Good morning! The Agenda is complete.

That's all for today, cheers! Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our View (Author) |

|---|---|---|---|

Rolls-Royce Holdings (LON:RR.) (£110bn | SR67) | Underlying operating profit £3.5bn (2024: £25 billion). Free cash flow £3.3 billion. 2026 guidance of £4.0bn-£4.2bn underlying operating profit and £3.6bn-£3.8bn free cash flow. Upgraded mid-term targets. | ||

GSK (LON:GSK) (£90.2bn | SR92) | Japan's Ministry of Health, Labour and Welfare has accepted for review a new drug application for bepirovirsen for the treatment of adults with chronic hepatitis B. | ||

London Stock Exchange (LON:LSEG) (£39.4bn | SR50) | Adjusted operating profit +10.8% (£3.5bn). Adjusted EPS +15.7%. 2026 guidance: organic growth 6.5% to 7.5%, constant currency EBITDA margin +80 to -100 basis points. New medium-term guidance for 2027-2029, “reflecting our confidence in continued strong progress”. | ||

Howden Joinery (LON:HWDN) (£4.61bn | SR87) | Revenue +4.1%, PBT +5.1%. "For 2026, our planning assumption is that the UK kitchen market will be level year on year, following several years of decline, in what remains a competitive marketplace.” Year-to-date performance in line with expectations, on track to meet current market expectations for FY26. | ||

Hikma Pharmaceuticals (LON:HIK) (£3.67bn | SR63) | Revenue +6%, operating profit -12%, reflecting the impact of a legal settlement. “Core” operating profit up 3%. 2026 outlook: revenue growth 2% to 4%, core operating profit $720m to $770m (2025: $741m). | ||

Man (LON:EMG) (£3.1bn | SR62) | Financial results for the year ended 2025 & Directorate change | AUM $227.6bn (2024: $168.6bn). Net inflows $28.7bn. Relative investment performance 1.3%. | |

Drax (LON:DRX) (£2.98bn | SR98) | Adjusted EBITDA £947m (2024: £1,064m). Outlook: full year 2026 expectations for Adj. EBITDA in line with analyst consensus estimates. | ||

WPP (LON:WPP) (£2.94bn | SR62) | Revenue -8.1%, or -3.6% like-for-like. Operating profit down 71% (£382m). Headline operating profit down 22.6% (£1,321m). Outlook: encouraged by the recent improvement in new business, but LFL revenue less pass-through costs to decline in the mid to high-single digits in H1 2026 with an improving trajectory in H2. | ||

Seplat Energy (LON:SEPL) (£2.5bn | SR94) | Group production averaged 131,506 boepd, up 148% from 2024. Revenue $2,726 million up 144.2%. Outlook: Production guidance of 135-155 kboepd. Mid-point represents a ~10% increase on 2025. | ||

Genus (LON:GNS) (£2.11bn | SR67) | H1 revenue +0%, adjusted operating profit +38% (£55.8m). Outlook in line with market expectations. | ||

Derwent London (LON:DLN) (£2.05bn | SR68) | New lettings of £11.3m signed at 10% ahead of ERV. EPRA earnings per share down 7.6%. Near-term reduction in EPRA earnings until Network income commences, with growth anticipated in H2 2026 and into 2027. Forecasting 25% to 30% growth in EPRA earnings per share by 2030. | ||

Ocado (LON:OCDO) (£1.97bn | SR20) | SP -8% Revenue +12.1%, adjusted EBITDA £178m (2024: £112m). Outlook: FY26 Technology Solutions revenue c.£500m and EBITDA margin c.30% excl. CFC closure fees. | AMBER/RED = (Graham) We have been quite sceptical of this one and that continues to appear the right approach. Management emphasis growth in adjusted EBITDA but adjusted earnings before taxes are still deeply negative at minus £353m (last year: £365m). There is a large accounting gain of £783m as Ocado Retail is no longer consolidated as a subsidiary, but is instead treated as an investment. That large accounting gain produces a statutory profit, but it doesn’t convince me that we need to change stance here. Multiple site closures in North America suggest to me that the model is just not working very well, and is not going to work. The company argues that it has learned from the experience. | |

Tate & Lyle (LON:TATE) (£1.78bn | SR37) | Q3 operating performance in line with expectations and consistent with the first half. Quarterly revenue +15% including the combination with CP Kelco, down 2% like-for-like. Outlook for FY March 2026 unchanged, continuing to expect like-for-like revenue and EBITDA to decline by low-single digit percent. | ||

Great Portland Estates (LON:GPE) (£1.39bn | SR38) | Agreed 16 Fully Managed deals since 1 January 2026. £9.1 million of annual rent, 9.7% ahead of ERV. | ||

