Good morning!

After yesterday's strong early gains, markets stabilised. The FTSE is set to open up 50 points today, around 10,630.

The Strait of Hormuz remains effectively closed for now: Bloomberg reports that only three ships were seen leaving the region yesterday, compared to a peacetime average of 135. The three ships that left were all linked with Iran.

It's also rumoured that Iran has been charging c. $2m for safe passage through the Strait. Hundreds of trapped ships in the region are waiting for clarity on when and how they can leave.

Meanwhile, the ceasefire itself is fragile. Israel has just heavily bombed Hezbollah in Lebanon, which Iran says is a violation of the agreement.

Overnight moves:

- Brent crude is up $2 at $95

- Gasoil is up $50 at $1,150

These high fuel prices, along with their overnight moves, demonstrate that we are still some distance from a return to normal.

All done for today, cheers! Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

British American Tobacco (LON:BATS) (£96.1bn | SR89) | Dragos Constantinescu will be CFO from September 2026. Currently CEO of Asahi Europe & International. Previously spent 16 years at BAT. | ||

Great Portland Estates (LON:GPE) (£1.25bn | SR27) | Letting of the remaining office space at SIX St Andrew Street, EC4, to an AI company. The building now generates £8.8m of annual rent. AI-related customers represent 11.7% of GPE's total office portfolio | ||

ME International (LON:MEGP) (£534m | SR81) | ME Group will install and operate Wash.ME laundry machines at ASDA sites across the UK. Targeting up to 700 laundry machines. The current total is >7,600 laundry machines. The long-term target is 20,000+. | AMBER/GREEN = (Graham) These shares are still nicely cheap after retreating from the 225p high seen last year. Growth forecasts in the short-term aren’t too impressive but long-term, the company is planning to approximately treble the size of the laundry business from its current size. Overall, a moderately positive stance from us continues to make sense to me. | |

Foresight group (LON:FSG) (£425m | SR80) | AUM +6% (£14bn). FUM +4% (£10bn). Record annual fundraising in higher margin retail vehicles. FY26 adjusted EBITDA to be in line with market expectations (consensus range: £65.2 million - £70.2 million). | AMBER/GREEN ↓ (Mark) | |

ITM Power (LON:ITM) (£398m | SR17) | The UK government backs ITM with a £40m equity investment through Great British Energy Group Limited and a £46.5m grant from the Department for Energy Security and Net Zero. The funds will support the establishment of a new large-scale automated manufacturing line. | ||

Avacta (LON:AVCT) (£311m | SR25) | Updated preclinical and translational data on the Gen Two AVA6103 program will be presented at the American Association of Cancer Research Annual Congress in San Diego on 21 April 2026. Initial clinical data in the AVA6103 program are anticipated in late H2 2026. A clinical data update on Gen One AVA6000 clinical data from the Phase 1a and 1b cohorts is expected in H1 2026. | ||

Gooch & Housego (LON:GHH) (£223m | SR62) | H1 revenue £81.9m, up 9.1% organically. Constant currency increase in the order book of 16.5% (to £167m). Net debt £37m. The Group continues to expect trading for FY 2026 to be in line with management's expectations. | AMBER/GREEN ↑ (Graham) Current organic growth rates are very encouraging, and the acquisitions are doing well. So there are enough positives for me to respect the momentum at play here, and bump this up by one notch to AMBER/GREEN. Honestly, though, it’s not one that I’m drawn to - it has a long history of pretty average returns for investors, which is not that surprising for a manufacturer. | |

Helios Underwriting (LON:HUW) (£140m | SR44) | The 2023 mid-point forecast improved to 17.0% in line with expectations, in the final quarter and these profits will be realised in May 2026. 2024: starting to see the mid-point forecast gradually improving to 9.3% profit on capacity, and the year is tracking towards a strong ultimate result. | ||

Mkango Resources (LON:MKA) (£122m | SR9) | HyProMag GmbH has completed the first commissioning runs for the commercial scale Hydrogen Processing of Magnet Scrap. | ||

