reiterates guidance for 2025. Revenue to grow 4-6%, core operating profit $730-770m. | |

| Inchcape (LON:INCH) (£2.7bn) | Trading Update | Q1 in line. Guidance for FY 2025 unchanged, excluding potential tariff impacts. | |

| Balfour Beatty (LON:BBY) (£2.2bn) | Texas Interstate Contract | $889m (£670m) contract to reconstruct a Dallas interstate road and construct nine crossings. | |

| AJ Bell (LON:AJB) (£1.7bn) | Trading Statement | Platform: Strong customer growth, +32k (+6%) in the quarter. D2C trading activity up in April. | |

| Domino's Pizza (LON:DOM) (£1.09bn) | Q1 Trading Statement | FY25 adj. EBITDA to be in line (£140.8-149.7m). Q1 LfL sales +0.5%, total system sales +2.1%. | |

| Supermarket Income REIT (LON:SUPR) (£963m) | Joint Venture with Blue Owl Capital | Eight of SUPR’s existing assets transferred into JV. SUPR receives £200m to sell 50% stake to JV | AMBER/GREEN (Graham) SUPR trades less cheaply than other REITs but it’s probably of significantly higher quality than most other REITs. This JV opens up the potential for management and performance fees on a larger asset base. |

| Alphawave IP (LON:AWE) (£876m) | Q1 Trading and Business Update | Economic uncertainty and tariffs: not able to provide guidance for the full year 2025 or beyond. | |

| Indivior (LON:INDV) (£867m) | 1st Quarter Results | Net revenue of $266m in line. FY guidance unchanged. On track for opex savings of over $100m. | |

| CVS (LON:CVSG) (£722m) | Disposal of Crematorium Operations | £42.4m price is 10x adj. EBITDA. Only 1.8% (3.2%) of CVSG’s total group revenues (adj. EBITDA). | |

| GB (LON:GBG) (£668m) | Trading Statement | SP down 14%. Full-year rev +3%. Adj. op profit +10% (£67m). Near-term tariff uncertainty. | AMBER/GREEN (Graham) The initial sell-off strikes me as a rather harsh response to the mild statement from GB Group re: economic uncertainty. I continue to have a favourable impression here and the value it offers is much better now than it was the last time I reviewed it! |

| Senior (LON:SNR) (£507m) | Trading Statement | Growth in line with exps. Tariff impact limited, manageable. Outlook unchanged. | |

| Resolute Mining (LON:RSG) (£485m) | Quarterly Activities Report | On track for production guidance, capex guidance on track. Net cash $100m. | |

| Molten Ventures (LON:GROW) (£485m) | Trading Update | NAV 671p (FY24: 662p). Cash £110m. “Our preliminary assessment indicates that our portfolio, being technology and software focused, is less exposed to the direct impact of tariffs.” | |

| RWS Holdings (LON:RWS) (£426m) | Trading Statement | ++1.3% organic CCY rev. growth to £344m. Adj. PBT £17m (24H1: £46m) impacted by non-trading items. Net debt £27m. Adjusted PBT is now expected to be in the range of £60m-70m for FY25. | BLACK (AMBER) (Mark - I hold) |

| Jupiter Fund Management (LON:JUP) (£377m) | Q1 Trading Update | AUM down £1bn to £44.3bn. Q1 outflows £0.5bn. “We have not seen any material change in client sentiment or flow activity to date since period end.” | AMBER/GREEN (Graham) Downgrading this one notch, mostly because of my previous decision that I could not stay GREEN on conventional fund managers in general. I do continue to rate this very highly for value. Additionally, I'm enthused by the institutional net inflow for the quarter and management's optimism that we will see more of this in the current year. Not all doom and gloom by any means. |

