Good morning!

I'm back from Mello, which was a triumph as usual, and will be with you for this morning's news. It was great to meet so many subscribers in person. Feel free to put any Mello highlights in the DSMR comments below.

Graham has updated the rating tracking spreadsheet for the over 500 companies we have covered recently on the DSMR. Check it out here.

Companies Reporting

Name (Mkt Cap) | RNS | Summary | Our view (Author) |

Wise (LON:WISE) (£13.7bn) | Rev +15% to £1.2bn, PBT +17% to £565m. Continued benefits of high interest rates. Intention to move primary listing to the US. |

AMBER (Megan) The currency transfer specialist has only been listed in London since 2021 and in that time it has delivered some remarkable growth metrics, which have been continued in these numbers. But investors have not responded as company executives would have liked (perhaps because of underlying fears from the history of currency transfer companies). Another British company looking to seek fairer fortunes in the US. At least we get to keep the secondary listing. | |

Unite (LON:UTG) (£4.19bn) | Sale of student properties with a total of 3,656 beds across five cities at a 1% discount to December 2024 book value. | ||

MITIE (LON:MTO) (£2.01bn) | Record contract awards and total order book +35% to £15.4bn. Net debt more than doubled to £199m. Proposed £366m cash and shares acquisition for AIM-listed peer. | AMBER/RED (Mark)

Some impressive top-line figures don't make it into the EPS. Negative working capital, and now debt taken on to fund an acquisition that doens't look obviously cheap, adds to the risk of a blow-up that all outsourcers seem to have periodically. | |

Fevertree Drinks (LON:FEVR) (£1.08bn) | Low single digit revenue growth in line with expectations. 10% US tariffs will be shared with US distribution partner Molson Coors. | ||

Wizz Air Holdings (LON:WIZZ) (£1.73bn) | Fleet size +11% but passenger numbers up just 2%. Rev +4%. Summer fares expected to be slightly lower than last year. | ||

CMC Markets (LON:CMCX) (£796m) | Net operating income +2%, with especially strong growth in Australia. Underlying EBITDA +12%. | BLACK/AMBER (Mark) This is a miss versus expectations at the profit level, driven by higher than expected costs. Given their history with IT developments and dedication of a significant amount of commentary to new developments without immediate impact, those concerns over costs are only getting more serious. As such, even a relatively cheap (cash-adjusted) rating doesn’t overcome the risk of further profit downgrades. | |

Workspace (LON:WKP) (£779m) | Net rental income (after accounting for disposals) -3%. Company back in profits. | ||

Young & Co's Brewery (LON:YNGA) (£612m) | Rev +24.9% to £485.8m, Adj EPS down 1.8% to 61.84p. Net debt excl. leases £336.3m down 6.5%, Net Assets flat at £774.4m. | ||

Dr Martens (LON:DOCS) (£579m) | Rev down 8% cc to £787.6m in line with guidance. Adj. PBT £34.1m (FY24 £97.2m). Net debt excl lease liabilities £94.1m (£177.5m). Total dividend 2.55p as previously guided. “We expect the FY26 Adjusted PBT to be within the range of market expectations” Tariff impact unknown. | AMBER/RED (Megan) The market is celebrating a very welcome decline in inventories and debt, which leaves the balance sheet in significantly better shape. But I remain unconvinced that the turnaround is in full swing. | |

Marlowe (LON:MRL) (£318m) | 1.1 New Mitie Shares & 290p cash for each Marlowe Share | PINK | |

Griffin Mining (LON:GFM) (£306m) | Rev $135.1m (2023: $146.0m). PBT $17.9m ($24.5m), EPS 6.08c (8.03c) | ||

Big Technologies (LON:BIG) (£297m) | Disputed companies have agreed not to dissipate assets. | ||

Jubilee Metals (LON:JLP) (£120m) | Binding offer from private mining and metals trading company to acquire the Group's chrome and PGM operations in South Africa for a consideration of up to US$90 million. | ||

