Good morning!

The Agenda is complete.

Spreadsheet accompanying this report: link.

We're finished for today, cheers!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Babcock International (LON:BAB) (£5.22bn) | Op profit +51% (£364m). £200m buyback. FY26: to hit adj. op margin 8% target one year early. | ||

ITM Power (LON:ITM) (£478m) | Launch of a German subsidiary that will build, own and operate hydrogen production plants. | ||

| Warehouse Reit (LON:WHR) (£454m) (also Tritax Big Box REIT (LON:BBOX) (£3.74bn)) | Recommended Acquisition of Warehouse REIT | Price per WHR share: 0.4236 new BBOX shares and 47.2p cash. Total value: 111p plus dividends. | PINK |

THG (LON:THG) (£406.8m) | Q2 much improved, as anticipated. Return to constant currency growth. Unch. FY25 guidance. | ||

Halfords (LON:HFD) (£376m) | Adj. PBT +6.4% (£38.4m). Early FY26 trading in line. Remain cautious on consumer spending. | ||

Filtronic (LON:FTC) (£339m) | Rev, EBITDA marginally ahead. Rev +120% (£56m). Strong position to meet FY26 exps. Forecasts at Cavendish for the current year (FY May 2026) are unchanged and suggest a small reduction in revenues (from £55m to £54m) and a larger percentage drop in adj. PBT (from £14.1m to £8.3m). These FY26 forecasts are still far ahead of FY24 performance, even if they don’t match FY25. We do not yet have forecasts for the following year. | AMBER/GREEN (Graham) [no section below] | |

Liontrust Asset Management (LON:LIO) (£262m) | Adj. PBT £48.3m (LY: £67.4m). Capital Allocation Policy (only 50% of EPS to be paid as a minimum). | AMBER/GREEN (Graham) Keeping a moderately positive stance on this due to its sheer cheapness, but there are still serious problems. Other fund manager stocks remain significantly more appealing than this one. | |

Hargreaves Services (LON:HSP) (£224m) | Revenue and PBT to be ahead of exps. Services Division: future years to also beat current exps. | ||

Vertu Motors (LON:VTU) (£202m) | FY26 anticipated in line. New car retail LfL volumes +7%, gaining mkt share. Used volumes -3.8%. | ||

Anglo Asian Mining (LON:AAZ) (£188m) | Momentum has continued to increase significantly. Demirli mine to start production in H2. | ||

Renold (LON:RNO) (£182m) | Italian manufacturer and distributor of transmission chain and ancillary products. €10m price. | ||

Duke Capital (LON:DUKE) (£148m) | Recurring rev +6% (£25.8m). Q1 FY26: £6.6m of recurring revenue expected, +4% year-on-year. | ||

Avingtrans (LON:AVG) (£139m) | Adj. EBITDA and Adj. PBT in line with recently upgraded market expectations. Net debt excl. IFRS16 £12.3m | ||

Marks Electrical (LON:MRK) (£66.1m) | Rev +2.6% to £117.2m. Adj. EPS -37% to 1.54p. Net Cash £8.8m (FY24: £7.8m). As we look ahead to the remainder of FY26, we anticipate improving revenue growth and higher gross margin than prior year, enabling us to reiterate our full year guidance. | AMBER/RED (Mark) [no section below] | |

Ultimate Products (LON:ULTP) (£64m) | Profits Warning. Four months to May 2025 Rev +3%, Adj EBITDA flat, impacted by lower order intake. H2 revenue now expected to be broadly flat = FY25 4% lower than FY24. adjusted EBITDA for FY25 to be around £12.5m (vs current consensus of £14.3m). Expects 2026 revenue to be lower than FY26. | BLACK (AMBER/RED) (Mark) | |

PROCOOK (LON:PROC) (£43.6m) | Revenue +11% to £69.5m, LFL revenue +5%. U/L Op profit +51% to £3.2m. Net cash £1m. 26Q1 revenue +13.7% (+2% LFL). “Beginning to deliver improved performance and we have both the opportunity and a clear plan to accelerate this further.” | ||

