Good morning! And welcome to our final report of Q1.

The FTSE was strong throughout yesterday’s session and is set to open today just below 10,100.

March has been a very tough month for stock indices - the FTSE is down 6% - but we are seeing a little strength to finish it off.

Markets yesterday were weighing up a) Trump’s willingness to scale down the war against Iran earlier than expected, and b) the potential for the Fed to cut rates this year, instead of raising rates, as outgoing Chair Jay Powell said that the Fed was not responsible for supply shocks.

Market forecasting at the moment is primarily an exercise in telepathy - what does Trump really think? What does the Fed really think?

What I do know is that the FTSE is on a trailing P/E ratio of about 16x, while UK small caps are at about 14x.

That compares to c. 25x for the S&P 500.

We're out of time for today, but if the rest of this shortened week is quiet, we should get to do a few backlog sections. Cheers!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£228bn | SR71) | The efzimfotase alfa (ALXN1850) Phase III clinical programme, designed to study a broad hypophosphatasia (HPP) patient population, demonstrated positive results. | ||

Unilever (LON:ULVR) (£99bn | SR66) | ULVR is now in advanced discussions with McCormick. An agreement could be concluded today. Unilever Foods (ex India) to be combined with McCormick. Upfront cash $15.7bn, with the majority of the consideration in McCormick equity. Unilever and its shareholders would own 65% of the combined company. | AMBER/GREEN = (Roland - I hold) [no section below] We covered this story in more detail when it broke on 20 March. Today’s update doesn’t provide enough information for us to consider valuation, but I’d note that the Foods business generated €2.8bn in operating profit last year, so previous City estimates of a mid-high $30’s billion total price tag seem both reasonable and consistent with today’s commentary. Judging from this morning’s statement, the structure of the deal that’s under discussion would mean that Unilever shareholders would remain exposed to the Food business for some time yet. | |

Lloyds Banking (LON:LLOY) (£53.5bn | SR77) | The details of the redress scheme differ from the scheme as laid out in October 2025. LLOY is assessing the implications and impact of the final rules. | ||

ROSEBANK INDUSTRIES (LON:ROSE) (£3.1bn | SR8) | “The Directors believe that a move to the Main Market is the natural progression for Rosebank as the Group scales, positioning the Company for its next stage of development.” | ||

3i Infrastructure (LON:3IN) (£3.0bn | SR83) | 3IN agreed to sell its 71% stake in TCR in March 2026, for expected net proceeds of €1,140 million, a c.50% uplift to the pre-sale valuation. “The majority of the portfolio continues to deliver growth which, given the TCR valuation uplift at exit, leaves the Company on track to deliver its target return for the full year…” | ||

Ashmore (LON:ASHM) (£1.41bn | SR67) | Japan Post Insurance and ASHM have agreed to establish a strategic partnership. Japan Post Insurance initially intends to invest a further US$1 billion into Ashmore funds. It is envisaged that Japan Post Insurance will acquire up to a 2.9% equity stake in Ashmore through open-market purchases. | ||

Sigmaroc (LON:SRC) (£1.30bn | SR86) | Increased facility of up to €825 million on investment grade terms together with a €300 million uncommitted accordion. 100bps improved margin and more flexible covenants. | ||

Princes (LON:PRN) (£912m | SR21) | Revenue +46% reflecting the inclusion of business combinations. Pro-forma revenue down 6% “reflecting deflationary pressures across several core raw materials and the strategic exit from low-margin contracts.” Pro-forma profit after tax of £61.4m (previous year: £9.3m). Outlook: “…confirms its medium-term guidance of £3 billion+ revenue, +300 basis points of EBITDA margin expansion from FY2024 levels, and underlying FCF conversion of greater than 60%.” | ||

Pets at Home (LON:PETS) (£800m | SR87) | Group underlying profit before tax (PBT) for FY26 is expected to be c£92m, in line with previous guidance. Outlook: Looking ahead to FY27, at this stage, we have c80% of our energy and FX requirements hedged and are comfortable with current analyst consensus expectations for Group underlying PBT. | ||

A G Barr (LON:BAG) (£691m | SR68) | Revenue +4%. Adjusted PBT +12.5% (£65.8m). Adjusted ROCE slightly lower at 20.4%. We entered FY26/27 with good momentum and will continue to demonstrate tangible progress against our strategic objectives. | GREEN = (Graham) I'm happy to stay positive on this. The main feature of the strategy right now is acquisitions: and I expect this to continue, based on the company's stated appetite for a leverage multiple of up to 2.5x. It had a net cash position as of January 2026, so it has a long way to go before it reaches the upper limit of the debt that it thinks it could afford. | |

Allergy Therapeutics (LON:AGY) (£665m | SR25) | Revenues +7% (+2.5% at constant currencies). Operating loss £2.5m before R&D. Cash position £10.1m. “With Grassmuno expected to be a major driver of the Group's business in Germany, its largest market, commercialisation is underway and sales momentum is expected to accelerate further in the second half of the financial year… the Group has sufficient funds for the entirety of the twelve-month going concern review period…” | ||

Dominos Pizza (LON:DOM) (£655m | SR60) | The Interim CEO is appointed permanent CEO. She was previously COO. | ||

Raspberry PI Holdings (LON:RPI) (£566m | SR35) | Revenue +25%. Adjusted EBITDA +25%. PBT +63% ($26.5m). “Strong sales momentum has carried into the opening months of this year. While the DRAM (dynamic RAM) environment limits second-half visibility, we have the inventory position, supplier relationships and pricing flexibility to navigate it effectively. Against that backdrop full-year profitability is anticipated to be in-line with market estimates, with revenue materially higher.” | ||

