Good morning! I had a chance to update our spreadsheet over the weekend, for anyone who likes to check our records.

I'm afraid I've run out of time for today. Thanks everyone. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£223bn | SR74) | Imfinzi (durvalumab) in combination with standard-of-care FLOT chemotherapy has been approved in the EU for early gastric and gastroesophageal cancers. | ||

TotalEnergies SE (LON:TTE) (£134bn | SR80) | Production is shutting down in Qatar, Iraq and UAE offshore, representing c.15% of the group’s total output. These barrels account for c.10% of Upstream cash flow. The majority of new production is due to come from outside the Middle East in 2026. This means that the benefit of higher prices should outweigh the loss of ME production. | ||

CRH (LON:CRH) (£51bn | SR56) | CRH Announces Intention to Delist from the LSE and Cancel Preference Shares | Further to the review announced in February, CRH has decided to delist from the LSE and maintain a sole listing on the NYSE, where it’s been listed since 2023. The last day of trading for CRH shares on the LSE will be 17 April 2026. CRH’s 5% and 7% preference shares will also be cancelled – full details in the announcement. | |

Scottish Mortgage Investment Trust (LON:SMT) (£13bn | SR n/a) | Shareholders will be asked to vote on permitting the Board “limited additional authority” to invest up to £250m (1.7% of total assets) of further investments in private (i.e. unlisted) companies. This will effectively extend the existing 30% limit on investment in private companies. This situation has arisen as a result of buybacks and the recent upward revaluations of some of SMT’s private investments, notably SpaceX – SMT’s largest investment. SpaceX accounted for approximately 15.1% of total assets on 31 Dec 25, up from 8.2% on 30 Nov 25. As a result, SMT’s ability to make further private investments is currently constrained. | ||

SEGRO (LON:SGRO) (£9.8bn | SR62) | Has signed an agreement to develop a powered shell data centre in Slough (30,000 sqm) and received planning permission for its first fully fitted data centres, which it’s developing with a partner in Park Royal, West London. | ||

| Standard Life (LON:SDLF) (£7.0bn | SR62) | 2025 Annual Financial Report | Operating cash generation up 5% to £1,474m, Capital Coverage Ratio up 4% to 176%. Adj operating profit up 15% to £945m, with total dividend up 2.6% to 55.4p. Outlook: “firmly on track across all 2026 financial targets”. | |

Derwent London (LON:DLN) (£1.86bn | SR71) | Network W1 (136,300 sq ft) has been fully let to Databricks, “a data and AI company” on a 15-year lease with a break at year to. The annual rent is £14.1m. “The London office market is entering a period of very low new supply while demand remains robust”. | ||

Sigmaroc (LON:SRC) (£1.37bn | SR76) | Revenue up 3.8% due to volume reduction, but adj pre-tax profit rose by 31% to £154m. Net debt down 7% to £472m (1.8x EBITDA). Outlook: “FY26 is expected to benefit from the German infrastructure stimulus and improving sentiment in selected end-markets, including steel and residential.” | ||

Great Portland Estates (LON:GPE) (£1.23bn | SR37) | Sale price gives 5.0% initial yield and price of £1,483 per sq ft, with annual rent of £9.2m and WAULT of 5.5 years. Valuation was “marginally ahead of the September 2025 book value and around 5% ahead of March 2025”. | ||

Craneware (LON:CRW) (£490m | SR40) | Launching buyback programme for up to $25m. “The Board believes that the current market price does not reflect the large addressable market opportunity of the Group or the strategic position the Group has within US healthcare”. | ||

