Good morning!

Despite ongoing political/military events, the FTSE is set to open unchanged this morning at about 8850.

12.15pm: it's a clean sweep, as we've covered all of the day's news! See you tomorrow.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Entain (LON:ENT) (£4.8bn) | SP +9% to 824p | AMBER (Roland) [no section below] Forecasts I’ve seen prior to today have suggested that Entain is expected to generate EBITDA of c.$1,100m this year. This suggests today’s upgrade could be equivalent to a c.5% increase to full-year estimates. The positive operating leverage implied here (the extra revenue has largely dropped through to EBITDA) suggests to me that BetMGM could report further improvements in profitability if revenue continues to rise. However, Entain’s profitability as a group has been poor in recent years and the shares were already trading on nearly 17x forward earnings prior to today’s gain. Net debt is also a little high for my liking. The algorithms view this as a Momentum Trap. I would want to see evidence of improved profitability and deleveraging before taking a positive view. | |

Assura (LON:AGR) (£1.6bn) | Assura’s board are reviewing PHP’s offer document and they assure shareholders of their objectivity. | PINK (Roland) [no section below] Assura’s board recommended KKR/Stonepeak’s cash offer last week, but PHP issued full offer documents and a detailed discussion of its offer on Friday, pointing out that at that time, the PHP cash/shares offer was worth 53p, slightly more than the KKR/Stonepeak cash offer (52.1p). Assura’s board now seems keen to reassure shareholders that the PHP offer is getting a fair hearing. Regardless of which offer succeeds, competition for AGR’s assets has most likely pushed up the price shareholders will receive. I share Graham’s view that it would be nice to see this business continue as a UK-listed entity as part of PHP, but there’s no doubt that would also be the more complex deal to complete. | |

NextEnergy Solar Fund (LON:NESF) (£404m) | NAV -9.2% to 95.1pps (£547m). Dividend +1% to 8.43p, covered 1.1x. FY26 dividend target 8.43p. | AMBER (Roland) | |

Costain (LON:COST) (£351m) | FY25 trading in line with exps, on track for 4.5% op margin. Forward work position 4x annual revenue. | GREEN (Roland) | |

Peel Hunt (LON:PEEL) (£107m) | Revenue +6% to £91m, LBT of £3.5m. Net assets £89m, cash £20m. FY March 26 has started more positively than February and March 2025. | GREEN (Graham) Happy to stay GREEN on this due to balance sheet strength (reducing risk) and the prospects for some recovery in activity levels. I do wish it had the discipline to insist on a breakeven result, even in very difficult years such as this. | |

Triad (LON:TRD) (£56m) | Rev +50% (£21.4m). PBT £1.5m. Good visibility of future work. Substantial OPSS contract. | AMBER (Roland) [no section below] Graham took a neutral view on IT consultancy Triad in November. The firm’s share price is almost unchanged from that level today. Although revenue growth was strong last year and profitability improved, an operating margin of 7% doesn’t seem that high to me for a consultancy. I wonder if remuneration is generous; I note the three senior executive directors enjoyed c.15% pay rises last year and collected total fixed pay equivalent to nearly 50% of operating profit. Triad’s performance certainly improved last year. But the current share price leaves the stock on a P/E of 33. With no forecasts in the market and a minimal outlook disclosure today, I think it makes sense to remain neutral. | |

Skinbiotherapeutics (LON:SBTX) (£40m) | Agreement re: sale of food supplements, and £4.1m is raised at 17p to support it. For two years, Superdrug will have the exclusive right to sell STBX’s supplements (which alleviate the symptoms of inflammatory skin conditions), but STBX will retain the worldwide rights to sell them directly online, using their own website and Amazon. Major shareholders are providing £4.1m and retail shareholders will also have the chance to invest up to £600k. | AMBER (Graham) [no section below] We’ve not covered this one before and the long-term record shows that it’s effectively a start-up, with no meaningful revenues until last year. I’m fine with giving it the benefit of the doubt today and a neutral stance as it raises funds at the current share price, to support a deal with Superdrug. These shares are probably still very speculative, but the fundraise itself is an important vote of confidence, and a deal with Superdrug must add to the company’s credibility. | |

