Good morning! The Agenda is complete.

Spreadsheet accompanying this report: link.

Wrapping it up there, cheers!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

WPP (LON:WPP) (£5.7bn) | PW: performance worsened in Q2. H1 LFL rev now exp -4.2% to -4.5% & H1 op profit £400-425m. | AMBER/RED (BLACK) (Roland) [no section below] | |

Londonmetric Property (LON:LMP) (£4.6bn) | £7.3bn portfolio after recent acquisitions, with rent of c.£410m. Avg 16% uplift on rent reviews. | ||

Jet2 (LON:JET2) (£3.8bn) | Rev +15%, PBT +12% to £593m. Passenger numbers +12%. FY26 trading in line with market expectations. Canaccord FY26E EPS: 223.7p (+5% vs FY25). | GREEN (Roland) Growth looks likely to slow somewhat this year, but Jet2 continues to generate respectable double-digit returns on capital and has one of the strongest balance sheets in the business. With the stock trading on a P/E of eight, I’m happy to take a chance on the slightly weaker outlook and maintain my positive view. | |

British Land (LON:BLND) (£3.5bn) | Norton Folgate 64% let. Storey at Bishopsgate now fully let, Storey at Broadgate 67% let in 6 weeks. | ||

| Cairn Homes (LON:CRN) (£1.13bn) | H1 2025 Trading Update | Confident in full year guidance: revenue growth >10%, operating profit c. €160m, ROE c. 15.5%. | |

Smarter Web (OFEX:SWC) (£856m) | Raised further £10.3m through share sale. Founder Webley now controls 10.7%. See Mon 5/7. | ||

ZIGUP (LON:ZIG) (£827m) | Rev -1.1%, adj PBT -7.6% to £167m. Fleet assets up 16.2% to £1.5bn. Outlook positive. | AMBER (Roland) | |

Close Brothers (LON:CBG) (£618m) | Focusing on commercial customers, stepping back from retail. £20m cost saving by 2030. | ||

Young & Co's Brewery (LON:YNGA) (£593m) | YTD rev +6.6% in total, +7% LFL. “Strong momentum […] confident about the year ahead”. | ||

Hunting (LON:HTG) (£496m) | SP +10% | GREEN (Roland) [no section below] | |

Everplay (LON:EVPL) (£457m) | Strong trading,. FY results to be slightly ahead of exps. Acquired all rights for “Hammerwatch”. | ||

Galliford Try Holdings (LON:GFRD) (£429m) | FY results to be slightly ahead of exps, with adj PBT >£41.6m. FY26: 90% of revenue secured. | ||

GYM (LON:GYM) (£283m) | H1 LfL rev +3%. Total rev +8%. Net debt £51m. Confident in FY outlook. Opening 14-16 new gyms. | ||

| Impax Asset Management (LON:IPX) (£257m) | Q3 AUM Update | AUM +3.1% to £26.1bn. Net flows -£1.3bn offset by £1.1bn takeover and market movements. | AMBER/GREEN (Graham holds) Leaving our AMBER/GREEN stance unchanged to reflect that the bull thesis is a bet against the continuation of current trends. If AUM can stabilise and return to growth, I do think that the potential returns from the current market cap are very interesting. |

SRT Marine Systems (LON:SRT) (£189m) | Rev +423% (£77.5m), adj. PBT £4.4m. Cavendish forecasts: FY26 rev £115.8m, adj. PBT £10.2m. | ||

Renold (LON:RNO) (£181m) | Rev +3.9%, adj. op profit +11%. Demand is slightly below FY25, expect it subdued in H1 (PW?). | PINK (recommended offer at 82p) | |

System1 (LON:SYS1) (£55m) | TU: Q1 revenue -7%. Tariff impact on European clients and currency headwind from the weak dollar. Outlook: revenue +15%, profits in line. Canaccord reduce their FY March 2026 revenue forecast from £45.1m to £42.9m, and their adj. PBT forecast from £5.9m to £5.7m. For FY27, adj. PBT is seen growing to £7.9m. Net cash £11.7m. Founder and President John Kearon, also the largest shareholder, steps back to become a NED. | AMBER/GREEN (Graham) [no section below] We discussed US growth concerns at the time of the full-year trading update in April. Today’s trading update does indeed see a soft revenue performance, including a 3% reduction in core “Platform” revenue. Forecasts are also a little weaker despite the company saying that profits for the year will be in line. Strategically the company continues to carry out its plan of winning large new corporate clients (80 new client wins in Q1) and building its US business (US Platform quarterly revenue +16%), and so non-US, particularly European revenue must have shrunk given the overall quarterly result. I’ll leave our moderately positive stance unchanged: while I do think this is primed to do very well for shareholders from the current valuation, especially considering the strong cash position that covers 20% of the market cap, I am mindful that their growth journey is currently facing up against some headwinds. The small downgrades to forecasts today also suggest that some caution is justified. But overall I do still very much like the story here. | |