Devolver Digital (LON:DEVO) (£107m | SR55) | Revenue +3% to $107.9m, Adj. EBITDA +19% to $11.4m, Adj EBIT $1.4m (FY24: $2.8m loss). Net Cash $36.6m (25H1: $34.7m). Outlook: Expect to deliver continued revenue and Adjusted EBITDA growth in 2026. Adjusted EBITDA is expected to be significantly first half weighted due to the pace of scheduled game releases. | AMBER = (Graham) [no section below] DEVO issued a confusing trading update last month. Today’s full-year results, not content with providing an adjusted EBITDA figure ($7.1m), also provide us with something called “adjusted EBITDA before performance-related impairments” ($11.4m). What would Charlie Munger think? The statutory loss is a whopping $16m. Commentary highlights that the impairment is “non-cash”, but this is misleading: the impairment has been triggered by weaker-than-expected sales and reduced sales projections - sales presumably have something to do with cash? I also note $3.7m of share-based payments, much larger than the company’s adjusted operating profit . On the positive side, the company did still finish the year with net cash of $36.6m. So I’ll leave our neutral stance unchanged. | |

Somero Enterprises (LON:SOM) (£99.8m | SR72) | Buyback expanded from $4m to $6m. M&A: “Taking a highly selective and disciplined approach, with a focus on small to mid-sized, complementary opportunities that align closely with Somero and its long‑term strategy.” May use limited debt. | AMBER = (Mark) The company certainly seems keener to pursue an acquisition-led growth strategy than in the past. However, this is probably a reflection of the maturity of their key laser screed products and the failure of their innovative products to gain traction in their end markets. Acquisitions certainly have the ability to be earnings-enhancing if paid for in cash or by taking on debt. However, they also increase the risk. There is a reason this highly cyclical business has always run with net cash: to survive the downturns. With no actual deal announced to judge, I keep our neutral view. | |

Strix (LON:KETL) (£86.4m | SR82) | £10m returned at 43p/share at 10.5% premium to last night’s close, 10.1% of the issued share capital. | RED = (Mark) On one level, it is good to see management returning cash rather than holding onto it or engaging in empire building. However, buying back shares at almost a 20x forward P/E just doesn’t make sense from a rational capital-allocation perspective and simply underscores why we are negative on this business at the current valuation. | |

Zephyr Energy (LON:ZPHR) (£71.4m | SR25) | Involved the diversion of a single payment to a contractor and resulted in funds of £0.7m being transferred to a third-party account. No impact to operations. | ||

Intercede (LON:IGP) (£46.9m | SR41) | FY26 Revenue -3% to £17.2m (CCY -0.5%). Recurring revenues £11.4m, 66% of total. Net Cash £20.0m (FY25:£18.7m). New orders worth $5.2m in aggregate including a $3.5m MyID CMS renewal from a longstanding US client. | ||

Celebrus Technologies (LON:CLBS) (£36.7m | SR53) | FY26 revenue expected to be approximately $23.3 million, broadly in line with expectations. (Consensus $24.1m) Software $20.0m (FY25: $30.3m) of which Celebrus software $9.4m (FY25: $13.3m). Celebrus ARR +10% to $15m. Net cash $32.0m (FY25: $31.5m). FY27: “...we have started FY27 with a good influx of new leads.” | BLACK (AMBER/RED ↓) (Mark) Roughly in line figures for FY26 quickly become a huge profits warning once the brokers forecasts are revealed. FY27 becomes loss-making and FY28 sees $10m cut from revenue and PBT slashed from $5.0m to just $0.7m. Given that the shift to SaaS billing began in 2021 and last year’s change of revenue recognition will already be in forecast numbers, management are running out of excuses. Things look slightly better on the cash flow front as they continue to hold a large cash balance and generate enough FCF to pay their forecast 3% dividend yield. However, the shares still price in significant recovery outside the forecast window. Something that has so far eluded them. With the company looking expensive on new forecasts, even taking into account the large cash balance it makes sense to downgrade our view following this large profits warning. | |

Van Elle Holdings (LON:VANL) (£35.7m | SR90) | 52.3p in cash, a 59% premium to last night’s close. | PINK (Mark) This looks like a done deal to me, and one that most shareholders will welcome with open arms. Recent history suggests that Van Elle’s assets will generate higher returns when operated by someone else under a different corporate structure. Getting a 5% premium to book value for these looks like a win-win for all concerned. | |

Rentguarantor Holdings (LON:RGG) (£34.2m | SR18) | Revenue +105% Q-o-Q, exceeding Company forecasts. Cautiously optimistic that its FY 2026 revenues will be ahead of current market expectations. | AMBER ↑ (Graham) | |

ImmuPharma (LON:IMM) (£23.4m | SR7) | Thanks shareholders for supporting £6m Lanstead Placing. Successful fundraising extends the Company's cash runway to at least H2 2028. | ||