Jupiter Fund Management (LON:JUP) (£994m | SR96) | Underlying PBT £138.3 (2024: £97.5m), driven by performance fees of £120m. AUM +19% (£54bn). Net inflows £1.3bn. £30m share buyback. Outlook: “...a number of leading indicators have moved in a positive direction. Investment performance has improved across all time periods and short-term performance is particularly strong.” | GREEN = (Graham) I’m going to leave our GREEN stance unchanged, respecting current momentum in the business itself and on the chart, but I do agree with the StockRanks. This is now in some ways a momentum play. The contrarian investment thesis has played out, and those who were willing to bet on it have already doubled their money. | |

CVS (LON:CVSG) (£961m | SR59) | Revenue +5.8%, like-for-like sales +2.7%. Adjusted EBITDA +3.9%. PBT down 4.4% (£15.2m). Leverage rises to 1.41x following investment in acquisitions, capex and share buyback. Confident in the Group delivering full year 2026 results in line with market expectations. | ||

PPHE Hotel (LON:PPH) (£843m | SR41) | Revenue +5.3% to £466.4m, EBITDA +1.3% to £138.2m, Adj. EPRA EPS flat at 125p. Outlook: Forward booking momentum across all regions is encouraging following a strong start to 2026. Remains confident in delivering 2026 results in line with market expectations. | ||

Vanquis Banking (LON:VANQ) (£324m | SR86) | Statutory PBT from continuing operations £8.3m (FY24: loss of £138.0m) and a statutory ROTE of 2.3%, in line with guidance for a low single-digit return. CET1 ratio 16.5% (FY24: 18.8%) provides the necessary headroom to support strategy and growth plans. Liquidity Coverage Ratio of 306% (FY24: 359%). | GREEN = (Graham) | |

Wilmington (LON:WIL) (£249m | SR74) | H1 Revenue +17% to £47.7m (+4% organic), Adj. EBITDA +9%to £10.4m, Adj. EPS falt at 9.9p, Net Debt £65m (25H1: £31.3m Net Cash. “Overall trading for FY26 in line with market expectations with a strong contracted order book for H2.” | ||

Pulsar Helium (LON:PLSR) (£149m | SR31) | In Q1 $2m spent on exploration and evaluation, warrants raised $4.1m, post period end equity fundraise for $10m. | ||

Jadestone Energy (LON:JSE) (£137m | SR68) | 2026 production guidance is set at 18,000-21,000 boe/d. Natural portfolio decline is expected to be offset by the positive impact of the PM323 infill drilling campaign, offshore Malaysia. Free cash flow guidance for the 2025-2027 period is revised to US$200-240 million at US$70/bbl Brent (down from $270m). | AMBER ↓ (Mark - I hold) | |

Mobico (LON:MCG) (£135m | SR13) | Revenue +6.2% to £2.76bn, Adj. Op Profit +9% to £198m. Covenant gearing 2.7x (2024: 2.8x), aided by proceeds from NASB disposal. Outlook: Group expects FY 2026 Adjusted Operating Profit to be in the range of £195m - £210m. | ||

Savannah Resources (LON:SAV) (£134m | SR34) | Revised bypass road design has now been completed and submitted to the Portuguese authorities. Power line relocation drawings have been approved by E-Redes, the national electricity distribution network operator. | ||

Macfarlane (LON:MACF) (£111m | SR71) | Revenue +11% to £300.8m, Adj. PBT -38% to £15.6m, Adj. EPS -34% to 7.62p, dividend held at 3.66p. “In 2026 we anticipate markets and the competitive environment to remain challenging.” Acquisitions not expected in the short term. | AMBER/RED = (Mark) The poor results here were as expected. The adjustments look mostly reasonable to me, putting them on a sub-10x P/E, which may prove to be good value. However, with challenging market conditions persisting, a dreaded H2-weighting, a weaker balance sheet, and flat EPS forecasts, it seems too soon to be considering this as a recovery buy. | |

| Avation (LON:AVAP) (£90.1m | SR48) | Half-year Financial Report | Revenue +1% to $56m, Op Profit +56% to $29.3m, LBT $5.7m (24H1: $9.8m LBT, Net Debt $543m (30 Jun: $604m), NAV PS +2.6% to £2.74. “Avation enters the second half of the financial year with a contracted lease portfolio providing visibility of cash flows, extended debt maturities following the successful refinancing of our unsecured debt obligations and continued demand for leased aircraft amid constrained new aircraft supply.” | AMBER/RED = (Mark) [no section below] A reasonable update with flat revenue and Net Assets increasing slightly. Net debt is down, but there is an increased finance charge leading to a loss. This is due to the accounting treatment of note repurchases. Without this they would have reported a modest profit. However, these results simply highlight the fundamental problem that, despite the large discount to net assets, those assets are unproductive in the current corporate structure, mainly due to the cost of unsecured debt. The recent selling by an activist hedge fund where I understand the company had largely engaged with their requests, shows that there is no easy way to close the gap to NAV, short of selling the whole enterprise to someone with a lower cost of capital. That the management seem unable or unwilling to do so (which undoubtedly would have been Rangely Capital’s preferred exit), means we remain unconvinced about the near-term investment case. |