Brave Bison (LON:BBSN) (£41m) (also Centaur Media (LON:CAU) (£50m)) | Mini-MBA acquired from Centaur Media for £19m EV. expected to increase Brave Bison pro-forma net revenue by 43% to £36.5 million and Adjusted EBITDA by 80% to £8.1 million. £13.5m placing (29.3% of enlarged share capital at 2.45p). | AMBER/GREEN (Mark - I hold Centaur) | |

Sanderson Design (LON:SDG) (£32.8m) | “…continues to trade in line with the Board's expectations for the full year.” Retail launch of the Highgrove by Sanderson very well received. Licensing continues to perform well - strong u/l revenue growth from previously signed agreements. New licensing agreements signed during the year-to-date. Manufacturing on track to achieve around break-even for the current FY, plus further cost-saving measures. Planned inventory reduction means net cash position is beginning to build. | AMBER/GREEN (Mark - I hold) | |

GSTechnologies (LON:GST) (£24m) | “The Treasury Policy allows for a significant proportion of the cash resources of the Company, as determined by the GST directors from time to time, to be held in Bitcoin.” | RED (Graham) [no section below] RED might be a harsh stance without having done in-depth research, but this one is categorised as a Sucker Stock and I think all companies joining the "bitcoin treasury policy" bandwagon should be treated with great caution. Bitcoin may be many things but GST justifies its new policy by saying that it is "a reliable store of value". | |

Various Eateries (LON:VARE) (£22.8m) | H1 Rev +9% to £24.7m, LFL sales flat, Adj. EBITDA £0.1m (24H1: -£1.3m), Net Cash £2.9m (24H1: £4.2m). Post-period LFL sales +7%. “The Group is trading in line with market expectations for the full year.” | ||

Tissue Regenix (LON:TRX) (£21.8m) | Rev +9%, Adj. EBOTDA $1.9m (FY23: $0.7m), Cash $1.9m (FY23: $4.7m). | ||

Velocity Composites (LON:VEL) (£16.2m) | Rev -3% to £10.4m, Adj. EBITDA £0.3m (FY24: -£0.2m), Net Cash £0.4m (FY24: £0.6m). “expects to achieve positive adjusted EBITDA and be cash generative in H2 FY25 - in line with current market expectations.” | ||

Pri0r1ty Intelligence (LON:PR1) (£12m) | “...applied to the OTC Markets Group for its Ordinary shares to be cross-traded publicly on the OTCQB Market in the United States.” | ||

Kelso group (LON:KLSO) (£10.7m) | Holds 5 investments. Since 23rd April 2025, The Works: +185.0%, Angling Direct: +34.3%, Selkirk: +19.7%, NCC +4.1%, THG flat. |

Graham's Section

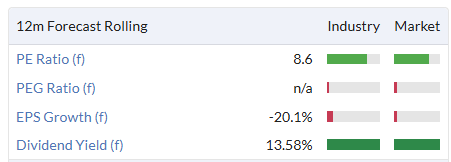

Liontrust Asset Management (LON:LIO)

Down 7% to 381p (£243m) - Annual Financial Report - Graham - AMBER/GREEN

Liontrust Asset Management Plc ("Liontrust", the "Company", or the "Group"), the independent fund management group, today announces its Full Year Report for the financial year ended 31 March 2025.

I last covered this fund manager in April, when we learned that the company had suffered net outflows of £1.3bn in Q4 of its financial year (to March).

We also learned that its AuMA had continued to fall since the end of March, down another 4% to £21.6bn. That was when tariff-related fears were at their worst.

As you’d expect, there has been a bounce since then, with AuMA back up to £22.7bn as of 17th June. So AuMA is back where it started this financial year.

These full-year results show adj. PBT of £48.3m and actual PBT of £22.3m.

Before going any further, let’s check if the adjustments are reasonable.

Last year, adjusted PBT was £67m, but there were £68m of adjustments. I was quite critical of these adjustments: here’s my analysis from last year.

This year, we have £26m of adjustments. At least it’s an improvement on last year!

The main item is £12m of spending on the “Business Transformation Programme”. There is also nearly £10m of intangible amortisation.

I’m happy for the amortisation to be adjusted out, which makes sense if we treat its intangibles as already being worthless. The latest balance sheet has net assets of £138m, or £66m if we exclude all intangibles. So roughly speaking, that’s the balance sheet support.