Lexington Gold (LON:LEX) (£15.4m | SR7) | Continues to make steady progress on the Jelani JV project's mining right application which remains on track for submission during Q2 2026. Refining and enhancing the Jelani JV project's technical study. | ||

MobilityOne (LON:MBO) (£14.6m | SR74) | Confirms it has secured a full-fledged Shariah-compliant Islamic digital banking licence from the Labuan Financial Services Authority. |

Graham's Section

Rentguarantor Holdings (LON:RGG)

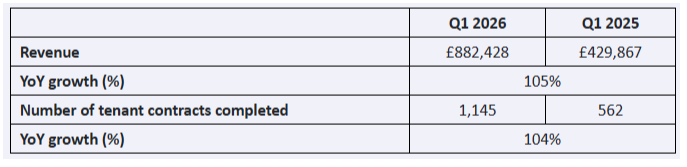

Up 15% at 27p (£39m) - Quarterly Trading Update - Graham - AMBER ↑

I stayed RED on this last month, at the full year results (share price at the time: 28.9p).

But Q1 revenue was up 105% year-on-year, which “materially exceeded Company forecasts”.

Quarterly revenue was £880k vs £430k in Q1 last year:

Should the current performance continue, the Company is cautiously optimistic that its FY 2026 revenues will be ahead of current market expectations.

Here’s a snippet from the CEO comment:

"This growth was a consequence of the substantial increase in tenant contracts signed during the period - 583 more than the corresponding quarter last year. This, I believe, demonstrates the success of our marketing strategy, with plenty of positive momentum generated ahead of the implementation of the Renters' Rights Act on 1 May 2026, which has the potential to create significant opportunities for the Company.

Operational highlights:

Two-year strategic partnership with the National Residential Landlords Association (great for advertising the service to landlords)

Extended partnership with Rob Rinder (“Judge Rinder”!)

Agreement with mydeposits to develop a rent deposit product

Graham’s view

I’m always going to be nervous if I have a negative stance on a rapidly growing company, even if I fear that it’s overvalued.

New estimates from Allenby for 2026 (our thanks to them) are as follows:

Revenue £4.6m (upgraded from £4.0m)

Adj. PBT £302k (upgraded from £240k)

Net cash £2.15m

Valuation is still very high.

The price to sales multiple is now 8.5x, having previously been 10x.

There is still no sensible earnings multiple.

And I also have one or two qualms about the profit forecast. Forecasts are based on “adjusted” measures, and last year RGG excluded some of their marketing spend - which I thought wasn’t quite right.

Nevertheless, I am now inclined to take this off the RED list.

While the stock is still very expensive compared to current financials, it’s also true that the business is:

growing very rapidly

beating expectations and possibly turning a profit (depending on the adjustments involved)

holding a reasonable amount of cash

I’m therefore taking this all the way up to neutral, as I previously promised to do in these circumstances.

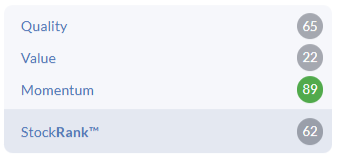

The StockRank is only 18 and it’s considered a “Momentum Trap”, so bear that in mind:

But I’ll be watching closely for more good news.

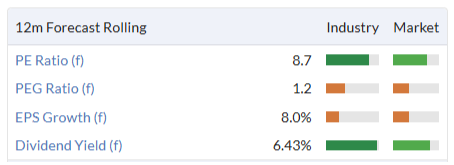

ME International (LON:MEGP)

Up 4% to 147p (£553m) - New Partnership with ASDA - Graham - AMBER/GREEN =

Solid news here from ME Group, the company behind many of the machines you find at shopping centres: photo-booths, laundry machines and children’s rides.

Wash.ME laundry machines will soon be found at ASDA Supercentre, Superstore, supermarket and petrol forecourt sites across the UK.

Some data points:

700 new machines to be installed at ASDA

Current total number of Wash.ME laundry machines: 7,600 in 12 countries.

Overall plans for ME Group this year: install 1,300 new machines (similar to the prior year).

So the ASDA deal should be a big help for this year’s overall growth plans.

Deputy CEO comment by Vladimir Crasneanscki (son of founder Serge):

"ASDA is a perfect company to partner with, their retail and petrol stations are excellent locations for our services and their innovative and fast-paced approach will enable us to deploy our units rapidly… this is the largest single client deal in the history of our laundry division and demonstrates the growing demand for our services."

