Good morning and welcome to Friday's report!

The quiet RNS will give me a chance to circle back to some of yesterday's releases that we missed.

Mello 2025: Ed, Mark and I will be at Mello in London next week, which will be a great chance to meet some of you in person. If you'd like to go and haven't booked it yet, we can offer a discount code "STOCKOPEDIA50", which can be used at this link. See you there!

12pm: today's report is finished, have a nice weekend everyone and I'll see you in person at Mello next week, if you can make it! Cheers.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

M&G (LON:MNG) (£5.4bn) | SP +6% M&G becomes preferred asset management partner in Europe for major Japanese insurer. Expected to deliver >$6bn of new business flows for M&G over five years. Dai-ichi Life intends to acquire 15% of M&G through on-market purchases and will then have the right to representation on M&G Board. Trading update: performance year-to-date is “broadly in line”. | AMBER/GREEN (Graham) [no section below] M&G’s total AUM was £346 billion as of Dec 2024 and so >$6bn (£4.45bn) of new business over five years may not be all that material. However, notice that the Japanese company will buy 15% of M&G shares through on-market purchases (regulators permitting) is interesting - and a good reason to mark up M&G shares in advance of those purchases. I’m moderately positive on M&G although I do find it very complex - we looked at its final results in March. | |

Harmony Energy Income Trust (LON:HEIT) (£209m) | Drax offered 88p but that offer has now lapsed in favour of a 92.4p bid from Foresight group (LON:FSG). | PINK [no section below] | |

hVIVO (LON:HVO) (£111m) | SP down 57% Major profit warning. Significant contract cancellation alongside a postponement and a smaller study cancellation. New 2025 revenue forecast £47m if there are no further contract wins (prev: £73m). New op profit forecast: loss of £12.1m (prev: profit of £5.8m). | BLACK (RED) (Graham) Net cash that's nearly as large as the current market cap provides some comfort. But losses are expected to eat into that cash balance this year, and it's difficult to have much faith in next year's forecasts. |

Backlog items (see below): AUTO, BOWL

Graham's Section

hVIVO (LON:HVO)

Down 57% to 6.99p (£48m) - Trading Update - Graham - BLACK (RED)

This is the company formerly known as Open Orphan.

I’m dismayed to report that this is an enormous profit warning.

Here are the numbers from Cavendish (many thanks to them for publishing on this first thing):

FY Dec 2025:

Revenue forecast down 36% (from £73m to £47m)

Operating profit forecast reduces from £5.8m profit to £12m loss.

Future years are also severely impacted:

FY Dec 2026: operating profit forecast cut from £10.9m to £3.6m.

FY Dec 2027: operating profit forecast cut from £15.2m to £8.2m.

Of course it’s difficult to have confidence in any 2026 or 2027 profit forecasts in this situation.

Turning to the company’s statement:

hVIVO… has received notification of a significant human challenge trial ("HCT") contract cancellation alongside a postponement and a smaller study cancellation. These client decisions are believed to be related to the current uncertainties in the pharmaceutical industry and the continued depressed biotech financing market. The current volatility in the pharmaceutical industry, particularly in the US, is impacting the whole CRO industry and has led to an increase in cancellation rates, postponement of clinical trials, and delays in approvals for new projects.

There are a few silver linings.

The new £47m revenue forecast is based only on contracted revenue for the current year - and the company “expects to achieve further contract wins during the course of FY25”.

Also, the sales pipeline is “at a record level”, with “high probability opportunities” that should provide “significant revenues in FY26”.

Recent acquisitions are said to be “progressing well”.

However, there is no getting away from the fact that this is an enormous profit warning.

CEO comment excerpt:

"Whilst we are disappointed to have received notification from these clients due to matters beyond our control, we still remain confident in the continued growth of human challenge trials and the overall prospects for hVIVO as we also continue to diversify our revenue streams and build our offering as a full-service CRO [contract research organisation].

Graham’s view

I have to be RED on this in the aftermath of an enormous profit warning that sees the company swing from a forecast profit into a large forecast loss.

However, I am open to upgrading my view on this once the dust has settled, as I note that the company had cash of £44m as of December 2024. With a market cap now of only £48m, one could argue that it’s in deep value territory here.