Palace Capital (LON:PCA) (£69.3m) | £35m assets sold at 6% premium to book. Rental income down 50% to £4.8m. Adj. EPS down 18% to 11.3p. EPRA NTA per share 251p. Net cash £22.2m (FY24: £11.5m) | ||

Van Elle Holdings (LON:VANL) (£41.7m) | Profits Warning. Rev -4% to £134m. FY25 U/L PBT £3.5m. Net Cash £1m (FY24: £5.5m). £6.5m headroom on facilities. Order Book £41.5m +£10m award in May (FY24: £35.1). | BLACK/AMBER (Mark - Hold) A second recent profits warning means that investors should be very cautious about forward earnings-based valuation judgments here, as fundamental momentum is clearly against the company in the short term. However, there is a reasonable discount to TBV and strong reasons to think that medium-term trends in housebuilding, energy, rail and water infrastructure are tailwinds, not headwinds. Adding to this, the highly activist shareholder base will no doubt be pushing for their assets to be made productive again soon, or sold to someone who can use them better. | |

Tern (LON:TERN) (£11m) | Loss £3.8m (FY23: £12.6m loss). Net Assets per share 2.0p (3.2p). |

Megan’s Section:

Wise (LON:WISE)

Up 9% to 1181p (£13.8bn) - Final Results - Megan - AMBER

It is rare to come across a company which epitomises the network effect quite as well as Wise. Since its inception in 2011, it has been on a mission to lower the cost of cross border payments - about £32trn of which occur annually, with an estimated £200bn in hidden fees.

By offering lower and more transparent fees, it has managed to build a customer base of 15.6m, up 22% on last year. And in building a bigger customer base, it is able to charge increasingly low fees (down 14 basis points to 53bps per customer this year), thus helping boost its customer base even further. In FY2025, £145bn of money was transferred across borders using Wise systems - well over double the amount of money moved four years ago when the company listed.

Wise generates revenue from two divisions, personal money transfer and business transfers. Personal transactions continue to account for most of the customer base and 76% of the operating income. In FY25, personal operating income rose 18% to £1bn, while business operating income was 12% higher at £322m.

The company also splits its top line figures into two lines: revenue (which refers to the fees collected for moving customers’ money across borders) and interest rate income on the first 1% of the gross interest yield on customer balances. Roland has explained the mechanics behind the interest rate income here, but put simply, the company aims to return 80% of the income generated from interest on cash held in its accounts (although that isn’t always possible owing to regulation). In FY25 cash held with Wise was 5.7 times higher than last year at £21.5bn and the company generated £444m in interest over 1% on those accounts, retaining £283m.

More investment, more growth

Like many asset light businesses, Wise boasts excellent operating leverage which means while sales rose strongly in the period, the cost of those sales was just 7% higher. The company reported underlying gross margins of 75% and reported gross margins of 85%.

Excellent profitability gives way to more investment in future growth. In FY25, the company expensed £129m of costs related specifically to product engineering. Within operating costs, management reported a 23% increase in investment on tech (to £66m) and a 47% increase in investment on marketing (to £54m). Marketing-related expenses are expected to triple over the next few years.

Good quality metrics

Underlying pre-tax profits (excluding the contribution of interest payments) rose 17% to £282m - an underlying PBT margin of 21%. That is well ahead of the medium-term guidance for underlying PBT margins of between 13% and 16%, although management does concede that this is likely to be higher in FY26 as well.

Underlying free cash flow was 35% up at £332m, a FCF conversion rate of almost 120%.

This is an asset-light business with £13.9bn in cash on the balance sheet (more than the entire market capitalisation of the business at the moment) and very little debt. Lease liabilities of £85.3m are primarily related to office space, on which the company took an £11.5m impairment this year.

