Good morning! I hope you had a relaxing weekend.

Out of time for today, thanks all. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our View (Author) |

|---|---|---|---|

JD Sports Fashion (LON:JD.) (£3.87bn | SR75) | £200m buyback to begin immediately with £100m tranche to complete by 31 July 2026. Second tranche will commence thereafter. | ||

Johnson Matthey (LON:JMAT) (£3.87bn | SR72) | Long stop date for satisfaction of conditions for sale extended from 21 Feb to 21 Jul 26. To reflect CT’s [weaker] business performance in FY26, the sale price has been cut to £1,325m from £1,800m previously. JM now expects to return c.£1,000m to shareholders (previously £1,400m). Return will be made through £800m special dividend + share consolidation and £200m buyback. | AMBER ↓ (Roland) [no section below] The CT sale was originally agreed in May 2025. During the y/e 31 March 25, the CT division contributed c.25% of group profit with an operating margin that was at least double the remainder of the business. At the time, I thought it looked like JM might be selling an attractive unit (and I still do). However, it seems trading has deteriorated due to the deferral of some key licensing projects and “reduced profitability” due to the “challenging market environment”. Assuming the original valuation multiple of 13.3x EBITDA is being maintained, today’s price drop suggests CT’s annualised EBITDA might have fallen by 26% to c.£100m. CT is involved in the chemical, hydrogen and fuel sectors, so I’m not sure how much of this is cyclical. This morning’s c.15% share price drop equates to a £580m reduction in market cap, slightly exceeding the £475m reduction in sale price. I think this is a fair reflection of the situation, but I wonder if investors should consider the risk that trading across the remainder of the group could also disappoint. I’m going to move our view down to neutral until we learn more. | |

MONY (LON:MONY) (£801m | SR79) | Revenue +2% to £446.3m, pre-tax profit +1% to £80.7m. Adj EPS +5% to 17.9p, in line. 2026 outlook: confident can deliver adj EBITDA in line with current consensus range (£142-153m). | AMBER/GREEN = (Roland) Growth remains almost non-existent, but these results showcase MONY’s usual high quality financials and strong cash conversion. With a P/E of 8 and an 8% dividend yield, I think what’s needed for a re-rating is for investors to gain confidence that MONY can protect itself from erosion by AI and find a route back to growth. On balance, I think the group’s exposure to complex regulated products, loyal customer base and apparent ambition to become a DIY savings and investment platform might provide this opportunity. However, I recognise that I don’t really know how far the incursion of AI services may yet stretch – or if better, AI-native competitors will emerge. On balance, I think the group’s low valuation and strong balance sheet mean it’s fair for me to maintain a broadly positive view. | |

Pantheon Infrastructure (LON:PINT) (£544m | SR77) | Has reset the term on its £115m RCF to 36 months (Feb 2029). Drawn margin payable has been reduced from 2.85% to 2.65% over benchmark. | AMBER/GREEN ↓ (Graham) [no section below] This is the infrastructure trust managed by private equity firm Pantheon. They also manage Pantheon International (LON:PIN) (in which I have a long position). Today's news from PINT is purely positive: their credit facility is extended at a lower margin. I gave this trust an overview last year and had a positive view. This appears to have been the right call as the share price is up by 21% since then and its discount to NAV has closed from 20% to what I think is now only 8% (to calculate this, I've deducted the 2.173p dividend from the September 2025 NAV, which was 122.7p, and compared that against the current 115.98p share price). While generally I'm happy to follow short-term momentum and stay GREEN on stocks that are rising, I'm not willing to do that for an infrastructure investment trust whose discount to NAV has closed to such an extent. Continued upside is inevitably capped in this case. So let's take it down just one notch, to AMBER/GREEN. | |

Caledonia Mining (LON:CMCL) (£433m | SR84) | After reviewing options, Caledonia has appointed Stanbic Bank Zimbabwe and CBZ Bank Limited as co-lead arrangers for the $150m facility needed to fund the Bilboes gold project in Zimbabwe. | ||

