Morning!

Market Backdrop

After a pretty tumultuous couple of days in response to the events in the Middle East, I am expecting some calmer waters today with the FTSE opening up 0.3% at around 10480. The moves in equity markets have been dominated by risk-off sentiment rather than necessarily companies with Middle Eastern exposure. For example, the spot oil price has responded understandably positively to the Straits of Hormuz being closed, as 20-30% of global oil supply typically passes through there. In response, companies heavily reliant on energy as a core input have sold off, but many oil producers haven’t really responded positively. That oil producers don't immediately soar may be logical; the market may be pricing a rapid resolution to the current war and a return to normal over a relatively short time. However, that makes the sell-off in oil consumers illogical. We can’t have both. Which leads me to conclude we have simply seen investors run for the hills.

Nowhere has this risk-off attitude been more obvious than in some of the smaller companies. Even companies with high StockRanks and no exposure to the ME or oil have had a pretty brutal sell-off. This leads me to conclude that stop-losses may have had a part. These can be an important part of an investor's risk management process. However, in times like these, they should probably be renamed “Guaranteed Losses” instead of “Stop Losses”, as they tend to get triggered at the worst possible times. This is especially true if investors choose to use them on smaller, more illiquid stocks. Ed looked at the question of applying stops to the NAPS portfolio recently. They were no panacea. While drawdowns were slightly reduced, so were returns. So if you have bought high-quality companies that are cheap and have improving fundamentals, there seems little reason to panic sell now.

08:00 Summary complete

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Weir (LON:WEIR) (£8.83bn | SR70) | Revenue +6% to £2.565bn, Adj. Op Profit +15% to £518m, Adj. PBT +4% to £447m, Adj, EPS +3% to 123.8p. Net Debt £1,274m (FY24: £535m). “Looking ahead to 2026, I am encouraged by the strength of our business. Our market‑leading hardware portfolio and growing suite of software solutions position us to benefit from the long‑term structural tailwinds across the mining industry. " | ||

Beazley (LON:BEZ) (£7.73bn | SR66) | Insurance Premiums written -1% to $6.1bn, PBT -19% to $1.146bn, EPS -17% to 113.4p, NTAV per share £5.84. | PINK | |

Barratt Redrow (LON:BTRW) (£4.83bn | SR43) | Appointment of Dean Banks as next Group Chief Executive. He will join the Group in the final quarter of 2026 and succeed David Thomas who has decided to retire from the business after 11 years as Group Chief Executive and 17 years with the Group. | ||

Quilter (LON:QLT) (£2.62bn | SR88) | AuMA +18% to £141.2 billion reflecting net inflows of £8.7 billion coupled with a positive contribution from markets. Revenue +5% to £701m, Adj. PBT +6% to £207m, Adj. EPS +4% to 11.0p, Dividend +7% to 6.3p for the FY. | ||

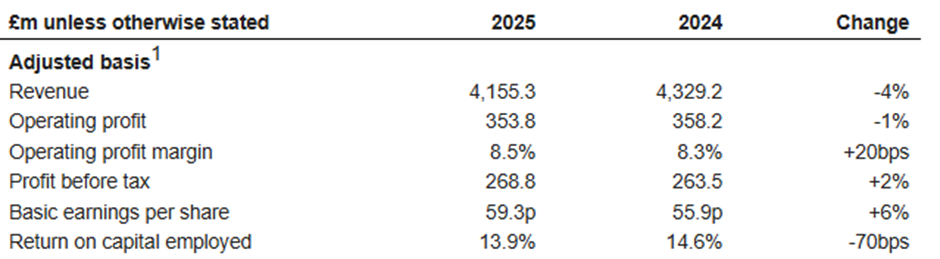

Vistry (LON:VTY) (£2.02bn | SR78) | Revenue - 4% to £4,155m, Adj. Op Profit -1% to £353.8m, Adj. EPS +6% to 59.3p, Net Debt £144.2m (FY24: £180.7m). “The Group expects to deliver good year-on-year revenue and volume growth, and an improvement in adjusted profit before tax in 2026, albeit with a lower overall margin reflecting the incentives offered during the current sales initiative.” | BLACK/AMBER = (Mark) While we don’t have access to broker coverage, it is clear that today’s outlook on margins represents a profits warning. Given this, the temptation is to now go for a reduced stance, instead of an improved one that we were previously mulling. However, the scale of today’s share price fall appears to exceed the size of the warning and puts the company trading well below tangible book value, despite them transitioning to an asset-light model where that tied up capital will be freed and eventually returned to shareholders. Today’s separate announcement that the Chairman & CEO (same person) will retire raises some questions about the speed and success of this strategic shift. However, I don’t see the fundamental tenets of this move being challenged. Hence I think it makes sense to keep our neutral stance. | |

