Good morning!

Markets are a little jittery this morning as President Trump says that the US is going to blockade all Iranian ports (starting at 6pm UK time). Negotiations between the US and Iran appear to have completely broken down.

Equity markets are set to open lower:

- The FTSE is opening down 60 points at 10,540

- The German DAX 40 is down 1.4%

- The S&P 500 is trading down 0.6% overnight

And energy prices are higher:

- Brent crude oil is up $5.50, approaching $99

- Gas Oil (diesel) is up 8% at $1,236

- UK Natural Gas is up 10% at 119p

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

GSK (LON:GSK) (£88bn | SR94) | Mocertatug rezetecan achieved confirmed objective response rates of 62% in platinum-resistant ovarian cancer (PROC) and 67% in recurrent or advanced endometrial cancer (EC) in BEHOLD-1 study. Promising efficacy and safety supports start of five phase III trials in 2026. | ||

National Grid (LON:NG.) (£67bn | SR67) | Performance in line with expectations and consistent with previous guidance. However, now expects a net impact of c.1p per share to underlying EPS related to customer refund charges in New England, related to a March judgement. | ||

Halma (LON:HLMA) (£15.8bn | SR70) | Acquired US firm Surgistar for $90m as a bolt-on to Healthcare subsidiary MicroSurgical Technology. Surgistar designs and manufactures ophthalmic surgical instruments. | ||

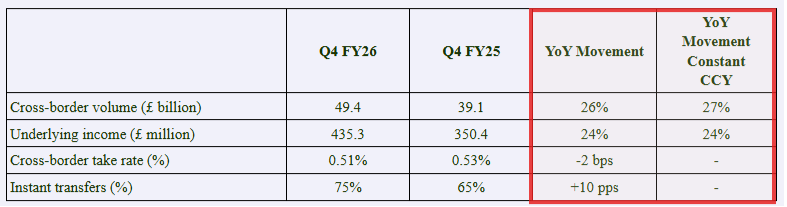

Wise (LON:WISE) (£12.1bn | SR44) | Q4 FY2026 Trading Update & Translation of IFRS financials into US GAAP | Cross-border volumes up 26% to £49.4bn, underlying income up 24% to £435.3m. Take rate reduced from 0.53% to 0.51%, percentage of instant transfers +10% to 75%. Expect FY26 underlying PBT margin to be towards the top of the 13-16% range. | GREEN = (Graham) I’m inclined to leave our GREEN stance unchanged here. At current growth rates, the investment thesis is fundamentally intact. I make some further comparisons with valuation at the privately-held Revolut, where I think that relative value arguments do favour Wise. |

Energean (LON:ENOG) (£1.60bn | SR53) | Energean Power FPSO is now fully operational and delivering gas to customers in line with contractual requirements. | ||

Sirius Real Estate (LON:SRE) (£1.58bn | SR75) | FY26: 18.4% YoY increase in rent roll, including +6.4% like-for-like. Expect to deliver FY results in line with expectations. | ||

Vistry (LON:VTY) (£1.08bn | SR80) | Adam Daniels has been appointed as CEO with immediate effect. He is currently the Executive Chair of one of Vistry’s two largest operating divisions. | ||

Polar Capital Holdings (LON:POLR) (£638m | SR94) | Q4 25 AUM +8% to £30.6bn at 31 March 26. Net inflows of £1.4bn, market gains of £0.8bn. Outlook: “entered 2026 with positive net inflow momentum […] but mindful of structural challenges facing the industry”. | ||

Custodian Property Income Reit (LON:CREI) (£431m | SR71) | Update on the Strategic Acqiusition of £36m Grove Court Portfolio | Secured 5% increase in passing rent with the portfolio’s largest tenant, a motor dealership that accounts for 27% of Grove Court’s rent roll. GC Portfolio occupancy remains at c.97%. | |

Concurrent Technologies (LON:CNC) (£181m | SR51) | Board Changes & Final results for the year ended 31 December 2025 | Revenue up 14%, pre-tax profit up 25% to £6.5m. Order intake increased “to a record £47m” driven by defence demand. FY26 outlook: “confident of delivering results for FY26 in line with market expectations”. | |