James Halstead (LON:JHD) (£515m | SR71) | Revenue down 2.2%. PBT £24.7m (2024: £28.5m). “...UK sales… have in the first two months of 2026 picked up with a greater perception of improved conditions. It is clear, to us, that backlogs of repair and refurbishment in key sectors remain. However, once again issues in the Middle East are causing head winds in respect of raw material, energy and transportation costs which, it must be noted, affect our competitors at least as badly. Inevitably this will have inflationary effects.” | BLACK (GREEN = ) (Roland - I hold) Exceptionally, I am leaving our GREEN view unchanged today even though broker forecasts have been downgraded today. There are two reasons for this. The first is simply that I think this is a high quality business that’s trading too cheaply. At the same time, shareholder equity is supported by a £70m net cash position, providing both a margin of safety and terrific optionality for management, if they need to invest to support emerging opportunities or to adapt to difficult conditions. This has proven to be a powerful advantage in the past, most recently during the pandemic when Halstead was able to rapidly expand its stockholdings to meet demand. | |

GlobalData (LON:DATA) (£500m | SR40) | The purpose of the Share Buyback Programme is to return surplus capital to shareholders and reduce the Company's share capital. All shares repurchased will be cancelled. | ||

GB (LON:GBG) (£452m | SR69) | £10 million extension of the Company's share repurchase programme, having completed £45m of repurchases during FY 2026. The Board considers this additional Share Buyback Extension to be an attractive use of surplus capital, aligned with our capital allocation policy, to generate significant shareholder value over the long-term. | ||

Hilton Food (LON:HFG) (£442m | SR81) | Adjusted profit before tax including discontinued operations of £73.2m within expected range, adjusted PBT from continuing operations of £69.0m. 2026 outlook unchanged since January 2026 Trading Update; adjusted PBT expected to be in the range £60m to £65m. Searching for a new Non-Exec Chair. When found, the current Exec Chair will become CEO. | ||

Future (LON:FUTR) (£366m | SR69) | SP -23% …while we expected continued shifts in the audience derived from Google search, these have been more pronounced than anticipated. This is driving lower year-on-year sessions, negatively impacting higher-margin programmatic advertising and ecommerce revenues… H1 revenue is expected to be broadly in line with management's expectations but the EBITDA margin is now expected to be in the range of 24-25% driven by the revenue mix… taking a cautious view for the balance of the year. | BLACK (AMBER ↓) (Roland) I am less optimistic than some of my fellow writers about the prospects for this business, but I do accept that Future’s earnings probably deserve a P/E higher than three. Having said that, I think there’s still some risk of further pressure on profitability and earnings due to the evolving nature of online search traffic and the impact of AI. In the absence of any apparent existential threat, I’ve downgraded our view to neutral today to reflect the mix of factors I can see in this situation. | |

Videndum (LON:VID) (£342m | SR10) | Raised £85m on 30th March at 270p, alongside debt-for-equity swap of an RCF. Debt reduced to £30.6m including finance leases. For FY 2026, the Board expects good revenue growth, supported by the introduction of new products in both FY 2025 and FY 2026. | ||

Mortgage Advice Bureau (Holdings) (LON:MAB1) (£313m | SR71) | Launch of Share Buyback Programme & Update on Move to the Main Market | Launched buyback for 479k shares to meet share option obligations (c.£2.6m). Expected admission to Main Market on 1 May 2026, with the last date of AIM trading to be 30 April 2026. | |

Avacta (LON:AVCT) (£284m | SR27) | Enrollment underway in second Avacta clinical program at first three specialist U.S. oncology centers. Initial data from trial expected later this year. | ||

Judges Scientific (LON:JDG) (£268m | SR38) | Revenue up 9.1%, adjusted op profit up 0.4% to £28m. Adj EPS down 2.9% to 275.3p, in line. Order intake down 10% vs 2024. 2026 outlook: “lower-than-desired order book” with YTD order intake 17% below the 2025 YTD comparative. US research funding freeze appears to be a significant issue, with no clarity on resolution. 2026 adj EPS to be in the range 200p - 250p (consensus: 222p). | ||

Empire Metals (LON:EEE) (£213m | SR10) | Sale of 75% interest in Eclipse Mining Licence is ongoing. Purchase has completed a drill programme but assay results have been delayed, so the purchaser has requested extra time. A A$50k non-refundable deposit has been received, with the balance of A$700k due at settlement pending successful due diligence. | ||

Galantas Gold (LON:GAL) (£165m | SR25) | TSXV is reviewing the Sol Transaction. Galantas provides a timeline to support its claim that the Sol Transaction and RDL Transaction were separate and independent and not part of a coordinated plan. Sol and RDL both had a common shareholder, Robert Sedgemore. | ||

Optima Health (LON:OPT) (£160m | SR73) | Launched offer to raise c.£35m at 175p per share to repay £30m bridge facility used to acquire PAM Healthcare in February. | ||

Pantheon Resources (LON:PANR) (£158m | SR20) | Repositioning business to make Kodiak the “cornerstone of the portfolio”. Actively pursuing farm-in opportunities. Net loss of $9m, cash at 27 March 26 of $15.1m, with $18m of debt (31 Dec 25). | ||

Rainbow Rare Earths (LON:RBW) (£138m | SR36) | Established its flagship Phalaborwa project in South Africa as a proven producer of REE. Identified possible opportunity in Brazil. Has just raised $14.6m from investors at 20p per share to support further work on these opportunities. | ||

BRCK (LON:BRCK) (£132m | SR77) | Received non-binding proposal for an offer of 65p per share from Atlas. The Board rejected this offer on the grounds of valuation. Has agreed to provide further information to Atlas to establish whether an improved offer is possible. PUSU date: 5pm on 28 April 2026. | PINK (GREEN ↑) (Graham) | |