However, I’m not willing to look past the costs of the “Business Transformation Programme”. I’m consistent on this when I look at companies in general: I’m not willing to ignore the costs of changing how they do business, because companies are often changing how they do business, so it’s not a one-off cost.

The BTP cost £12m in FY25, and nearly £6m in FY24.

Here’s what the Chair said on the topic, so you can decide for yourself if you’d be willing to treat these costs as one-off:

The Group has also been engaged in a business transformation programme designed to overhaul Liontrust's operating model. This includes implementing BlackRock's Aladdin platform; a Middle-Office operating model with BNY; BNY Front Office Services; and a new enterprise data platform - BNY Data Vault. The Group also outsourced factsheet and regulatory reporting in 2024 and has been finalising the outsourcing of trading for investment funds and institutional accounts to BNY's Buyside Trading Solutions service. These changes are strengthening data management, delivery and analysis across the business while also providing operational and cost efficiencies.

Remember that actual PBT for the year was £22m. With the adjustments, PBT rises to £48m.

I’m willing to add back in the intangible amortisation. So for me, the “real” PBT figure is £32m. We could perhaps allow a portion of the BTP spending to be treated as one-off, depending on how much benefit of the doubt we are willing to give, which could bring adj. PBT closer to £40m.

Dividends

The company is paying out 72p for FY March 2025, which is significantly higher than adjusted EPS (56.8p) and far higher than actual EPS (26p).

As it’s not sustainable to pay out like this, the company announces a “Capital Allocation Policy”.

As part of the new CAP, our dividend policy has been updated to reflect a disciplined approach to capital management, targeting a sustainable dividend funded by current earnings. As such, Liontrust's dividend policy will be to pay a minimum of a 50% of Adjusted diluted EPS in ordinary dividends, to be paid to shareholders following the publication of the Company's Half Year and Annual results.

If this had applied to the current year, Liontrust would only have been obliged to pay out 28.4p.

There is also a pledge to buy back shares with excess capital “when it makes economic sense to do so”.

Outlook

The outlook statement doesn’t seem to acknowledge the problems facing the business. They just experienced nearly £5bn of outflows, or c. 18% of starting AUM, and this is what they say:

Liontrust continues to build on the strong foundations of the business by executing our four strategic objectives…

Our investment strategies have maintained their strong reputation and independent recognition, and we are broadening our offering, including in alternatives for which we believe there will be strong demand.

This impressive progress in the development of the business to achieve our four strategic objectives puts Liontrust in a very strong position to take advantage of the opportunities for active asset managers. Our brand, communications, distribution, operating model and strong capital position will enable Liontrust to deliver growth.

Would it not be more reassuring if they admitted how badly they were doing?

Graham’s view

I’ve been pretty clear for a while that I don’t rate Liontrust very highly against other fund managers. Their strategy, competitive positioning and even their commentary on their own performance - none of it fills me with confidence.

Despite this, I’ve stuck with my AMBER/GREEN stance for a while, due to the extraordinary cheapness of the stock against its historical norms.

Investors at the current share price get £93 of AuMA for every £1 invested in the stock.

Stockopedia categorises it as “Contrarian”, offering quality and value but without momentum.

Note, however, that the dividend yield shown below will not be paid on an ongoing basis. The real yield might be in the region of 5-7%.

I’m reluctantly going to stay AMBER/GREEN on this as despite the negatives, it does still offer some attractions. I admit that these attractions are based on the numbers, not on the quality of the business.

Balance sheet strength, for example, which is a legal requirement: Liontrust has £75m of working capital.

And even at the lower payout ratio, the dividend yield should still be useful, with the potential for cash to also be set aside for buybacks and other opportunities. The share count should start to go down rather than up.

I’m AMBER/GREEN because the numbers still seem to justify this, even if the quality of the business and its strategy don’t. Out of all the fund managers I’ve studied, this is the one that I think is most badly in need of a change in leadership.

Mark's Section

Ultimate Products (LON:ULTP)

Down 30% to 50p - Trading Update - Mark - BLACK/AMBER/RED

As is often the case, the word “now” reveals that this is bad news:

As a result, H2 revenues are now expected to be broadly flat vs H2 FY24, with FY25 revenue expected to be approximately 4% lower than last year.

