Good morning and welcome to Friday's report.

Update: I've added a section on DFS from the backlog.

That's all we have time for today - thank you for all your comments this week. I hope you enjoy the weekend.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Unilever (LON:ULVR) (£100bn | SR57) | Confirms press speculation that the company has received an inbound offer for its Food business and is in discussions with McCormick & (NYQ:MKC). | AMBER/GREEN = (Roland - I hold) Today’s news continues a run of media speculation this week about a possible disposal of the Food business. As a shareholder, my view is that this would probably be neutral or positive for the business, so I’m leaving my view unchanged today. | |

Smiths (LON:SMIN) (£7.3bn | SR65) | Agreed sales of Smiths Interconnect and Smith Detection for a total of £3.3bn. A further £1.5bn shareholder return will begin following the completion of the Detection sale later this year. Updates FY26 guidance to reflect sale of Smiths Detection; now expects organic revenue growth of 3-4%, with H2 growth of 5-7% and operating margin of c.20%. | ||

Gamma Communications (LON:GAMA) (£790m | SR60) | Appointed Damien Maltarp as CFO. He joins from LSEG and previously BT. Maltarp will join “at the latest in September 2026” - the current CFO is leaving at the end of March. The CEO will provide oversight of financial operations in the interim. | ||

J D Wetherspoon (LON:JDW) (£685m | SR43) | H1 like-for-like sales up 4.8%, revenue up 5.7%. Adjusted pre-tax profit down 31.9% to £22.4m. Wetherspoon has outperformed industry index but warns that cost pressures and consumer affordability may result in profits that are slightly below current market expectations. | BLACK (AMBER/RED =) (Roland) Today’s profit warning follows on from downgrades during the autumn and in January. While the valuation has become more modest, so has Wetherspoon’s profitability. I’m leaving our broadly negative view unchanged until some signs of stability emerge. | |

SDCL Efficiency Income Trust (LON:SEIT) (£493m | SR n/a) | Sale of a portfolio of assets to Kyotherm for up to c.£105m, a discount of c.9% to Sept 25 book value. This is expected to result in a c.1.2p reduction in NAVps. Day-one cash proceeds are expected to be c.£84m. This will be used to reduce debt, bringing pro forma gearing to c.65%. No change to FY26 target dividend of 6.36p. | ||

Cab Payments Holdings (LON:CABP) (£229m | SR46) | The Board has rejected the StoneX possible offer of 95p on the grounds that it “significantly undervalued CAB Payments”. | PINK | |

Atlantic Lithium (LON:ALL) (£142m | SR22) | Parliament of Ghana has ratified a 15-year Mining Lease for the Ewoyaa Lithium Project. Agreed royalties will apply from 5% to 12%, depending on Spodumene pricing. The lease allows the company to advance discussions re. funding and move towards a final investment decision. | ||

Smarter Web (LON:SWC) (£136m | SR18) | CFO Albert Soleiman has resigned with immediate effect and will step down following a handover period. He is thanked. The current Financial Controller and Head of Projects (& former CFO) will become interim CFO. | ||

Strategic Minerals (LON:SML) (£132m | SR43) | Metallurgical study shows a 19.2% increase in WO3 overall recovery to 85.8%. Recovery of silver has also been confirmed. | ||

Taylor Maritime (LON:TMI) (£113m | SR98) | Plans to undertake a further return of at least $30m in Q2 2026 by way of a partial compulsory redemption of shares. Company says a previously agreed $17m vessel sale has now been completed and confirms that it intends to continue the managed realisation of the company’s assets. | ||

Arrow Exploration (LON:AXL) (£64m | SR72) | Mateguafa 11 (M-11) well has been drilled to a total measured depth of 11,455 MD feet and has encountered oil bearing sands in the C7 and C9 Carbonera formations. Corporate production is approx. 5,325 boe/d. M-11 is expected to contribute additional production. New reserves report shows 10% reduction in 2P reserves to 20,102Mboe. | ||