Megan’s view:

There is very little not to like about Wise, except for the sector in which it operates. Currency transfer companies don’t have a great track record on the market, and perhaps it is that which has kept investors on the fence.

Now, the founders are seeking their fortunes elsewhere by transferring the primary listing to the US. Management is quite honest about the reasons for moving the listing, but does fall short of saying ‘we want our share price to be higher’ (there are some words about liquidity instead).

I understand the UK market’s reticence, but it does seem a shame when this is a high-quality, fast-growing tech company that the LSE craves. The US listing process should reveal any demons, so I will withhold a more positive stance until then. AMBER.

Dr Martens (LON:DOCS)

Up 22% to 73p (£578m) - Final results - Megan - AMBER/RED

The market seems relieved that Dr Martens’ results for both FY25 and forecast numbers for FY26 are “in line with expectations”. There is nothing more spectacular than that in these numbers, and yet the share price has leapt more than a fifth in morning trading. Expectations for this troubled retailer were clearly not high.

In line means a 10% decline in sales to £788m (or -8% at constant currencies), with reported revenue down across all three of the company’s operating regions. Adjusted pre-tax profits were 15% lower at £34.1m and, after taking into account impairments, costs associated with restructuring and other exceptional costs, reported PBT was just £8.8m.

Digging into the minutiae of the operating performance reveals a few more positives. The catastrophic pace of revenue decline reported in the first two quarters (-17.6% and -18.2% respectively) has slowed in the second half. Revenues fell 2.8% in Q3 and 5% in Q4 thanks to a steadying of the e-commerce and DTC channels. Both the Americas and APAC regions performed better in the second half as well, although the performance definitely can’t be called reassuring. Across all its regions, Dr Martens continues to be impacted by wider market promotional activity, while the wholesale arm suffered again as partners shifted excess stock.

That stock shift has, however, had a positive impact on the balance sheet as inventory levels come back to a much more normal level. Alongside the fire sale of stock through wholesale channels, management chose to spend significantly less on new inventory, meaning total inventory levels fell by £62.7m - ahead of the £40m target.

Net debt has also fallen quicker than management had previously guided. With bank loans and lease liabilities falling alongside an increase in the cash position, net debt came in just under £250m. This is below the £310m target and the £360m figure reported this time last year.

There is also better news from the restructuring activity, which was initiated in 2024 and seems to be delivering results. Management says it has cut £25m of annualised costs, ahead of expectations, with these savings reportedly already having an impact in FY25 numbers (although it’s hard to tell exactly where, because the profit numbers aren’t impressive).

Those cost savings did come with one-off expenses which impacted reported profits this year, but the market seems optimistic that numbers will be better in the year ahead.

Megan’s view:

There is undoubtedly progress in the turnaround here. Management has done a good job to get the balance sheet in much better shape than it has been for many years.

There is still work to be done, though, and I fear today’s major share price jump has been a little premature as the company struggles to return to growth. I’m going to keep the rating at AMBER/RED.

Mark’s Section:

CMC Markets (LON:CMCX)

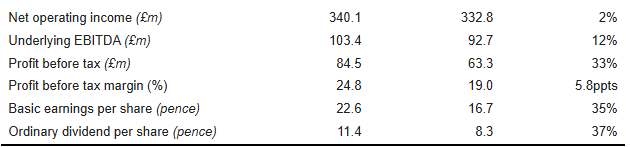

Down 12% to 250p - Final Results - Mark - BLACK/AMBER

As others have pointed out in the comments, there is a whole lot of verbiage in the results commentary, mainly about new markets that they are allowing traders to access. However, at the heart of this business is a very simple model. They generate revenue from traders and investors who trade and invest, with the profit being the difference between the income and the cost of operating the platforms used. Here are the headlines:

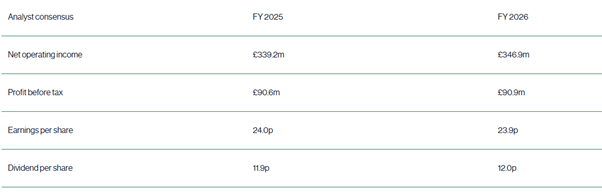

This is how it lines up with the consensus on their website, that I captured for The Week Ahead:

So this looks like a miss to me. Net operating income is in line, but PBT comes in 7% below, and EPS 6% under the consensus. Dividends are typically 50% of EPS, so this comes in below as well.