Enquest (LON:ENQ) (£285m | SR80) | 2025 production 45,606 boepd, at top end of guidance (40-45kboepd). Costs delivered slightly below guidance. Settled Magnus contingent consideration for one-off $60m payment. 2026 guidance: storm damage has hit North Sea production. FY26 guidance 41-45 kboepd. | ||

| Capricorn Energy (LON:CNE) (£185m | SR83) | Operational and trading update | 2025 revenue $119m, capex $77m, net cash $103m. Working Interest production of 20,024 boepd. 2026 outlook: production guidance 18,000-22,000 boepd, capex $85-95m w/ op costs $5-7/boe. | |

Smiths News (LON:SNWS) (£177m | SR98) | Received Warning Notice from UK Pension Regulator (tPR) re. Tuffnells pension scheme. tPR is considering issuing a Financial Support Direction against Smiths News. The maximum tPR can seek is estimated at £3,467,000. | GREEN = (Graham) This update, while negative for Smiths News, does not relate to their current trading. And the maximum liability is affordable. Therefore, I don’t view this as a negative news story that needs to change my existing stance on the company. | |

Pulsar Helium (LON:PLSR) (£142m | SR31) | Jetstream #6 drilled to 2,597ft. #7 underway with a target depth of 3,000 feet. 2D seismic totalling 41.5 miles completed on Topaz Project on 20 Feb 26. | ||

Atlantic Lithium (LON:ALL) (£135m | SR13) | Company is awaiting outcome of Ghana Goct committee meeting on 12 Feb 26 to consider ratification of Ewoyaa Mining Licence. Company received conditional takeover proposal recently, but discussions have now ceased with no agreement. | ||

Camellia (LON:CAM) (£125m | SR66) | Trading Update | Improved crop yields and prices mean that the company expects to report improved trading performance with “approximate break-even trading results for 2025” (FY24: £5.5m loss). | |

Gemfields (LON:GEM) (£92m | SR38) | Auction revenues of $53m, 121/135 lots were sold (189,620 carats). Avg sale price $279/carat. | ||

Smarter Web (LON:SWC) (SR23) | Acquisition: Web Design & Digital Marketing Agency & Subscription Agreement Update - £26,745 Proceeds | Acquired Squarebird for £1,690,000. Will be funded with £675k in new shares, £270k from SWC’s cash, £340k from Squarebird’s cash and £405k in deferred payments. | [GN] Market cap depends on the share count as discussed here. |

Helix Exploration (LON:HEX) (£53m | SR12) | Commencement of gas production at the company’s flagship Rudyard Project making it the first Helium gas producer in the state of Montana. | ||

Synectics (LON:SNX) (£42m | SR82) | New contracts. Agreement to enhance and maintain a traffic monitoring camera system for a Southeast Asian government. A further two contracts to supply its COEX camera range in the Netherlands. | AMBER = (Roland) [no section below] The company has secured its first contract in the transport vertical in SE Asia, potentially opening a new avenue for growth. There’s also a camera win for an renewable project in the Netherlands. It’s all positive, but no financial details are provided today. This suggests to me that these are business-as-usual wins, with no impact on FY26 expectations. I don’t see any reason to change my neutral view ahead of March’s FY25 results. | |

Aoti (LON:AOTI) (£39m | SR28) | FY25 revenue and adjusted EBITDA margin in line with consensus. Expectations: revenue $66.1m, adjusted EBITDA margin 10.8%, net debt $11.2m. Due to reimbursement issues, will cease treating new Arizona Medicaid patients from 1st April 2026. Arizona is expected to have contributed approx $9.2m of revenue in 2025. Could cause positive or negative adjustments to the 2025 results. | BLACK (FY26 estimates reduced at PanLib: revenue estimate down 6.7%, adj. EBITDA estimate down 45.4%.) | |