Cairn Homes (LON:CRN) (£1.2bn | SR50) | Revenue +10% to €944.6m, Op Profit +12% to €168.6m, EPS +19% to 21.3c, Net debt €171.3m (FY24: €154.4m). Operating profit of c.€180 – €185 million (previously c.€175 – €180 million); | ||

Metro Bank Holdings (LON:MTRO) (£769m | SR48) | Net Interest Income +22%, Revenue +16% to £585.1m, u/l PBT £98m (FY24: £14m LBT), RoTE 6.4% continues to increase in line with guidance (2028 guidance to deliver greater than 18% RoTE). CET1 flat at 12.5%. EPS 7.8p, TNAV/share £1.63. | ||

Allergy Therapeutics (LON:AGY) (£741m | SR20) | The comprehensive panel of biomarkers of efficacy demonstrated the strong immunomodulating response which was highly consistent in all peanut allergic subjects after treatment with VLP Peanut | ||

Galliford Try Holdings (LON:GFRD) (£536m | SR95) | H1 Revenue +1.3% to £934.9m, Adj. Op Profit +225 to £21.6m, Adj. EPS +18.5% to 18.6p, Avg Month-End Cash £189.9m (25H1: £176.4m) | ||

Capita (LON:CPI) (£406m | SR83) | Has been selected to deliver the Synergy Business Process Services contract worth £370 million over 10 years starting March 2026, to deliver tech-enabled back-office services for public servants across four major UK government departments. | ||

Gulf Marine Services (LON:GMS) (£262m | SR91) | Received instructions from a client in the Middle East, in response to the ongoing situation in the Gulf region, to immediately evacuate personnel from four vessels operating under its jurisdiction as a precautionary safety measure. | BLACK/AMBER ↓ (Mark) | |

SRT Marine Systems (LON:SRT) (£194m | SR36) | New contract with a new sovereign customer to supply a national SRT-MDA System with a total value of US$261 million. | ||

Netcall (LON:NET) (£176m | SR51) | H1 Revenue +15% to £26.5m, Adj. EBITDA +13% to £6.45m, Adj. PBT +11% to £5.43m. Net Cash £14.8m (25H1: £20.9m). | ||

dotDigital (LON:DOTD) (£170m | SR56) | Alia, a US-based SaaS platform serving 2,700+ customers and forward-looking ARR in excess of $8m, acquired for an initial consideration of $30m, with a total maximum consideration of up to $60m dependent upon future performance. | ||

Pulsar Helium (LON:PLSR) (£148m | SR31) | Gas was encountered at 642m with a preliminary bottom-hole pressure of approximately 953 psi, indicating a robustly pressurized reservoir system at greater depth relative to previous wells. | ||

SIG (LON:SHI) (£115m | SR48) | LFL Sales flat at £2,591m, u/l Op Profit +28% to £32.1m, u/l LBT £20m (FY24: £14.3m loss), Net Debt £518.2m (FY24: £497.3m) | ||

Avation (LON:AVAP) (£85.7m | SR40) | Andrew Hiscock appointed as Chief Financial Officer, with immediate effect. | ||

MTI Wireless Edge (LON:MWE) (£49.1m | SR86) | Revenue +13% to $51.5m, PBT +12% to $5.41m, EPS +17% to 5.86c, Net Cash $9.4m (FY24: $6.0m). | ||

Ondo InsurTech (LON:ONDO) (£24.7m | SR2) | Rollout of LeakBot across Selective Insurance's 15-state Personal Lines footprint. | ||

Eenergy (LON:EAAS) (£19.7m | SR27) | £1.1m contract for supply and installation of solar PV systems for Unity Schools Partnership & £0.7m for supply and installation of LED lighting. |

* Market caps at previous trading day’s close

Graham’s Section:

Mark’s Section:

Surface Transforms (LON:SCE)

Up 20% at 0.11p - Major Customer Update: Loss of Contract - Mark - BLACK/RED

Just a brief comment on this one as it appears on the most viewed list, but after a 95% fall in the share price yesterday, it is way below our £10m cut-off.