Graham’s view

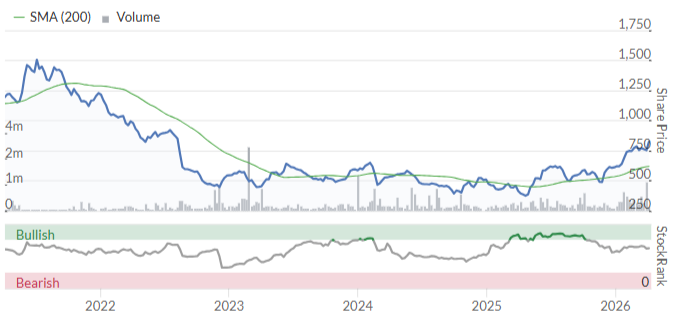

Roland covered MEGP’s annual results in some detail last month - there was quite a lot to digest considering that the results had been delayed, the shares suspended, and an accounting error discovered.

The shares were suspended for a few weeks in March; when they came back, the share price actually ticked up a little:

And yet they are still nicely cheap after retreating from the 225p high seen last year:

Against that, growth forecasts in the short-term aren’t too impressive. The laundry business is the main growth driver currently (revenue up 17% last year), while the photobooth business is stagnant (revenue down 4%).

Long-term, the company is planning to approximately treble the size of the laundry business from its current size. They must see very considerable demand!

Overall, a moderately positive stance from us continues to make sense to me.

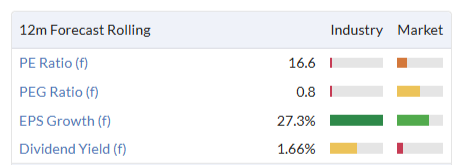

Gooch & Housego (LON:GHH)

Up 9% at 890p (£244m) - Half- Year Trading Update - Graham - AMBER/GREEN ↑

Recent momentum has been encouraging at this photonics business:

Today’s H1 update is merely “in line”, but it has seen the share price rising by nearly 10%. So sentiment must have been pretty sceptical going into it.

Highlights:

H1 revenue +9.1% organically to £81.9m

Organic book up 16.5% organically to £167.3m

The integration of two acquisitions is “proceeding to plan”, with capacity being expanded at both “in response to significantly increased demand”.

Successful acquisitions:

“Phoenix Optical” was bought in October 2024 for up to c. £7m, bringing in around £7m of revenues.

US-based “Global Photonics” was bought in May 2025 for $17.5m, bringing in $11m of revenues.

Balance sheet: net debt of £37m. A new CFO joins the company today.

Outlook: in line with management's expectations.

Estimates: thanks to Cavendish for updating us today. Forecasts are unchanged:

FY26 revenues £175.3m, adj. PBT £16.2m, adj. EPS 45.9p

FY27 revenues £182.7m, adj. PTB £19.5m, adj. EPS 54.3p

Graham’s view

I always struggle to get excited about this one. It always seems to be either not doing very well, or trading too expensively.

The latter is the case currently:

Stylistically, it’s a High Flyer - limited value, but high momentum.

There’s no doubt in mind that it’s a highly reputable company: it has a long history and many locations across the UK, US, Europe. It even has a few sales offices in Asia.

And in addition to its geographic diversification, there is diversification across industries; optical components are widely applicable. GHH sells into the aerospace, defence, industrial, telecoms, and life science sectors.

Current organic growth rates are very encouraging, and the acquisitions are doing well. So there are enough positives for me to respect the momentum at play here, and bump this up by one notch to AMBER/GREEN.

Honestly, though, it’s not one that I’m drawn to - it has a long history of pretty average returns for investors, which is not that surprising for a manufacturer

Mark's Section

Van Elle Holdings (LON:VANL)

Up 53% at 50.5p - Recommended cash offer for Van Elle - Mark - PINK

Congratulations to those who kept the faith here; they are rewarded with a cash offer of 52.3p per share. This is pitched at a sizeable premium to the share price, and not just a recently depressed one:

45.9 per cent. to the volume weighted average price of 35.8 pence per Van Elle Share over the 12 months ended 8 April 2026.

However, this is only a 5% premium to book value, which is not overly generous in these terms. Although I note the acquirer is paying up for the intangible assets, not something that was a given with the recent performance of the business.