However, the operating loss forecast this year can be expected to take a large bite out of that cash balance. And then we’ll be relying on an improvement in 2026 to bring it back up again.

I'm no expert in this sector, but I'm willing to take the company at its word that macro factors are responsible for increasing the risk of contract cancellations. So let's hope that they can get back on track once the "volatility" in the pharma industry has died down.

However, one unfortunate feature of the company’s current governance is that the ownership of Board members has reduced. The CEO currently owns 0.6%, as does one of the NEDs.

Chairman and co-founder Cathal Friel previously held a 3.1% stake, which he sold last year with the share price at 29p (“to satisfy institutional demand”). He is not seeking re-election to the board at the AGM next week.

This context is another reason for me to be a little doubtful about recovery prospects here - commiserations to anyone holding this one.

Backlog

Auto Trader (LON:AUTO)

Down 10% yesterday, now at 793p (£7.0bn) - Graham - AMBER/GREEN

These results were considered underwhelming by the market yesterday.

Key points:

Revenue +5% (£601m)

Operating profit +8% (£377m)

EPS +12% (31.66p)

This is an exceptionally high-quality company - look at the conversion from revenue to operating profit. We rarely see margins like this in any industry, but profitable “marketplace”-type stocks are able to do it.

An important reason for this is that successful marketplaces tend to resemble monopolies: this lets them generate above-average margins and returns over the long-term. Auto Trade says “we remain more than 10x larger than our nearest competitor”.

Maintaining and fully exploiting that position does require ongoing development, however. AutoTrader’s AI tools, collectively referred to as “Co-Driver”, are now helping retailers to quickly generate effective cars ads.

At the same time, Deal Builder helps buyers to set up their purchase online, and is now part of Auto Trader’s “core advertising proposition”.

Market overview: high demand for used cars, and limited supply of cars aged 3-5 years, “has led to cars selling at a faster rate than any time our recent history”.

However, this hasn’t helped Auto Trader’s revenues:

We have seen a 5% increase in the number of cars advertised through Auto Trader which is slightly higher than the increase in overall used car transactions. Fast speed of sale has meant retailers have benefitted from increased utilisation of Auto Trader's slot-based advertising model. As a result, even though consumer and retailer activity have both increased, it has not directly benefited revenue…

As for new cars, the retail channel saw a 4% decline last growth but is up 6% so far in 2025. The company has a positive outlook here:

With the announcement of a UK/US trade deal and the Government's plans to soften the Zero Emission Vehicle ('ZEV') mandate, we expect overall new car registration volumes to be well supported over the next two to three years.

CEO comment excerpt:

"Despite broader macroeconomic uncertainties, the UK car market is in good health and we continue to deliver against our strategy to improve car buying and retailing."

"We remain confident in the outlook for the business given our strong market position, the value we deliver for customers, and our unique data and technology capabilities."

Outlook: retailer revenue growth was only 5% last year, and the speed of sale remains an issue for Auto Trader in the current year, but they do expect retailer revenue growth of 5-7% for 2025.

Losses at Autorama, owner of van leasing company Vanarama, will reduce in line with expectations.

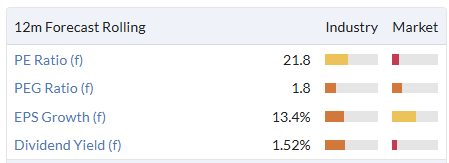

Graham’s view

I think the quality of this company is largely undisputed. The question is how to time an entry - it tends to trade richly (PER in excess of 20x almost as a rule) and so investors have to balance that against their desire to own a company with a formidable competitive position.

Today, I’m happy to give this an AMBER/GREEN.

An overly simplistic strategy that I’ve used in the past is: for a very high-quality company that I’d be happy to own long-term, I’m generally ok with buying it below a PER of 20x, even if the growth outlook isn’t very impressive.

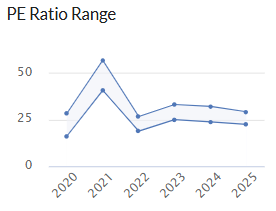

Auto Trader is now trading at around 22x:

There’s no shortage of car buyer criticisms to be found, especially to do with the site having too many ads in its search results, and too many non-local “cinch” results. Dealers will often complain about Auto Trader, too.