| Marshalls (LON:MSLH) (£360m | SR60) | Final Results | Revenue up 2%, adj pre-tax profit down 16% to £43.7m. Dividend reduced by 16% to 6.7p. Landscape Products delivered 4% volume growth and market share gains, while Building Products delivered 4% revenue growth. Outlook: market activity in Jan/Feb was “consistent with the close of 2025”. There’s currently no clarity on the impact of the conflict in the Middle East. Excluding any adverse impact, full year expectations remain unchanged. | AMBER/RED = (Roland) [no section below] Marshalls shares have fallen by a further 15% since I commented on the company’s November trading update. Today’s full-year results appear to be in line with expectations (after three profit warnings last year) and the outlook for FY26 is also unchanged, with a caveat that events in the Middle East could have an adverse impact. The StockRanks view this as a possible Contrarian stock and I would like to upgrade to a neutral view. Unfortunately, I’m not quite convinced that this is justified by today’s results. Revenue growth was minimal and profit fell last year, while net debt excluding leases rose by 3% to £137.9m. This represents leverage of 1.8x EBITDA or more than four times adjusted net profit. That’s a little higher than I’d like for a low margin, capital-intensive and cyclical business. In today’s results, management also disclose the periodic usage of an invoice factoring facility with a key customer to help manage “short-term funding requirements”. We don’t know how this facility might have affected year-end net debt, but it’s possible that effective net debt is higher than reported today. If leverage was lower or the outlook a little sunnier, I might have moved back to a neutral view today. As things stand, I am going to remain cautious for a little longer. |

Avacta (LON:AVCT) (£313m | SR28) | This is the company’s second clinical program and the first sustained-release pre|CISION peptide drug conjugate. Preliminary safety and pharmacokinetic data is expected in the second half of 2026. | ||

SRT Marine Systems (LON:SRT) (£215m | SR42) | Revenue up 95%, pre-tax profit up 48% to £3.1m. £350m active contract order book from five sovereign customers, with a further £195m contract recently signed with a sixth customer that is pending activation. “The Board remains confident in the Group's ability to continue delivering progress in the second half and in the long-term prospects of SRT.” | AMBER = (Graham) I have some historical issues with the narrative that this company has attached to its results, and I continue to find these issues. Fortunately, I am under no compulsion to change our view from neutral. Most broker forecasts are unchanged today (in fact the EPS forecasts have been cut by 5% at Cavendish) and the StockRank is 42, with a ValueRank of only 15. | |

Cab Payments Holdings (LON:CABP) (£200m | SR48) | StoneX made an all cash proposal to the Board of CABP at 95p per share, a 32% premium to the “undisturbed” price on 30th January (the share price prior to takeover news going public). | PINK | |

Falcon Oil & Gas (LON:FOG) (£160m | SR31) | Further to update on 12 Mar 26, the transaction remains subject to a number of terms and conditions. These include approval by the Supreme Court of British Columbia – this is being opposed by one of Falcon’s shareholders. A Court hearing is now due on 24 Mar 26. If the transaction is not completed by 30 Mar 26, it may be terminated by either side. | ||

Liontrust Asset Management (LON:LIO) (£152m | SR86) | Acquiring River Global for all-share consideration of up to £9.7m. RGH had AUM of £2.7bn on 27 Feb 26, which would increase Liontrust’s pro forma AuMA to £24.4bn. 88% of RGH funds were first or second quartile performers over the last year. | ||

Beeks Financial Cloud (LON:BKS) (£130m | SR23) | Contract timing and move to a revenue share model for Exchange Cloud reduced H1 financial performance vs the prior period, but provide good visibility for H2. “...while contract timing and deployments with major organisations can be unpredictable, the growth in underlying recurring revenue and the current sales pipeline supports the Board's outlook of a full year performance in line with its expectations.” | AMBER/RED ↓ (Roland) Today’s half-year results reveal an H1 loss due to an unusually high lag between contract signing and revenue recognition. The result is that Beeks will need to generate 108% of this year’s forecast earnings in H2 in order to meet full-year expectations. In fairness, a heavy H2 weighting is normal for this business, so it may be deliverable. However, as I explain below I do have some concerns about visibility on full-year revenue and the underlying profitability of this business model. In my view there is now an increased risk FY26 results may miss expectations. For this reason and others, I have opted to take a cautious approach and downgrade our view by one notch today. | |

Team Internet (LON:TIG) (£97m | SR61) | The provisional results for FY25 are in line with previous guidance. The Board reiterates that the Group continues to trade in line with market expectations in FY26. | ||