Duke Capital (LON:DUKE) (£131m | SR75) | Expects recurring cash revenue of £7m in Q4 FY26 (+8% YoY). Total cash revenue for Q4 expected to be £8.5m, following deferred receipt of Fabrikat disposal proceeds (2024). | ||

Peel Hunt (LON:PEEL) (£127m | SR80) | Now expects to deliver full year revenues of over £140m and profits that are materially ahead of market expectations. Events in Middle East are weighing on market conditions and may affect the level and timing of transactions. | GREEN = (Graham) | |

Strategic Minerals (LON:SML) (£116m | SR36) | Begun infill drilling with drillhole CRD042 at Redmoor. Planning eight holes totalling 3,850m, scheduled to take six months to complete. | ||

Jubilee Metals (LON:JLP) (£105m | SR21) | Implementation of Mine Plan at Molefe & Financial report for 6 months to end-December 2025 | Total saleable Cu units up 8.7% to 1,543t. Copper revenue up 70.5% to $14.1m, EBITDA from continuing operations up 169% to $2.0m. Operating loss of $4.2m. | |

Anpario (LON:ANP) (£89m | SR68) | Revenue up 24% to £47.2m, pre-tax profit up 54% to £8.0m. Adj EPS up 33% to 39.5p, in line. LFL sales excluding Bio-Vet rose by 12%. Outlook: YTD trading is in line. Working to mitigate any logistics impact re. Middle East. | AMBER/GREEN ↓ (Roland) A good set of results from this animal feed specialist, showing improved quality metrics and a growing presence in the key US market. The balance sheet looks very strong, with net cash of £12.4m and the outlook for 2026 is largely unchanged today. The only caveat to this is the potential for shipping disruption and higher energy and commodity prices as a result of the situation in the Middle East. When combined with slowing earnings growth (+2% forecast in 2026) I have decided to err on the side of caution and move my previous GREEN view down by one notch. On a long-term view though, I continue to see good prospects and attractive value here. | |

Venture Life (LON:VLG) (£83m | SR49) | Revenue up 32%, operating loss increased to £1.3m due to “disproportionate position” of the cost base following recent divestments. Adj EPS up 15.4% to 3.89p, in line. Outlook: confident in meeting management guidance for 17-months to 31 May 26. | ||

Shield Therapeutics (LON:STX) (£80 million | SR33) | European Medicines Agency have published the CHMP meeting highlights in which they confirm their adoption of a positive opinion for the extension of the indication for FeRACCRU® (ferric maltol) to include adolescents for treatment of iron deficiency. | ||

Severfield (LON:SFR) (£71m | SR69) | FY26 pre-tax profit expected to be in line with market expectations of £10.2m. Net debt of c.£28m to be lower than expected. UK and Europe order book of £438m, record Indian order book of 331m. FY27 outlook (PW): adj pre-tax profit to be £12m to £15m reflecting “a cautious view” (below PanLib previous forecast of £18.2m). | BLACK | |

Journeo (LON:JNEO) (£69m | SR51) | Contracts to provide security for three infrastructure sites under the four-year framework with “a major UK utility” announced in September. Expect to complete work during 2026. | ||

Ariana Resources (LON:AAU) (£50m | SR33) | Operating loss of £2.6m, loss before tax of £12.4m due to change in accounting treatment of Zenit. Net cash of £5.4m at year end. | ||

Touchstone Exploration (LON:TXP) (£37m | SR42) | Production 4,686 boe/d, -18% vs 2024. Revenue down 20% to $45.8m, net profit of $10.9m ($0.04 per share), versus $8.3m in 2024. Net debt reduced to $72.9m from $77.8m at 30 Sept 25. | ||

Zenith Energy (LON:ZEN) (£36m | SR33) | Received updated independent valuation of Italian solar development pipeline. Capacity increased to 173.5MWp, valuation €54.7m (previously 110.5MWp/€27.5m). | ||

Gelion (LON:GELN) (£29m | SR5) | Exceptional performance results from Gelion’s Nano-Encapsulated Sulfur (NES) Cathode Active Material platform. Seeking to replace strategic minerals in lithium-ion battery cathodes with Gelion’s NES. | ||

Poolbeg Pharma (LON:POLB) (£29m | SR32) | Received formal notification of the grant for its POLB 001 cancer immunotherapy-induced Cytokine Release Syndrome ("CRS") patent application from IP Australia, the Australian patent office. | ||

Metals One (LON:MET1) (£20m | SR5) | $1.8m in convertible loan notes have been advanced to LBR and Metals One has now exercised its right to secure 30% ownership of LBR through conversion of the notes. LBR has acquired an industrial plant for $1.36m that will require c.$4.5m of work to begin production. | ||

Cirata (LON:CRTA) (£19m | SR3) | Revenue up 77% to $13.6m, adj EBITDA loss reduced to $3.8m (2024: $14.4m). Total bookings up 96% to $13.9m. FY26 outlook: timing and conversion of new business remains uncertain, but guidance unchanged at this point. | ||

Solvonis Therapeutics (LON:SVNS) (£17m | SR19) | Granted patent for monoamine modulator compound series designed to modulate serotonin, dopamine and noradrenaline transporter systems. | ||

Altitude (LON:ALT) (£15m | SR29) | FY26 revenue to be ahead of expectations at $43.5m to $44.4m (+16.6%-19.3% vs 2024). FY26 adj op profit to be in line with previous guidance of $3.7m, flat versus FY25. Exited some uneconomic accounts, which will adversely affect FY27 revenue. | ||