But that’s natural when a company achieves monopoly status in its sector: you become a magnet for complaints.

Given its competitive position, I think the stock is a fine buy-and-hold candidate. But I do like to hold out for a juicy entry point, and I'm not sure we are there right now.

Hollywood Bowl (LON:BOWL)

Down 8% yesterday to 266p (£448m) - Half-year Results - Graham - AMBER

There was little hint of a profit warning in yesterday’s headline, but the shares fell 8% anyway:

STRONG PERFORMANCE AND PROFITS IN LINE DRIVEN BY INVESTMENT IN GROWTH STRATEGY AND CONTINUED DEMAND FOR FAMILY-FRIENDLY, AFFORDABLE LEISURE

Like-for-like revenue growth was only 2.1%, having been negatively impacted to the tune of 1.1% by some calendar effects (Easter/leap year). So I guess that “real” LfL revenue growth was 3.2%.

Canada led the charge with LfL 3.7%, vs. UK only 1.5%.

And Canada also saw 13.6% growth in overall revenues as it expanded to 15 centres (vs. 75 in the UK).

H1 adjusted PBT fell 9% to £28.0m. Actual PBT fell 4% to £28.3m ~ nice to see that there is little difference between the adjusted and actual figures.

Capex: there was a £20m capex spend in H1, of which £14m was expansionary. This tends to depress profits in the short term as high depreciation charges are incurred on new capital whose profitability has not yet matured.

Outlook:

On track to have 130 total centres by 2035 (I’m not used to seeing a company with a 10-year goal!)

“Resilient demand” and “well insulated from inflationary pressures”. Low labour-to-revenue ratio of <20% in the UK.

But this is where investors and analysts start to worry:

The recent warm and dry weather - marking the driest spring in over a century - has had a short-term impact on trading over that period. In response, we have proactively managed margins and costs, maintaining strong operational performance, which remains at historically high levels.

Despite this temporary headwind, we remain confident in our outlook for the second half of the year. We are well-prepared for the key July and August holiday period and continue to expect full-year EBITDA to fall within the range of current analyst forecasts.

“Within the range” of forecasts is fair enough, but perhaps the company could be slightly more forthcoming and say that they expect to be towards the middle, the top, or the bottom end of the range?

The company's brokers are Investec and Berenberg. Rival broker Peel Hunt cut their PBT forecast for BOWL yesterday from £52.6m to £50m, according to Proactive Investors.

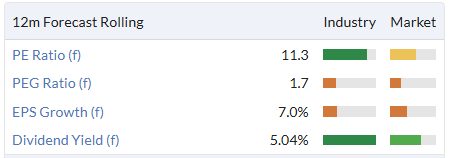

Net cash is £23m before leases and the company continues to pay a useful dividend (yield c. 5%).

Graham’s view

Roland covered BOWL’s half-year trading update in April and while generally taking a positive view, he noted that LfL growth was starting to look weak.

I’ll downgrade our stance now, as I think there is a heightened risk of an "official" profit warning later in the year. I also feel the company could be more helpful when it comes to providing forecasts.

My overall impression of Hollywood Bowl remains positive. Unlike many of the capital-intensive leisure businesses we cover, it does generate profitable returns. Even more impressively, it has been doing this while it expands, which is no mean feat.

So at this valuation it still could be interesting:

But my AMBER stance reflects the short-term risk that weak LfL growth persists, and as stated above, the risk of an "official" profit warning.

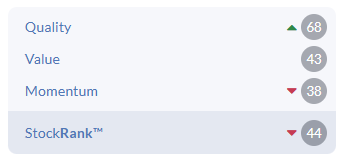

The momentum trend is not currently BOWL’s friend, and is deteriorating:

PS: to hedge against dry and warm weather, perhaps BOWL shares would pair well with cider maker CCR. Therefore, come rain or shine, at least one of the companies in the portfolio would be happy about the weather. I'm sure you can think of more examples where the weather risk could be hedged!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.