Given the miss is below the line, it is tempting to think that the issue here is costs, but I think this may be more complicated than that. They say:

Net operating income increased by 2% to £340.1 million (FY 2024: £332.8 million) but was impacted by periods of weaker trading revenue early in the second half of the year, which was partly offset by a rebound in performance towards the end of the year, in part as a result of a revised hedging strategy we implemented in late January as well as increased volatility.

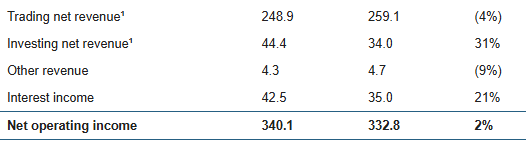

This appears to be a change in hedging strategy, presumably to protect them against Trump-related market volatility. My very simple understanding of the sector is that IG tend to be fully hedged, and hence lower risk against market moves, while Plus500 tend to be less hedged, relying on the fact that most clients lose money over time. CMC tend to sit in between with what they call a dynamic hedging strategy. Historically, this has given them an advantage - higher returns per trading volume than IG, but lower risk than Plus500. So it is the drop in net trading revenue that may be the issue here. Investing revenue has grown strongly, but is a much smaller part of the revenue pie:

Sadly, their results presentation no longer includes the previous set of KPIs with gross client income and percentage retention, which enabled investors to judge the success of their dynamic hedging strategy.

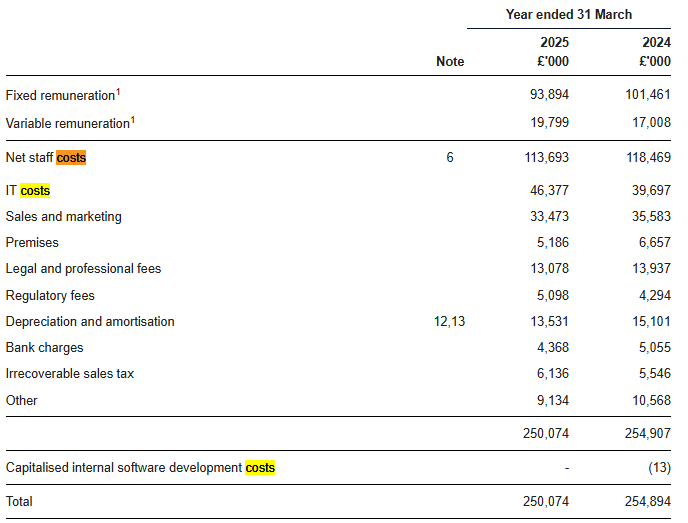

Then on the cost side, almost every item is down, apart from bonuses reflecting higher profitability, and IT costs:

It is worth noting that they don’t play games by presenting adjusted figures to investors. While they do capitalise some intangibles, they are relatively modest compared to the overall staff costs, and roughly match amortisation. They don’t exclude share-based payments or classify a lot of costs as one-off. This is a refreshing change compared to an increasingly aggressive stance on accounting adjustments by many companies today. The result is that this is a genuinely cash-generative business.