Zenith Energy (LON:ZEN) (£42m | SR39) | Acquired additional agrivoltaic development project in Lazio, Italy, with an installed capacity of c.10MWp. Total consideration is €1.02m. | ||

Works co uk (LON:WRKS) (£23m | SR74) | Plans to cease trading online immediately; its website will become “non-transactional”. £2m of closure costs. Upgrades FY26 and FY27 EBITDA guidance for continuing operations to £13.5m and £15m respectively (previously £11m and £12.7m). | AMBER/GREEN ↑ (Roland) The company makes a simple and compelling case for shutting down its online sales and upgrades forward profit guidance as a result. Given the modest valuation and positive sales trends prior to today, I think it’s fair to upgrade our view by one notch. | |

Sound Energy (LON:SOU) (£18m | SR28) | Tendrara Gas Gathering Systems has been fully tested and commissioned. Entered into €1.3m term loan with 20% interest per 120 days to provide working capital prior to revenue from LNG sales from Tendrara. Also raised €0.5m in a placing at 5.0p per share (37.5% discount to last closing bid price). | ||

Ground Rents Income Fund (LON:GRIO) (£17m | SR9) | Sold freehold ground rent interests in Manchester and Southampton for a combined price of £4.58m. This represents a 0.6% discount to independent valuation and 5.3% net initial yield. Proceeds used to repay a secured loan. Further disposals are progressing. | ||

Power Metal Resources (LON:POW) (£15m | SR57) | Investing $1m for 2.6% in Next Minerals S.A., a Chile-based copper mining company. Deal provides exposure to the “mine-ready Comahue underground copper mine” in the Antofagasta region of Chile. | ||

Plexus Holdings (LON:POS) (£9m | SR20) | Received orders from a UKCS operator that “will lead to about £1.5m of work” under the recently announced framework agreement (13 Nov 25) for rental wellhead services. Revenue is expected over a 12-month period, subject to rig scheduling. |

Roland's Section

Unilever (LON:ULVR)

Up 1.3% at 4,631p (£101bn) - McCormick & Co - Response to media speculation - Roland - AMBER/GREEN =

(At the time of writing, Roland has a long position in ULVR.)

News that Unilever is considering a sale of its entire Food business (including Hellmann’s, Marmite and Knorr) probably shouldn’t be a complete surprise.

The group has already spun out its ice cream and spreads businesses in recent years. CEO Fernando Fernandez has made it clear his focus is on expanding the faster growing and high margin Personal Care and Beauty operations.

Here’s what we know about this story so far:

Tuesday 17 March: Bloomberg reports that Unilever is considering the separation of its food business.

Wednesday 18 March: The FT reports that Unilever has held discussions with Kraft Heinz Co (NSQ:KHC) on a “megamerger of their food brands”.

Thursday 19 March: Unilever confirms that the company has received “an inbound offer” for its Foods business from US food group McCormick & (NYQ:MKC).

Unilever confirms that it has received an inbound offer for its Foods business and is in discussions with McCormick & Company, Inc. There can be no certainty that any transaction will be agreed.

Talks appear to be at a fairly early stage and Unilever’s management is careful to tell us how much they still like the Food business:

The Board believes Foods is a highly attractive business, with a strong financial profile led by market-leading brands in growing categories and is confident in the future of the Foods business as part of Unilever.

Roland’s view

Unilever’s business has always been distinguished by its heavy exposure to emerging markets, where competitive pressure from cheaper supermarket own brands is lower and the power of food brands is still stronger.

Even so, I think there’s no avoiding the direction of travel in this sector. While my household still purchases Marmite and Persil, there’s no doubt our kitchen contains more supermarket-branded food products than it did in the past. That’s less true in the bathroom cupboard, perhaps providing anecdotal support for the group’s strategy.