Tekmar (LON:TGP) (£15m | SR65) | Contract for supply of Tekmar’s Cable Protection Technology to the wind farm developer. Expect revenue to be recognised in FY26 and H1 FY27. | ||

Quantum Helium (LON:QHE) (£13m | SR23) | Revenue AU$323k, net loss of AU$1.6m. Continued repositioning to helium-focused US portfolio. Resource report validated over 1BCF of 2U gross helium prospective resources at Sagebrush and Coyote Wash. Cash of AU$3.4m at 31 Dec 25. | ||

Tap Global (LON:TAP) (£13m | SR7) | Revenue down 5.6%, pre-tax loss of £500k. Cash at 31 Dec 25 of £433k, registered users up 4.7% to 398k. | ||

Catalyst Media (LON:CMX) (£10m | SR15) | Loss after tax of £0.15m (-0.73p per share). NAVps of 147.2p, unchanged. Investee SIS has seen headwinds in Q4 that are “likely to impact the full year outturn.” | ||

Plexus Holdings (LON:POS) (£8m | SR19) | Revenue down 58%, loss before tax of £2.1m. Net debt c.£0 at 31 Dec 25. H1 broadly in line, but projects are seeing “significant delays in starting”. Now expects FY26 revenue to be “significantly below previous expectations”. Expects working capital resources and revenues generated to be sufficient [to fund operations] for the immediate future. | BLACK |

Graham's Section

Peel Hunt (LON:PEEL)

Up 4% at 107.6p (£133m) - Trading Ahead of Expectations - Graham - GREEN =

The last interesting RNS from Peel Hunt, in January, was also entitled “Trading ahead of expectations”.

It’s all rather gratifying for me, as I’ve been saying since December that market expectations made no sense - they were too low.

Today’s update for FY March 2026 is brief, so why not post it in full.

Against a backdrop of considerable economic uncertainty, following the completion of recent Investment Banking transactions and a continued strong performance in our Execution Services business, we now expect to deliver full year revenues of over £140m and profits that are materially ahead of market expectations.

The war in the Middle East has increased geopolitical uncertainty, which has pushed energy prices higher and prompted central banks to reassess inflation risks. While the duration and ultimate impact of these developments remain unclear, they are weighing on market conditions and may affect the level and timing of transactional activity. During this period of uncertainty and market volatility, Peel Hunt remains focused on supporting clients, while maintaining disciplined cost management and capital allocation.

To recap: I noticed in December that the company had already earned net income of over £8m in H1, and yet consensus forecasts in the market suggested that full-year profits would be lower than that.

In January, I contacted the company’s PR firm.

They informed me that just prior to the January trading update, expectations were for full-year PBT of £12m. But the company had already generated £11.5m of PBT in H1.

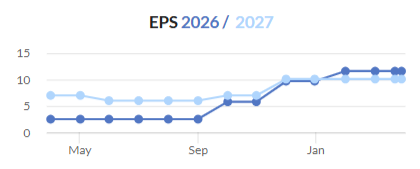

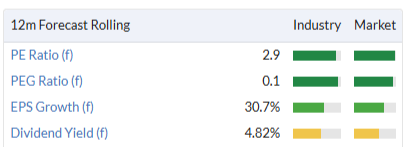

The StockReport shows that Peel Hunt’s broker, Keefe, Bruyette & Woods, has now meaningfully increased the EPS forecast:

On the StockReport, the FY26 net income forecast is £11.5m.

Assuming 25% tax, that implies PBT of nearly £15m. Granted that revenues and profits can be lumpy, but that still implies a c. 75:25 split between H1 and H2.

Other sources suggest a higher full-year PBT forecast. I have again contacted the company’s PR firm, hoping for clarification.

Whatever the truth is, it’s pretty clear to me that there hasn’t been a meaningful link in recent months between official consensus forecasts for Peel Hunt, and how the company is actually performing.

I’ve been GREEN on this stock, and it’s on my watchlist. After another ahead-of-expectations update, I’m naturally going to stay GREEN on it today.

In addition to an earnings multiple that is lower than the market seems to comprehend, there are also £100m+ of net assets (almost fully tangible) supporting the c. £130m market cap.

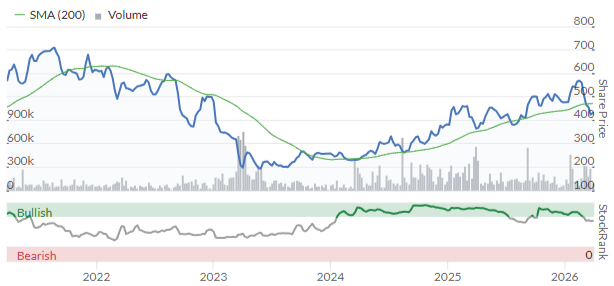

And despite issuing two “ahead” updates in 2026, the share price has made almost no progress year-to-date, reflecting wider market weakness. A prime takeover target, maybe?

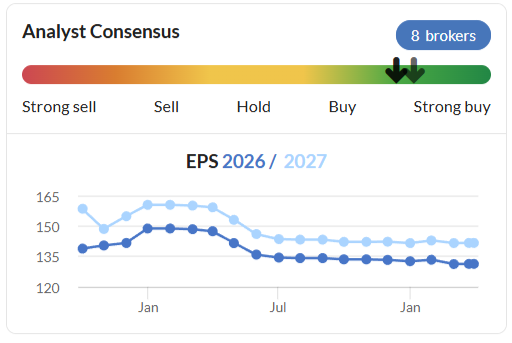

The StockRank is 80.