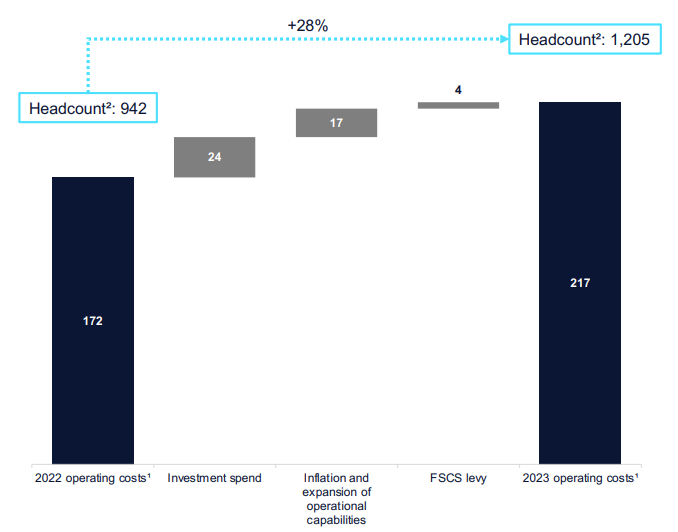

However, CMC have a rather chequered history of IT and IT Staff costs. They were a major beneficiary of strong trading revenues in 2020/2021, but also increased their costs significantly, investing in developing a non-leveraged trading platform for the UK. (They already had an Australian investing platform.) As far as I can tell, this has failed to gain traction in the UK market and seemed to cost far more than originally planned. From 2022 to 2023 their headcount increased 28%:

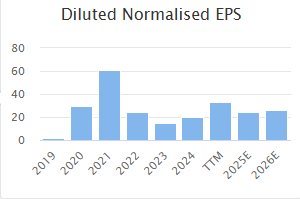

This led to a significant reduction in EPS associated with these increased costs:

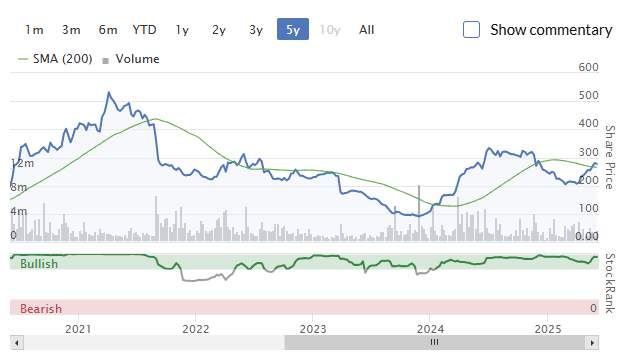

The share price went from over £5 to below £1 briefly:

The profitability and share price only started to recover when the company started to cut costs, in the FY24 results, saying:

Annualised savings of £21 million to be realised in FY25, with one-off cost of circa £4.3 million in FY24

Therefore, this part of this morning’s results presentation may worry some:

They continue to focus on reducing core costs. However, this is more than offset by planned investment into growth areas. Their narrative is that the move to “tokenised” trading and 24-7 markets will more than offset this in terms of net trading income. However, the history of their delivery of a UK non-leveraged platform suggests that there is a risk that they are overestimating the impact and underestimating the costs required.

With all this going on, it is unsurprising that the share price has been volatile this morning:

Outlook:

The bit of the outlook statement that actually matters is:

Recent trading conditions have also been supportive, providing good momentum into FY 2026

Which is vague but positive. Prior to today’s update, analysts were forecasting flat EPS for FY26, with modest Net Operating Income growth offset by higher costs. It will be a while before analysts update their models following today’s results call, and those updates make it into the consensus. So in the absence of better information, I think we should take this morning’s EPS as the most likely forward figure.

Valuation

At around 250p the historical (and perhaps most likely forward) P/E is 11. This isn’t obviously cheap for a fairly static EPS figure. However, the company also has significant amounts of net cash. £248m is around 89p a share, meaning the cash-adjusted P/E could be considered a far more reasonable 7x. Not all of this will be distributable as it will need to be retained for regulatory capital. However, this makes the company look cheap, especially if investors believe that the significant ongoing investments will lead to more rapid growth in net income in the medium-term.