Strategic Minerals (LON:SML) (£88.6m | SR33) | Discovery of a distinct and continuous, tin-dominant zone of mineralisation separate to the Redmoor Sheeted Vein System. | ||

ECO Animal Health (LON:EAH) (£69.1m | SR92) | Has secured agreements with key strategic distribution partners providing comprehensive coverage across the EU's major poultry markets. | ||

Made Tech (LON:MTEC) (£52.6m | SR68) | H1 Revenue +28% to £27.8m, Adj. EBITDA +35% to £2.4m, Adj. PBT +31% to £1.9m, Sales Bookings -68% to £13.4m, Contracted Backlog -8% to £74.4m, Net Cash £11.9m (25H1: £9.1m). Outlook: Trading ahead of recently upgraded expectations, management anticipates Adjusted EBITDA to be materially ahead of market consensus as contractor mix, utilisation and operational leverage continue to improve. Richard Swinyard will be joining the Group as Chief Financial Officer, with effect from 2 March 2026. | GREEN = (Mark - I hold) | |

Rentguarantor Holdings (LON:RGG) (£42.1m | SR25) | Licence agreement Tenancy Deposit Solutions, trading as mydeposits, to develop a rent deposit product to be offered alongside RentGuarantor's existing professional guarantor service. mydeposits represents approximately 400,000 landlord members and protects more than £1.3 billion of tenant deposits across the UK private rented sector. | ||

Angling Direct (LON:ANG) (£37.2m | SR86) | Revenue +13.8% to £103.9m, Net Cash £10.9m (FY25: £12.1m). “…the Board is confident in delivering a FY26 Adjusted EBITDA of circa £4.8m, ahead of recently upgraded market expectations.” (Pre-IFRS 16 Adj. EBITDA of £4.35 million.) | AMBER/GREEN = (Mark) | |

Corcel (LON:CRCL) (£34.5m | SR4) | 326-line km of high resolution 2D seismic data acquired over the KON-16 block | ||

ATC Music (LON:ATC) (£24m | SR9) | Revenue +33% to £67.5m, adj. EBITDA in line with market expectations of at least £1.25m/ | ||

Eco Buildings (LON:ECOB) (£18.9m | SR15) | Parties have formally agreed to progress to the next stage of implementation of the Senegal manufacturing and housing programme. G2’s €1.75 million contribution for its 35% equity stake, has now been allocated into the JV subsidiary. | ||

Hardide (LON:HDD) (£18.9m | SR49) | £1.8m of new orders from the existing major North American energy sector customer. “These orders lead the Board to expect a further material improvement in revenues and performance for the current financial year to 30 September 2026 as against previous expectations.” | ||

Oriole Resources (LON:ORR) (£15.3m | SR18) | 2 additional drill hole results, incl. 7.8m at 1.29g/t & 1.0m at 4.16g/t. | ||

Nexus Infrastructure (LON:NEXS) (£10.6m | SR52) | FY Revenue +16% to £65.9m, Operating Loss £1.1m (FY24: £1.9m Loss), Net Cash £10.9m (FY24: £12.8m). “The year is progressing in line with management expectations, seasonally weighted to the second half. The strong order book and improving market sentiment provide positive indications for the future.” | ||

Croma Security Solutions (LON:CSSG) (£10.1m | SR69) | H1 Revenue +9% to £5.0m, EBITDA -24% to £0.436m, PBT -45% to £0.252m, Net Cash £4.4m (25H1: £4.2m). “Positive trading performance since the half-year with a strong new business pipeline to support the Board's confidence in the outlook for the full year” |

Graham's Section

Jupiter Fund Management (LON:JUP)

Up 6% to 200p (£1.06bn) - Annual Financial Report - Graham - GREEN =

Very strong numbers from this fund manager today:

Material progress with an encouraging outlook

Here are some of the financial highlights.

Underlying PBT £138.3m (2024: £97.5m), helped by £120m of performance fees (2024: £31m of performance fees)

Actual PBT £131.9m (2024: £88.3m)

Administrative expenses reduced 2%. Cost savings targets delivered ahead of schedule. It was the fourth consecutive year of headcount reductions.

Assets under management: AUM rose 19% to £54bn, helped by net inflows of £1.3bn (2024: net outflows of £10.3bn).

Important to note that Jupiter completed the acquisition of CCAL Investment Management earlier this month, bringing in an additional £15 billion of AUM.