We’ve been broadly negative here recently, with our rationale being that:

The discount to tangible assets may still be attractive to some, and may yet lead to a competitor viewing them favourably as an acquisition target. However, over the last few years, they have been very positive about the medium-term outlook for the business, only to repeatedly profit warn due to weak end markets. There are political factors in the UK that may have affected this unexpectedly, and in cyclical markets they will be right one day. However, given all this, I don’t place very much faith in the forecasted strong recovery in 2027 and 2028 and hence it seems too soon to consider upgrading our view.

One of the clues that a catalyst may be on the way was the inclusion of Van Elle in the “Realisation” category at Rockwood Strategic:

The problem was that the company had been in this category at Rockwood for some time. It will have been a long and uncomfortable wait of declining corporate performance for those who are held on for this outcome. It seems that there is no gain without pain when it comes to financial markets!

Support:

Unsurprisingly, Rockwood are supporting this offer with their 17.6% of the equity, as are the directors who are recommending the offer. In addition, Otus Capital Management and Peter Gyllenhammar have given letters of intent for their 26.1% combined. This makes 45%, so while not technically enough to carry a Scheme of Arrangement on its own, it would be a rare shareholder who doesn’t support a deal of this premium when the alternative is weak ongoing corporate performance.

Acquirer:

Strabag SE (WBAG:STR) is an Austrian-listed construction firm with an established presence in the UK since 2011 and is involved in major projects like the HS2 tunnels and the Woodsmith Project for Anglo American. They have a dedicated precast concrete factory in Hartlepool producing concrete tunnel segments for HS2.

Given Strabag’s £9.3bn market cap and reported €3bn of cash, I don’t see why they shouldn’t be able to complete on what is a small bolt-on deal for them.

Mark’s view

This looks like a done deal to me, and one that most shareholders will welcome with open arms. Recent history suggests that Van Elle’s assets will generate higher returns when operated by someone else under a different corporate structure. Getting a 5% premium to book value for these looks like a win-win for all concerned.

Somero Enterprises (LON:SOM)

Up 1% at 188p - Buyback Expansion and Further M&A Framework Detail - Mark - AMBER

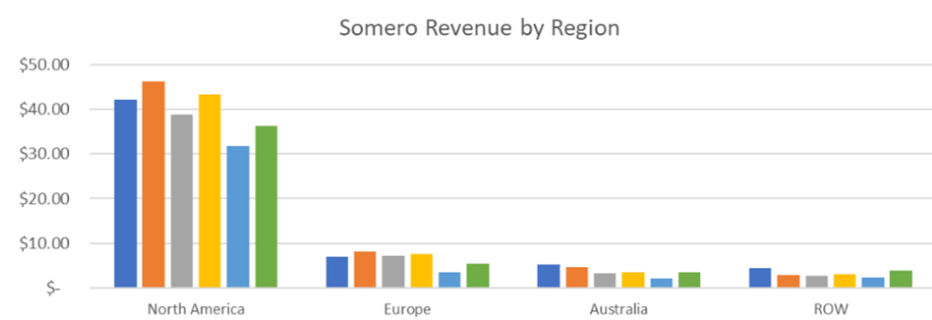

Their ongoing buyback is extended from $4m to $6m. However, I have to question if this is the best use of their cash. Despite recent share price falls, they are still be trading at a mid-teens forward P/E. As I pointed out when I reviewed this for The Week Ahead, this remains almost entirely a play on North American Non-residential construction:

Fuel price rises disproportionately impact US consumers due to lower tax take compared to Europe. So, despite being in a better place overall in terms of energy balance, the US is potentially more at risk of a consumer retail recession, which would reduce demand for warehousing and other key drivers of Somero sales.

The better news is that the company appears to be more active when it comes to growing inorganically, and may be able to take advantage of weak trading elsewhere:

Management has engaged experienced advisors to support market outreach, opportunity assessment, and post-acquisition integration planning, ensuring the Company is prepared should suitable opportunities arise. Any opportunity would be assessed carefully in light of prevailing conditions and alternative uses of capital.

The reality is that the company’s innovations have failed to generate meaningful sales, so organic growth has not materialised. While many customers still buy a Somero Laser Screed for their customer service, you only have to go to one of the industry trade shows to understand that this is increasingly a commodity product. So an increasing focus on growing via acquisition makes sense.

In the past, management have been highly averse to taking on debt. This has meant the company's balance sheet has been bullet-proof, but at the cost of capital and tax efficiency. This is a notable change of tone from a refreshed management team:

The Company's strong cash generation and balance sheet provide flexibility to support targeted opportunities. While debt may be used prudently and selectively, the Company does not intend for it to become a sustained feature of the balance sheet. Any use of debt would be measured, with a focus on maintaining a strong balance sheet and deleveraging following an acquisition in a timely manner.