Mark’s view

This certainly doesn’t look expensive for a very cash-generative business, especially when one adjusts for the amount of cash on the balance sheet. There are no games here with the type of adjustments that plague so many companies these days, either. However, they have clearly missed expectations with increased costs. Given their recent history with IT spend on an unleveraged platform, there has to be a major worry that costs will get out of hand again on projects of dubious real returns. This is reinforced by a significant proportion of the commentary being related to investment into things such as a multi-asset wallet or tokenised access to financial products. I may just be old and/or curmudgeonly, but none of these are things I understand or want to access to! Even something I understand, like 24/7 trading, sounds like an unnecessary distraction from the things that will really compound my wealth.

As such, it would seem sensible to wait and see if these initiatives gain traction quickly enough for net operating income to grow faster than costs. Otherwise, the share price seems at risk of tracking the earnings lower. Graham rated this GREEN recently, but given today’s miss versus expectations and concerns over growing costs, I think this has to be downgraded to AMBER.

Van Elle Holdings (LON:VANL)

Down 5% to 37p - Trading Update - Mark (I hold) - AMBER

I last looked at this company in detail when they warned in March. At the time, their broker, Zeus took 6% out of FY25 revenue forecasts to £137.3m. With the financial year ending on 30th April, we get the unaudited figures:

Group revenue for the year is expected to be £134m, approximately 4% below the previous year, reflecting the challenging market conditions that have prevailed throughout the Period.

We then get the impact on profits:

Despite these challenges, as a result of a strong operational performance the Group delivered stable gross margins and with a focus on cash management, undertook several cost saving initiatives. Consequently, underlying profit before tax for FY25 is now expected to be approximately £3.5m.

While they don’t explicitly say this, this sounds a lot like a profits warning. Something a look at the updated Zeus note quickly confirms:

FY25 revenue of £134.0m is down 4% yoy (FY24: £139.5m) and 2.3% below Zeus’ £137.2m estimate, which was previously reduced from £146.1m at the time of the March trading update. In terms of profitability, PBT reduces from our expectations of £4.0m in line with today’s guidance of £3.5m.

EPS is reduced by around 14% to 2.4p. The reasons given are:

…widespread delays to contract start dates, in particular due to significant delays to Building Safety Act ('BSA') approvals. The start of several major contracts which were due to commence in the final quarter of FY25 have now been deferred into FY26, impacting the final quarter performance.

While I don’t doubt these reasons are genuine (it seems the lack of BSA approvals has been a real problem for the industry and something the new government has been keen to correct), the story of delays from FY25 to FY26 doesn’t seem to be supported by Zeus, who also reduce future year estimates:

In FY26 and FY27 we reduce revenue forecasts by a similar amount to today’s change, bringing outer year revenue to £149.4m and £160.2m, respectively. This feeds through to a 12-14% reduction PBT of £6.0m (prior: £7.0m) and £8.0m (prior: £9.2m) in FY26 and FY27, respectively.

This may just be caution on the part of brokers, but I can’t remember a company where a delay of contracts between fiscal years led to a downgrade of the current year and an upgrade to the following year. It is far more normal to get what we see here, which is a multi-year downgrade. Progressive, in contrast, maintain their £7.0m and £9.9m future years PBT estimates, but it sounds like they may be setting us up for a downgrade unless market conditions improve prior to next month’s results. We also get an update on net cash from the company:

The balance sheet remains strong. Net cash as at 30 April 2025 (excluding IFRS 16 property and vehicle lease liabilities) was £1.0m (30 April 2024: £5.5m) after investment for growth in capital equipment and acquisitions, including the final consideration payment of £1.9m for Rock & Alluvium, and the initial net cash consideration of £1.3m for Albion Drilling. The Group's current funding facility of £8.0m has £6.5m available for drawdown, providing significant liquidity headroom.