CEO comment:

"Jupiter delivered a strong set of results in 2025. During the year, we generated net positive inflows across both client channels for the first time since 2017, supported by a marked shift in client sentiment with improved investment performance across all time periods…

As we move into 2026, we are in a demonstrably stronger position than we were twelve months ago… With leading indicators improving and momentum building across the business, we have increased confidence in being able to deliver on our targeted 70% cost:income ratio in the medium term."

It took a long wait, but sentiment finally turned when it came to some of these mainstream fund managers. In the end, it took rising UK equities (FTSE over 10,000) combined with nervousness around US valuations to get it done.

The Jupiter share price chart reflects the bull thesis playing out:

In the words of Matthew Beesley, H2 saw “growing demand for risk assets and early signs of a potential shift in client allocations away from US equities”. Passive US-focused mega-cap investing didn’t outperform other strategies as it had done before.

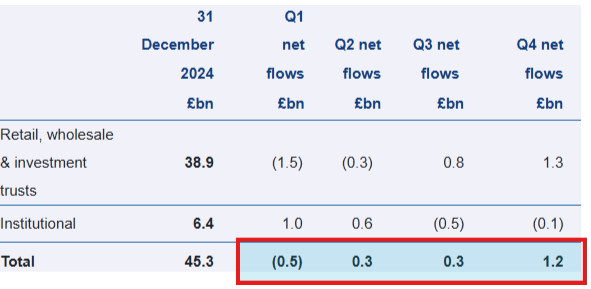

This table shows how Jupiter’s net flows improved throughout the year:

The retail/wholesale channel flipped from a £1.5 billion outflow in Q1 to a £1.3 billion inflow by Q4, which I think demonstrates how private investor sentiment towards the likes of Jupiter improved during 2025.

As for most recent trading, “this positive momentum has continued into the start of 2026, and we continue to be net positive across both... client channels as of today.”

Graham’s view

I went back fully GREEN on this in October and am glad I did so, with the market cap up by 32% since then.

And I’m inclined to stay GREEN on it today, given the positive momentum. Let’s just consider some pros and cons.

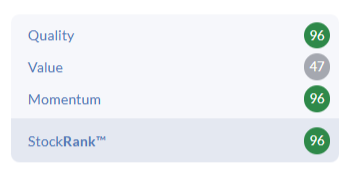

The StockRank is 96 but it’s not a Super Stock, it’s a High Flyer due to having a modest ValueRank.

AUM vs market cap: adding £15bn of CCLA AUM to the Dec 2025 figure, total AUM is around £69 billion. This gives £65 of AUM for every £1 invested in the stock at the current valuation. While still not expensive, I also don’t consider this to be a depressed valuation any more. In October the figure was £82 of AUM for every £1 invested in the stock.

Underlying EPS for 2025 was only 8.7p, compared to 10.9p in 2024, if the impact of performance fees is excluded.

Similarly, before performance fees, Jupiter’s underlying PBT fell in 2025, from £59.2m to £46.6m.

So if we aren’t totally certain about performance fees, which are primarily driven by Jupiter’s thriving “Systematic Equities” division, we do need to be a little more cautious about what might be achieved in future.

Therefore, from a value perspective, I’m much less enthusiastic about Jupiter now, compared to before.

It might still be undervalued, but the undervaluation is less obvious now.

On the other hand, the company is now generating inflows for the first time in nearly a decade, which means the market is willing to pay a much more premium rating for the stock.

What I’m going to do is leave our GREEN stance unchanged, respecting current momentum in the business itself and on the chart, but I do agree with the StockRanks. This is now in some ways a momentum play. The contrarian investment thesis has played out, and those who were willing to bet on it have already doubled their money.

Vanquis Banking (LON:VANQ)

Down 3% to 122.2p (£318m) - Results for the year ended 31 December 2025 - Graham - AMBER/GREEN =

This is another financial stock in turnaround mode:

The results for 2025 are as expected: very low ROTE of 2.3% on the back of a statutory pre-tax profit of just £8.3m. But it is a vast improvement on the prior year, when ROTE was negative 32%!

Other key points:

CET1 ratio 16.5%, down compared to last year, but still at a level I’d consider very conservative.

Customer loans up 22% to £2,824m, ahead of prior guidance. Second charge mortgages and credit cards supported the increase.

Operating costs collapsed to £265m, from £399m last year. Last year’s results included £131m of “notable items”, including a c. £70m goodwill write-off at Moneybarn.

The reduced operating costs are key to the story here. There are genuine operational cost savings (£28.8m), much lower complaint costs (down by £20.8m) and the absence of major write-offs as we saw last year.

Indeed, this is a far, far cleaner performance in 2025 with “notable items” reduced from £131m to only £3m.