I wonder if this adds to the risk of the business. The reason the past management were so risk-averse was that they had experienced many cyclical booms and busts in the past. For example, it is likely that the company would have failed in 2008/9 if they hadn’t entered this period with a cash buffer. I am not expecting a downturn this severe to be on the horizon, but if Somero take on debt to make an acquisition, it leaves them more exposed if it did.

Mark’s view

Roland nudged our view up to AMBER following recent results based on the quality of the business and the cash generation. However, he considered there to be better value elsewhere in small-cap land. Today’s announcement doesn’t change that view. There is the potential for them to increase earnings by using their cash balance to acquire other businesses, but so far, no specific deal has been forthcoming. Plus, if they take on debt to do any deals, this will come at the cost of added risk. There was a reason previous management always ran the company with a significant cash buffer, even if it meant lower capital efficiency.

Foresight group (LON:FSG)

Down 4% at 360p - FY26 Trading Update - Mark - AMBER/GREEN ↓

It looks like we haven’t looked at Foresight before on the DSMR. However, I note that Roland wrote about the company as part of his recent look at Jim Slater’s ZULU Principle. The high returns on capital, single digit P/E and forecast earnings growth were enough for Roland to add Foresight Group to the SIF portfolio and to his personal holdings, and for me to add it to my watchlist.

It is perhaps no surprise that the share price performance has been weak in 2026. Being an asset manager usually means geared exposure to markets and this has been a volatile period. Plus the phrase “Private Credit” has become a swear word recently. However, I think there are several reasons why these concerns are likely to be overblown:

When I reviewed Pollen Street recently, I concluded that the type of fund that they operate had little exposure to the events that have given Private Credit a bad name. I expect the same here.

Foresight have much more exposure to infrastructure, an asset class that has historically been far less exposed to economic cycles.

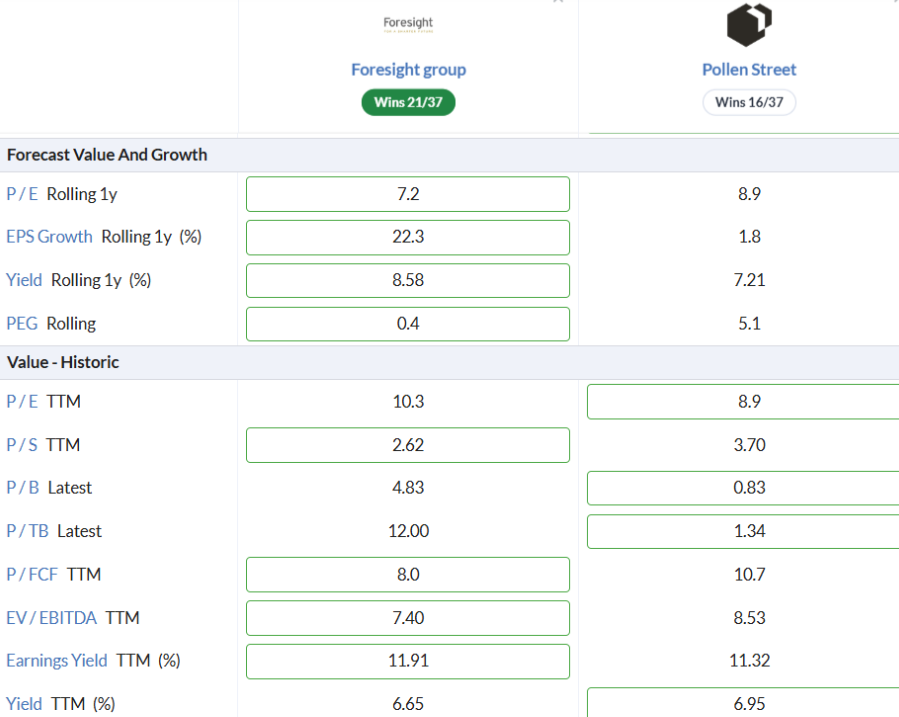

There are some key differences between Foresight and Pollen Street beyond a greater focus on infrastructure. For example, Pollen operates a hybrid model, investing alongside customers, and has a specific focus on European middle-market financial services. However, fundamentally, I consider them peers, largely exposed to the same factors. So it is notable that Pollen has bounced back from recent market-driven weakness and Foresight hasn’t:

This leads to a valuation disparity on forecast numbers, but not historical ones:

Which makes today’s trading update key. This is said to be in line:

We expect FY26 core EBITDA pre-Share Based Payments ("SBP") to be in line with market expectations (FY26 consensus range: £65.2 million - £70.2 million, FY25 actual: £62.2 million).