The share price fall yesterday tells you it is really bad news:

The Company has been informed by General Motors ("GM") that it is re-sourcing its supply of brake disks with effect from 31st March 2026.

We knew they had customer concentration but I’m not sure this was ever revealed how concentrated they were:

GM is the Company's most significant customer and in FY 2025 formed £15.3m (84%) of revenues and 85% of discs sold and was under contract until 2030.

It seems likely that GM have finally lost confidence in the company to deliver brake discs at the agreed timing and price, which means they will almost certainly want their money back instead of brake discs:

Additionally, since November 2024 GM has provided the Company with operational support and financial assistance including advance payments of £14.4m.

Their last trading update revealed that they had £1m of gross cash and had £13.3m of customer pre-payments outstanding. They also had £9.1m of current debt at 30 June 2025. There was £17.1m of PP&E and £6.9m of inventory. However, as these appear to be furnaces, brake discs and raw materials to make brake discs that are no longer wanted by their major customer, these should have a large haircut applied in any valuation.

This means that I don’t see a scenario where GM gets all the money they lent them back, let alone any return to shareholders. Indeed, the use the word “stakeholders” here suggests where this is going:

The Company has not yet had the opportunity to speak directly with GM about the termination, but the loss of this contract has a material impact on the Company's ability to trade and as a result the Directors intend to immediately engage corporate restructuring advisers to protect stakeholder's interests.

Given the history of production problems and missed deadlines, which has led to almost 20 equity raises during the company’s life as a listed business, perhaps the only ones truly sorry to see them go will be those who work for their broker.

Mark’s view

It goes without saying that the chances of the company avoiding insolvency are slim, and the chances of shareholders receiving anything in these proceedings is similarly remote. RED

Gulf Marine Services (LON:GMS)

Down 12% at 20p - Regional Events - Mark - BLACK/AMBER ↓

This news is perhaps understandable, given what is going on in the world:

…received instructions from a client in the Middle East, in response to the ongoing situation in the Gulf region, to immediately evacuate personnel from four vessels operating under its jurisdiction as a precautionary safety measure.

However, what is surprising is that their contracts don’t protect against this:

GMS is continuing to monitor the situation closely and is currently working to quantify the potential impact of the recent developments on its operational and financial performance.

That they need to quantify this suggests that this isn’t immaterial, or only a customer problem. Any disruption may impact the company’s cash flow profile and ability/willingness to start making the long-awaited shareholder returns.

Their broker Zeus add some useful colour:

GMS is currently assessing the implications of the vessel personnel evacuation for its revenues, and the rates it will be able to continue to charge the client during this period of operational cessation. We would expect this to be subject to discussions with the client. We are not making any updates to our forecasts today, and note that existing 2026 company guidance has not yet taken account of any benefit from the new vessel acquisition announced earlier this year, providing some element of potential mitigation for any revenues lost elsewhere. We await further updates on vessel activities, and any change to full-year 2026 guidance.

So it seems that they will likely still get paid, but the rates may be lower, and subject to negotiation. At the moment four out of their 14 (soon to be 15) boat fleet are impacted, but I don’t think we can rule out some of the rest of the fleet being affected. As their corporate name suggests, the bulk of the fleet is based in the Gulf.

Their NTAV is of course unaffected by these events. However, I can’t help feeling shareholders would actually prefer Iran to blast a few of the ships out of the water (assuming that all personnel are safely evacuated and they are suitably insured)! I have been unconvinced by their recent strategy of starting to expand the fleet again, before they have got the debt fully paid down or begin to make shareholder returns.

Mark’s view

The share price has been strong this year, with shareholders extrapolating recent contract wins and extensions into a brighter outlook. The only major upgrade has come from the additional ship being added to forecasts, and we await their formal guidance for FY26:

If I held, I think I’d be tempted to take profits at this point.Unlike many recent fallers, this appears to face a genuine risk to operations and the disruption could have a negative impact on 2026 outlook, especially if other contracts in the region end up being affected.