| Asos (LON:ASC) (£370m) | Interim Results | Gross margins up 490 basis points, revenue down 13% to £1.292bn. Adj LBT £69.5m vs £120m in 24H1. “For FY25, we expect revenue growth towards the bottom end of consensus range.” Re-iterates FY25 profitability guidance. | RED (Graham) [no section below] Enormous albeit reduced losses continue at this attempted turnaround. The unadjusted H1 operating loss is staggering at £210m after £177m of costs to vacate their Atlanta distribution centre. Net debt remains very significant at £276m although if the company hits its adj. EBITDA target of c. £140m then the leverage multiple might be less than 2x. Watch out though - even on an adjusted basis, there's a huge gulf between EBITDA and the pre-tax loss. The balance sheet is deeply in the red in terms of tangible value. I hope the company's new commercial model succeeds but I also think it's important to highlight the risks when reviewing leveraged, loss-making businesses. Even if ASOS enjoyed a moat in the past, I don't think it has one today. These numbers are very off-putting and I'm inclined to mark this down to RED. |

| Brickability (LON:BRCK) (£195m) | Pre-Close Trading Update | Rev +7% to £637m (+1% LFL), FY25 Adj EBITDA +11% to £50.0m ahead of market expectations. | GREEN (Mark) |

| Science (LON:SAG) (£184m) | Trading Update & Response to Ricardo | Positive start to the year, with revenue and profitability slightly ahead of the Board's plan. A robust balance sheet with significant cash resources. | AMBER/GREEN (Graham) [no section below]

We have some more lambasting of the Ricardo board by Science Group today. My concerns remain twofold: 1) that Science management will use up all of their mental energy on this battle that they have instigated with Ricardo, that they may or may not be able to win, while their concentration might have been more productively directed elsewhere; 2) they will use up a very large chunk of cash on an investment that - according to their own logic - might not be a very good one. Selling a 20% stake in Ricardo, if that is their eventual decision, will be much harder than buying a 20% stake. I maintain a moderately positive stance on Science Group but their strategy does concern me. |

| XP Power (LON:XPP) (£174m) | Q1 Trading Update | Rev -18% CCY to £53.8m, Net debt £65.4m down £28.1m from year end. Order intake +30% to £57.4m. Expect tariff costs to be passed through the supply chain. | AMBER/RED Mark [no section below] For the first time in a while, orders are exceeding their booked revenue for the quarter. They say, “some customers brought forward orders previously scheduled for Q2 in response to improving prospects.” but surely trying to beat tariffs is a more realistic reason, leaving Q2 potentially weak. Net debt is down, with the benefit of reduced inventories, but mainly a £40m placing. This also doesn’t include costs and penalties if they lose their appeal for the ongoing legal case. With a strong H2-weighting and potential tariff impacts to come, this looks susceptible to further bad news. |

| Somero Enterprises (LON:SOM) (£134m) | Trading Update | Q1 weaker than expected. Updated guidance Rev $105m from $114m consensus, EBITDA $24m vs $29m, cash $28m vs $31m. | BLACK (AMBER/RED) (Mark) The uncertainty caused by tariffs is causing a decline in sales in their key North American market. The forward metrics make the company look cheap, but these are predicated on them hitting these updated numbers. Today’s update doesn’t give a lot of confidence in this, although a flexible cost base may help. We’ve sat on the fence on this one for a while, but with competition concerns also looming, it feels like today is the day to downgrade our view. |

| ASA International (LON:ASAI) (£103m) | 2024 Results and Q1 Business Update | Robust start to 2025. March 2025 loan portfolio +1% q/q, +22% y/y. At risk loans stable at 2.2%. | |

| Tracsis (LON:TRCS) (£94m) | Interim Results | Rev flat at £36.3m, Adj. EPS -25% to 7.7p, Cash £22.1m. Without further material contract wins, the Board expects FY25 adjusted EBITDA to be in the range £12.5m - £13.5m. | AMBER Mark [no section below] |

| Afentra (LON:AET) (£87m) | Final Results | Gross avg production 21,111 bopd (2023: 20,180 bopd). Rev $180.9m, net cash $12.6m, PAT $49.8m. Post year-end: Gross Q1 prodn averaged 22,120 bopd (Net: ~6566, bopd). | |