BRCK (LON:BRCK)

Up 26% at 51.9p (£167m) - Statement regarding possible offer - Graham - PINK (GREEN ↑)

This brick business, formerly known as Brickability, changed its name in February.

Today’s announcement is pretty exciting for shareholders:

BRCK Group PLC… announces that on 17 February 2026, the board of directors of BRCK… received an unsolicited, indicative and non-binding approach from Atlas Holdings LLC. to acquire the entire issued and to be issued share capital of BRCK.

Atlas is an American private equity firm with offices in London and the Netherlands.

BRCK says it gave information to Atlas regarding its prospects, and Atlas subsequently made an offer of 65p per share.

The BRCK board determined that this “fundamentally undervalued” their company.

But the discussions haven’t ended there:

The Board has agreed to provide some limited further information to Atlas to establish whether it is prepared to improve its Indicative Offer Price. The Board has indicated to Atlas that, in order to avoid unnecessary distraction of management and costs, the entry into a detailed due diligence process with Atlas would be subject to Atlas putting forward a proposal on terms that the Board would be minded to recommend to shareholders.

Graham’s view

This announcement is positive for many reasons.

Any bid from a serious buyer demonstrates real underlying value. Atlas are a reputable outfit who previously bought De La Rue.

The proposal in mid-March was at a nearly 50% premium to the prevailing share price. It’s a nearly 60% premium compared to last night’s price.

At the same time, the BRCK board have been clever enough not to accept the first offer they received while their shares were trading at a P/E multiple of only 4.3x.

And unlike other companies where a bid process can drag on for many months and prove to be an enormous distraction for everybody, the BRCK board have explicitly said that this is something they are going to try to avoid.

In our spreadsheet this is going down as PINK because it’s now in a potential takeover situation. In terms of my view, for what it’s worth I’m going to upgrade this GREEN (from Mark’s AMBER/GREEN)

Some risk warnings: this is financially leveraged (net debt last seen at £67m at the interims), is vulnerable to cyclical demand, and its EPS forecasts were reduced last year before ultimately stabilising:

But all of that might well be priced in at the current market cap, especially considering the private equity interest that has now been revealed. So I’m comfortable upgrading this by one notch.

A G Barr (LON:BAG)

Up 7% to 663p (£743m) - Final Results - Graham - GREEN =

A.G. BARR, the multi-beverage business with a broad portfolio of market-leading UK brands including IRN-BRU, Rubicon and Boost, today announces its Final Results for the financial period ended 31 January 2026 ('FY25/26').

We were positive on this beverage group for all of last year. Most recently, Roland was positive on it at the full-year trading update in January

The share price has been quite boring:

This has left it on a modest rating for a very sound business:

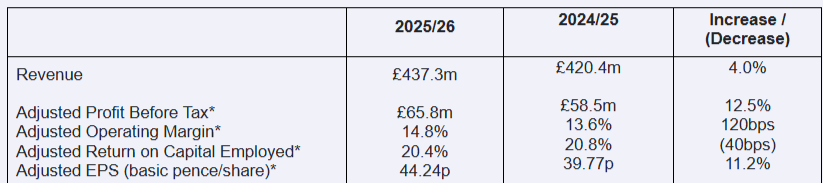

Today’s results show a pleasing increase in revenues, profits and margins, with the only slight negative being that they didn’t improve ROCE. But ROCE is already at an acceptable level:

And I’m very pleased to give credit where credit is due: CEO Euan Sutherland has produced a very clean set of results, statutory PBT coming in at £62.6m (equivalent to 95% of adjusted PBT). Statutory PBT is nearly 18% year-on-year.

So we have excellent results that are also cleaner than last year.

I would however point out that £6m of the FY26 revenues are from an acquisition (“Innate-Essence”), so the 4% revenue growth figure given is not organic.

That acquisition is currently loss-making, so the profit growth figure given is organic.

Another small acquisition (Frobishers) occurred near year-end.

Dividend: raised 11% year-on-year.

Cash: the company finished the year with £41.6m of net cash, lower than the prior year-end, due to acquisitions.

Outlook:

We entered FY26/27 with good momentum and will continue to demonstrate tangible progress against our strategic objectives. Our core soft drinks portfolio will be supported by expanded distribution, targeted brand refreshes and multiple new product launches. The integration of recent acquisitions - Frobishers Juices Ltd and Fentimans Ltd (post period end) - is well underway and progressing to plan, leaving us well positioned to realise targeted operational efficiencies from H2 and in the coming years.

As noted by Roland in January, there is scope for margins to improve at Fentimans - this will hopefully make a meaningful contribution to profits in the years ahead.

The Fentimans acquisition completed in the new financial year, so is not relevant to the FY January 26 results. It’s the largest of the three acquisitions by A.G. Barr over the past year.

Graham’s view

While the underlying business doesn’t seem to have changed much, aside from the acquisitions, there are one or two interesting things to point out.

On debt capacity:

The Board retains an intention to operate an efficient balance sheet, allowing for the option of using a prudent level of debt to capitalise on business growth opportunities when appropriate. We are comfortable that the cashflows and earnings profile of the Group could support a debt capacity up to 2.5x EBITDA.

Remember that the company had net cash as of January 2026. So if it really started going for net debt/EBITDA of 2.5x, this would imply very busy and very large M&A activity.

This goes back to the metrics that the company is focusing on:

The Company aims to consistently deliver on the following key financial metrics:

· Revenue growth ≥ 4% per annum, representing above-market growth;

· Operating margin within 14-16% range; and

· ROCE within the range of 19-21%...

I don’t object to this, but I wonder if they have made the distinction between organic and inorganic revenue growth? If they aren’t fussy about where growth is coming from then, combined with their appetite for debt, we could be seeing a lot of M&A at BAG.