Victoria (LON:VCP) (£30m | SR23) | Q3 revenue (to December) was down 3%. Trading in the first half of January was then “significantly impacted by weak consumer confidence and weak footfall at our end customers due to geopolitical events across our key markets…” Q4 revenue to be “below its previous expectations and approximately 5% below FY25.” FY26 EBITDA to be c. £95m vs. expectations £110.7m. | BLACK (RED =) (Graham) | |

Novacyt SA (LON:NCYT) (£24m | SR25) | Novacyt has conditionally agreed to acquire Southern Cross Diagnostics, “a profitable distributor of diagnostic and life science products, for an initial cash consideration of AUD$8.5m” (£4.4m). SCD has been a distribution partner for Novacyt subsidiary Yourgene Health. | ||

Kelso group (LON:KLSO) (£13m | SR33) | Kelso has increased its stake in The Works (market cap £23m) to 7.0%, up from 6.6%. [GN: sounds like a c. £100k purchase?] The Works “is one of the most undervalued companies on the UK stock market”. | ||

Nanoco (LON:NANO) (£12m | SR16) | Nanoco has moved to add Apple Inc as a named co-party in the existing litigation that Shoei brought against Nanoco in the US. This “does not increase the materiality or potential value of this claim”, but is “prompted by the positions Shoei has taken in the litigation”. |

Graham's Section

Smiths News (LON:SNWS)

Down 4% to 69p (£170m) - Statement re Tuffnells Parcels Express Pension - Graham - GREEN=

A technical and not very pleasant update from Smiths News:

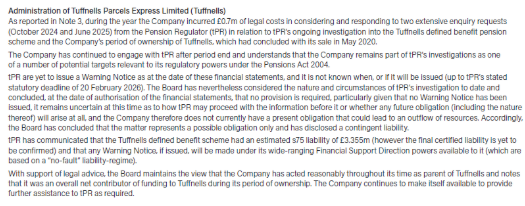

Smiths News (LSE: SNWS), the UK's largest news wholesaler and a leading provider of early morning end-to-end supply chain solutions, confirms that on 20 February 2026 it received a Warning Notice from the UK Pensions Regulator in relation to the Tuffnells Parcels Express Pension Scheme, the possibility of which was disclosed in the Company's last annual accounts (see Note 20).

It’s a reminder that if we don’t read annual reports in detail - something that might not be practical for most well-diversified portfolios - we can’t complain if we miss disclosures in them.

Tuffnells was an unfortunate acquisition for Smiths News: bought for £113m in 2014, and sold for £15m in 2020. And the damage that it caused continues to linger. Tuffnells subsequently went into administration and has been restructured under new owners.

I’ve hunted down Note 2020 from the most recent Smiths News annual report (don’t worry - the text is bigger in the document itself!).

The note says that in the Board’s view, “no provision is required” in relation to the Tuffnells pension scheme, and that the estimated liability in the pension scheme was £3.355m at that time.

Thankfully, the liability has now only grown to £3.467m, and that’s “the maximum amount tPR [the Pensions Regulator] can seek in aggregate from all targets”.

Others besides Smiths News may be required to pay:

In addition to Smiths News, a number of other parties connected to Tuffnells are identified in the WN [warning notice] as potential targets of tPR's powers.

It remains unclear how much Smiths News might be required to cough up.

Graham’s view

I’m going to stay positive on this for reasons which I think are fairly straightforward:

This update, while negative for Smiths News, does not relate to their current trading.

The maximum liability is affordable. Smiths News is highly cash-generative, has moved into a net cash position, and pays dividends (yielding >8% according to the StockReport)..

This type of problem - lingering issues from failed M&A - is not a regular occurrence for Smiths News. The company hasn’t made a major acquisition in many years. I think that Tuffnells itself may have been the last one.

Therefore, I don’t view this as a negative news story that needs to change my existing stance on the company. So I’m positive, and I’m staying that way.