Artisanal Spirits (LON:ART) (£35m) | New franchise launched in Vietnam, another milestone in the Group’s strategic expansion in Asia. They already have a franchise in Korea and a subsidiary in Taiwan, alongside longer established China and Japan subsidiaries. | AMBER (Graham) [no section below] I last looked at this in December, noting that the company was unprofitable but claimed to have spirits on the balance sheet worth in reality over £100m (vs. their value of £26.5m on the balance sheet). FY24 results reiterated this claim. On balance I think a neutral stance continues to make sense. I might upgrade already if not for a net debt position of £27m. The company says that this has peaked and is underpinned by their whisky assets. Let’s see if they can now generate cash as they have claimed they will. | |

Ondo InsurTech (LON:ONDO) (£30m) | LeakBot device to be piloted to 5,000 homeowners’ insurance customers in Utah. | AMBER/RED (Graham) [no section below] While the company said (in April) that it had “no anticipated requirement for future funding”, I remain cautious given cash of probably less than £3m and losses pencilled in for the next two years. Today’s announcement provides further evidence that the company is gaining traction with its leak detection sensors in the United States - let’s see if it can make it to breakeven before additional equity is required. | |

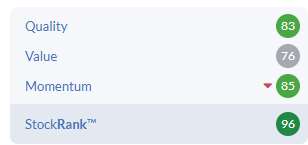

Mission (LON:TMG) (£26m) | In line. Restructuring complete. Client retention strong. Searching for a successor to interim CEO. | AMBER/GREEN (Graham) [no section below] I last covered this collection of creative agencies in March, when we learned that net bank debt had reduced to £9.4m, with the potential for it to reduce further given an earn-out payment scheduled for June 2025 (although there is no mention of that in today’s update). With the company continuing to trade in line, I’m going to tentatively upgrade this to AMBER/GREEN. It has a StockRank of 98, including a ValueRank of 93 (P/E ratio only 5x). Recoveries are always somewhat fragile, and this is no different, but I think it could be worth another look. | |

Clean Power Hydrogen (LON:CPH2) (£22m) | Memo with an Irish energy developer, will now negotiate sale of initial five MFE220 units. | RED (Graham) [no section below] We haven’t covered this one before. It listed in early 2022, at the tail end of the IPO boom, with a placing at 45p. The shares are down by nearly 90% since then, with no revenues reported yet, although forecasts suggest that revenues will be generated in 2026. According to the most recent going concern statement, the company is likely to need more funding within 12 months. | |

Safestay (LON:SSTY) (£15m) | Awarded a business interruption insurance claim for £1.4m, to be received in the next 21 days. | AMBER (Graham) [no section below] We’ve been a little worried about this hostel owner and operator. See Roland’s most recent coverage in February - it has not yet reached sufficient scale or efficiency to post a profit, and net debt was last reported at close to £18m. I’m likely to downgrade it if its fortunes don’t improve soon. For now, this business interruption claim should provide some very helpful additional headroom. The insurance sector hasn’t covered itself in glory by taking such a long time to make these payments! |

Graham's Section

Peel Hunt (LON:PEEL)

Down 1% to 86.4p (£106m) - Full-year Results - Graham - GREEN

Peel Hunt has published results for FY March 2025.

This stock featured on my 2025 watchlist.

Key points:

Revenue +6% to £91.3m, “despite ongoing low levels of equity capital markets (ECM) activity”.

Loss before tax £3.5m (FY25: loss £3.3m), due to restructuring costs. On an adjusted basis, there’s a small profit.

I believe these numbers are slightly better than market expectations, e.g. the revenue forecast on the StockReport is £89.1m.

Investment banking - revenue down slightly, 147 clients, vs. 150 a year ago. But there’s a good increase in the number of FTSE-350 clients, from 43 to 52. The average market cap of retained clients increases to £870m. Acted on two of the three major London IPOs.

Execution - revenue increases 14%, “due to our position as a highly valued liquidity provider to our clients, as well as increased trading volumes”.

Research & Distribution - revenue increases 10%.

The firm is preparing to open an office in Abu Dhabi.

Retailbook - the retail investment platform created by Peel Hunt (but now with a range of other investors involved), has “reached several key milestones in FY25”.

On political solutions to the decline of London listings:

The increasing rate at which companies are exiting the London market presents a significant challenge for the UK economy. Peel Hunt remains at the forefront of the reform agenda, championing solutions to revitalise UK equity markets. Numerous policy initiatives are already in progress, and we are leveraging our connectivity to drive further advancements

Outlook: FY March 2026 has “started more positively” with Trump trade deals and lower interest rates at the Bank of England.