Which they helpfully quantify at the EBITDA level:

Accordingly, the Board expects adjusted EBITDA for FY25 to be around £12.5m (versus current consensus of £14.3m).

The reasons given are:

A weighting towards lower margin product categories and sales channels

Lower order intake, with orders deferred from Q4 FY25 to Q1 FY26.

The shares had been recovering recently, presumably on the expectation that the company would benefit from lower freight rates:

This is confirmed in today’s update, but is not enough to overcome the weakness in sales and mix.

Forecast Changes:

The real kicker is that this is a multiyear warning as they also say:

Looking ahead to FY26, the current order book indicates a slow start to the year (currently down 7.5% vs this time last year). Given the current trading environment, the Board therefore believes it is prudent to expect FY26 revenue to be lower than FY25, at a level broadly in line with the current order book position.

Previously they had been expecting a boost to sales and a recovery in EPS, as the table they provide of the consensus prior to today’s update shows:

Strangely for a company of this size which has issued very few shares over the years, they have four brokers covering them. So, I can build a new consensus quite easily:

I’ve highlighted the FY26 change here, as the RNS doesn’t give specific figures. Despite them saying orders have been delayed into FY26, revenue is now forecast to be 16% lower, and EPS drops by a whopping 55% versus previous expectations. The FY27 consensus is only Cavendish, who were the only one of the four to look that far ahead. Even here, the recovery is modest by historical standards and still significantly below 2024 actuals.

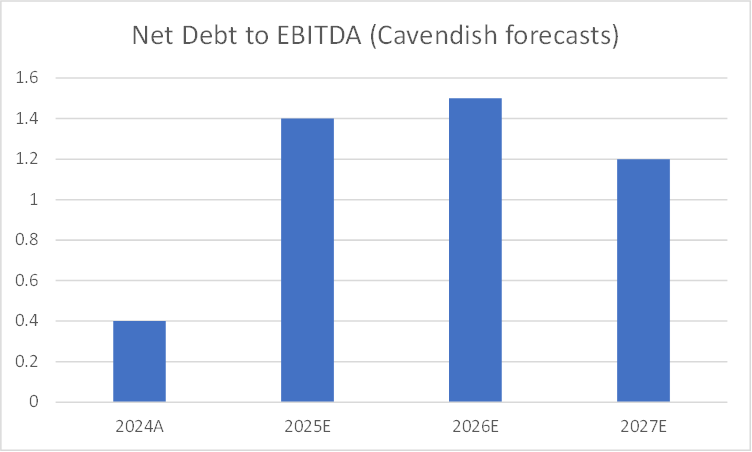

Net Debt, Dividends & Buybacks:

The bad news keeps coming. While the brokers vary slightly in their modelling of net debt, the consensus is mostly for net debt to be a little worse in FY25 and a little better than previously forecast in FY26 due to lower working capital on lower trading. However, the lower forecast EBITDA means that net debt to EBITDA soars. I’ve taken Cavendish’s figures here as they’ve done the calculation for me!

While this isn’t such a high figure that would imperil the company’s existence, the current capital allocation policy is to target net debt to EBITDA of 1.0 and only buy back shares below this figure. This means that, under the current policy, we can expect no share buybacks for the next few years. Indeed, this drop shows the folly of this type of policy - they were recently buying back shares in the high-70 pence range, and will not buy back shares no matter how low they go over the next few years.

The dividend payout is also a victim of the current weak trading and higher net debt ratio. Canaccord, for example, cut FY25 estimates from 4.7p to 3.8p and FY26 from 6.2p to just 2.6p. What was a potentially very good income stock for investors, has a more modest (in current UK markets) yield of 5% at current prices.

Strategy:

Finally, one has to question the strategy here. There has been a shift in management roles, with Andy Gossage taking the CEO role. His skillset is much more aligned to scaling a branded business. Indeed, they say in the RNS:

In recent years the Group has delivered substantial improvements to its branding, product development and operational performance, including the deployment of robotic automation, AI and process change. The Group's focus now is on replicating those improvements within the sales function, with a number of initiatives underway which the Board is confident have the potential to deliver a significant improvement in the Group's financial performance.

However, so far this strategy has failed to generate the sales growth necessary to offset the increased costs of implementation. The jury is out as to whether this is a strategic misstep or whether it is just taking longer to bear fruit.