Either way, I’m happy to stay GREEN on this.

Roland's Section

Future (LON:FUTR)

Down 28% at 278p (£262m) - Pre-Close Trading Statement - Roland - BLACK (AMBER ↓)

Unfortunately it’s bad news for Future shareholders this morning. The “global platform for specialist media” – which owns a range of magazines and the Go.Compare price comparison platform – has issued a profit warning for the half-year ending 31 March 2026 (today).

The key takeaway is that the drop-off from Google Search traffic (including pay-per-click advertising) to Future’s websites has been “more pronounced than anticipated” and has caused a fall in margins.

Updated outlook & guidance:

H1 revenue is expected to be broadly in line with expectations (i.e. slightly below) but the EBITDA profit margin is now expected to be 24% to 25%, due to the revenue mix.

H2 organic revenue is expected to decline “by a low single-digit percentage”.

The full-year EBITDA margin is expected to be 25% to 27%.

In December the company guided for “modest organic revenue growth in FY 2026”, but consensus forecasts suggest the market was expecting total revenue to be flat at £739m this year.

Today’s commentary suggests to me that a small decline in revenue is now likely for the year to 30 September 2026.

Similarly, Future’s EBITDA margin last year was 30% and the company’s outlook guidance in December was for a stable margin of “around 30%”this year.

We don’t have access to any updated broker notes this morning so I’ve made a guess at the likely reduction to EBITDA and EPS estimates:

Applying the mid-point of today’s margin guidance to a revenue estimate of £725m gives me an updated FY26 adj EBITDA estimate of £189m.

According to the company, previous consensus was for FY26 adj EBITDA of £221m, so this could be a c.15% reduction.

I’d expect this to translate to a larger reduction in adjusted earnings, so I would guess that this morning’s c.25% share price fall is probably a reasonable reflection of the likely cut to earnings forecasts. If so, that would give me a revised FY26 adj EPS estimate of c.100p.

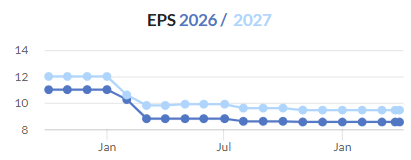

This implies a forward P/E of 3, similar to the valuation prior to today’s warning:

H1 Trading commentary:

During the first half of this year, B2C direct digital advertising revenue in the UK and US has continued to perform well and is expected to deliver year-on-year growth, with particularly strong demand for Future Optic (the company’s AI optimisation tool).

SheerLuxe, a Google-Zero brand acquired in January, is performing ahead of our expectations

Magazines revenue continues to remain highly resilient

Go.Compare revenue decline has moderated in H1, with a return to growth in March and we expect revenue growth in H2.

Within B2B, we have also seen a moderation of revenue decline in H1 and expect new product launches to deliver a return to growth in H2.

Reading this doesn’t suggest an obvious issue, but the devil is in the detail – changes to Google Search have impacted the profile and profitability of traffic.

Google Search vs Google-Zero

Indeed, today’s warning is explicitly blamed on changes on traffic from Google’s search and advertising tools:

However, while we expected continued shifts in the audience derived from Google search, these have been more pronounced than anticipated. This is driving lower year-on-year sessions, negatively impacting higher-margin programmatic advertising and ecommerce revenues and has also led to PPC cost inflation across the industry.

The hazards of relying on Google Search traffic and advertising algorithms for a big chunk of your revenue are well known and are not new. Businesses relying on Google to drive traffic have lived with this kind of risk for many years. Periodic changes to Google’s algorithms can result in sharp rises in advertising costs and/or a sudden drop-off in traffic. I have experienced this myself in a past life – it’s not much fun.

One growing problem is that Google’s AI overviews (at the top of search results) mean that many people no longer click through to the source website for information. That’s bad news for publishers who then cannot monetise this traffic – even though the search users have benefited from the publishers’ work.

Future is of course aware of all of these issues and is already pursuing a Google-Zero strategy – here’s what the company said about this issue with its FY25 results in December:

Our audience strategy of diversification into email, direct, social, also known as "Google-Zero", impacts all of our strategic initiatives.

Thanks to the scale and diversity of our audience, overall engagement has remained steady. Website sessions are only 56% of our audience and of this 56%, only 27% is coming from Google Search, with other sources including Google Discover and News, Social and Emails.

The company also recently spent £40m to acquire SheerLuxe, a “highly-recognised Google-Zero brand that draws an audience of 6m across social, newsletters, websites and podcasts, skewed to Gen Z”.

Roland’s view

The Board believes that the Group is fundamentally undervalued. The Board is actively focused on driving value from the assets which deliver a strong platform effect and to realise value for shareholders from those that do not.

Future’s core business model (in magazine publishing and price comparison) is essentially built on driving traffic from which it can harvest commission payments for users who click on a link and make a purchase (from a third party).

Speaking as someone who has been involved in a similar business (on a much smaller scale) in the past, my main issue with this model is that I do not think it produces very high quality earnings. I also think that the kind of problem reported today may well recur, randomly, in the future.

Shifting dependency from one traffic channel to another won’t necessarily reduce the risk of future problems, although genuine diversification of traffic and building loyal direct audiences does help.

Having said all of that, I do think Future’s earnings probably deserve a P/E multiple that’s higher than three.

The risk remains that further downgrades will follow today’s profit warning. Our research finds that stocks often underperform for an extended period following an initial warning.

In this case specifically, the transition of a proportion of web traffic from search to AI and other channels remains a live evolution. The next step – which I expect to see at some point – is that AI services will start monetising their growing role as a gatekeeper to brands’ traffic.