That £3m relates to a provision for the FCA Motor Finance compensation scheme. But it’s a rounding error in the grand scheme of things.

Net interest margin: growth in Second Charge Mortgages has helped pull the net interest margin down to 16.8% (previously 18.5%). This might not be the most lucrative form of lending to focus on, but it’s a perfectly legitimate strategy for management to choose. Second-charge mortgages are lower-risk, lower-margin products compared to VANQ’s other lending products.

Outlook: ROTE is seen rising to “low double digits” in 2026, and then “mid-teens” in 2027.

The ROTE guidance of low double-digits for 2026 and mid-teens for 2027 remains unchanged. However, profitability in 2H26 is expected to be higher than 1H26, as balances mature and interest income builds.

It looks like they’ve introduced a heavier H2-weighting for 2026 than previously anticipated.

Dividend: none yet. The last one they paid was a small 1p dividend in 2024.

Graham’s view

I’ve been moderately positive on this and I think it makes sense to stay that way, today.

The bank is trading at a discount to tangible NAV (£358m TNAV vs. £318m market cap) but I think that’s fair, given that it’s still working its way through a turnaround and isn’t expected to achieve an attractive ROTE until next year.

Overall, it seems to me that they are taking a low-risk approach to the turnaround. The balance sheet is being managed conservatively, the product mix is relatively low-risk, and cost savings are a major focus.

That’s totally fine with me. I always try to give companies high praise when costs are controlled and when the accounts are clean. And these accounts are really, really clean.

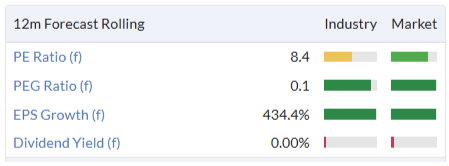

The StockRanks like this, too:

Looking ahead for a possible catalyst, I note that a dividend is expected to be paid out of 2026 profits. As we approach that milestone, I can imagine more investors getting interested in this story.

This still offers some potential value, in my view:

Mark's Section

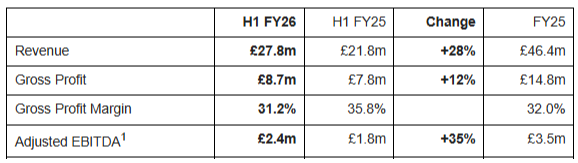

Made Tech (LON:MTEC)

Up 8% at 38p - Interim Results & Appointment of Chief Financial Officer - Mark (I hold) - GREEN

These are a strong set of half-year results:

Adj. EBITDA is rarely my preferred measure. However, there is a low level of amortisation of intangibles here, with them saying;

Intangible assets comprise historic investment in Capability IP and are expected to be fully amortised by the end of FY26. All R&D costs in the Period, including investment in technology platforms, were charged to the income statement.

There were no exceptionals, lease payments are relatively modest. Adj. PBT at £1.9m shows similar growth rates and the gap to the statutory figure is narrowing. Share Based Payments are significant. At the very least, investors should be looking at the fully diluted share count. It is worth noting that not all these SBP are management LTIPs, but include Save As You Earn, which can be an important in retaining key staff:

The SAYE scheme allows all employees to participate in the growth journey of the business. The contributory scheme was launched in October 2024, and given its success, all eligible employees were invited to participate again in October 2025. As a result of the take-up circa 37% of all eligible staff are participating in the SAYE scheme.

Outlook:

What is a little concerning is that the strong performance hasn’t been replicated in sales activity, with low bookings in the half meaning that the backlog has declined:

They are quick to point out the lumpiness of orders, so this perhaps doesn’t reflect anything other than contract signing timelines:

Our sales pipeline remains robust, and while bookings can be lumpy between periods, recent bid activity and conversions support our confidence in continued momentum in H2 FY26 and into FY27.

Indeed, they report an increase in government procurement activity after a lull period. A dynamic that holders of another technology provider to the UK Government doing very well at the moment, TPX Impact, will be familiar with.

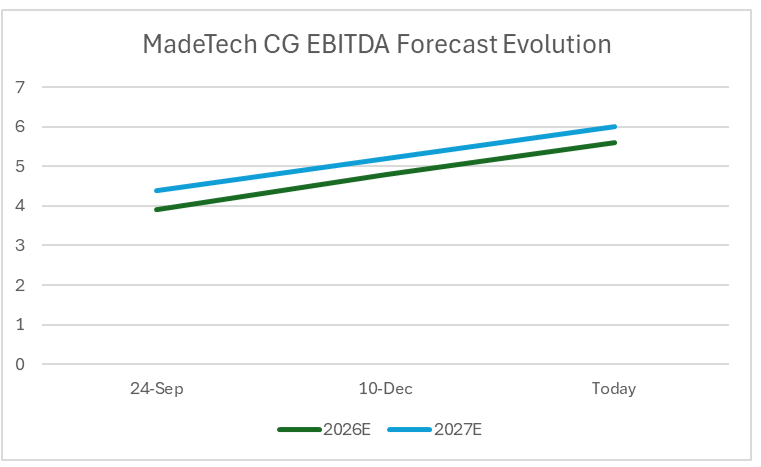

This weaker sales booking hasn’t stopped them announcing their second materially ahead statement for the full year:

Trading ahead of recently upgraded expectations; management anticipates Adjusted EBITDA to be materially ahead of market consensus as contractor mix, utilisation and operational leverage continue to improve

Forecasts:

Their broker, Canaccord Genuity say:

We lift FY26-27 revenue forecasts by 4% & EPS by 5-12%. Our 60p target price is unchanged and implies ~70% upside from current levels.

This didn’t immediately scream “materially ahead” to me. However, the guidance is for EBITDA, and with a significant cash balance, the EPS won’t be affected as much by positive operational trading. CG have raised FY26 EBITDA by 17%, and by 44% since they initiated coverage on the company six months ago:

Balance sheet:

As already mentioned, this is a cash-rich company, with cash rising to £11.9m from £9.1m a year ago and £10.4m at the end of FY25. Canaccord increase their year end cash estimate slightly to £13.5m.

This looks to be real cash, with receivable of £9.8m comfortably exceeding payables of £6.6m. Cash is earmarked for organic or inorganic growth in Software, and area they see the most opportunity to help public sector bodies achieve their goals:

We remain in the early stages of commercialising our software portfolio and continue to take a disciplined approach to investment, focused on proving the model, deepening client adoption and building a sustainable platform for growth. Alongside organic development, we continue to actively explore targeted acquisitions within software and adjacent capability areas.

Net tangible assets are around £15m compared to a market cap of £55m, so there is not much in the way of tangible asset backing. However, you wouldn’t expect there to be in this sort of business, and there is no sign they will need this backstop.

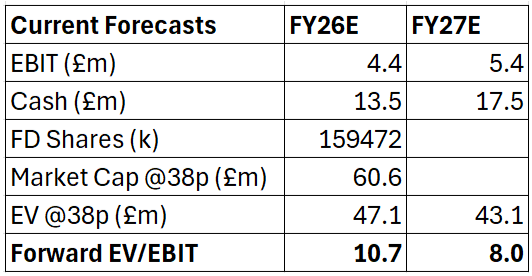

Valuation:

Given the cash balance, enterprise valuation metrics are going to be most relevant here. Canaccord calculates that the company trades on an FY26 EV/EBITDA of 7. This tends to be around the market median, and perhaps a little above the level for smaller UK companies. However, this company is forecast to grow earnings rapidly, and the FY27 EV/EBITDA of 5.8x looks good value.

On my own preferred measure of fully diluted EV/EBIT, the metrics are slightly higher than when I last reviewed the company. However, they still look low for a business growing at these rates:

Mark’s view

I am pleased to see I upgraded this to GREEN at 31p following their previous “significantly ahead” statement in December. The lower sales bookings give me slight pause for concern, but at the end of the day, the current trading performance suggests this is merely timing effects. The share price is now higher than the forecast but those forecasts have been upgraded. It is not quite as good value now. However, momentum is clearly with the business and with the UK government clearly focussing on digital transformation, following the Spending Review-related hiatus, I don’t see why FY27 won’t see further upgrades in time. As such, I am in no rush to moderate our view.

Jadestone Energy (LON:JSE)

Down 10% at 22p - Guidance and Reserves Update - Mark (I Hold) - AMBER ↓

I’m a little disappointed with today’s guidance, and it is clear from the share price reaction that the market holds the same view:

2026 production guidance is set at 18,000-21,000 boe/d. Natural portfolio decline is expected to be offset by the positive impact of the PM323 infill drilling campaign, offshore Malaysia, which is due to commence near the end of Q1 2026 with first oil expected around mid-year.

2025 average production came in at 19,829 boe/d, so production is likely to end up flat year-on-year. However, costs are increasing form the $243m of 2025:

2026 total production costs of US$260-300 million, which includes additional costs relating to triennial subsea maintenance programs, costs associated with the five-yearly dry-docking of the CWLH FPSO, logistics contract renewals in Australia and costs deferred from 2025. With the confluence of these combined activities, the Group expects 2026 will mark a near-term peak in total production costs.

Revenues last year were over $400m, so they will generate an operating profit even with costs at the upper level of guidance, and they have reduced capex:

2026 capital expenditure of US$50-80 million. Approximately two-thirds of 2026 capex will be directed towards development activities primarily in Malaysia (with the upper end of the range reflecting a contingent PM323 well) and Vietnam, with a further ~15% at CWLH while the remainder is largely dedicated to ensuring and protecting reliability across the business.