| InvestAcc (LON:INAC) (£82m) | Final Results & Q1 Trading Update | Rev £2.5m, trading EBITDA £0.9m, in line with expectations. Group operating loss £2.2m. Cash after minimum regulatory capital & deferred consideration paid in Q1 2025 £4.8m. | |

| Activeops (LON:AOM) (£60m) | Trading Update | Rev +13-15% CCY, Adjusted EBITDA flat at £2.4m. Cash £20.6m (2024: £17.6m). | |

| Severfield (LON:SFR) (£59m) | Pre-close TU | FY25 U/L PBT £18-20m in line with (recently reduced) expectations, net debt £44m. Confirms some insurance coverage for bridge remediation issues. | AMBER/RED Mark [no section below] Today’s rise appears to be a relief rally that there has been no further deterioration in trading here. They say 2026 is trading in line, but it is worth noting that this is forecast for a further decline in EPS from 2025. The good news is that it looks like some of the issues they have had remediating the work they have done on bridges is covered by insurance. However, research provider progressive still expect net debt to be flat over the coming years, and including lease debt it is equivalent to the current market cap. Despite some contract wins for 2027, this makes it still look more expensive than better-run competitor Billington. |

| Lords Trading (LON:LORD) (£44m) | Property Transaction | Sale and leaseback of four properties for £13.1m. | |

| ECO Animal Health (LON:EAH) (£36m) | Trading Update | Revenue 7% below expectations, EBITDA marginally ahead of expectations vs £7.2m forecast. Cash £25m. Monitoring tariff impact, prices increased to reflect any tariff. | AMBER Mark [no section below] |

| MicroSalt (LON:SALT) (£29m) | Q1 Business Update | Bulk revenue in Q1 2025 represents 142% of the total bulk revenue for all of 2024. | |

| Shield Therapeutics (LON:STX) (£24.5m) | FY Results | Rev +185% to $32.3m. Loss $27.2m. Cash $6.5m +$10m gross from placing post-year-end. Cash flow positive by the end of the year. | |

| One Health (LON:OHGR) (£23m) | Trading Statement | Rev +22% to £28m, U/L EBITDA in line with expectations. | |

| Vianet (LON:VNET) (£17m) | Trading Update | Revenue flat at 15.3m, Adj. EBITDA flat at £3.6m, net debt £0.4m. 1p dividend declared, “confident” outlook. | AMBER/RED Mark [no section below] |

| Checkit (LON:CKT) (£16m) | Final Results | Rev +17% to £14.1m. LBITDA £2.1m (FY24 £3.4m), Net cash £5.1m (FY24 £9.0m). Cash breakeven in calendar 26. | AMBER/RED Mark [no section below] |

| Pennant International (LON:PEN) (£12m) | Final Results | Rev £13.8m down 11%. Adj. LBT £0.3m (2023: PBT £0.6m). Net debt £2.3m (2023: £1.9m). | AMBER/RED Mark [no section below] |

| Rome Resources (LON:RMR) (£10m) | Operations Update | Drilling to commence within the next 10 days following the withdrawal of the rebel group from the area. | |

| Diales (LON:DIAL) (£10m) | 25H1 Trading Update | 25H1 similar to 24H1, in line with expectations. Net cash £2.3m down from £4.3m at FY24 year end. On track to deliver full year results in line with market expectations. | AMBER/RED Mark [no section below] The company expects an in line full year. However, this doesn’t seem particularly exciting given that this means a forward P/E of around 13. They claim they have “momentum”, but PBT for 25H1 is similar to the previous year, which doesn’t suggest much of that. Cash is also down, although they say it has risen to £3m as of 10 April. They are likely to hold their 1.5p dividend for an almost 8% yield. However, key priorities include the acquisition of new talent, but in this industry, this often requires golden hellos, suggesting that the cash balance may well be used for that. Overall, it is hard to get excited by a company on a fairly high rating for a people business with a history of not being paid on time, and little near-term growth opportunities. |

| Podium Minerals (ASX:POD) (£8m) | Possible Offer | Conditional proposal at 6.5p from current 53% shareholder. Last night’s price: 5.24p. | PINK |

Graham's Section

Supermarket Income REIT (LON:SUPR)

Up 0.7% to 77.8p (£971m) - Strategic JV with Blue Owl Capital - Graham - AMBER/GREEN

Some interesting news here as Supermarket Income REIT offloads eight properties into a joint venture.