We are seeing a rotation out of US assets into Europe and greater institutional positivity towards the UK. ECM activity in the UK remains generally subdued but could gain traction should macroeconomic conditions continue to stabilise. Meanwhile our M&A franchise remains highly active with a strong pipeline of transactions.

Balance sheet: net assets have reduced by a few million pounds to £89m, almost fully tangible and mostly consisting of liquid current assets. Cash at year end was £20m (previous year: £38m) and the company acknowledges that it has “occasionally” used its £20m RCF and £10m overdraft to support clients’ trades.

Graham’s view

I’m going to stay GREEN on this due to the combination of a) balance sheet strength, covering most of the market cap and hopefully reducing the risk associated with the share; and b) the prospects for some recovery in UK equity markets, which appear slightly stronger now than they’ve seemed for some time.

Peel Hunt has great strength in mid-caps too but even if we focus on small-caps (represented below by the AIM All-Share Index), there has been a noticeable bounce off the tariff-related lows. Even a very modest IPO flow could do a lot for performance here. Of course the index is still far below the post-Covid high, which fuelled an enormous IPO boom:

Mid-caps (represented by the FTSE-250 Index) have been doing fine in share price terms, but IPO activity here is much rarer:

One aspect of Peel Hunt’s performance that does frustrate me is that it doesn’t adjust its costs quickly enough to prevent annual losses. It would be a sign of great financial discipline if it could do that, and it has been close, but it just hasn’t been able to manage that in recent years.

In FY25 it reduced headcount by 5%, as it tried to reduce costs and get to breakeven.

But staff costs are still up by 3%, even on an “adjusted” basis which excludes share-based payments and staff restructuring costs.

On an unadjusted basis, total staff costs rose nearly 10%.

Perhaps it’s too much to expect a bank like this to achieve breakeven in an IPO drought, but I remember that Cenkos (now Cavendish (LON:CAV)) used to be able to do it.

In any case, I am still GREEN on this for now.

Roland's Section

Costain (LON:COST)

Up 8.5% to140p (£381m) - £10m Share Buyback & H1 Trading Update - Roland - GREEN

Construction and infrastructure group Costain has issued a half-year update confirming that trading remains in line with FY25 expectations. This follows an in-line update at May’s AGM.

Margin guidance is also unchanged from May, suggesting that Costain will hit its 4.5% adjusted operating margin run rate target “during FY25”. As Mark commented in May, this seems to suggest that the full-year margin will be lower than this, but that FY26 results could benefit from a full-year of improved profitability.

Commentary on the group’s order book certainly seems confident:

Forward work position “more than four times annual revenue”

FY25 wins to date include new contracts in nuclear energy (Sizewell C)

Further work with Anglian Water to deliver an extra 260km of strategic pipeline

“Busy bidding further new work across all sectors”

£10m share buyback / pension: Costain has also announced a new £10m share buyback alongside today’s update. It looks like this is largely going to be funded by cash saved by not having to fund contributions to its defined benefit pension scheme this year.

The group’s scheme is said to have been fully funded (>101%) at the end of March, which allows the annual £3.3m pension contribution to be suspended.

This also frees up additional cash due to the suspension of the dividend parity requirement attached to the pension contribution plan. This requires Costain to make matching pension contributions for all dividends paid in excess of the £3.3m standard contribution.

This year’s dividend is forecast to cost £7.2m, so this means an extra £3.9m is available.

My sums suggest a total of £7.2m is being saved by avoiding pension contributions this year. This has been rounded up to £10m to fund a buyback that’s scheduled to complete by 23 December 2025.

Costain’s balance sheet looks in decent health and the shares have an earnings yield in excess of 10% at current levels. Taking this into consideration, I think a buyback could provide attractive returns at current levels, assuming profitability remains stable.

Updated estimates: house broker Panmure Liberum has updated its earnings forecasts slightly today to reflect the expected impact of the buyback:

FY25E EPS +1% to 14.4p

FY26E EPS +2% to 15.9p

These figures put Costain on a FY25E P/E of 9.8, falling to 8.9 in FY26.

Year-end net cash is now expected to be £172.6m. Although this may be a peak figure, the company is likely to be generating a useful interest income from its cash, adding to profitability at a PBT level.

Roland’s view

Costain appears to have decent momentum and to be on track to achieve a decent level of profitability for a business in this sector.

While it’s worth remembering that such businesses need to maintain healthy cash positions (as I discussed recently here), I think that Costain’s buyback and dividend look both affordable and justified.