Journeo (LON:JNEO) (£73m | SR73) | Strategically important contract with Danske Statsbaner, Denmark's largest state-owned passenger rail operator. Value is more than £0.6m. This is the first widescale on-train system contract secured by Journeo's Nordic subsidiary since acquisition in September 2023. | AMBER/GREEN = (Roland) [no section below] | |

Ten Lifestyle (LON:TENG) (£67m | SR72) | Expects to report H1 Net Revenue of c.£33.7m, up 6% (up 9% at constant currency). H1 Adjusted EBITDA is expected to increase by £1.0m to c.£7.0m (up 28% at constant currency). “We remain on track to deliver in line with the market's expectations for the full financial year.” | ||

System1 (LON:SYS1) (£27m | SR73) | Expects to report a performance for FY26 in line with guidance. “The strong level of new business wins secured throughout FY26 and particularly in the final quarter, provide a positive outlook for FY27… now expects FY27 Adjusted EBITDA to be materially ahead of current market forecasts, with an Adjusted EBITDA margin of no less than 15%...” | AMBER/GREEN ↑ (Roland) Following the recent sale of founder John Kearon’s stake to Brave Bison (LON:BBSN), System1 has now announced a significant upgrade to FY27 guidance. While revenue expectations remain fairly flat for the year ahead, profit expectations have doubled, seemingly reflecting cost savings and improved operational leverage following recent internal changes. Today’s upgrade comes just six months after a major profit warning. I would like to see more consistency here and would also like to see evidence the business can expand its revenue base. However, I think today’s upgrade and the resulting P/E of 10 are probably enough to justify a broadly positive view, so I’ve moved up one notch to AMBER/GREEN today. | |

Satsuma Technology (LON:SATS) (£26m | SR0) | Following discussions with shareholders, the Board has agreed to appoint two proposed Directors as NEDs and to adjourn the requisitioned General Meeting. | ||

Wishbone Gold (LON:WSBN) (£20m | SR10) | Results from the Company's 2025 drilling campaign confirm the presence of gold and copper mineralisation within the Red Setter diorite trend, which extends for approximately 4 kilometres. These assay results further support the potential for the project to host a large-scale mineralised system. | ||

DSW Capital (LON:DSW) (£14m | SR81) | The outbreak of war with Iran has severely impacted M&A activity in the UK, with many deals the Group expected to complete in March being aborted or postponed. The board now expects to report Total Income of c.£6.2m, Adjusted EBITDA of c.£1.6m and Adjusted profit before tax of c.£1.3m for FY March 2026. | BLACK | |

Zinc Media (LON:ZIN) (£10m | SR30) | The BBC has commissioned two major geopolitical documentary series from ZIN’s award-winning factual label, Brook Lapping. | ||

Croma Security Solutions (LON:CSSG) (£10m | SR69) | Completes the acquisition of Southern Security Services Limited, an established electronic security and specialist locksmith business based in Poole, Dorset. Consideration £0.55m. Includes a freehold property valued at £0.4m. |

Graham's Section

SRT Marine Systems (LON:SRT)

Up 4% to 88.75p (£223m) - Half Year Report - Graham - AMBER =

SRT, the AIM-quoted developer and supplier of sovereign civil defence maritime surveillance systems, and navigation safety devices, announces its unaudited interim results for the six months ended 31 December 2025 (the "Period").

There was positive news from SRT recently, with the announcement that allegations of corruption in the Philippines had been formally dismissed.

This is a company which has produced many false dawns for investors, over many years. Historically, I had a strong dislike for how it talked about its order pipeline - a number that never seemed to have much connection to reality.

More recently, however, the pipeline has at last converted into strong orders, and I’ve been very keen to see how these orders would convert into real profits.

There are two divisions.

Navigation safety transceivers. This provides “a consistently profitable base for the group.”

“Systems” - civil defence maritime intelligence systems for governments, which is “on a rapid scaling trajectory”.

Today’s half-year results (to December) are as follows:

Revenues +95 (£51.1m)

PBT +48% (£3.1m)

The “active project order book” is £350m. Checking last year’s half-yearly report, the “forward project order book” was £320m a year ago.