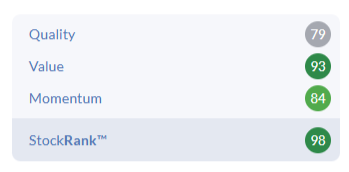

The StockRanks are with me:

Victoria (LON:VCP)

Down 7% to 24.35p - Trading Update - Graham - BLACK (RED =)

Victoria PLC (LSE: VCP), the international designer, manufacturer and distributor of innovative flooring, provides a trading update and outlook for FY2026.

I’ve been very negative on this one for a long time, saying in December that I thought it was a probable zero for shareholders.

I’m unlikely to change my mind today after a profit warning.

Q3 (to December) was ok:

Revenue down 3% (an improvement from H1 which was down 7%)

Excluding Rugs, which has been disrupted by the transition of manufacturing from Belgium to Turkey, revenue was down 1.5% in Q3.

But then Q4 got off to a bad start:

Trading in the first half of January, however, was significantly impacted by weak consumer confidence and weak footfall at our end customers due to geopolitical events across our key markets: western Europe; North America and the UK. Whilst recent weeks have shown improvements in trading, the board now expects Q4 revenue to be below its previous expectations and approximately 5% below FY25.

As a result, the board expects post-IFRS16 EBITDA to be approximately £95m for FY26 as a whole*.

Expectations are helpfully provided. Market expectations were for FY March 2026 revenues of £1,064m and EBITDA of £110.7m.

That’s a 14% miss against EBITDA expectations, and it comes with just five weeks left in the financial year.

I always think it’s a little worse when a large miss is announced just before the financial year-end. Granted that conditions can change quickly and that seasonal effects can be at work, but it doesn’t inspire confidence for investors when the profit outlook can change so quickly.

But then this is not a stock that has been inspiring much confidence recently:

“Progress on EBITDA improvement initiatives”

Management's immediate focus remains on delivering EBITDA improvement initiatives within our control.

The bondholders will call the shots here in my view, and I view the commentary now as being more aimed at placating them rather than giving all that much hope to shareholders.

Management have been busy:

A new ceramics line in Spain.

Relocating rugs manufacturing from Belgium to Turkey (“shipping disruptions have been greater than anticipated”).

Integrating UK underlay businesses with Australian businesses.

There is a positive spin on a reduced outlook for 2027:

Whilst a lower starting point on volume will reduce the outlook for 2027, the currently disclosed EBITDA improvement initiatives remain on track, and further EBITDA improvements have been identified across the divisions and will be quantified as part of the ongoing budget process.

And there is a vague reference to “broader governance improvements”:

Increased rigor in tracking these improvements is being implemented along with broader governance improvements, and further detail of these initiatives will be provided in due course.

I wonder what these might be?

Capital structure and cash initiatives:

The Company remains focused on strengthening its capital structure and continues to engage with all its capital providers to progress refinancing plans for the benefit of all stakeholders including to address its 2028 senior secured notes.

My understanding is that €167m of 2028 senior secured notes are still outstanding. They have an even lower rating (CCC-) than the 2029 notes, to which they are subordinated, and are expected to receive pennies on the pound at best, in the event of a default.

Graham’s view

Checking my notes from the interim report, I see that net debt was over £1 billion, with a leverage multiple of 8.6x, and the business made an underlying pre-tax loss.

It needs multiple economies to boom in order to have any chance of survival for the equity, in my view. It especially needs a boom in demand in Western Europe and the UK.

Unless external conditions suddenly start to make business very easy, I don’t see how it gets out of this situation without very high equity dilution (as a best-case scenario). The EBITDA multiple would be far too high even if the business was profitable. But it's not, and so the whole thing probably needs to be restructured.

A business in this financial condition simply can’t afford to have its outlook repeatedly downgraded:

Roland's Section

MONY (LON:MONY)

Up 1.5% at 155p (£822m) - Preliminary Results - Roland - AMBER/GREEN =

Today’s in-line results and outlook statement have received a cautiously optimistic response from the market – perhaps unsurprisingly given MONY’s low valuation and strong continued strong profitability:

However, as I noted in The Week Ahead, MoneySupermarket.com owner MONY has been a big casualty of the AI sell off. This has added to existing concerns that the business had gone ex-growth.