TAO Alpha (LON:SATS) (£48m) | Hires influential bitcoin expert (with a large YouTube channel) to be their Chief Bitcoin Strategist. | RED (Graham) [no section below] Their new bitcoin strategist has a really polished-looking YouTube channel so well done to him for that. However when I check the company's Feb 2025 balance sheet, I see that there was almost nothing of value on it. There were also no revenues on the income statement. Three weeks ago the company raised £5m and adopted a Bitcoin Treasury strategy - it can own bitcoin and other "stablecoins", i.e. "mature coins which the directors believe provides liquidity within the parameters of cash equivalency". Incidentally, the recent £5m raise had an unusual structure: it was an "investment" with "no interest or fees", a maturity date of November 2025, and a conversion price of 0.2p. In other words, a convertible loan note. The company has also announced the launch of a "second secured convertible loan note" for £100m, to be offered to accredited investors in the US. These notes have a conversion price of 1p. If shareholders are planning to vote for conversion (and I'm not sure if there will be a viable alternative), then why on earth are the shares changing hands at 10p? This makes zero sense to me. | |

Finseta (LON:FIN) (£18m) | SP -25% "On track to deliver expectations." H1 revenue +16% (£5.9m). Adj. EBITDA £0.3m due to investment. Expecting significant H2 revenue growth consistent with previous years, at an improved gross margin compared to H1. | AMBER/RED Graham [no section below] It's a remarkable share price fall, considering the headline to this trading update is "on track to deliver full year results in line with Board expectations, including significant revenue growth". I can find two reasons for the fall. Firstly, there is a very, very large H2 weighting. Full-year revenues are supposed to be c. £15m,, and full-year adj. EBITDA is supposed to be £1.7m. The company in H1 has therefore only achieved 39% of full-year revenue, and 18% of full-year adj. EBITDA. The company says that there has been encouraging new customer onboarding in H1 but it needs a very large jump in H2 to bridge the gap to full-year expectations. The second reason for selling activity today could be the news that a major shareholder reduced their interest last week from nearly 10% to only 8.2%. While today's announcement is not strictly speaking a profit warning, I'm going to interpret as one, and therefore take a moderately negative stance, as I perceive a high risk that the company fails to meet full-year forecasts. Hopefully it can prove me wrong! | |

Shearwater (LON:SWG) (£11m) | FY25 revenue, adj. EBITDA slightly ahead of expectations. Confidence in growth in FY26. | ||

Croma Security Solutions (LON:CSSG) (£11m) | Meets expectations for FY25. Revenue +10% (£9.6m). Market conditions remain challenging. |

Graham's Section

Impax Asset Management (LON:IPX)

Unch. at 194.8p (£257m) - Graham - AMBER/GREEN

At the time of writing, Graham has a long position in IPX.

After sensing a great deal of cheapness here for a long time, I eventually took the plunge and bought a few shares in this one last Christmas, at 247p.

When the ESG agenda was more confident, and when inflows were easy, this stock traded as high as £14 per share.

There was a profit warning in April, and I consider myself lucky to be only down by about 20%. Earnings forecasts did get revised higher again in May. The company has also started buying back its own shares.

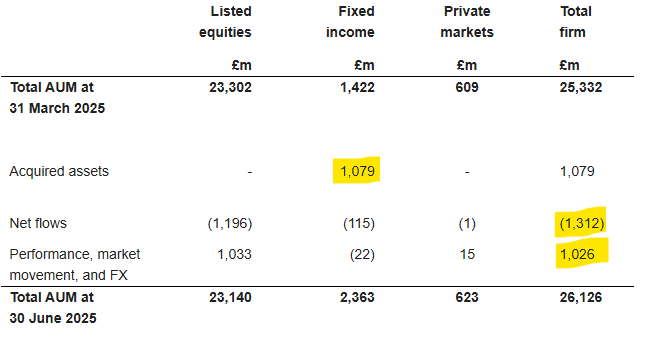

Today’s Q3 update shows continued outflows during Q3 (to June), of £1.3bn.

Thankfully this is offset by positive asset value growth of £1.0bn, despite the tariff issue that kicked off at the beginning of the quarter.

Impax has also completed an acquisition that brings in £1.1bn of fixed income assets.