The company doesn’t compare this year’s £350m figure directly to the £320m figure given last year. I think this might be the reason:

We now have five sovereign customers, with approximately £350m of active contracts under implementation, of which £123m of revenues have been realised, leaving a net £227m to be delivered as this phase of contracts complete.

So in other words, the £350m is not a forward-looking order book at all. It sounds like £227m is a much more realistic measure of what most of us would consider to be the current order book.

Cash increases year-on-year from £22.4m to £41.6m - this also requires further investigation. The cash flow statement (or more specifically, a footnote attached to the cash flow statement) shows a £12m decrease in receivables in H1, i.e. there’s a £12m cash flow boost from customers paying down their invoices.

Also from the cash flow statement, I can’t help noticing that the company’s payables balance has increased to £58m, compared to just £22m a year ago.

In other words, there’s been a £36m cash flow boost from this working capital item over the past year.

Checking the annual report for the year to June 2025, I see that the overwhelming majority of the movement here was thanks to customers paying for goods and services upfront (“contract liabilities”, within “accruals and deferred income”).

Therefore, despite a profit of only £3m over the past six months, the c. £20m increase in the cash pile can make sense: customers are both paying upfront for work not done yet, and catching up on invoices for work already done.

Turning back to today’s highlights, they mention a contract they first announced last month:

£195m new contract with new (sixth) sovereign signed post period end, pending activation. £1.8bn of further validated new system contract prospects from new and existing customers. Five active sovereign customers and systems.

The £1.8bn “validated new system contract prospects” is the type of number I criticised SRT for publishing in the past.

However, the actual £195m contract is a different story, although it is apparently “pending activation”. When a customer puts pen to paper, it becomes “real” rather than what I would consider to be a value promise or a hope.

Comment by long-standing CEO Simon Tucker:

"Our business continues to accelerate in line with the growing global market for, and interest in, maritime domain awareness. Today's results reflect our strategic first-mover advantage and years of sustained investment in technology, products, people and market development, which have positioned SRT as a market leader that the market and our customers trust for their growing MDA requirements. I look forward to continued growth in the second half and in the years ahead."

Profit margins - some observations

Gross margin was 27%, “lower than in the prior comparative period, due to the type-mix of system deliverables completed during the period”.

The company doesn’t mention what the previous gross margin was, so I’ve calculated it myself. It looks like it was 46% in H1 last year.

This isn't really a problem - shareholders aren't going to complain about a nearly 50% increase in PBT - but it’s important to highlight that this is looking a much lower-margin business than it was before.

In fact, the contrast in performance becomes even more stark if we look at operating profit.

In H1 last year the operating profit margin was 13.7% (£3.6m profit on £26.2m of revenue).

In H1 this year? 7.3% (£3.7m profit on £51.1m of revenue).

So operating profit has only increased by £0.1m, despite revenues almost doubling.

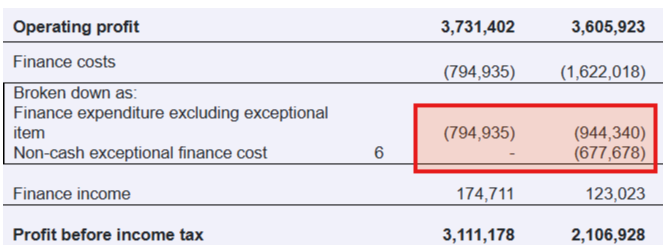

When you look at it through that lens, the real reason for the increase in PBT is lower finance costs.

This table shows the most recent H1 on the left-hand side, with the previous year’s H1 on the right-hand side:

Total finance expenditure, including an exceptional finance charge, was almost £1m higher last year. If that had been repeated in the current year, there would have been no increase in PBT, despite all the increased revenues.

Estimates

Many thanks to Cavendish for publishing on SRT today. They have reiterated most of their FY26 forecasts despite the new £195m contract that was announced last month.

FY26 forecast are as follows:

Revenue £115.8m (+48%)

Adj. PBT £10.2m (+98%)

They reduce adjusted EPS forecasts by 5%, due to new estimates of share dilution.