Valuation:

At around 50p, this is on 9.3x 2026 earnings. This isn’t crazy, but not particularly cheap for a forward multiple in the current markets. This looks worse on an EV value and rises to around 12x. If we take Cavendish’s stab in the dark for FY27, then things look better at around 7x earnings or 10x debt-adjusting. Buying on this basis is largely a statement of faith. On an asset basis, the company still trades on around 2x Tangible Book Value. While this metric doesn’t mean it is necessarily overvalued, it will not provide any support if trading should deteriorate further. The 5% forecast yield is reasonable, but as already described, there will be no buybacks with current debt levels.

Mark’s View

There is no getting around that this is a stinker of a warning. The downgrades to FY26 are severe, and impact the company on a number of levels. There are a lot of fans of this company for its straight-talking management and willingness to engage with investors. While it may be that a strong recovery is on the cards in better consumer conditions, this is a fair way in the future. I’m not convinced that basing an investment case on a strong recovery far out in the future is a great one. Especially as we have now had three profits warnings and there are questions over the recent strategic shifts within the business. Roland rated this AMBER/GREEN for the recovery potential after the last warning. However, with that recovery seemingly now very far in the future, I think this may be now and AMBER/RED.

Brave Bison (LON:BBSN) / Centaur Media (LON:CAU)

Acquisition of MiniMBA - Mark (I hold Centaur) - AMBER/GREEN

This deal was well known with Sky News breaking this as a rumour in early May, which was subsequently confirmed by RNS from both companies. Last week the exclusivity was extended by 7 days, which suggested it was a done deal, as it has proven today. The details are as expected with £19m paid on an EV-basis.

Long-term this looks to be one of those rare sales where both parties are getting a good deal. Centaur get cash, which simplifies their business and enables them to maximise value from the rest and return cash, as major shareholder Harwood is no doubt pushing for. Brave Bison gets a business they can grow and has cross-selling synergies with the rest of their business. They presented at the Mello investment conference recently and the story of development they had and cross-selling opportunities was quite impressive. This must have captured other investors too as the price has been strong recently:

What put me off investing was the uncertainty over the financing of the deal. It seemed to me that there would have to be an equity component, and this has been borne out with today:

Brave Bison will partly finance the cash consideration for the Acquisition through a placing and direct subscription of 27,615,467 new Ordinary Shares at a price of 49 pence per Ordinary Share (on a post-Share Consolidation basis) (the "Issue Price") to raise gross proceeds of approximately £13.5 million (the "Fundraising")

· Issue price (prior to the Share Consolidation) of 2.45 pence represents a discount of 4% to the mid-market closing price of 2.55 pence on 8 May 2025, being the last trading day before the potential Acquisition was announced.

The scale of the raise exceeds what I was expecting and the price is marginally worse. I’m surprised that the shares haven’t reacted more negatively to this today. After all, any institutions or HNWs that wanted increased exposure here could have bought at 2.45p in the placing, so why buy today at 3p?

One of the most impressive parts of this deal is that Mini-MBA founder Mark Ritson has put £4m of his own money into Brave Bison equity (or at least he will have over the next two years). As far as I am aware, he had no equity in the previous owner Centaur Media.

In terms of the impact on financials, this is what Brave Bison say:

The Acquisition of MiniMBA is expected to increase Brave Bison pro-forma net revenue by 43% to £36.5 million and Adjusted EBITDA by 80% to £8.1 million. Post-completion, 47% of operating profits (before central costs) will be derived from repeatable, non-cyclical, high-margin income from the monetisation of digital content, with the balance generated from marketing & technology services.

However, the dilutive impact of the raise makes the EPS changes much less impressive. Cavendish are forecasting EPS (prior to the upcoming share consolidation) to rise to 0.31p in FY25. This is up from 0.28p last year making around 10% EPS growth. This makes the P/E of around 9 still look good value. However, it is worth noting that when I last reviewed this on the DSMR the P/E was 8x and the company was forecast to have more net cash. So the rating here has increased. This is probably justified by the improving outlook from this and recent deals.

In the event that the mid-market closing price per Ordinary Share exceeds 3.0 pence on the date(s) of redemption(s), the B Shares will be capable of redemption by the LTIP Executives at any time with an aggregate value (the Redemption Value") equal to 15% of value created for the Company’s shareholders from the adoption of the LTIP to redemption(s) of the B Shares...