Balancing this, I expect them to be paid during suspension of operations, just at a potentially lower rate, so it won’t be a serious impact, unless operations are suspended beyond expiry of contracts. And this remains a SuperStock:

Overall, world events increase the risk here and I think it is probably right to reflect that in a more circumspect view, until it is clear that missiles are no longer flying around the Middle East. AMBER

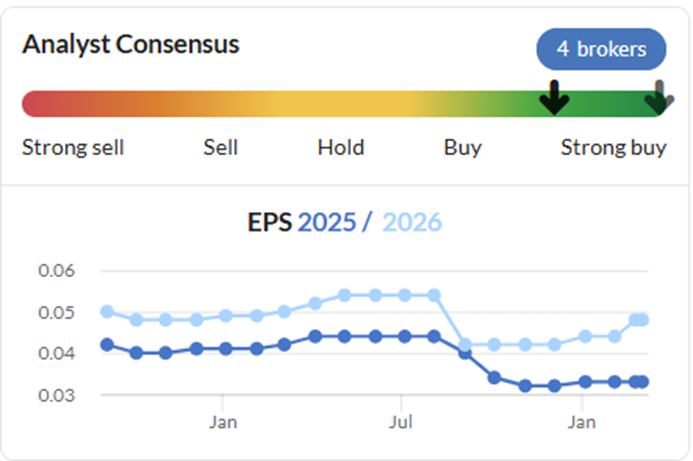

Vistry (LON:VTY)

Down 17% at 522p - Full year results for the year ended 31 Dec 2025 - Mark - BLACK/AMBER =

These results aren’t anything to write home about, with revenue down 4%:

But they aren’t terrible either, with adjusted EPS rising 6% and coming in above the 55.7p consensus in Stockopedia. (Sadly companies of this size don’t tend to use brokers who make their research publicly available so we can’t check directly.)

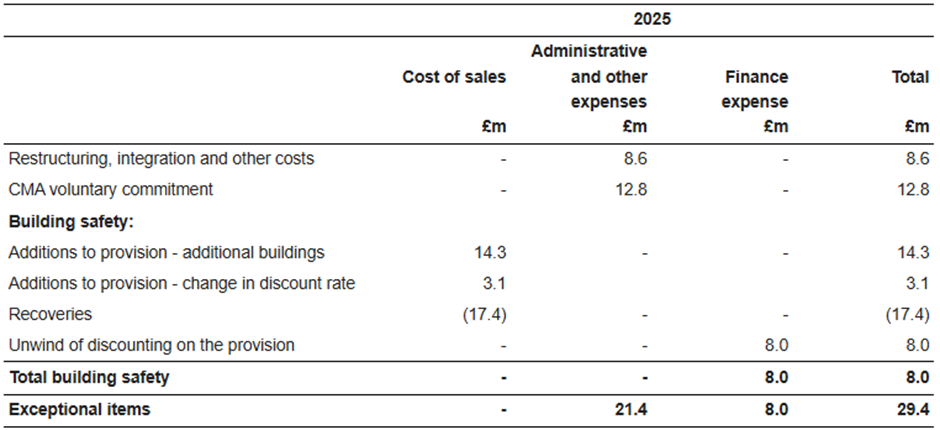

Adjustments:

There remains a large gap between adjusted and statutory figures. Exceptional items have once again proven to be less exceptional than one would have hoped for:

Building safety provisions appear to have netted off as they have already been provisioned for, but remain a cash drag. Restructuring costs are back, but perhaps less material than they would be elsewhere given the scale of the business. The CMA commitment at least seems one-off:

The Group, together with six other UK housebuilders, entered into a voluntary binding commitment in response to the potential concerns investigated by the UK Competition and Markets Authority (CMA). Under this commitment, the participating housebuilders will contribute £100m in aggregate to His Majesty's Government, to be allocated to programmes that fund and support the construction of affordable homes in England, Scotland, Wales and Northern Ireland. The Group's share of this contribution is £12.8m.