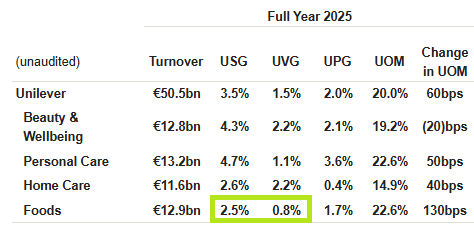

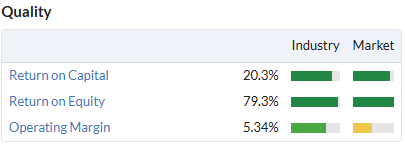

Unilever has also already disposed of some of its lower-quality and slower-growing food operations. The remaining Food business generated an attractive 22.6% operating margin last year, but was still the slowest-growing part of Unilever’s business when measured by revenue or volume growth:

Estimates from analysts at Jefferies quoted in the FT today have suggested the Foods business could command a valuation of $36-37bn.

Selling such a large element of the business would leave the group looking very different. However, given that McCormick is a much smaller business (market cap c.£11bn) I wonder if the deal might be structured as a reverse merger, leaving Unilever shareholders (once again) with a stub of shares in the spun-out entity.

This is all speculation for now – but as a shareholder, my general view is that a disposal of the Food would probably be neutral or positive for the business. Given the recent share price pullback, I don’t see any reason to change my previous AMBER/GREEN view following today’s news.

J D Wetherspoon (LON:JDW)

Down 12% at 552p (£608m) - Interim Results - Roland - BLACK (AMBER/RED =)

Unfortunately it’s another profit warning today from this popular pub chain, following a downgrade in the autumn and a further cut to expectations in January.

Chairman Tim Martin was more explicit in his guidance than he sometimes is – possibly not a good omen:

There is clearly considerable pressure on consumer finances, combined with higher taxes, wages and energy costs for the hospitality industry. This may result in profits that are slightly below current market expectations.

Wetherspoon shares are down sharply today, but our view has always been that this is a well-run business with attractive scale. Do today’s half-year results provide any hope that value may be emerging here?

Half-year summary

I think the underlying trends highlighted by today’s interim results can best be described as mixed. On the one hand, sales performance was positive:

Revenue up 5.7% to £1,087.8m

Like-for-like sales +4.8%

Bar sales +7%

Food sales +1.3%

Slot/fruit machines +8.9%

The company also says it has outperformed an industry tracker index for the last 42 months, maintaining this record in February. This could suggest Wetherspoon continues to take market share, or at least has better pricing power than peers:

NIQ RSM Hospitality Business Tracker Feb 26: Pub Groups LFL 1.0%

Wetherspoon Feb 26 LFL +3.2%

Slightly oddly, I notice that Wetherspoon doesn’t appear in the list of participants for this industry survey.

Unfortunately, a 5.7% increase in sales over the last six months was not sufficient to cover the 7.3% increase in operating costs over the same period. Profits fell sharply:

Adjusted pre-tax profit down 31.9% to £22.4m

Operating margin 4.9% (H1 25: 6.3%)

Adj earnings per share down 27.9% to 15.5p

Interim dividend unchanged at 4p per share

The commentary in today’s report makes it clear the problem of rising costs outpacing revenue growth is a long-running trend:

At the same point in FY19, sales per pub were 35.4% higher in H1 2026 - above inflation.

However, energy costs are 80% higher than in H1 FY19 and wage costs are said to be 61% higher than they were then.

The company claims the pub sector has lost around 15% of its beer trade since the pandemic. This is perhaps more challenging for Wetherspoon’s value-and volume driven business model than it might be for some premium operators.

Property & Capital expenditure: changes to the group’s pub estate were limited during the period, with six pubs opened and six closed. At the end of the period, 794 managed pubs were trading, with a total of 15 expected to open during the financial year.