Blue Owl Capital (NYQ:OWL), their new partner, is a New York-based alternative asset manager.

The plan is that the JV will grow its assets up to £1bn over the coming years and that SUPR will benefit from the returns in the JV itself, from management fees (0.6% of gross asset value) and possibly performance fees.

Some details:

5x Tesco, 3x Sainsbury’s and 1x Morrisons have been transferred into the JV.

They are transferred at a 3% premium to their Dec 2024 book value, with a combined value £403m.

Supermarket Income REIT is selling a 50% stake in these assets to their JV partner, so it receives £200m cash.

That cash will be used to “reduce debt in the near term and to invest in other supermarkets either directly for SUPR or indirectly through the JV, based on the investment profile of assets.”

Leverage - the JV, like SUPR itself, will use leverage and is expected to have an LTV of c. 55%. After reinvesting the proceeds of its sale to the JV, SUPR will have an LTV “at the upper end” of its 30-40% range.

Graham’s view

My only concern here - and I don’t know if it’s a valid one - is that SUPR might end up competing with the JV for the most attractive supermarket investment opportunities.

For example, consider this: “the intention of the JV partners is to scale the vehicle, whereby the JV will have a right of first refusal over pipeline assets which meet specific investment criteria.”

Does this mean that SUPR could end up owning through the JV 50% (or probably less) of an asset that it might otherwise have been able to buy outright?

That is my one concern but apart from that, this seems to be an exciting development that opens up the potential for SUPR to generate management/performance fees on a larger asset base.

Roland was AMBER/GREEN on SUPR last month after reviewing their interim results, and I am generally AMBER/GREEN on REITs and investment trusts generally as I think the entire sector is probably undervalued (trading at steep discounts to NAV and attracting unusual takeover interest from intelligent buyers). Please check Roland’s article for a detailed overview of the company's recent performance.

SUPR itself is not trading at a very steep discount to NAV - perhaps c. 11% - but it benefits from blue-chip tenants (Sainsbury’s, Tesco, Carrefour, etc.), index-linked income and long lease terms. So it makes sense in my mind that it should trade less cheaply than others in the sector.

The JV announcement opens up a new path for their development that I hope will be highly complementary to their existing operations.

I’m therefore happy to keep our AMBER/GREEN on this.

Jupiter Fund Management (LON:JUP)

Down 0.4% to 69.9p (£375m) - Q1 Trading Update - Graham - AMBER/GREEN

Let’s check in on this fund manager.

For Q1 we have a £1bn reduction in AUM, thanks to £0.5bn of outflows and £0.5bn of negative market movements. AUM falls to £44.3bn.

The flows have a little bit of brightness in them, which feels unusual - there was a £1bn net inflow from institutions, driven by one large mandate, offset by a £1.5bn net outflow from retail investors.

For context, last year, Jupiter saw total outflows of £10.3bn and this included heavy redemptions both from institutions and from retail investors. Net flows from institutions were negative every quarter in 2024 with only one exception which was approximately flat. So a positive quarter is an uncommon event.

And they are bullish on prospects for continued institutional flows:

Our pipeline remains strong and we are confident of continuing to generate further net inflows from Institutional clients through 2025.

As for more recent trading, there hasn’t been much market positivity in Q2 so far, as we already know:

After the period end, we have seen elevated market volatility across asset classes as a result of trade policies. Although this will undoubtedly have an impact on client risk appetite, mispriced assets present an opportunity for high-conviction active asset managers. Estimated AUM at 22 April 2025 was £43bn.