In table format:

In total, AUM grows from £25.3bn to £26.1bn.

CEO comment excerpt:

The majority of our AUM follows investment strategies that have outperformed their generic benchmarks this calendar year, and in our larger listed equities business, there was a significant reduction in net outflows compared to the previous two quarters, with positive flows in June, reflecting strong institutional client commitments and fresh momentum in our wholesale channels in Europe."

That there were enormous net outflows of over £10bn in H1, which included the loss of huge mandates from St. James’s Place.

Estimates: many thanks to Andy and Paul at Equity Development for alerting me to their latest note on IPX. Paul has left the estimates unchanged, including AUM at the end of FY25 of £25bn. This might be considered conservative seeing as AUM is currently above that level, but I think it’s reasonable to allow for further net outflows and/or market weakness. Their EPS estimates for the current year is 19.5p, putting the shares on a PER of 10x.

(For context, EPS last year was 28p, and 30p the year before that.)

Graham’s view

I still think this is a really interesting recovery stock - not that it’s necessarily in recovery yet! But it’s trading at a low PER and a very cheap multiple of AUM (over £100 of AUM for every £1 invested in the stock at current levels). This multiple is as cheap as the fund managers which I consider to be undifferentiated and less interesting than Impax.

There’s no guarantee that it will happen, but if we see AUM stabilise and then any sort of return to growth, I think the shares are priced for a fabulous recovery. By this I mean that the shares should trade at a higher multiple, e.g. 15x (with higher earnings than currently) or at a much more attractive multiple of AUM, e.g. £50 of AUM per £1 invested in the stock (with higher AUM than currently).

If that doesn’t happen, then I would at least hope for a merger/takeover at a reasonable price. But of course I can’t guarantee that this will happen either.

I do feel confident in saying that fund managers' valuations are at extremely depressed levels. And I’m personally willing to bet that at least a couple of them will recover.

I’m leaving our stance on this unchanged at AMBER/GREEN to reflect the fact that the bull thesis is a bet against the continuation of current trends.

Roland's Section

Jet2 (LON:JET2)

Down 6% to 1,709p (£3.6bn) - FInal Results - Roland - GREEN

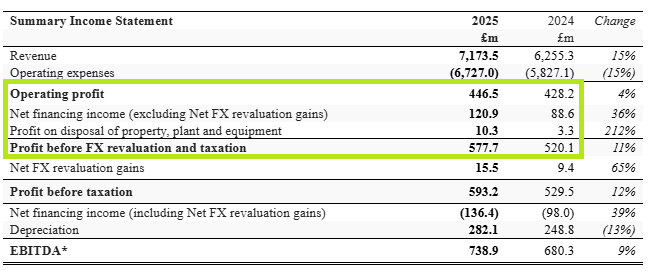

Jet2 plc, the Leisure Travel group (the "Group" or the "Company"), announces its preliminary results for the year ended 31 March 2025.

We’ve generally been positive on this well-run short-haul airline and package holiday operator. Today’s results seem unlikely to alter that trend.

The key numbers from today’s results are all moving in the right direction:

Revenue up 15% to £7,173.5m

Pre-tax profit up 12% to £593.2m

Earnings per share up 15% to 213.1p

Total dividend up 12% to 16.5p per share

£250m buyback announced in April is over 35% complete

This growth reflects underlying expansion of the business over the last year. The total number of passengers flown rose by 12% to 19.7m while higher-margin package holiday customers rose by 8% to 6.58m.

Jet2’s focus on holidays means it receives a lot of cash upfront in the form of customer deposits. In addition to this, the company has always prudently maintained a strong balance sheet. Today’s results show a reported net cash position of £2.0bn, including £3.2bn of total cash and £1.1bn of own cash (excluding customer deposits).

As these numbers imply, the group does have some debt. But the cost of this borrowing is hugely outweighed by interest income, boosting the group’s profits considerably:

Net finance income increased Jet2’s operating profit by 27% last year – a remarkable result that’s generating meaningful returns for shareholders, helping to support dividends and buybacks.

(As a side note, Jet2 was one of the stocks I discussed in a recent screening piece on cash-rich companies.)

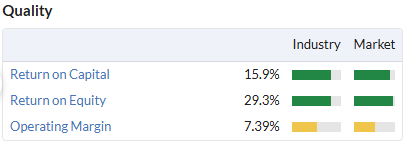

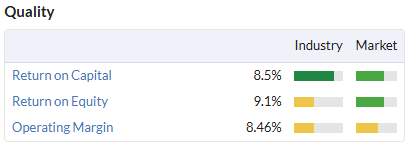

Profitability: Jet2 boasts very respectable quality metrics, according to the StockReport:

Checking today’s results tells me that last year’s performance was slightly weaker on margins, with an operating margin of 6.2%.