However, that is quite a large consensus range. We can see notes from Cavendish and Singer, who have £68.2m and £69.0m forecast for Adj. EBITDA, respectively.

Perhaps worryingly, Cavendish’s note today doesn’t update us; they merely say “We will review our forecasts on the back of the announcement”. Singer hasn't published anything this morning, as far as I can see.

Cavendish forecast £10.7bn closing AUM for FY26 and Singer £10.8bn. This is probably why forecasts are under revision, as today’s trading statement looks around 8% shy of these numbers:

Assets under Management ("AUM") and Funds under Management ("FUM") increased by 6% and 4% to £14.0 billion and £10.0 billion respectively.

And these appear to have been helped by FX moves, rather than hindered as is often the case for other companies. It seems that while in-line, results may come in towards the bottom end of guidance range, if AUM is any indication of this.

However, there are signs that growth can continue. For example:

Record annual fundraising of £630 million was achieved in higher margin retail vehicles, a 7% year-on-year increase (FY25: £587 million) and a 93% increase over the last 3 years (FY23: £327 million)

However, a 7% rise would just see them return to the AUM level previously forecast for the period just ended. They are therefore likely dependent on their fund performance for the bulk of the forecast increase in AUM. However, a shift to higher margin retail vehicles may protect profitability, even if AUM ultimately disappoints.

Interestingly, Singer calls Foresight out as a winner from recent global events, saying:

Foresight has a proven origination/deployment/asset management track record in renewable energy generation across Europe. We think that energy independence will re-appear on the political agenda, given the impact of conflict in the Middle East, and institutional investor demand to participate in this theme will redouble – even in light of a higher interest rate backdrop – where Foresight would benefit.

So there may well be long-term upside that is not yet captured in forecasts.

Mark’s view

I view Foresight as a more defensive business than Pollen Street as they are not reliant on the performance of their own invested funds to generate their earnings. I continue to see a lot to like in a growing asset manager on a single digit P/E, although I wouldn’t be surprised if what appears to be an AUM miss leads them to some small downgrades soon.

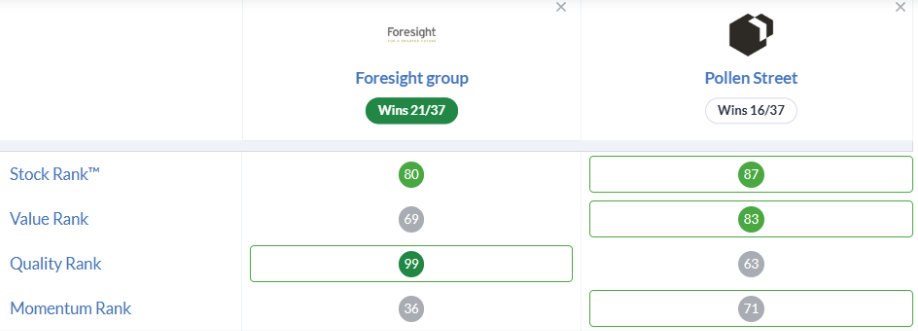

In light of this, Pollen Street has the edge in terms of Momentum:

Whereas we were GREEN on Pollen Street recently, a slightly more cautious AMBER/GREEN view makes sense for Foresight, at least until we have updated broker numbers to confirm whether forecasts have been reduced or not.

Strix (LON:KETL)

Up 5% at 40.7p - Proposed Tender Offer - Mark - RED =

The market has liked this proposed tender offer this morning:

The Tender Offer will return up to £10 million to Eligible Shareholders at a Tender Price of 43 pence per Ordinary Share, representing a premium of 10.5 per cent. to the closing price of 38.9 pence per Ordinary Share on 8 April 2026.

But I see this in a less favourable light. While it is better than the company simply hanging on to the cash, the actual amount means that shareholders will likely only be able to sell around 10% of their holding at this premium:

The Tender Offer will represent up to approximately 10.1 per cent. of the Company's issued Ordinary Share capital as at the Latest Practicable Date.

Directors say they do not intend to participate, but they hold a couple of per cent of the company at best. Everyone else would seem daft not to tender as much as possible.