In addition, as Mark commented in May, applying a 4.5% operating margin to FY26 forecast revenue of £1,270m suggests an operating profit of £57m. My sums suggest this could be slightly ahead of current forecasts, which have already been upgraded several times over the last 18 months:

A positive outlook and reasonable valuation are reflected in a high StockRank:

I’m happy to stay GREEN on Costain today.

NextEnergy Solar Fund (LON:NESF)

Up 0.9% to 70.8p (£407m) - Full Year Results - Roland - AMBER

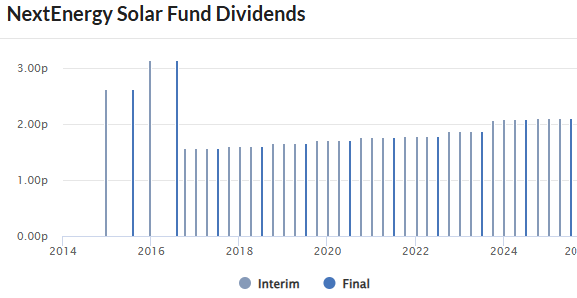

This solar energy and battery storage investment trust has now declared dividends of 76.3p since IPO in 2014 – equivalent to £395m or (almost) today’s entire market cap.

However, higher interest rates have left shares in this sector trading at hefty discounts to book value, leaving trusts unable to issue new equity to fund new projects. Instead, NESF (and others in this sector) have been forced to resort to selling assets and using the cash to repay short-term debt, shore up NAV and fund share buybacks.

This is not necessarily as desperate and/or cynical as it might seem at first glance. There is some sound financial logic behind this strategy, as highlighted in today’s results.

Capital recycling programme: NESF is currently midway through a Capital Recycling Programme targeting 245MW of sales.

According to today’s results, 145MW of disposals have been achieved so far, raising £72.5m and achieving a 2.76p increase in NAV per share.

The sale of the final 100MW of assets being targeted is currently said to be “in a competitive sales process”.

The key factor here is that selling these assets has created accounting value because they have generally been sold at a premium to book value. This has allowed NESF to repay some of its debt and also buy back shares at a discount to book value.

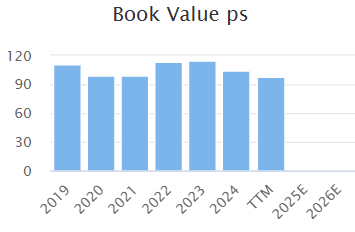

Selling assets at a premium to book value and then buying back shares at a discount should be accretive to NAVps, assuming book values for the remaining assets remain stable. The StockReport shows us that NESF’s book value has fluctuated within a range in recent years:

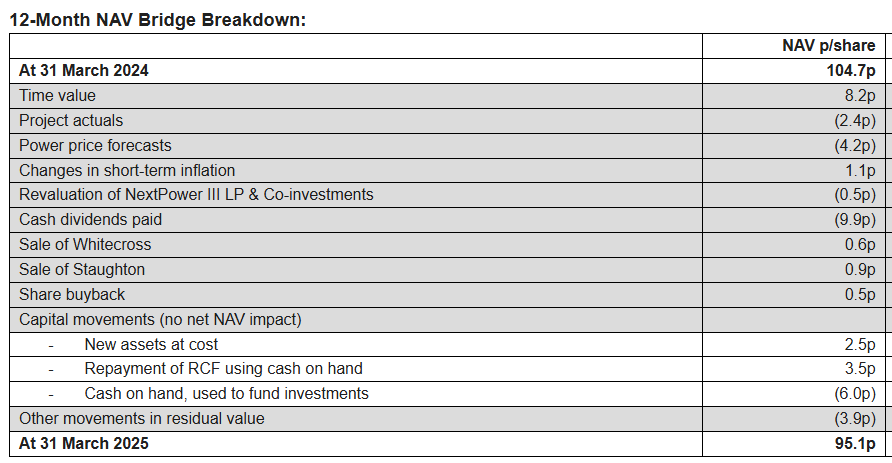

Unfortunately, NESF’s book value fell by 9% last year, despite the company’s efforts to support it. This fall highlights the cocktail of other variables the fund needs to manage successfully:

The biggest movement – time value – reflects the unwind of the discount on future cash flows due to the change in valuation date. In other words, future cash flows are one year nearer and so worth more than they were one year ago.

Project actuals reflect the impact of weather conditions and maintenance issues. Electricity generation was 5% below budget last year, due to some adverse conditions.