The total awards are limited to 12.5% of the Company’s issued ordinary share capital, but this could still be significant dilution. When the shares were trading at 2p, this wasn’t really an issue. However, with the shares starting to trade around the point where the LTIP kicks in, this should start to be considered in any valuation.

Centaur

On the other side of the deal:

Following Completion, it is the Board's intention to use the net proceeds from the Transaction to return capital to shareholders and will consult with shareholders before deciding how the proceeds will be returned. The quantum, timing and form of any such return of capital shall be at the discretion of the Board…Further details of the Capital Return (including the quantum, timing and form) will be announced in due course.

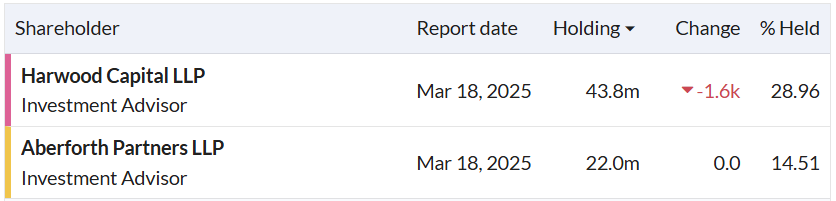

Apart from the use of the unnecessarily pretentious “quantum” instead of “size”, this is as expected. No doubt the return will be made in the form that major shareholders, Harwood and Aberforth, prefer:

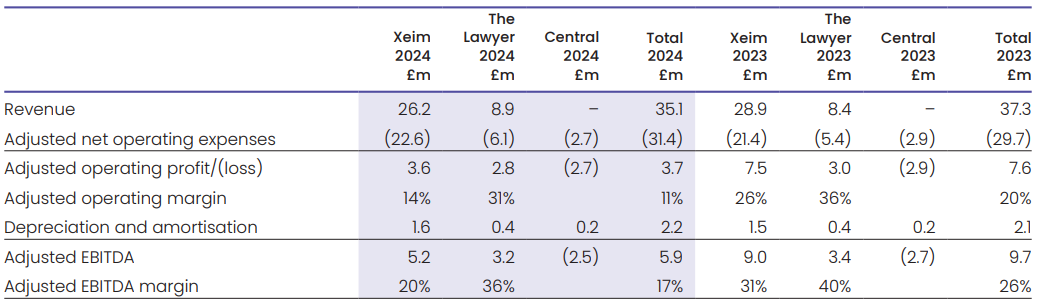

It was actually Christopher Mills’ enthusiasm for Centaur at Mello that persuaded me to take a small position here. Following completion, Centaur will have £27m cash, for a £23m EV at 34p. The Lawyer is clearly the high value asset here:

Given its moat and cash generation, they must hope to get around 10xEBITDA or more for this. The read through is that the rest of “Xiem” excluding mini-MBA must generate around £0.8m EBITDA, but will probably not fetch a high multiple. Still, that suggests upside from here. The big problem is the central costs. How quickly the company can get a good price for the remaining assets and how easily they can slash those costs are central to the investment case here. I’m sure Harwood will be pushing hard on both fronts, though.

Mark’s View

Brave Bison: Although the rating has gone up a bit since I last reviewed it on the DSMR, so has the potential upside from recent deals. I am a little cautious that the execution risk has also increased and that we are nearing the share price level where options dilution may kick in. Plus the shares may come under pressure in the short-term due to the placing price now being someway below yesterday’s close. However, on a long-term view I like the potential, especially the shift to more recurring revenue in a highly competitive industry. So am happy to keep the AMBER/GREEN rating.

Centaur: As a trading company, without mini-MBA and based on last year’s EPS downgrades, this would be an AMBER at best. However, with the end in sight for value realisation, I think it deserves a slightly more positive view. Until The Lawyer is sold, we won’t know if it truly is a valuable, high-multiple business. Plus the central costs will be an increasing weight until all sales (or closures) are concluded. However, with Christopher Mills pushing on both fronts behind the scenes, I think the chances of a positive outcome form the current price are high. So I’ll go for AMBER/GREEN as a special situation.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.