Zeus are forecasting 3.5p of adjusted EPS for FY26, but this is a 15-month accounting period and includes the recently sold Billi business. Going forward, EPS is forecast to be 2.2p for FY27 and 2.3p for FY28. So the company is tendering for shares on close to 20x forward earnings. At current interest rates, this is only slightly better than keeping the cash and putting it in gilts!

The company has net cash and continues to have an ongoing buyback. However, the same argument applies to these shares bought. At this level, it may be destroying shareholder value rather than enhancing it.

Clearly, management feels that, with the balance sheet rebuilt following the sale of Billi, there will be a cyclical recovery in the core business outside the current forecast window that will make these repurchased shares look like good value. However, given recent history, I have my doubts. It may well be that management is hanging on to past glories and anchoring on previously higher share prices.

Following the sale of Billi, the shares trade at a discount to Book Value, which may be part of the rationale, but they are still buying back shares at a premium to Tangible Book Value, and there is no sign that these assets will be made productive any time soon.

Mark’s view

On one level, it is good to see management returning cash rather than holding onto it or engaging in empire building. However, buying back shares at almost a 20x forward P/E just doesn’t make sense from a rational capital-allocation perspective and simply underscores why we are negative on this business at the current valuation. RED

Celebrus Technologies (LON:CLBS)

Down 11% at 84p - Trading Update - Mark - BLACK/AMBER/RED ↓

Here’s the key bit for the year just ended:

Full year revenues for FY26 are expected to be approximately $23.3 million, broadly in line with expectations (FY25: $38.7 million), and at the pre-tax level we expect an adjusted loss before tax of approximately $0.2 million (FY25: profit of $8.7 million), slightly ahead of expectations and reflecting careful cost control through the second half.

Broadly in line is, of course, market code for slightly below, by about 3% in this case. This doesn’t seem like the end of the world, and they say their adj. LBT is ahead of expectations. However, losing less money than expected isn’t anything to write home about.

ARR increases, but it appears by much less than expected:

Celebrus ARR is expected to be $15.0 million (FY25: $13.6 million), an increase in the year of 10.3%. From an existing customer perspective, FY26 had a Net Revenue Retention of 97.6% through securing renewals across the business, along with some uplifts. Two existing banking customers, however, reduced their banking footprint through divestitures, which meant a reduction in the Celebrus software fees during those renewals. New business, via direct and partners, underdelivered against our expectations. Several deals at contractual stage in Q4 were lost or further delayed, which ultimately brings us to the Celebrus ARR for the year as outlined.

$15.0m is below the $15.6m ARR reported at the half year.

This is problematic. The narrative from the company has been one of temporarily depressed profits while they pursue a transition to a SaaS model. However, they began this transition in 2021, so if customers were previously signing 3-year deals, this should have all worked its way through by around 2024. Yet here we are, 5 years later, trying to deliver SaaS growth.

Profitability isn’t helped by a change in revenue recognition:

From 1 April 2025, the Group introduced a number of changes to its commercial contractual arrangements with customers which impact accounting for contracts including the definition of cost of sales, the segmentation of revenue type and the move to straight line revenue recognition of future license revenues.

However, again, you’d expect these sort of changes to gradually work their way through to give zero net impact after a few years. Which makes it partially disappointing that Cavendish make huge cuts to forecasts again today. The $10m reduction in revenue for FY28 and the cut from $5.1m PBT to just $0.7m is not down to revenue recognition this time.

The company continues to hold a large cash balance of $32m, and only around $5m of this was due to payment of upfront license fees at the half-year, meaning the average cash balance isn’t likely to be far off that level. This may be one reason that the share price hasn’t fallen anywhere near as much as the forecast drop in profit forecast.

Free Cash Flow is better, and the EV prior to today’s fall was just $23m. However, Cavendish is forecasting $1.2m FCF for the current year, putting this on a forward EV/FCF of around 19. Even in FY28, the FCF only just covers the forecast 3% dividend.

Mark’s view

Despite losing over 2/3rds of their value over the last year, the shares don’t look cheap:

The reality is that the forecasts have fallen by more than this amount. The company is running out of excuses for this underperformance. The shift to SaaS that began in 2021 really should have worked its way through by now, and the change to revenue recognition last year should have already been in forecast numbers.

Roland took an AMBER view following their H1 Trading Update. However, with huge downgrades to future forecasts today, it would seem sensible to knock this down further to AMBER/RED.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.