Lower margins are said to reflect inflationary cost pressures and a later booking profile, presumably implying some price reductions on late bookings to ensure capacity is filled.

However, the group’s return on capital employed was unchanged at 15.9%, suggesting that on a longer view the company is continuing to deploy capital successfully.

Spending over the last year included new bases at Bournemouth and London Luton, bringing 85% of the UK population within a 90 minute drive of one of the company’s 13 UK bases. Seven new Airbus A321neo aircraft were also added to Jet2’s fleet last year.

Outlook: travel is a cyclical business. While Jet2’s focus on relatively affordable short haul leisure travel probably dampens some elements of cyclicality, it doesn’t remove it.

The share price has dipped today and my guess is that a slightly more cautious tone on outlook is probably responsible.

While the company states that it is currently trading in line with market expectations, the tone of CEO Steve Heapy’s comments suggests to me a level of underlying uncertainty. Here are a couple of examples:

Bookings for Summer 2025 continue to be made closer to departure, as previously announced, but it is clear that customers' eagerness to get away from it all and enjoy a relaxing overseas holiday in the sun remains strong, provided pricing is attractive...

We are satisfied with our progress for FY26 to date, although we remain mindful of the late booking profile which limits forward visibility and the evolving geo-political and economic landscapes.

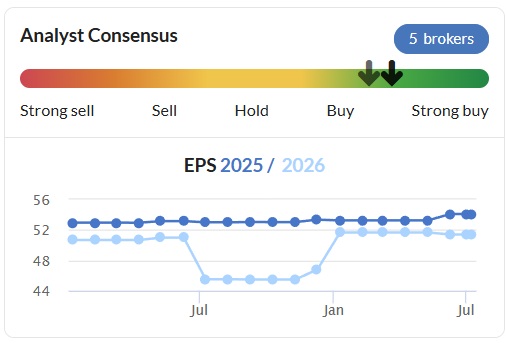

Estimates: with thanks to broker Canaccord Genuity, we can see that forecasts are largely unchanged today, except for some very slight adjustments:

FY25A EPS: 213.1p

FY26E EPS: 223.7p (previously 223.9p); +5% versus FY25

FY27E EPS: 229.5p (previously 234.0p); +2.5% versus FY26

The gist of CG’s view seems to be that operating margins will remain under pressure, but that finance income will continue to reduce the impact on the bottom line.

Roland’s view

Jet2 is one of the AIM market’s largest and most successful companies and it continues to expand. Passenger numbers rose by 12% last year and on-sale seat capacity for this summer is currently 8% higher than last year.

In this context, I think it’s interesting to note that this airline remains a relative minnow alongside budget travel giants Ryanair and easyJet.

Ryanair’s latest monthly metrics show the airline flew 19.9m passengers in June. That’s slightly more than the 19.8m that Jet2 carried in the whole of last year! easyJet expects to fly c.100m passengers in its current financial year.

While these larger airlines target a broader range of routes and customer segments, I think these figures support the view that Jet2 could still have plenty of runway left for growth.

Today’s FY26 estimates price the stock at less than eight times forward earnings, backed by one of the strongest balance sheets on the UK market. Notwithstanding the macro risks, I’m happy to maintain my previous GREEN view following these results.

ZIGUP (LON:ZIG)

Down 7% to 337p (£755m) - Preliminary Results - Roland - AMBER

ZIGUP plc (LSE:ZIG), the leading integrated mobility solutions platform providing services across the vehicle lifecycle, is pleased to announce its results for the full year ended 30 April 2025.

In May, I tentatively upgraded my view on van hire and accident repair group Zigup to AMBER/GREEN, after the company said its results for the year to 30 April would be “modestly ahead” of expectations.

Today we have the actual numbers, which have received a negative reception from the market despite being billed as “ahead of expectations”.

Did I get it wrong in May, or is today’s drop highlighting a potential buying opportunity? Let’s take a look.

FY25 results summary

2024/25 were always expected to be reset years following the bumper profits generated during the supply chain crisis period of 2022/23.