2025 results: key points

Today’s results highlight both the strengths and weaknesses of MONY’s business. Here are the main numbers:

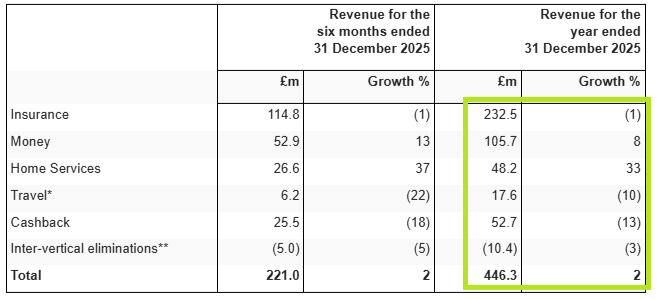

Revenue up 2% to £446.3m

Adjusted EBITDA up 2% to £145.1m

Operating margin 26.3% (FY24: 25.8%)

Pre-tax profit up 1% to £80.7m

Adj EPS up 5% to 17.9p

Dividend up 1% to 12.63p per share

The company says that its re-engineered cost base, modern tech platform and “increasing use of AI” helped to cut operating costs by 4% last year. MONY has entered into an agreement with OpenAI, giving the group access to the latest models.

This reduction in costs helped to support an increase in profitability, despite revenue only rising by 2%. My sums suggest MONY generated a return on capital employed (ROCE) of 41% (FY24: 36%) and free cash flow of £92m. This latter figure represents 114% conversion from net profit of £81m – an excellent result that I see as a hallmark of a high quality business.

However, the problem is obvious enough – there’s no real growth here.

Trading commentary: MONY operates in key segments – Insurance, Money and Home Services. There’a also Travel, but this is currently fairly immaterial.

Underlying conditions in some of these markets have been difficult in recent years, reducing activity such switching or new account applications. Areas of weakness have often offset stronger results elsewhere. Management attempt to put a positive spin on this in today’s commentary:

The strength in our breadth continues to provide us with resilience, as different markets move through their cycles. All of this translates to a highly effective, resilient and profitable business, with strong operating cashflow and efficient capital allocation, that is well positioned to deliver sustained and consistent growth.

Unfortunately, the main area of weakness last year was Insurance. This is also MONY’s the largest sector, generating roughly half of all revenue:

Insurance revenue was down 1%, with challenging market conditions in car and home offset by strong performance in other channels such as Life.

The size of the Insurance segment means that decent growth in Money (banking and credit cards) and Home Services (a recovery in energy switching) was not enough to move the needle on group results:

It’s also a little disappointing to see a 13% decline in cashback revenue last year.

Cashback revenue fell 18% [in H2] with consumer confidence remaining subdued impacting both retail spending and merchant marketing budgets as they focused on profitability.

MONY acquired cashback business Quidco for up to £101m in October 2021. At the time, Quidco was generating annual revenue of £59m with adjusted EBITDA of £7.9m.

Five years later, Quidco’s revenue appears to have fallen by 11%, while cashback EBITDA is unchanged at £7.8m. Being part of the broader MONY ecosystem does not seem to have provided opportunities for structural growth in the cashback business, although it looks like there have been some cost-saving benefits.

Based on this EBITDA figure, my guess is that the Quidco acquisition is only generating a mid-single digit ROCE. The sellers appear to have timed their exit well here, in my view and I am not convinced the low-margin cashback business is generating very much value for MONY shareholders.

The only exception to this might be if Quidco users are being converted to higher-margin and more loyal MoneySupermarket.com users than they would otherwise have been anyway. This is hard to determine.

2026 Outlook

Today’s outlook is in line but rather brief:

Our recent trading performance coupled with momentum in our strategic execution gives the Board confidence that we will deliver Adjusted EBITDA for 2026 in line with our current published consensus range.