Roadside Real Estate (LON:ROAD) (£105m | SR24) | Acquiring a portfolio of 12 “premium-quality operational petrol station forecourts” and a convenience store clustered predominantly in Cumbria. Hoch had gross assets of £13.7m and generated a pre-tax profit of £1.8m in the year to 31 March 2025. Purchase will be funded with a new £25m HSBC bank facility and additional debt from Tarncourt (a related party to the CEO). | ||

EKF Diagnostics Holdings (LON:EKF) (£104m | SR50) | Agreed to acquire Beep Insights Technology, “an IOS and Android software application that combines data from sports performance wearables connected via Bluetooth with real-time glucose and lactate tracking to give personalised metrics to improve sport's performance training.” | ||

Journeo (LON:JNEO) (£73m | SR50) | Agreement to supply bus stop infrastructure for a large local authority in the South of England, a longstanding existing customer. | ||

Ondine Biomedical (LON:OBI) (£57m | SR4) | 2025 revenue rose by 29%, in-house capacity upgrades underway to support future growth. Completed patient enrolment in LANTERN Phase 3 US trial. | ||

MTI Wireless Edge (LON:MWE) £55m | SR98) | Received order from an existing customer to supply military antennas worth c.$2m to a local defence company. Expected to deliver in 2026/27. | AMBER/GREEN = (Roland) [no section below] Assuming equal delivery over 2026 and 2027, today’s order news will equate to c.$1m of revenue and perhaps $100k of operating profit in each year. This is less than 2% of last year’s full-year figures. There’s no change to broker forecasts from Shore Capital or Allenby today, so I’m left with the conclusion that today’s contract wins are most likely business as usual and already reflected in existing forecasts. While I think current forecasts are more likely to be upgraded than downgraded, that hasn’t happened yet. I was moderately positive following a similar update last week. I do not see any reason to change this view today, especially given the rising valuation here – I estimate the shares are now trading on c.16x FY26E earnings. | |

Marks Electrical (LON:MRK) (£50m | SR49) | FY March 2026 revenue £108.5m. Adj. EBITDA £2.65m and net cash £4.45m, both ahead of the range previously indicated. “The Group enters FY27 with positive trading momentum and a strengthened cash position.” | ||

Calnex Solutions (LON:CLX) (£43m | SR51) | Trading slightly ahead of market expectations. Revenue +19%, and an improvement in profitability. Cash £9.3m. “The progress achieved in FY26 provides a strong foundation for continued profitable growth through FY27 and FY28.” | ||

Edx Medical (OFEX:EDX) (£40m | SR1) | “...the Company will continue to require capital to fulfil its potential… its access to capital from certain funds, its liquidity profile and visibility to investors will be improved by the AIM Admission.” | ||

Churchill China (LON:CHH) (£33m | SR83) | Revenue down 2.6%. PBT down 29% to £4.4m. Has forward purchased 64% of its gas requirements for 2027. “...it is only in a prolonged conflict with dramatically increased pricing, that this would materially impact the expected results.” | AMBER/GREEN ↑ (Roland - I hold) I am tentatively moving to a more positive view as today’s results are in line with expectations and show the company continuing to invest in long-term sustainability while staying focused on its core business model. The 7% dividend yield is comfortably supported by cash flow while the discount to book value improves the potential returns on offer for new buyers. The main medium-term risk, in my view, is that structurally high UK energy costs will continue to put pressure on profitability and make it progressively harder for Churchill to maintain its competitive advantages. | |

Arecor Therapeutics (LON:AREC) (£24m | SR10) | Lead product AT278, designed to transform Automated Insulin Delivery systems, has advanced across both product development and commercial partnering. 2025 continuing operations: revenue £1.7m (2024: £1.6m). Cash £6.1m. | ||

Cambridge Cognition Holdings (LON:COG) (£18m | SR20) | Orders up 73%, order book up 21%, but revenue down 10% (£9.4m) due to weak opening order book. Adj. EBITDA loss £0.5m. Cash £1.1m. Now expects 2026 revenue of £9.5m, up from £8.8m expected at year-end. Positioned “for growth in revenue, earnings and cash generation in 2026.” | ||

SysGroup (LON:SYS) (£11m | SR36) | FY March 2026: revenue +7.6%, adj. EBITDA £1.2m, ahead of market expectations. Net cash £2.7m. “Entered FY27 with positive momentum”. | ||

Mothercare (LON:MTC) (£8m | SR39) | Retail sales by franchise partners fell 22% to £180m. Adj. EBITDA £1.25m. Net borrowings £5.7m. Pension deficit £35m. |

Graham's Section

Wise (LON:WISE)

Up 6% to £10.26p (£10.5bn) - Q4 FY2026 Trading Update - Graham - GREEN =

Thank you to David Wordsworth in the comments for providing early comments on this one.