The good news is that Jupiter has not seen “any material change in client sentiment or flow activity to date since period end”. I guess that means the exodus of client funds is continuing at a slow rather than an accelerated pace.

Graham’s view

I’m AMBER/GREEN on several fund managers now and the question is whether I should adopt that stance here, too (although I was fully GREEN on Jupiter in February).

As this is not a fund manager where I have especially more conviction vs. others in the sector, I think AMBER/GREEN probably makes sense here, too.

The value on offer is of course exceptional by historic standards with c. £114 of AUM on offer for every £1 invested in the stock at current prices. It’s also trading at a PER of 10x earnings, although it’s important to recognise that earnings estimates haven’t exactly been stable.

I agree with the company that the recent political/economic volatility might actually be helpful if investors decide to reallocate away from the United States into regions where Jupiter has more focus, particularly the UK and Europe. Jupiter say they are seeing “early-stage evidence” of this.

So it’s not all doom and gloom here, in my view. There is value on offer and there’s at least the potential for a change in sentiment towards UK and European equities. Plus, we’ve had an institutional net inflow for the quarter, which is something to write home about.

I’m a fan of this one for value. Of course it’s perfectly possible that overall net outflows continue for the foreseeable future, bleeding AUM. That, along with fee erosion, has been a toxic mix for fund managers. But surely it has to hit a bottom somewhere?

GB (LON:GBG)

Down 10% to 238p (£600m) - Trading Statement - Graham - AMBER/GREEN

I tend to agree that the sell-off here was a little harsh this morning, after the company published an update on trading for FY March 2025.

That said, the company did slightly miss the revenue forecast on the StockReport (£288m), revenue coming in at £283m, up 3% at constant currencies.

I think that adj. operating profit is more or less in line at £67m, up 10% year-on-year.

The improvement in adjusted operating profits was “supported by continued cost control, simplification and efficiency improvements”. But watch out for £4.5m of exceptional costs - and I’m not sure how exceptional they really were.

Net debt falls to £48.5m (March 2024: £80.9m).

Outlook (emphasis added):

Looking forward, GBG is well-diversified by region and end market, underpinned by recurring subscription revenues and strong NRR with a more focused and sustainable approach to achieving profitable growth. The Group's strategic progress, including recent innovations such as our new identity platform, GBG Go, means we are well-positioned to capitalise on the attractive long-term structural growth opportunity in our key markets. In the near-term, we expect to gradually accelerate growth, but recognise this may be moderated by the impact of increasing tariff-related macroeconomic uncertainty.

Graham’s view

The market appears to have latched onto the final sentence of the outlook statement which to me seems an overly harsh interpretation of the trading statement. Unless there has been a downgrade to estimates that I’m unaware of?

On balance, I’m inclined to leave my AMBER/GREEN stance unchanged here, the same stance I took in November. A big difference is that the share price was 354p in November, and it’s only 238p today.

EPS forecasts have been stable, which means there’s been a big drop-off in the valuation:

If I liked it at 18x earnings, I guess I should really like it at less than 14x earnings!

In truth, this is not a stock in which I have enormous conviction, but its roster of blue-chip clients has impressed me and I can only see demand for the type of services it provides - identity verification, fraud prevention - increasing over time. So a moderately positive stance makes sense to me.

Mark's Section

Somero Enterprises (LON:SOM)

Down 17% to 203p - Trading Update - Mark - BLACK (AMBER/RED)

Like many businesses, a lack of economic confidence is driving delays. Interestingly, this is now felt in the US as much as the rest of the world, with Somero saying:

While customers continue to report robust bidding levels and healthy project backlogs, economic uncertainty and a lack of clarity around the timing of project starts or resumptions are impacting capital investment decisions. As a result, trading in Q1 was weaker than expected.

Somero has always trumpeted their flexible cost base and they are quick to take action:

…the Company has initiated a targeted operational workforce reduction of approximately 15%...together with a reduction in variable expenses and tighter cost controls, these actions are expected to partly offset the profitability impact of lower revenues in 2025.