This is partly because a planned infill well at their high-cost Montara is being postponed, since it is unclear what the payback will be in the current oil price environment. Indeed, cost overruns on a previous in fill well on this field have meant a reduction in FCF expectations:

In light of the 2026 guidance set out today, as well as the Group's preliminary expectations for 2027, the Group's unlevered free cash flow guidance for the 2025-2027 period is revised to US$200-240 million at US$70/bbl Brent.

This is down from $270m at this time last year.

The bigger picture:

This reduction in FCF expectations is disappointing. However, zooming out, there is still a possible investment case. Revenue - Production Costs - Capex for FY25 comes in at $52m, so that means FY26-27 should generate $148-$188m in FCF. The current market cap is $164m and there is $89m of net debt. While it may no longer be trading at a discount to expected FCF 2025-2027, you don’t have to assume much continued production to generate a positive economic return from here. Indeed the company says: “The 2P NPV10 of the Group's 2P reserves at end-2025 was US$519 million”.

This is down on the previous year, primarily due to reduced oil price assumptions, but it is still double the current EV.

Mark’s view

Given some of their production is high cost, the company is highly geared to the oil price: “Every US$10/bbl move in the underlying Brent assumption changes the 2025-2027 free cash flow guidance by ±US$90 million.” So it certainly won’t be a company that anyone who is bearish on the oil price will want to go near. However, there would seem to still be significant value for those who think the current oil price can strengthen from here.

When I looked at this in September last year, I updated our view to AMBER/GREEN following a return to accounting profitability with the shares at around 20p. While I don’t think today’s update changes the long-term valuation, the near term view has moderated, so I am doing the same with our view, and reducing it to AMBER.

Angling Direct (LON:ANG)

Up 10% at 55p - Full Year Trading Update - Mark - AMBER/GREEN =

Another good news story, with a second upgrade for the year:

The Board is pleased to report that the momentum experienced in Q3 continued into Q4 and it now expects to report Adjusted EBITDA of circa £4.8m, ahead of market expectations upgraded in October 2025.

This is largely a UK online story, with sales there rising 20%, and now making up 41% of revenue. UK retail store sales are up 11.1%, but it is also worth noting that LFL sales were a more modest 5.8%. This still isn’t bad considering the weak market conditions and that weather may not have been conducive to outdoor activities recently!

They opened six stores and closed one during the year. The costs of the store rollout and a small buyback are why cash continues to decline, reducing from £12.1m last year to £10.9m at 31 January this year. However, this seems to be significantly ahead of the £6.0m, their broker Singer had forecast for net cash excl leases.

Things are less rosy in Europe where the bulk of their sales are online. Here they say:

Outside the UK, the Group's European online sales decreased to £4.1m (FY25: £4.6m) as the Group maintained focus on its key markets of Germany and the Netherlands while continuing to balance market optionality and a forward-looking view of the likely returns in this area. Further progress was made in reducing European operating losses and positioning the operation for long-term profitable growth, with the ambition to build a sustainable European business while increasing our total addressable market.

One of the bull arguments for a number of years has been that the losses in Europe mask the underlying profitability of the UK operations. I think this is certainly true. However, giving them the benefit of this requires them being able to generate sustainable growth in Europe, or be willing to shut down this operation. They have so far been unable to do the former and unwilling to do the latter. With declining European revenue, I wonder if now is the time to rip off the bandaid.

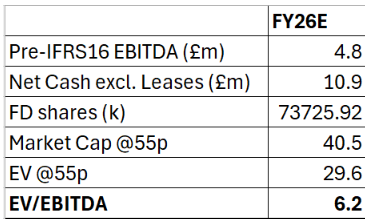

Forecasts:

I can’t see any updated coverage today. Last time their broker Singer upgraded their forecasts in line with the previous company guidance of “revenue of not less than £102.0m” and “adjusted EBITDA of not less than £4.35m”. The new figure of £4.8m is on a pre-IFRS basis, giving me the following:

