Good morning!

As it's the Fourth of July, US stock markets are closed today.

Spreadsheet accompanying this report: link.

As there is nothing else of interest today, I'll wrap up the report there. See you later when I publish The Week Ahead!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Future (LON:FUTR) (£741m) | £300m 5-year unsecured bond, 6.75% coupon. BB+/Ba2 ratings (junk). Also refinances its £300m RCF. | AMBER/GREEN (Graham) I like to see a business graduating from RCFs and other banking facilities to the bond markets, where debt is typically longer-term and less restrictive in terms of covenants. So this is good news. And I don’t think it will make any difference to the total debt being used by the company: as of the interim results it already had total facilities of £650m, of which it was only using £300m. Their leverage multiple was 1.1x which would not ordinarily be considered very dangerous. However, trading is under some pressure with organic revenues currently declining. See Megan’s coverage of the May profit warning here. On balance, this still looks quite interesting to me at the current valuation, albeit not without risk. The company's credit ratings are sub-investment grade. | |

MJ GLEESON (LON:GLE) (£227m) | FY25 PBT within market exps (£21-22.5m). FY26 to be at lower end of current exps (c. £24.5m). | BLACK (AMBER/RED) (Graham) Offers deep value vs. balance sheet strength but with earnings expectations in a downtrend, I have to stay AMBER/RED for now. Changes to the management structures appear to make sense, shortening reporting lines and giving the regional CEOs more control. | |

Avation (LON:AVAP) (£104m) | 10 aircraft to be delivered by Q2 2028. Actively considering ways to refinance $310m Notes due 2026. | AMBER/GREEN (Graham) [no section below] I’m happy to leave the AMBER/GREEN here but I note the company has $310m of Notes expiring in 15 months, along with a B2 issuer rating from Moody’s, i.e. in a bond context, Avation is considered “speculative and a high credit risk”. They’ll need to address this refinancing in a timely manner or it could have negative consequences for shareholders, e.g. being forced to accept a takeover bid at an inferior price. | |

Roadside Real Estate (LON:ROAD) (£71m) | Acquires former Sainsbury’s Petrol Filling Station from joint venture, for £1.25m. | ||

Huddled (LON:HUD) (£11m) | Deal with Ingenuity removes capacity constraints. Accepts £1.5m of new equity at 3.2p. |

Graham's Section

MJ GLEESON (LON:GLE)

Down 5% to 370p (£216m) - Trading Statement - Graham - AMBER/RED

Unfortunately this update includes a small downgrade to expectations for FY26.

It comes after a more serious profit warning in June, when Roland wisely downgraded our stance on it to AMBER/RED.

FY June 25: adjusted PBT will be in line with market expectations (£21 - 22.5m).

Gleeson Homes: 1,793 home sales completed (FY24: 1,772 homes).

It sounds reasonably busy, although I do note the drop in build sites (more on this later).

Net reservation rates have “improved significantly” to 0.64 per site per week (H2 last year: 0.50), excluding multi-units.

Forward order book of 845 plots (June 2024: 559 plots).

68 build sites (June 2024: 79 sites)

However, as flagged by Roland last month, the sale of some “extensive land holdings” in East Yorkshire didn’t happen. Gleeson are reviewing their options in relation to this.

Reorganisation: this division is losing its CEO and being reorganised under a “Central division” and “Northern division”. The leaders of these divisions will now report to the CEO of MJ Gleeson, not to a CEO of Gleeson Homes.

The outgoing CEO of the division is not thanked for his efforts after six years with the company:

The strengthened management structure is expected to lead to a marked improvement in performance and delivery, improving pace and quality of build and management and control of costs.

Later, the CEO of the group says “commercial delivery was not where we needed it to be”.

Gleeson Land: 7 disposals happened in FY25. 3 further disposals which had been anticipated, are now expected in H1 FY26. The FY25 operating profit result will therefore be at the lower end of expectations (£7 - 8.4m).

Net debt was £0.8m at year end (previous year: net cash £12.9m), “due to timing issues”. At least we can assume this means there wasn’t any window-dressing!

Outlook:

The housing market lacks confidence and remains subdued and the Board does not see a short-term catalyst for any substantial improvement.

However, as reflected in our robust sales rate, there are customers for well-located homes at the right price….

Continuing capacity issues in the planning system have delayed site openings and Gleeson Homes will operate from fewer sites than anticipated in the current year. However, our strong pipeline and improvements in our own process give us confidence in our ambitious growth plans.

Gleeson Land's performance in FY2026 is expected to be similar to FY2025 with delivery weighted to the latter part of the year...

Taking these factors into account, the Board expects that profit before tax and exceptional items for FY2026 will be at or around £24.5m, the lower end of current market expectations.

Graham’s view

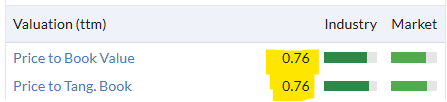

I got this wrong back in February, taking a positive stance (at 498p/£291m), noting that the company had (fully tangible) balance sheet net assets of £297m.

After the recent profit warnings, it is now trading at a discount to this net asset figure:

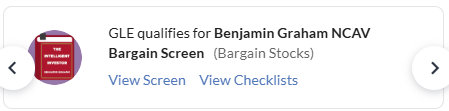

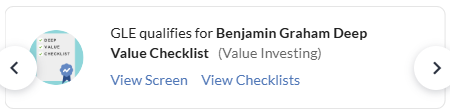

Which means that it’s showing up on Ben Graham deep value checklists:

The problem, of course, is that the market also cares about earnings.

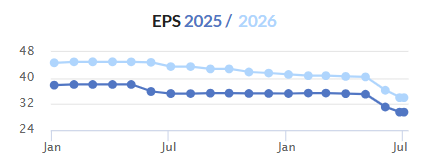

Back in June, Singer cut their FY26 adjusted PBT forecast by 20%, to £26.3m.

The latest estimate from Gleeson itself is that the actual figure might be c. £24.5m, i.e. 7% lower than Singer’s June estimate.

So I can’t argue with the share price fall today.

And I am going to have to stay negative on the stock, as we find that in the short-term, profit warnings tend to be followed by more profit warnings - and this is now the second warning in a row from Gleeson.

Looking out long-term - say three years from now - I’m more optimistic. In my experience, housebuilders trading at a discount to tangible book have limited downside risk (assuming that they are solvent, of course!).

I also think the decisive actions today re: management are promising. The CEO of MJ Gleeson will now have to be more hands-on at Gleeson Homes, as Gleeson Homes will no longer have its own CEO. And the two regional CEOs will have more control over their own regions. Surely these must be positive developments?

So I think over a 3-5 year timeframe, for people who want to own a housebuilder stock, Gleeson holds promise. But in the short-term, I do have to stay AMBER/RED on it, due to the risk of another profit warning.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.