These actions are only a partial offset, though. Here’s the impact on FY25 guidance:

· | Revenues of approximately US$ 105.0m (previous market consensus estimate: US$ 113.6m) |

· | EBITDA of approximately US$ 24.0m (previous market consensus estimate: US$ 28.6m) |

· | Year-end cash of approximately US$ 28.0m (previous market consensus estimate: US$ 31.2m) |

As far as I can tell, the consensus here is only their house broker, Cavendish. This is how Cavendish adapts their forecasts to match this update:

We have reduced our forecasts for FY25, with a 7.6% cut in revenue to $105.0m leading to a 16% reduction in adj EBITDA to $24.0m. This results in adj PBT of $21.3m and adj EPS of 29.4¢, both down 17.7%. We also adjust our net cash forecast in line with guidance from $31.2m to $28.0m. Using the group’s capital allocation formula, the lower cash position and lower EPS results in the total dividend reducing by 19.3% to 18.3¢.

Adjusting for today’s fall in share price, this means that the company is trading on a P/E of around 7.5, adjusting for the cash balance, with a yield of around 7%. This seems good value. However, there are two potential problems. The first is that there must be significant amounts of uncertainty in the forward guidance here. As I showed when I reviewed this in January, this is highly dependent on North American sales:

With this market looking shaky, the risk of a further profits warning must be high.

The second issue is that the competition seems to have the edge in Europe, and I can’t see the current messaging from the US administration helping sales in this region.

Mark’s view

In January, I said that I was slightly more positive than Graham on this company. However, that was before the current tariff narrative had made a major dent in non-residential construction confidence in the US. There is a chance that in the medium term, near-shoring has a positive impact on the demand for Somero’s products in the US. However, the short-term outlook looks increasingly negative, hence I am going for a tentative downgrade to AMBER/RED today.

RWS Holdings (LON:RWS)

Down 40% to 71p - Trading Statement - Mark (I hold) - BLACK (AMBER)

This update starts off ok:

The Group delivered 1.3% organic constant currency ("OCC")¹ revenue growth in the period (H1 FY24: -2%), consolidating the return to growth seen in H2 FY24. Reported revenue is expected to be approximately £344m, a 1.8% decline versus prior year.

However, there is a sting in the tail:

Adjusted profit before tax ("PBT") performance in the first half has been impacted by several non-trading items, including foreign exchange, increased amortisation and the impact of the sale of PatBase (all as previously guided) and an increase in the proportion of technology investment being expensed in the year.

Consequently, the Group expects to deliver adjusted PBT of approximately £17m in the first half (H1 FY24: £46m). The non-trading items account for the majority (£23m) of the decline versus prior year, with the balance due to the gross profit impact of the mix changes noted above.

This has the feel of a new CEO kitchen-sinking things (or at least adapting what they consider inappropriate under the previous regime), which then feeds through to FY guidance:

Our updated view of the level of capitalisation of our technology investments will result in an increase in overheads of approximately £8m in FY25, with a corresponding reduction in capital expenditure. While we anticipate an improvement in gross margin in the second half, we expect the full year gross margin impact from mix changes to be around 300 bps. As a result, adjusted PBT is now expected to be in the range of £60m-70m for FY25, based on an H2 GBP / USD FX rate of 1.33.

Bearing in mind that the FY24 results had an adjusted PBT of £106.7m, this represents a 40% year-on-year reduction at the mid-point of the guidance. Adj EPS for 2024 according to the company, was 21.6p, so pro-rata this works out to be around 13.2p. Sadly, individual investors can’t see the research on this company, so we are flying blind to some extent. However, Stockopedia had a 19.5p consensus prior to today’s update. The shares have fallen 34% today which is largely in line with my calculated drop in EPS, so on one level this seems fair.

However, Stockopedia also had this on a forward P/E of less than 6, before today’s update, which suggests that the market didn’t really believe these anyway. The fall therefore looks a little harsh, and the company is back on a P/E of under 6, assuming that the new CEO really has grasped the nettle.