Let’s do a quick recap of this rapidly growing fintech’s progress.

Quarterly cross-border volume +26% year-on-year to £49.4bn

Quarterly active customers +22% year-on-year to 11.3m

Customer holdings +37% year-on-year to £29.4bn

In table format:

They continue to accept a lower “take rate” (fee on currency conversion), with this rate falling further to 51 basis points (0.51%).

When I looked at the Q3 update from Wise in January, I noted that the take rate had fallen year-on-year from 56 to 52 basis points. So the decline continues.

This reflects “a balanced approach to investing in price and the business to support long-term growth”.

I hate the phrase “investing in price” but it gets the message across. Growth is clearly the priority, and the company is still very profitable.

On the subject of profits:

Continue to expect FY26 underlying PBT margin to be towards the top of the 13-16% range (including costs related to the Dual Listing) as we remain focused on investing in long-term growth and becoming 'the' network for the world's money

US dual listing: FY26 results will be presented in USD and in accordance with US GAAP (generally accepted accounting principles). The LSE listing will be the company’s secondary listing, while the US listing will be primary.

What this says to me is that the company’s future investor communications will be directed primarily towards US-based investors.

CEO comment:

"We are making good progress on building the network for the world's money. Our infrastructure makes cross-border transactions cheaper and faster and, in January, we became one of the first payment institutions to be granted membership to Payments Canada, paving the way to direct access there.

More and more people are using Wise at home or abroad for their everyday spending, for paying bills, for savings and investments. That's why last month we formally launched our UK current account with a physical branch concept on Oxford Street in London."

Graham’s view

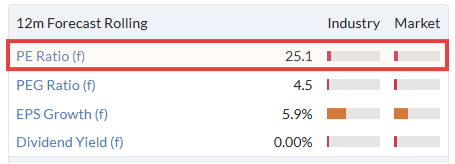

I updated our stance on this to GREEN in January (at 954p), and don’t regret doing that. For high-quality businesses, P/E multiples of 20+ don’t scare me away (but this earnings multiple is complicated - more on that shortly).

Why pay up for Wise? In one sentence: rapid growth, huge ambitions, and the potential for valuable network effects as a provider of currency market infrastructure used not just by individuals but by major institutions.

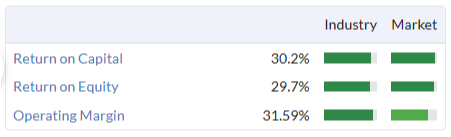

And it’s not just a story about hope for the future. The business is already highly profitable:

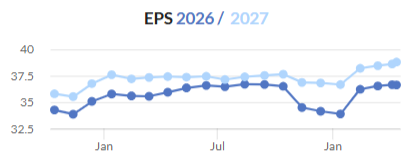

And earnings forecasts have held up pretty well over the past year, even rising:

Wise’s market cap today is equivalent to $14bn, still just a fraction of the $75bn valuation at which Revolut raised money late last year.

They are very different businesses, but at a high level:

Revolut 2025 revenue $6bn, PBT $2.3bn

Wise FY March 2026 revenue £1.74bn / $2.3bn, underlying PBT c. $370m at a 16% underlying margin.

Revolut is winning when it comes to size, growth and profitability. So in that sense its higher valuation makes a lot of sense. But let’s pin down some of the big-picture differences in valuation.

On price to trailing sales, Revolut is twice as expensive:

Price to trailing sales: Revolut 12.5x, Wise 6x

However, Wise appears to be more expensive when it comes to the trailing earnings multiple:

Price to trailing PBT: Revolut 33x, Wise 38x (on underlying PBT)

The Wise earnings multiple is complicated by the fact that its “underlying” earnings are much lower than actual earnings.