Zeus previously had £2m net cash estimate, whereas Progressive say £1m was in line with their forecasts. The headroom doesn’t sound huge compared to the size of their turnover. However, they must consider it ample as they used the £2.9m consideration they received for their logistics assets post-period-end to reduce the size of their funding facility. Again, Zeus and Progressive vary significantly in their forecasts, with Zeus expecting modest improvements in net cash in subsequent years, whereas Progressive see net cash building to almost £11m by the end of FY27, which would be a quarter of the market cap.

Valuation

With such a wild difference between some of the key factors between brokers, it is quite challenging to make a valuation judgment based on earnings. Taking Zeus as the most cautious (which is probably wise, as we are already on the second recent profits warning), they are on 9x forward earnings. This isn’t obviously cheap. Although, there are several reasons to think that they are ahead of several multi-year positive trends in housebuilding, energy, water and rail infrastructure projects.

What gives me greater confidence that this may be undervalued is the price to TBV is currently 0.75. Larger, and much more productive peer, Keller, trades on 2.28xTBV. While I don’t think Van Elle could justify this sort of rating, it does show the difference that could be made if Van Elle can improve the productivity of their assets.

Mark’s view

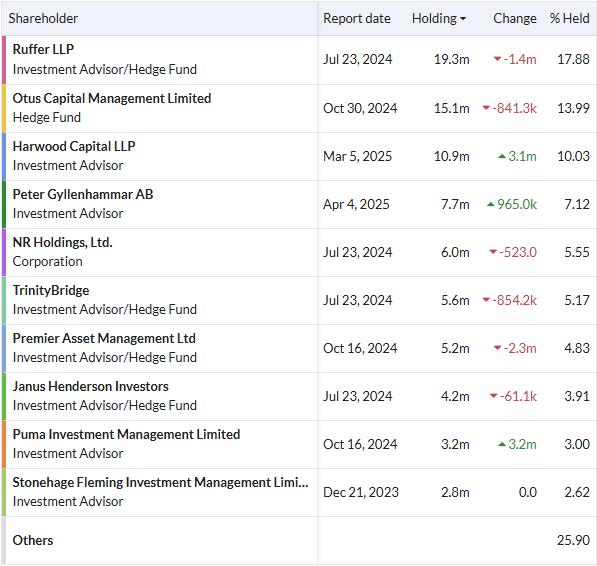

As a very experienced and successful investor pointed out to me at Mello yesterday, the shareholder register here is not the type to sit back and let this trade sideways for years:

Rockwood/Harwood have already instituted a management change a couple of years ago. Peter Gyllenhammar has been adding recently. Ruffer and Otus tend to be more gentle activists, but I see no reason why they would support actions to out value here.

Still, there is no getting around the fact that this is the second profits warning in short succession. As such, a downgrade to AMBER seems the best balance between a share that could still be good value, but for which short-term fundamental momentum is going in the wrong direction. Personally, I had been reducing into recent strength as the share price had been unusually strong on no news, but I added again on this morning’s dip. Although it must be noted that my position size is smaller than it was a few months ago.

MITIE (LON:MTO) / Marlowe (LON:MRL)

FY Results & Offer for Marlowe - Mark - PINK/AMBER/RED

This is the other big news this morning, with Mitie making a bid for Marlowe.

Under the terms of the Acquisition, each Marlowe Shareholder will be entitled to receive: for each Marlowe Share 1.1 New Mitie Shares and 290 pence in cash

They say this is a 26.5 per cent. to the closing price, 38.8 per cent. premium 3-mo VWAP and 41.7 per cent. to the 6-mo VWAP. However, this was based on a Mitie share price of around 160p, and it is now trading around 140p. This values the bid at £4.44 instead of £4.66. Still, with a goo chunk of the bid in cash, this is only about 5% off the bid price.