They also say:

Cash generation continues to be strong and the Group had a modest net debt² position of c.£27m at 31 March 2025, after payment during the first half of the £37m final dividend for FY24.

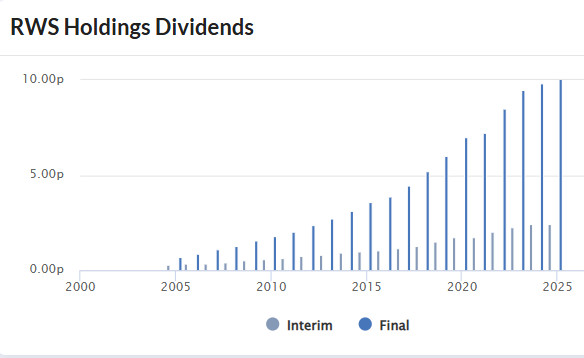

Net debt was £13m at the year end, so this suggests £23m of FCF during the period, for an annualised FCF yield of around 17%. They don’t specifically mention the forward dividend in the update, and a new CEO is always a risk to a large payout. However, I think a new CEO will still be keen to maintain a dividend record that looks like this:

Given the big split between final and interim dividends, I at least expect the interim dividend to be maintained. A held FY dividend would now be a 17.4% yield, covered by FCF.

Mark’s view

When I looked at this in December, I kept the previous GREEN rating. This has clearly been a mistake, with the shares dropping over 60% since then. A series of profits warnings have eroded confidence here, including a huge drop in share price today. However, despite this, I struggle to be too negative. This remains a highly cash-generative business, despite the adjustments and write-downs it has suffered recently. The fall today looks overdone to me, as it leaves the company likely with a 17%+ dividend yield covered by free cash flow. In the past, this would have been the kind of FCF that would have been attractive to private equity firms. However, Andrew Brode’s holding would have always been a blocker to any corporate action:

With Brode having been willing to let £LTG go from the listed markets, there is also the possibility that he will say enough is enough here.

Perhaps AMBER is the best balance between the risks and opportunities.

Brickability (LON:BRCK)

Up 4% to 63p - Pre-Close Trading Update - Mark - GREEN

It is a relatively short update here:

Group revenue for the full year is expected to be approximately £637 million, an increase of c.7% over the prior year (FY24: £594.1 million) and c.1% higher on a like-for-like ("LFL") basis. This outturn reflects good momentum in trading throughout the second half of the financial year, notwithstanding subdued market conditions, and a strong final quarter in the Group's Contracting Division where a number of projects within its specialist cladding and fire remediation businesses were delivered ahead of schedule and prior to the FY25 year-end.

This sounds like there is partly a timing element to this, but the impact is positive:

FY25 Group adjusted EBITDA is expected to be ahead of market expectations at approximately £50.0 million, c.11% ahead of the prior period (FY24: £44.9 million).

This compares to their broker, Cavendish’s, previous forecast of £48.7m. They say:

We are revising our forecasts in-line with company guidance and with FY25E adjusted PBT of £38.0m and adjusted EPS of 8.5p, which are 2.9% and 2.6% above our previous forecasts, respectively. Despite the FY25E upgrades, we make no changes to our FY26E or FY27E forecasts.

This confirms that this is more about timing than a significant step up in trading. However, this has also improved their financial position:

The Group remains in a strong financial position, with leverage3 as at 31 March 2025 expected to be approximately 1.14x, a reduction from both the year ended 31 March 2024 and the half year ended 30 September 2024.

Cavendish calculates this to be £57m versus their previous £60.2m estimate, so this is a handy beat, and helps give confidence in the financial situation of the company.

Given the debt, EV measures are probably best here, and the EV/EBIT of around 5 continues to look good value, for what should be towards the nadir of the construction cycle.

Mark’s view

Roland rated this GREEN in February, and while this upgrade is small and a one-off, it reinforces that this is a well-run business that is trading on a modest rating in difficult market conditions and remains deserving of that view.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.