Wetherspoon’s is also continuing to expand its franchised estate. Eight franchised pubs opened during the half year, bringing the total to 16. Around 15-20 are expected to open in the current year. Franchised pubs are said to “have performed well” and could potentially improve Wetherspoon’s profitability, given their capital-light nature.

Outlook

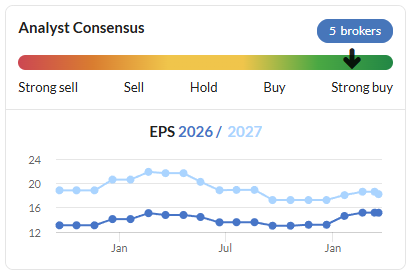

I don’t have access to updated broker forecasts today, but the c.10% drop in the share price this morning suggests to me that consensus earnings could fall by a further 5% or more.

My guess is that the stock’s forward valuation is likely to remain broadly unchanged. The current rating is below JDW’s historic average P/E, but I think this may be justified by weaker profitability and the uncertain outlook:

Roland’s view

Today’s results highlight the long average tenure of the company’s pub and kitchen managers (15.7 years and 11.7 years respectively) and other employer quality metrics such as high food hygiene scores and Top Employer ratings.

I continue to see this as a well-run business, but there’s no escaping the pressure this business model is under at the moment from rising costs and pressure on consumer finances.

I think the company’s focus on the value end of the market may not be helping in this regard – JDW shares have underperformed big listed peers over the last five years:

I’m relieved to see Graham downgraded our view to AMBER/RED in January, since when the share price has fallen by a further 20%.

I’m going to leave that view unchanged today to reflect the continued decline in profitability.

However, if Wetherspoon can deliver on revised guidance over the remainder of the financial year (y/e July), then I’d hope that we might be able to return to a neutral view later in 2026.

Works co uk (LON:WRKS)

Up 19% at 44p (£28m) - Update regarding online proposition - Roland - AMBER/GREEN ↑

This is a fairly unusual announcement – a retailer announcing that it is stopping online sales and upgrading its profit guidance as a result.

Today’s news from The Works has received a rapturous reception from investors. It’s not hard to see why. As Mark discussed in January, we already knew that store sales were outperforming online after two consecutive years of online logistics issues.

This update makes the case for abandoning online sales even more clearly:

Since launching online in 2012, 90% of sales have still come from “its profitable estate of more than 500 stores”.

Operational problems experienced with two different third-party fulfilment partners over the last two years have “outweighed the progress made” with online sales.

Given the “small and reducing revenue contribution and loss-making performance” of online, the Board has decided the online channel “is no longer sustainable”.

With immediate effect, The Works’ has now moved to “a non-transactional website”. A quick check this morning shows this has already happened – price information is available together with a find your local store facility.

New trading model

The company’s website will act as an online shop window for the business. Closure of online operations is expected to reduce operating costs and sharpen the focus on the group’s store estate, which is expected to expand further:

The store estate offers significant growth potential, with ongoing like-for-like (LFL) sales growth and scope to expand the Group's footprint by a further 100 locations. A net 5 new stores are set to open in FY26, with a further 10 planned for FY27.

Outlook & Upgraded Guidance

This is where it gets exciting.

Management says that like-for-like sales are up by 3.3% for the year to date (y/e 30 April). This is expected to support a FY26 pre-IFRS 16 Adjusted EBITDA of £11.0m in line with current market expectations.

Checking back, the equivalent EBITDA measure for FY25 was £9.5m, so it seems The Works is able to generate profit growth from much lower sales growth than JD Wetherspoon (see above).

The closure of online is expected to result in around £2m of exceptional costs.

However, once these have been adjusted out, the profitability of the remaining business is expected to improve significantly. As a result, EBITDA guidance has been upgraded today:

FY26 guidance for continuing operations is restated to pre-IFRS 16 Adjusted EBITDA of £13.5m (+23% vs £11m previously).