Sure enough, Zigup’s profits did fall last year while its revenue flatlined:

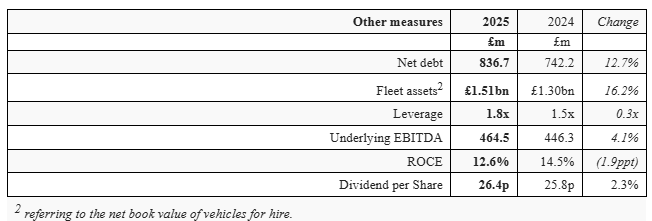

Revenue down 1.1% to £1,812.6m

Adjusted pre-tax profit down 7.6% to £166.9m

Reported pre-tax profit down 37.4% to £101.5m

Adjusted earnings per share down 4.9% to 58.4p

Revenue appears to be below consensus expectations of £1,882m, but adjusted EPS of 58.4p is ahead of Stocko consensus for 54.1p. I assume that this adj EPS figure is the “ahead” result management has referred to today.

Trading in the core Northgate van hire business appears to have been relatively strong last year, with revenue up 5.2% to £683m and rental profits up 9.1% to £120m.

Zigup’s overall result was held back by falling profits elsewhere:

the continued normalisation of disposal profits (down 15% to £53m)

lacklustre profitability in the claims management division, where revenue was flat at £872m and operating profit fell by 26% to £38m.

Disposal profits are a core element of any vehicle rental business, but in fairness I think the company’s fleet is still evolving as the changes made during the supply chain crisis are unwound. I would expect this decline to level out fairly soon – the company says the average age of its UK fleet fell by 5.5 months to 28.5 months last year.

Rental profits grew ahead of rental revenue last year, indicating an improved margin and suggesting decent demand for hire vehicles.

This growth seems to have been concentrated in Spain, where the average number of vehicles on hire rose by 9.4% last year. In the UK, there was a 2.6% decline in vehicles on hire.

The net result of all this change was that Zigup invested in expanding and freshening its rental fleet last year. This resulted in a free cash outflow for the year of £58.1m and an increase in net debt, although this may not be a problem if the newer vehicles generate expected positive returns going forwards:

For hire businesses I tend to look at net debt as a proportion of rental asset value, using 50% as a rule of thumb for comfortable leverage. These figures show this ratio reducing from 57% to 55% last year, which seems positive.

However, lower profits mean Zigup’s net debt to EBITDA ratio rose to 1.8x, which is towards the upper end of what I’d want to see for a business with somewhat average profitability metrics:

The company’s profits are heavily adjusted, but on a statutory basis my sums suggest an operating margin of 7.5% for FY25, with a return on capital employed of 7.2% – both below the comparable figures from last year.

Outlook

As with Jet2, I think the reason for today’s share price drop is likely to lie in the outlook rather than in last year’s results.

Today’s FY26 guidance is positive, suggesting further trading growth in the two operating divisions, albeit with some apparent uncertainty on disposal profits:

We see good opportunities in FY2026, with robust demand for our mobility solutions across our markets.

We would expect this to include achieving mid/upper single digit underlying EBIT growth for our operating divisions, before taking into account disposal profits.

I am inclined to take a cautious view on the overall outlook for profits this year. Last year’s weaker trading in the UK hire business provides one clue about possible challenges. So too does the weaker FY25 result from the claims business, which came despite management commentary on “insurance contract extensions” and “new partner channels”.

Broker consensus forecasts ahead of today suggested FY26 adjusted earnings could fall by 5% to 51.4p per share. I’m not sure if this commentary implies any change to these expectations, given today’s earnings were ahead of previous expectations.

Roland’s view

Excluding disposal profits from guidance is understandable in some ways, as I explained above.

But in another way, I don’t think it’s really acceptable. Disposal profits are a core element of the vehicle rental business model. Zigup sold over 20,000 used vehicles last year, equivalent to nearly half its rental fleet.

In today’s results, the company says used van disposal pricing has been stable since October 2024. Management also reminds us that it has “successfully forecast and highlighted” disposal pricing trends on a number of previous occasions.

All of this leaves me wondering why today’s guidance for segmental profit growth has been caveated by the exclusion of disposal profits. I can’t help feeling this might be a way of disguising the possibility that overall profit growth this year will be limited, or even negative (in line with forecasts).

My view on this business is mixed. I upgraded to AMBER/GREEN in May but had previously been neutral.

The shares often look cheap and indeed today’s results leave Zigup trading below book value, with a near-8% dividend yield that’s remained covered by earnings (albeit not by cash flow).

On the other hand, leverage is significant and profitability appears to be under pressure. Looking ahead, consensus expectations prior to today were for a further drop in earnings for FY26. Today’s outlook statement doesn’t address these expectations directly, in my view, instead providing caveated guidance about underlying divisional profits.

It’s possible that I’m being too cautious, but I’m going to revert my view to neutral today

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.