Graham’s view

I’m a little biased here by my history of studying this one - I may not be able to look at it with “fresh eyes”.

I don’t like saying it, but I’ve never had complete trust in the commentary attached to its reports, and that remains the case today.

For example, there is the use of the distinction between “active project order book” and “forward project order book”.

There is the focus on unadjusted PBT this year, whereas last year there was a focus on adjusted PBT.

Last year, the company highlighted PBT before its exceptional finance charge.

This year, when there was no exceptional finance charge, the company focused on statutory PBT (making for an easier year-on-year comparison).

For these reasons, I’m not inclined to upgrade our stance here. The StockRanks do back me up on this, not seeing much Value or Quality:

So I’m neutral on this. I’m still very much intrigued to see what SRT will do next, and there is every chance that it succeeds for its shareholders - but from a personal perspective, I have to be honest that it does not appeal to me.

Roland's Section

System1 (LON:SYS1)

Up 22% at 258p (£33m) - Trading Update - Roland - AMBER/GREEN ↑

This morning’s brief trading update from this “marketing decision-making platform” has made System1 one of the top three risers on the UK market today. It has also prompted an early broker upgrade for the FY27 financial year, which starts on 1 April.

“Record H2 revenue” - here are the main points:

After a challenging H1, Q3 momentum continued into the final quarter.

Management expects to report “record H2 revenue and a performance for FY26 in line with guidance”.

New business wins secured throughout FY26 “provide a positive outlook for FY27”.

Recent cost savings and restructuring activities have included “changes to the Group's organisational structure, sales incentivisation and go-to-market approach”.

These changes are expected to support “greater operational leverage” as revenue growth accelerates.

Operational leverage refers to the impact of changing revenue on profits. Businesses with a high proportion of fixed costs, such as software companies, can see profits rise much more quickly than revenue. Today’s updated guidance suggests this is expected to happen – in quite a big way – in FY27.

Outlook

… the Board remains comfortable with consensus Revenue forecasts for FY27 but now expects FY27 Adjusted EBITDA to be materially ahead of current market forecasts, with an Adjusted EBITDA margin of no less than 15% and the opportunity for further margin expansion as revenue scales.

Updated forecasts

FY26 results are expected to meet revised (downgraded) company guidance previously announced in September:

FY26 revenue: £37m

FY26 adjusted pre-tax profit: £2.0m to £2.5m

FY26 EPS estimates: it’s worth flagging up here that the FY26 EPS forecast of 22p on the StockReport appears to be stale – Canaccord and Singer Capital have FY26E EPS estimates of 11.6p and 11.0p respectively following September’s profit warning.

FY27 broker estimates:

Previous consensus expectations were for FY27 revenue of £38.8m and adjusted EBITDA of £4.3m.

With thanks to broker Canaccord Genuity, we have access to updated forecasts through Research Tree this morning:

FY27E revenue: £39.1m.

FY27E adj EBITDA: £6.0m (prev. £4.1m).

FY27E adj pre-tax profit: £4.5m (prev. £2.7m).

FY27E adj EPS: 24.9p (prev. 14.8p).

Operational leverage refers to the impact of changing revenue on profits. Businesses with a high proportion of fixed costs (often software companies) can see profits rise much more quickly than revenue.

Canaccord’s updated forecasts reflect today’s guidance from the company – even though revenue is only expected to rise by 5% in FY27, pre-tax profit is expected to double, compared to previous forecasts for c.20% growth.

These estimates price System1 shares on a forward P/E of 10 at the time of writing – potentially quite cheap if the company can start to deliver consistent year-on-year growth.

Brave Bison investment & founder departure: I can’t discuss System1 today without also mentioning a recent change to its shareholder base.

On 2 March, System1 founder John Kearon announced the sale of his 23% stake to Brave Bison (LON:BBSN), a business we’ve covered a number of times over the last year. Kearon has now also stood down as a director of System1.

This sale came shortly after the company announced on 30 January that a Board committee chaired by Kearon to “provide strategic guidance, challenge and oversight” to the business had been scrapped.