FY27 Adjusted EBITDA guidance is upgraded to £15.0m (+18% versus £12.7m previously).

Roland’s view

While adjusted EBITDA is not the same as actual earnings, today’s upgrades appear to provide a reasonable level of support for this morning’s c.20% share price rise.

With the stock trading on a FY26E P/E of 6 prior to today’s news, I think it’s probably fair to say that the shares may remain reasonably valued. If the company’s store-only strategy performs as expected, then I think a further re-rating may be possible.

The Work’s capital-light model means that its quality metrics are strong, so cash generation could also be good when the drag from online is eliminated:

Today’s upgrade should also create a more positive trend in earnings forecasts:

Mark was neutral on The Works in January, largely due to the continued problems with online sales. Given the strength of today’s upgraded guidance the removal of the drag from online, I think it’s reasonable for me to move our view up by one notch to AMBER/GREEN today.

DFS Furniture (LON:DFS) (Backlog)

Unch. yesterday at 149p (£365m) - Interim Results - Roland - AMBER =

Furniture group DFS reported half-year results on Thursday that appeared to be in line with expectations. Although the share price was largely unmoved on the day, the stock has been a big casualty of the recent sell-off in consumer stocks:

Graham turned neutral at a higher price in January, admitting that DFS’s strong H1 profit growth and reduced net debt meant the picture had improved significantly.

He also noted that “if a furniture group like DFS is doing so well […] UK consumer sentiment cannot be as bad as some companies would have us believe”.

January’s update included an upgrade to full-year guidance that lifted FY26 EPS estimates by 15% to 15.2p:

Half-year summary

This week’s interim results leave full-year guidance unchanged but do provide a little more colour on recent trading. Here are some of the main points:

Revenue up 8.6% to £547.7m

Order intake growth YoY: 2.3% (H1 25: +10.1%)

Gross margin up 1.1% to 57.8%

Pre-tax profit up 92% to £30.3m

Adj EPS up 85% to 9.8p

Net debt reduced by £56.1m to £60.6m

Leverage multiple of 0.8x (H1 25: 1.6x)

The increase in H1 profit is certainly very impressive, although order intake appears to have slowed since last year.

However, one point I’d make is that the company admits working capital timing means actual leverage at the year end was 1.0x – the top end of DFS’s target range of 0.5x - 1.0x.

Personally, I would prefer this business to target a net cash balance (like its delisted peer SCS) to reflect the risks associated with the huge negative working capital position on the balance sheet:

H1 inventories, receivables and cash: £89m

H1 trade payables: £245.8m

If orders slow, DFS will stop receiving cash upfront from customers but would still need to unwind its outstanding payables.

This may not happen if trading remains stable, but management commentary suggests there could be some risk of weaker trading in H2:

Since the half year we have seen some softening in footfall linked to adverse weather conditions over the period and consumer confidence remains delicately balanced.

Outlook & Guidance

DFS left its upgraded guidance from January unchanged this week:

We remain focused on executing our strategy and in combination with our disciplined approach to gross margin and cost management we are comfortable reiterating our guidance of full year PBTu(A) in the range of £43-50m. This assumes no material supply chain disruption resulting from current geo-political events impacting the timing of delivery of customer orders.

This guidance implies H2 pre-tax profit of between £12 and £19m, compared to £13.3m for the same period last year.

Consensus FY26E EPS of 15.2p puts the stock on a forward P/E of <10 after recent falls, potentially unemanding for a business where returns on capital have now returned to >10%.

Roland’s view

Given the improvement in H1 profit, I guess that achieving a similar result in H2 shouldn’t be too demanding. However, there’s a strong seasonal bias to H1 in this business so I’m not sure how certain this is.

There might be a case for upgrading our view to be more positive, especially as DFS currently enjoys a decent StockRank and Super Stock styling.

However, like Graham I am not entirely sure how robust profits are here and would prefer to see a stronger balance sheet. On balance I am going to remain neutral today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.