Of course, today’s downgrade isn’t the first in recent times for this business. Future also warned on profits a year ago:

Given this, perhaps we might argue (more optimistically)) that the downgrade cycle is nearing its end, and that Future’s performance might soon bottom out.

Mark was previously AMBER/GREEN on Future, most recently in February when he acknowledged the likelihood of a “relatively slight miss”. I think today’s warning justifies a more conservative view, but I do agree that the overall valuation of the business suggests there could be some value here.

To reflect this mix and our general practice of downgrading our view on shares following profit warnings, I’m moving our view down by one notch to AMBER today.

Anpario (LON:ANP)

Up 3% at 443p (£91m) - Final Results - Roland - AMBER/GREEN ↓

Anpario plc (AIM: ANP), the independent manufacturer of natural and sustainable feed additives for animal health, nutrition and biosecurity, is pleased to announce its full year audited results for the twelve months to 31 December 2025.

Today’s results look quite strong to me and are in line with guidance that has been upgraded repeatedly over the last 15 months:

Despite this, the share price is almost unmoved and Anpario stock remains down by nearly 10% on a year-to-date view:

The reason for this year’s sell-off is of course the conflict in the Middle East.

Anpario generated about 12% of pre-tax profit from its Middle East & Africa operations last year, but it’s also exposed to the logistics disruption in the region and potential commodity/energy price rises:

Clearly recent events in the Middle East will cause disruption, the impact of which it is too early to assess. However, we have an experienced team who have managed through similar periods and our subsidiaries have the benefit of good local inventory with which to continue to service our customers.

Moving on, does this sell-off provide a potential buying opportunity for investors taking a medium-term view? Anpario’s performance is much improved from a couple of years ago, with new products and recent acquisitions apparently performing well.

Let’s take a look at these results.

2025 results summary

Headline figures are strong:

Revenue up 24% to £47.2m

Like-for-like sales (excluding BioVet) up 12%

Pre-tax profit up 54% to £8.0m

Adjusted earnings up 33% to 39.5p per share

Total dividend up 11.1% to 12.5p per share

Net cash of £12.4m at year end (2024: £10.5m)

Trading commentary suggests a year of respectable progress:

Full-year contribution from Bio-Vet, which generated £6.7m of revenue and is said to be performing in line with expectations under a new Americas management team. It’s expected to help broaden species exposure and strengthen growth in the US, a key target market.

Strong LFL growth in the Americas, Europe and Asia.

Good growth in premium product classes such as Orego-Stim and Optomega Algae.

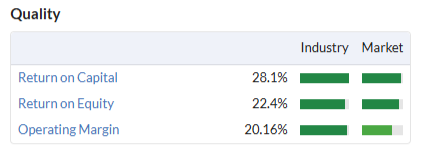

Profitability and cash flow: the accounts support the StockRanks’ view that this is a good quality business:

My sums show Anpario’s operating margin improving to 16.7% last year (2024: 12.8%), while I calculate a return on capital employed of 18.1% (2024: 12.6%). ROCE is not quite at the 20% level I’d view as a benchmark for a true high quality business, but for a business of this kind I think 18% is pretty respectable.

Today’s accounts show net profit of £6.8m being converted into free cash flow of £7.4m (excluding working capital movements and acquisitions). That’s another indicator of quality, in my view.

On a related note, the net cash position of £12.4m now accounts for about 14% of the current market cap and should provide a comfortable margin of safety to help address any supply chain issues.

Outlook

Trading so far this year is said to be in line with expectations, with continued growth in North America and “a strong start and return to growth for the Middle-East region”.

With thanks to Shore Capital for publishing on Research Tree, we can see that 2026 forecasts have edged slightly higher today, while Shore has also introduced forecasts for 2027.

Shore FY26E revenue / adj EPS: £50.0m / 40.3p (previously £50m / 38.8p)

Shore FY27E revenue / adj EPS: £52.5m / 42.5p

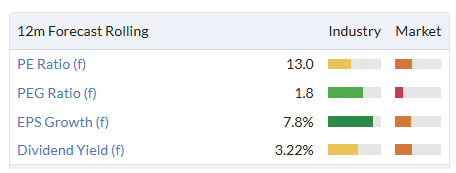

These estimates put the stock on a forward P/E of 10.7 with a prospective dividend yield of 3.2%.

Adjusting for net cash gives a FY26 P/E of 9.2.

Roland’s view

Today’s forecasts imply 2026 revenue growth of 6% and earnings growth of 2%, with earnings growth improving to 5.5% in 2027.

This is a slower rate of growth than that seen last year, which may justify some moderation in the valuation. However, as far as I can see the only real concern for investors at this time and share price is the potential impact of the conflict in the Middle East. In addition to shipping disruption, the business could be affected by higher prices for energy and certain commodities.

There’s precedent for this – the war in Ukraine caused problems for Anpario, albeit the Middle East impact might not be so severe:

As far as I can see, the impact of the situation in the Middle East is impossible to quantify at the moment. It may amount to a lot or a little, in terms of profit impact. The company is at pains to emphasise that it has an experienced logistics team and good stocks in place, so the situation may well prove to be manageable.

Excluding this known unknown, I think Anpario looks attractively valued, with a strong balance sheet and decent medium-term prospects.

I was GREEN on Anpario in January at a higher valuation. I would normally leave this unchanged today, but I think the combination of slowing earnings growth and unknowable risks from the situation in the Middle East mean it might be prudent for me to move my view down one notch to AMBER/GREEN.

On a longer-term view, however, I remain positive on the outlook and valuation here.