Kearon appears to have swapped his 2.9m System1 shares for 9.8m new shares in Brave Bison, issued at 74p.

This deal gives an implied value of 248p per System1 share for Kearon’s holding and gives System1’s founder an 8.74% holding in Brave Bison.

Alongside this transaction, Brave Bison also spent £1.3m buying System1 shares in the market.

The acquisition of Kearson’s stake means Brave Bison now has a 27.96% holding in System1, at a blended average price of 241.8p. It looks like the company intends to play an active role in improving System1’s performance:

Brave Bison is supportive of the strategy presented by the board of System1 at the company's capital markets day in October 2025 and, where possible, intends to provide support in the execution of this plan.

Roland’s view

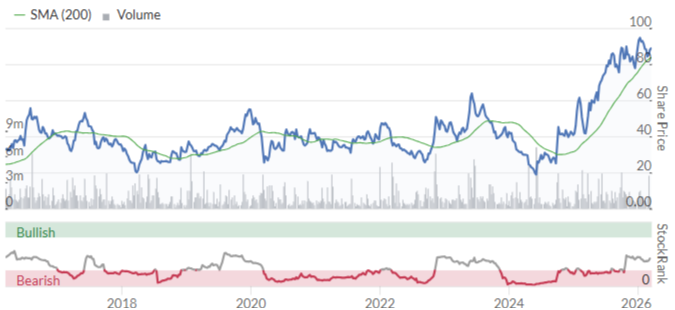

A dire lack of consistency has been a big issue for System1 (and its shareholders) in recent years. Despite seemingly exciting potential to develop a market-leading advertising testing platform, profits have swung around wildly and revenue growth has often been disappointing:

This has been reflected in a frustrating share price chart – the stock remains 65% below its 2024 highs:

Today’s remarkable upgrade also comes only six months after a major downgrade to FY26 and FY27 forecasts:

All of this suggests to me that management has consistently struggled to maintain new business momentum and generate visibility on forward sales.

Today’s comments about operational changes suggest to me System1 may finally be moving closer to its long-term ambition of becoming a true software platform, rather than a hybrid consultancy/software business.

We’ll need to see the full-year results to be sure, but the projections of improved profitability shared by the company’s broker this morning seem encouraging to me.

The presence of John Kearon on System1’s board never seemed to have the positive influence other shareholders might have hoped for. Perhaps Brave Bison – which itself has strong boardroom ownership – will be able to deliver better results.

Mark was AMBER on System1 in September when the company warned on profits. I would also like to see a more consistent track record of delivery here.

However, I think it’s fair to upgrade our view given today’s material profit guidance upgrade and the stock’s seemingly reasonable valuation. AMBER/GREEN.

Beeks Financial Cloud (LON:BKS)

Down 10% at 171p (£117m) - Interim Results - Roland - AMBER/RED ↓

Beeks Financial Cloud Group Plc (AIM: BKS), a cloud computing and connectivity provider for financial markets, is pleased to announce its unaudited results for the six months ended 31 December 2025.

Today’s half-year figures from Beeks look a little mixed to me, with solid revenue growth offset by a loss-making performance for H1. Although full-year expectations are left unchanged, I’m not sure the market was expecting an H1 loss.

Here are the main figures:

Revenue down 7% to £14.65m.

Annualised Committed Monthly Recurring Revenue (ACMRR) up 15% to £32.8m.

Total Contract Value of new contracts signed in H1 up 23% to £11.9m

Gross profit down 25% to £4.5m.

Underlying EBITDA down 28% to £4.12m.

Underlying pre-tax loss of £(0.69)m (H1 2025: £1.89m profit).

Underlying EPS: -0.68p (H1 2025: 2.61p).

Cash flow from operations before working capital movements down 24% to £4.37m.

Net cash: £3.29m (H1 2025: £6.57m).

According to the company, the disconnect here is that a number of new contracts signed late in H1 will start to deliver revenue recognition in H2. This is expected to drive a strong H2 revenue performance and a return to profit.