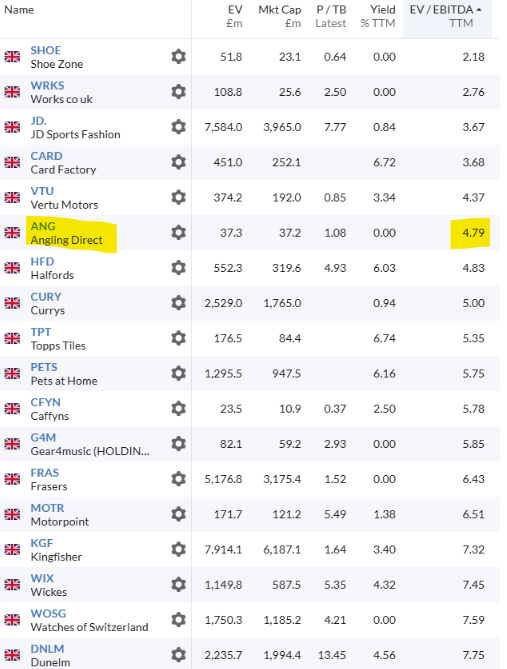

Without updates to forecasts, it is hard to estimate what this will look like as a forward valuation. There is little in the way of concrete outlook in this trading statement to guide us, either. The base case should probably be further modest UK growth as the store roll-out matures, making this look increasingly good value. It is at the lower end of the EV/EBITDA of the Specialty Retailers on a historical basis:

And should look even better value on a forward basis.

Mark’s view

Roland was AMBER/GREEN following the half year results. With the share price around the same level as it was then, and a further upgrade, it is tempting to be even more positive. However, the clear inability to generate growth in Europe plus the ever present risk of weather disruptions, and an unimpressive long term ROCE, are enough to keep my view the same.

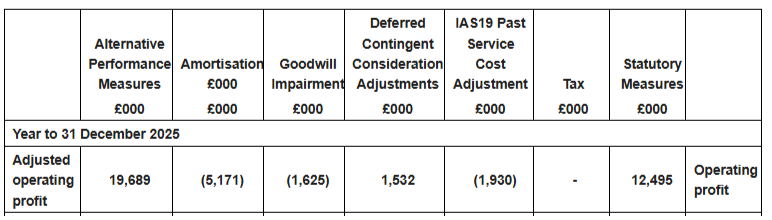

Macfarlane (LON:MACF)

Unch. at 71.4p (£112m) - Annual Results 2025 - Mark - AMBER/RED =

That these results would be poor is largely expected following multiple profits warnings recently:

There is a widening gap between the statutory and adjusted figures , though, which bears a closer look:

Amortisation will be non-cash. The Goodwill impairment is based on the issues at their Pitreavie acquisition where there was a recent fatality. I am assuming the deferred co-co adjustment is them making lower payments in light of this and largely offsets this value. Pension adjustments look to be genuinely one-off. So overall, I don’t see any major issues with these.

Balance sheet:

I’ve never found this to be the strongest of balance sheets. But they have operated with relatively low net working capital ever since I’ve been following them, without issues. The balance sheet has not stopped them using debt to make a number of acquisitions over the years. They don’t break out their payables into trade and acquisition-related figures in these accounts, and the figure has increased in line with revenue suggesting no major stress. However, it is worth noting that gross debt has gone up from £14.8m to £30.5m, versus a facility limit of £40m. With their facility classified as current, the current ratio has gone from 1.18 to below 1.

The company clearly doesn't feel under significant financial strain as they have maintained their dividend payout for the year, whereas brokers were forecasting a cut. This may be a good sign for a recovery. However, the balance sheet risk level has increased slightly here, in my opinion.

Outlook:

This is pretty downbeat:

In 2026 we anticipate markets and the competitive environment to remain challenging.

The company seem to suggest that it will be a H2-weighting, which often worries the market. Their broker, Shore, pick up on this saying:

FY26F outlook remains unchanged, with the market and competitive environment expected to remain challenging. However, management’s strategic and operational actions are expected to achieve benefits in H2. We leave our FY26F broadly unchanged, with adj. PBT of £16.2m (+4% growth yoy) and adj. dil EPS of 7.7p (+1% growth yoy, reflecting higher tax).

“Broadly” appears to be a 3% cut to FY26E Adj. PBT, with 5% taken out of FY27.

Acquisitions:

Historically the company has used their cash flow to make acquisitions and generate above average EPS growth for what is often a fairly mature pedestrian business. Perhaps understandably, these are off the table in the next year or so:

Management is focused on actions to improve the performance of Packaging Distribution, to recover the Pitreavie business and to continue the development of our specialist Manufacturing Operations…Whilst acquisitions are not anticipated in the short term, the Group continues to work on the acquisition pipeline for the future.

This is probably the right thing to do given the balance sheet and the issues they have had. However, the problem as I see it, is that it is during these challenging times that they should be able to get a bargain. Instead, they are stuck doing internal improvements until conditions improve, at which point they may have to pay more.

Mark’s view

Roland reduced our view to AMBER/RED following the profit warnings last year, something I agreed with when they issued a trading update in November. At the time, I suggested that acquisitions, which have been the main growth driver here, would be off the table. This has been confirmed today. With market conditions still described as challenging, this means that they will be unable to take advantage of market weakness by buying competitors. The rating is not expensive if they hit their EPS forecasts. However, with a weaker balance sheet, flat forecast EPS and a H2-weighting means my broadly negative view remains in place.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.