The company says market consensus for 2026 adj EBITDA is £146m, with a range of £142m to £153m.

2025 EBITDA was £145m, today’s guidance suggests profits are expected to be broadly flat once again in 2026.

A combination of cost control and a £25m buyback may help to lift earnings per share again this year.

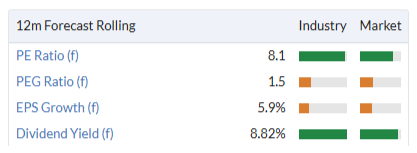

My feeling is that consensus is likely to remain broadly unchanged following today’s results, leaving MONY shares on a forward P/E of 8.5 with an 8% dividend yield:

Roland’s view

Today’s results and stable outlook leave MONY looking very cheap, with a tempting 8% yield.

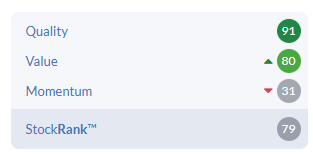

Given the financial quality of the business, I am not surprised to see the StockRanks view this as a Contrarian stock – high quality and value, but low momentum. I don’t expect this profile to change very much when today’s numbers have been digested by the algorithms:

At this kind of valuation, I would argue that only modest growth is needed to justify the current share price and perhaps a moderate re-rating.

The big question is whether this business will be sustainable, or if clever AI chatbots and agents will simply replicate what MONY does without requiring AI-native users to go to the effort of visiting MONY’s websites.

A quick search suggests that for simple product queries, such as Savings accounts, AI already has most of the right answers (albeit some are cribbed from MoneySupermarket.com).

However, I can see some areas where the company might be able to develop or maintain a competitive advantage for a little longer:

Price comparison for complex, regulated products. You can’t get insurance quotes on AI chat and I think the barriers to entry may be higher here. An AI agent would effectively have to replicate much of MONY’s UI and back-end integrations with insurers.

The company says it has now launched its own MoneySuperMarket ChatGPT app, so has a route-to-market from OpenAI. This could be tough for new brands to complete with.

Membership/loyalty services. MONY sees this as a growth area and says that its SuperSaveClub (SSC) now has “a loyal, engaged base of more than 2.1 million members” and contributes 16% of group sales. These members make a significantly greater contribution to the group’s results than other users:

Members transact more often and generate higher value, with an average revenue per user (ARPU) of £35, compared with £20 observed more widely in the group;

Cross‑enquiry rates also remain significantly higher at 45%, more than double observed outside the club;

SSC incremental margin is 75%, compared with 62% for non‑club customers.

Will MONY become a financial platform? A recent product launch and associated commentary in today’s results makes me think that management is working towards the possibility of becoming a consumer savings and investment platform.

The company has recently launched Savings by MoneySuperMarket, which allows customers to find a competitive savings account and manage it without having to leave the platform (my bold):

Once set up, they can view balances, track deposits, top up through a holding account, and switch into new products in just a few clicks. This is unlike anything we've been able to offer on the platform before. Built in the SSC ecosystem, members also benefit from rewards, personalised prompts, and educational content, helping them maximise returns and build financial confidence.

Savings also provides a natural gateway into Investments, and a seamless path from short‑term savings to longer‑term financial growth which we will be launching later in the year.

I haven’t used this service, but it sounds very similar to AJ Bell’s Cash Savings hub and the equivalent service at Hargreaves Lansdown.

I wonder if MoneySupermarket.com will leverage its strong brand and market share to become a mass-market savings and investment platform. If done well, the group could disrupt the cosy status quo for existing players, while also defending itself against any erosion of its business by AI services.

Conclusion: I don’t know how far new AI-native tools will go in displacing products and services such as price comparison. But on balance, I am a little more positive about MONY than I was prior to considering today’s results.

Given the value on offer and the high cash yield, I think it’s very fair to maintain my previous broadly positive view of AMBER/GREEN following these results.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.