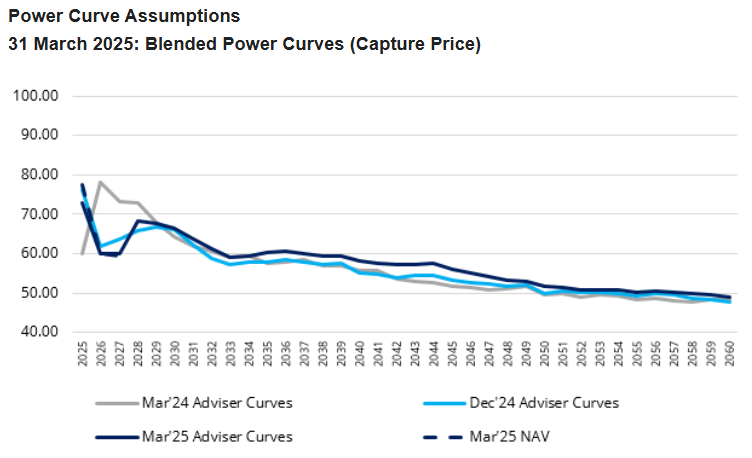

Power price forecasts are self explanatory and were a further negative factor, extended the trend seen in recent years:

Dividend: Renewable energy companies like NESF need to juggle interest rates, power price forecasts and fluctuating weather in order to sustain a reliable dividend.

Today’s results confirm a full-year payout of 8.43p per share, covered 1.1x by net cash available for distribution of £56.4m.

Management expects cash cover for the dividend to improve to 1.1x-1.3x this year, although the target payout has been left unchanged at 8.43p. This gives a prospective yield of 12% at current levels, one of the highest in the sector.

Gearing: renewable energy projects often have relatively low expected returns on capital, but returns can be improved by use of gearing.

NESF’s gearing appears to be at the higher end of what’s typical in this sector. Today’s results report total gearing of 48.4%, up from 46.4% one year ago. It seems that disposals have not been sufficient to reduce overall gearing against other negative impacts.

For contrast, peer Bluefield Solar Income Fund (LON:BSIF) reported a figure of 43% in its last accounts and larger wind-focused trusts Greencoat UK Wind (LON:UKW) and Renewables Infrastructure (LON:TRIG) (disc: I hold TRIG) were both under 40% at the end of 2024.

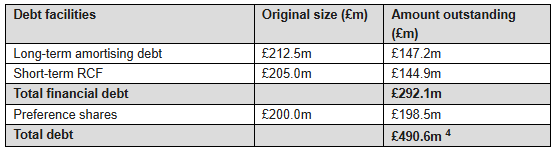

NESF debt falls into three categories, with an average cost of 4.9% (FY24: 4.5%):

The company says its long-term debt is at fixed rates and is on track to be fully repaid by subsidy-linked project cash flows over time.

However, the floating-rate RCF will need to be managed using surplus cash or disposals, as far as I can see.

The preference shares are a little unusual – checking the annual report, the company has 200m of these with a fixed coupon of 4.75% (£9.5m annually). These cannot be redeemed before 2030.

Overall, I don’t think NESF’s debt situation looks unsustainable. However, my initial impression is that the higher level of gearing (and potential inflexibility of the preference shares) could carry some extra risk.

Roland’s view

Last year’s results show how difficult it is to predict exact cash flows from renewable energy assets. Over time, the broad trend may be correct, but it’s subject to regular disruptions. This is likely to increase as the proportion of unsubsidised assets in the market grows over time.

One way that NESF and others are mitigating this risk is by entering into more long-term power purchase agreements (PPAs) with large private sector customers such as industrial groups and data centre operators.

At the end of March 2025, 16% of NESF’s were subject to a long-term PPA. Deals such as these could support attractive and predictable cash flows from what are long-life assets – the average remaining lifetime of NESF’s assets is almost 25 years.

As an income investment, NESF has a decent track record over the last decade. The payout has never been cut and and it expects dividend cover to improve slightly this year, implying a 12% yield.

My concern would be that buybacks and disposals – while mathematically correct – equate to a slow-motion liquidation. NESF is already one of the smaller companies in this market and would ideally get larger, in my view. Consolidation might be one option, as we’ve been seeing among some smaller REITs.

The combination of small size and above-average gearing means I think the risks here are slightly higher than elsewhere. But with NESF trading 25% below book value and offering a covered 12% dividend yield, I think it could still be worth closer consideration for interested investors.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.