It’s worth remembering that Beeks is increasingly shifting to revenue share contracts, meaning the company has to outlay initial cash on equipment to support new contracts before generating a share of revenue in the future.

The company remains confident about the longer-term potential for this business model (my bold):

Seven exchanges globally have now signed for our Exchange Cloud® offering, four of which are under the revenue share model. While this model typically results in lower upfront deployment revenue, while still incurring set up costs, we expect it to deliver greater revenue in the medium term than the prior model, as client engagement scales. Even at an early stage, this model has delivered ahead of our ambitions. It has successfully shortened sales cycles, but crucially, the live sites are transitioning into monthly profitability ahead of our anticipated timeline, paving the way for increased profitable revenue growth in future years.

Unfortunately, the first half of the current year saw a more extended lag between contract signing and revenue recognition than usual. No explanation for these delays are provided today, so we don’t know if this lag will remain an issue with future new wins:

During H1 FY26 this lag was more pronounced than usual, resulting in a lower level of revenue recognition in the first half. The majority of these deployments have now been completed, positioning the Group to recognise the associated revenue streams in the second half of the financial year.

The short-term impact of this situation is that financial performance worsened in H1 as Beeks invested in new contracts before being able to bill anything to its clients:

On the income statement, operating expenses rose by 15% to £6.4m during the period, despite revenue falling 7%.

The impact of past capital expenditure was also evident – Beeks’ depreciation charge for the half year rose by 25% to £3.4m (H1 25: £2.7m). High-end server equipment needs regular replacement.

On the cash flow statement, operating cash flow fell to reflect lower revenue and weaker gross margins, but spending on property, plant and equipment (presumably mostly hardware and software) rose by 166% to £3.2m. That’s 70% of the total PP&E expenditure for the previous year.

Capitalised software development was also significant, at £1.1m (H1 24: £1.4m). This is largely a cash outflow on salaries and other expenses, even though it bypasses the income statement.

Finally, the balance sheet shows lease liabilities rising to £7.1m (FY24: £5.9m, H1 24: £2.0m). Beeks drew down £1.5m of debt in H1 to “fund deployment” of recent wins while still maintaining a good level of cash liquidity.

As a result, gross cash was stable at c.£7m but net cash halved to £3.3m.

Outlook - H2 performance is critical: I am not going to delve too deeply into the H1 accounts. What matters is whether the expected H2 revenue growth will be delivered and whether it will convert to the expected level of profitability.

Here is an outline of how I see the numbers on revenue, based on today’s results and guidance:

H1 revenue: £14.7m.

Half-year run-rate revenue implied by today’s ACMRR figure: £16.4m.

“H2 FY26 revenue will be supported by c.£4.5m of revenue recognition from contract wins secured towards the end of H1 FY26 [and certain other recent contracts].

My estimate of pro forma total FY26 revenue = £35.6m

Consensus forecast FY26 revenue of £40.3m

In February, I said I felt there was still a shortfall of around £4.5m in revenue needed to meet full-year guidance. As far as I can see that situation is still unchanged today.

In my view, today’s outlook statement from CEO Gordon McArthur ackonwledges this, suggesting full-year expectations are still linked to further conversions from the sales pipeline:

Momentum has continued in H2 FY26 with multiple significant contracts in discussion across the Group's offering. While the timing of deal signature can be hard to predict, the current sales pipeline supports the Board's outlook of a full year performance in line with its expectations.

Updated broker estimates

With thanks to both Progressive Research and Canaccord Genuity we have confirmation today that expectations are unchanged:

Canaccord: FY26E revenue £41.0m / adj EPS: 8.9p

Progressive: FY26E revenue £39.5m / adj EPS 8.2p

Averaging these estimates gives figures of £40.3m and 8.55p, matching the consensus shown on the StockReport and putting Beeks on a FY26E P/E of c.20.