James Halstead (LON:JHD)

Up 3.8% at 123p (£516m) - Interim Results - Roland - BLACK (GREEN = )

(At the time of writing, Roland has a long position in JHD.)

Today results from this family-owned flooring company are much as I’d expect – super profitability and a fortress-like balance sheet, but flagging sales and a somewhat uncertain near-term outlook.

Executive chair and family member Mark Halstead expresses it slightly differently, but I think the message is the same:

I am pleased to report a robust balance sheet, strong cash inflow and a record interim dividend achieved against a backdrop of challenging markets. Our very long record of dividend increases continues and the markets in which we operate continue to generate demand which in turn gives us confidence in the medium term.'

H1 results summary

James Halstead’s accounts are always wonderfully free of adjustment and hype. If all companies reported like this it would save us a lot of time when preparing these reports.

Unfortunately, there’s no escaping the negative trends highlighted by these numbers:

Revenue down 2.2% to £127.2m

Pre-tax profit down 13.3% to £24.7m

Earnings down 12% to 4.4p per share

Interim dividend up 3.6% to 2.85p per share

Net cash of £70.8m (Dec ‘24: £63.7m)

A small fall in revenue and a much larger fall in profit tells us that James Halstead’s margins came under pressure when compared to the first half of last year. The group’s operating margin for the period fell to 18.6%, from 20.8% during the same period last year. This is likely to dent the company’s excellent quality metrics slightly, but I don’t see the overall picture changing too much:

Today’s reporting is clear and tells us that the group’s gross margin remained relatively stable at 44.56% (vs 44.75%). This means that the main reason for the fall in profit was a 6.2% increase in operating costs, “largely in the UK”.

One other point worth making is the strength of the balance sheet – £70m net cash is clearly more than needed, but it gives James Halstead terrific flexibility and strength in adverse markets. The company is able to invest in inventory to meet demand or acquire assets at opportunistically (for example), without ever needing to worry about its financial health.

We saw this most recently during the pandemic, when Halstead was able to massively increase its inventories to meet demand and maintain availability.

A £70m net cash position also generates a useful income – net finance income was >£1m in H1, providing a useful boost to operating profit.

Trading commentary:

The UK is also Halstead’s largest market (44% of turnover) and saw sales rise by 1% during the period, despite a slowdown in the final months of calendar 2025.

A “prudent approach to credit with customers” is also said to have contributed to a slowdown – Halstead doesn’t want to supply products to customers who might struggle to pay.

Underlying conditions in the UK don’t sound too bad, though, with a pick-up reported for the early months of this year:

However, our ongoing expectations are for increased sales in the UK as spending on education, prisons, health care and aged care, particularly refurbishment, picks up.

Overall exports fell by 5% compared to the same period last year, mainly due to weakness in Europe and Australia/New Zealand. However, there were some bright spots in other export markets:

USA (+15%)

Canada (+25%)

Africa (+41%)

Middle East: “comparable with last year”

Outlook - mild downgrade

However, once again issues in the Middle East are causing head winds in respect of raw material, energy and transportation costs which, it must be noted, affect our competitors at least as badly. Inevitably this will have inflationary effects.

The fundamentals of our business, product ranges and routes to market are well established and the markets in which we operate continue to generate the demand that, despite short term challenges, gives us confidence in the medium term.

When a company focuses on its medium-term prospects, it often means the short-term outlook is more challenging than expected. That seems to be true here.

Today’s results have been accompanied by small downgrades to earnings forecasts from both Panmure Liberum and Zeus. Our thanks for making these available on Research Tree.

Both brokers cite cost pressures and uncertain end market conditions as headwinds for near-term profits.

Here are the revised forecasts. Earnings are now expected to be flat this year, whereas previous expectations were for a modest return to growth:

Panmure Liberum FY26E EPS: 9.9p (-3.9% vs 10.3p previously)

Zeus FY26E EPS: 9.4p (-6.8% vs 10.1p previously)

Averaging these two gives me a FY26 consensus estimate of 10.2p per share, providing continued cover for the expected 9p dividend.

That’s equivalent to a P/E of 12 and a 7.3% dividend yield at current levels. I think that could be cheap for a £500m company whose balance sheet is backed by £70m of net cash.

Roland’s view

James Halstead is a family business with strong brands (Polyflor is the main product), good market share and an incredible balance sheet. While market conditions are weak at the moment, I don’t see why they shouldn’t recover in time. When that happens, I think the company will be well positioned to benefit.

In the meantime, I remain happy to continue holding the stock and collecting dividends.

One key attraction of this stock is its dividend. Last year saw the dividend rise for the 49th consecutive year. Today’s results show the interim dividend has been increased by 3.6% to 2.85p per share, suggesting to me that 2026 might be the year when Halstead achieves 50 years of unbroken dividend growth.

In the past, low interest rates and high demand for the stock as an AIM IHT portfolio stalwart meant that Halstead shares traded at a strong valuation, with a low dividend yield. That’s not the case anymore.

The stock currently offers a forecast yield of around 7.3%. I topped up my holding at the end of last year and may consider doing so again at current levels, if funds permit.

The risk, of course, is that current weakness and cost pressures will persist or worsen more than expected. That can’t be ruled out, but for me, the company’s 110-year history (founded in 1915) and family ownership provide some comfort in this regard.

I’m obviously biased as a shareholder, but on balance I think James Halstead is too cheap at current levels. The fact that the shares have risen today even though broker forecasts have been downgraded suggests the market may share this view.

The stock is relatively illiquid and probably not suited for short-term trading. But on a longer-term view, I think this could be a significant opportunity. To reflect this view, I am going to leave Graham’s previous GREEN view unchanged today, despite these results technically being a (small) profit warning.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.