The bid price probably isn’t helped by Mitie scraping their share buyback to pay for it. It is hard to disentangle the effects of the share buyback change, meger arbitrage and that Mitie also released their final results this morning:

Lots of things are moving in the right direction:

· | Revenue1 up 13% to £5,091m (FY24: £4,511m), including 9% organic growth primarily driven by new contract wins and scope increases, pricing and projects upsell, alongside a 4% contribution from acquisitions | ||||||

· | Record contract awards2 up 21% to £7.5bn TCV of wins and renewals/extensions (FY24: £6.2bn) | ||||||

· | Record total order book2 up 35% to £15.4bn (FY24: £11.4bn), reflecting book-to-bill ratio of 1.47x; renewals rate fell to 59% (FY24: 79%) reflecting the loss of two public sector contracts | ||||||

· | Record pipeline up 27% to £23.7bn (FY24: £18.6bn), of which >70% is due to be awarded in next 18 months | ||||||

· | Operating profit before Other items3,4 up 11% to £234m (FY24: £210m | ||||||

However, EPS is virtually flat:

Basic EPS before Other items up 3% to 12.7p (FY24: 12.3p), with the benefits of higher operating profit and share buybacks offsetting a 4.8ppt increase in the effective tax rate to 23.7%, and higher finance costs

This is a handy beat on the 11.5p forecast in the Stock Report, but a P/E of 12 doesn’t seem particularly cheap for such modest bottom-line growth. There are some pretty big adjustments in there too:

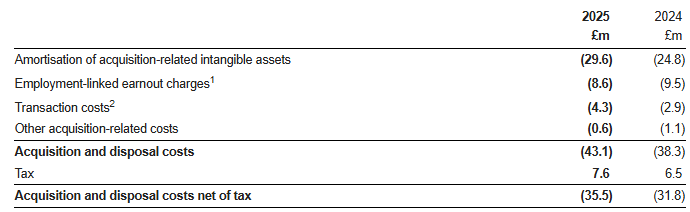

While its normal these days to exclude amortisation of acquired intangibles, the other lines are hardly one-offs, as today’s offer for Marlowe shows, the rest appear to be a normal part of Mitie’s business. They also say:

Strong balance sheet with post-IFRS 16 leverage of 0.8x average net debt/EBITDA5 (FY24: 0.6x), at the low end of our 0.75-1.5x target range; covenant leverage of zero

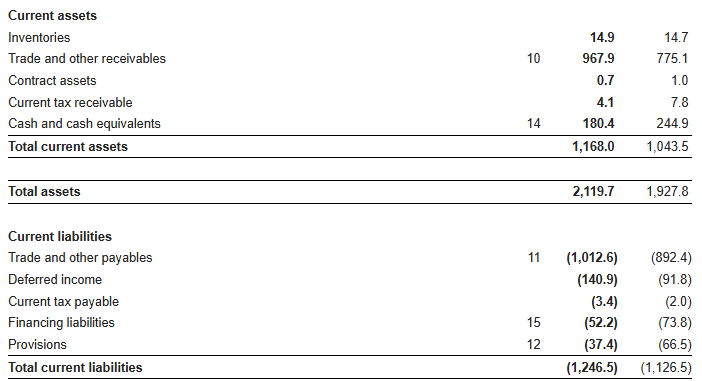

The leverage ratio may be modest, but I’m not sure I’d call the balance sheet strong, as like many outsourcers, they have negative working capital:

This means that they are only one large onerous contract away from a rights issue, or worse. Marlowe, in contrast, has a 1.69 current ratio. Mitie will be taking on £275m of debt to pay out the 290p/share to Marlowe shareholders.

Mark’s view

Marlowe didn’t look cheap prior to today’s news:

Especially as their EPS track record is quite patchy:

Which makes the deal look quite attractive, even if the premium is relatively modest when the fall in the Mitie share price is taken into account. However, Marlowe is fairly conservatively financed for their sector, and I can easily understand why shareholders there will be keen to take the offer but protect themselves by selling the Mitie shares they get as soon as possible. I’m AMBER/RED there.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.