Roland’s view

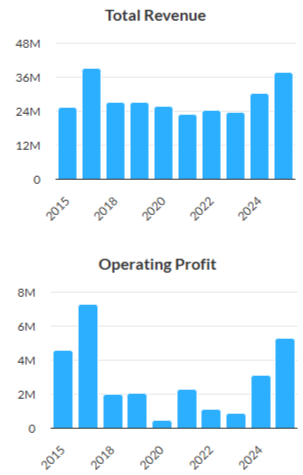

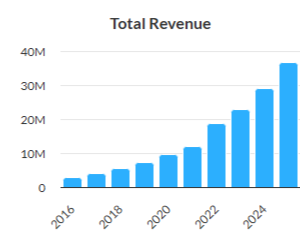

It’s worth noting that Beeks does have a long and quite impressive record of revenue growth. The group’s business of providing data centre space that’s close to major financial centres has demonstrable advantages and demand only seems likely to grow (although I have not researched possible competitors):

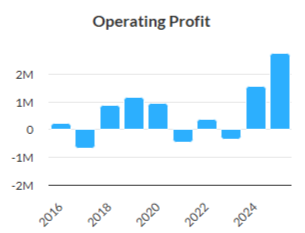

Profit growth has been less consistent, but growth has resumed over the last couple of years:

CEO Gordon McArthur owns 30% of the business, so his interests should be well aligned with those of shareholders.

However, I do have some concerns.

Extreme H2 weighting: Beeks typically reports a heavy H2 weighting to profit – the last two years have seen operating profit split roughly 20/80. However, the H2 weighting required to meet FY26 forecasts is 108% – Beeks needs to erase the H1 loss and generate 100% of full-year profit.

I might be more confident if I believed the company had full visibility of the revenue needed to meet FY forecasts, but I’m not sure this is the case.

I’d also prefer to know that the cause of the revenue recognition “lag” reported for H1 had been resolved, or at least explained to shareholders.

Despite today’s in-line guidance, I can’t help feeling that there is still some risk of a profit warning before the financial year ends in June.

More generally, my experience is that tech companies transitioning to new revenue models sometimes suffer a longer-than-expected period of underperformance before the benefits of the new model are felt. I wonder if that could be the case here.

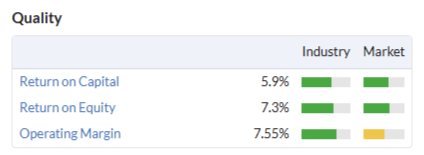

Profitability: my second concern is a long-running issue that I and my co-writers have often flagged up – Beeks simply isn’t very profitable. It seems to have the economics of an equipment leasing business, rather than a software company:

The hefty increase in capex and depreciation indicated by today’s results doesn’t change my view that this business may not have the attractive tech-style quality characteristics that are suggested by its valuation.

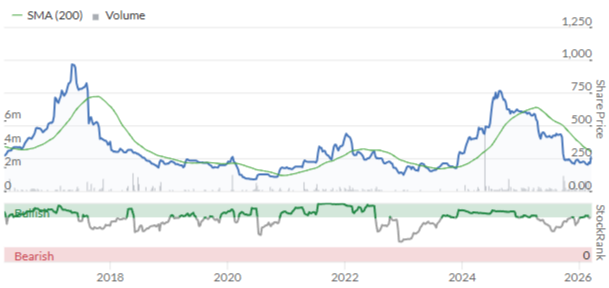

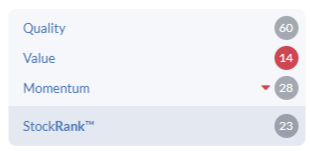

In short, I think the shares look expensive – a view the StockRank algorithms seem to share:

Momentum: my final concern is that the StockRanks currently view Beeks as a Falling Star – a losing style associated with quality stocks that are falling out of fashion.

Having been badly burned by some Falling Stars in my own investing, I’ve learned to treat this style with respect. Beeks’ very low StockRank does not give me much confidence in the quantitative picture.

Verdict: I accept that I may be missing the longer-term opportunity, but holding stocks with negative characteristics can also carry a significant opportunity cost in the shorter term. I would prefer to wait until Beeks was cheaper or more profitable before considering an investment.

For all the reasons outlined above, I am going to move our view down by one notch to AMBER/RED today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.