Outlook:

I don’t think any of these explain today’s share price weakness, which is focussed on the following guidance:

· The Group expects to deliver good year-on-year revenue and volume growth, and an improvement in adjusted profit before tax in 2026, albeit with a lower overall margin reflecting the incentives offered during the current sales initiative.

· The shape of profit delivery is expected to be similar to that in 2025. This is due to the greater margin impact of the sales initiative in the first half, and the step up in demand expected from the affordable housing stimulus in the second half.

Their focus on volume but at the cost of margin, means they expect profits to be flat on 2025. The StockReport shows expectations were for a 19% rise in EPS so this is undoubtedly a miss versus prior expectations, even if we can’t see the details. From secondary sources, it seems that Stifel expects this strategy to push down consensus profit forecasts by about 5-10%.

Balance sheet:

Things look better on this front with net debt declining to £144.2m from £180.7m the year before. However, as we find with an embarrassingly large number of companies, they shoot their buyback bolt prior to a profits warning, and then don’t have the capacity to renew it:

Remaining £29m of the current £130m share buyback programme to be completed, with no further capital distribution proposed on the back of the 2025 results in order to prioritise debt reduction. Future distributions to be reviewed at the half year.

This buyback is said to be in lieu of dividends, so the lack of extension perhaps means they don’t see any chance of a short-term improvement in trading.

Strategy:

Vestry has been undergoing a change of strategy over the last few years, with a focus on a partnership model. The idea is that it is moving away from traditional speculative housebuilding to focus on a high-volume, "capital-light" model centered on affordable, mixed-tenure housing. By removing the need to hold a large landbank, this should make the returns on capital much higher, and free capital for shareholder returns. That the buyback is not extended may be another sign that things aren’t moving as quickly as many would like in this area.

Vistry Group is trying to emulate the US-based homebuilder NVR, and its shareholder register is stacked with US funds that appear to have bought in to back this transition:

While progress is perhaps slower than many would like, there are signs that there may be progress, as they say:

In November 2025, Homes England issued bidding guidance under the £37bn 2026-2036 SAHP, confirming bids would be invited early in 2026. Vistry is well positioned to deliver at pace with Homes England, the Greater London Authority and our other partners, with the programme targeting 300,000 homes over its term. Bidding opened at the end of February for Homes England's part of the SAHP, and our bid is in the process of being submitted. We are hoping to have a high degree of visibility of Vistry's grant under the programme by the half year.

Vistry's current status as a Strategic Partner under the 2021–2026 programme suggests it is in a strong position to win significant business under the 2026–2036 successor programme. In September 2025, Vistry and Homes England launched Hestia, a £150 million joint venture designed to accelerate large-scale, mixed-tenure sites which aligns directly with the long-term goals of the new SAHP. So it would seem to be highly unusual for them not to play a major part in this programme.

CEO Retirement

The primary architect of the partnership strategy is Greg Fitzgerald, the Group's Executive Chair and CEO. He spearheaded the pivot in September 2023 to dismantle the group's traditional housebuilding arm and merge it into a single, partnerships-focused entity. So it is perhaps a little more worrying than usual that he:

...has informed the Board that he intends to retire from the Company. Greg's retirement will see the separation of the Chair and CEO roles.

This seems well planned with him remaining in the role “for up to 12 months, or until a successor is appointed.” However, you do have to wonder if he thought the strategy was about to really transform the company (and share price), why would he choose now to retire?

Mark’s view

When Roland reviewed the company’s trading update he made no change to our neutral view, saying:

Vistry’s move to a capital-light partnership model also has the potential to drive a re-rating as its capital requirements fall. With the shares now trading c.10% below tangible net asset value, I’m tempted to move up to AMBER/GREEN, but the group’s stubbornly daily net debt position means I’m going to maintain my previous neutral view for a little longer.

Given today’s profits warning, his caution looks warranted,and the temptation is now to go for a reduced stance, instead of an improved one. However, the scale of today’s share price fall appears to exceed the size of the warning and puts the company trading well below tangible book value, despite them transitioning to an asset-light model where that tied up capital will be freed and eventually returned to shareholders. Today’s separate announcement that the Chairman & CEO will retire raises some questions about the speed and success of this strategic shift. However, I don’t see the fundamental tenets of this move being challenged. Hence I think it makes sense to keep our neutral stance of AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.