This goes back to the fact that Wise is an electronic money institution, not a UK bank, which restricts its ability to pay interest on client balances.

Long-term, Wise intends to pay out far more interest to clients than it currently does. Therefore, its “underlying” PBT ignores the interest earned by Wise that it would like to pay to customers, but is forced to keep for now by regulations.

It’s a very conservative way of looking at things, but I do think that underlying PBT is a useful measure.

Unfortunately, it does add a wrinkle to valuation: do we use the actual profits used by the company, or the (lower) profits that they would prefer to earn?

Those hypothetical lower profits would probably be accompanied by much faster growth, which would increase profits over time. So actually I think investors can use whichever earnings measure they prefer when it comes to valuation.

Overall, I’m inclined to leave our GREEN stance unchanged here. At current growth rates, the investment thesis is fundamentally intact.

As an aside, I note that the IPO price five years ago was £8, and the share price has really struggled to stay above this level. But revenues are up by 300% over this timeframe:

Churchill China (LON:CHH)

Up 8.5% at 325p (£36m) - Final Results - Roland - AMBER/GREEN ↑

(At the time of writing, Roland has a long position in CHH.)

Churchill China plc (AIM: CHH), the manufacturer of innovative performance ceramic products serving hospitality markets worldwide, is pleased to announce its Final Results for the year ended 31 December 2025.

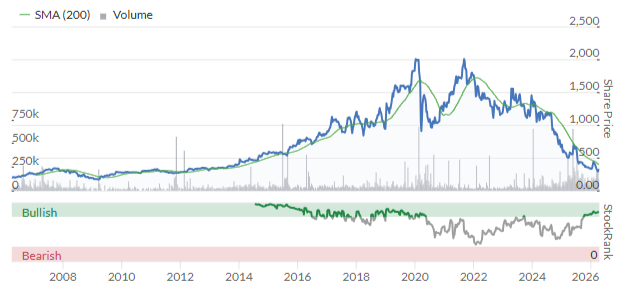

The twin headwinds of high UK energy costs and subdued demand have seen shares in Churchill China fall to 14-year lows in recent months:

Today’s results have received a relatively positive reception, with the company reporting market share gains and reminding shareholders that it has hedged most of its gas requirements for 2026 and 2027.

The hedging had previously been disclosed so shouldn’t be a surprise, but after a difficult few years it is a relief to see that today’s results are largely in line with expectations, albeit down on 2024.

2025 results summary

Revenue down 2.6% to £76.3m

Pre-tax profit down 29.4% to £6.0m

Earnings per share down 31.4% to 39.7p

Dividend down 44.7% to 21.0p per share

Net cash up 6.9% to £10.8m

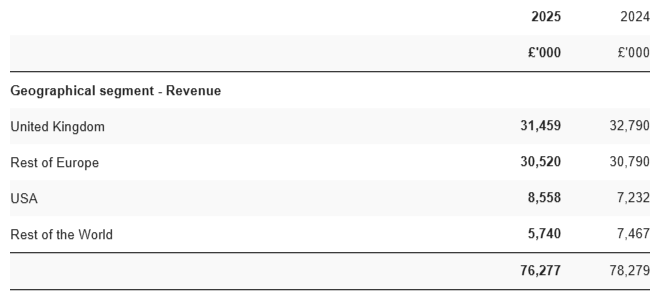

Trading in the UK weakened slightly during the second half, which the company attributed to political uncertainty ahead of November’s Budget. In Continental Europe, the company’s largest market, the second half was stronger than H1 leaving full-year performance unchanged.

Sales rose in the US, where Churchil reports minimal impact from tariffs, due to the higher tariffs applied to Asian exporters relative to the UK.

The main area of weakness was the Rest of the World – markets where Churchill is more reliant on new installations (rather than replacement purchases). For obvious reasons, new restaurant openings remain subdued in many markets:

Profitability: Lower sales volumes combined with a planned reduction in inventories to reduce manufacturing volumes last year. Factories such as Churchill’s have relatively high fixed costs, so when production falls below optimum levels, the business can suffer from negative operating leverage.

We see this in today’s results, with profits falling by c.30% despite sales that were only 3% lower. As a result, the group’s operating margin fell by almost 3% to 7.4% (2024: 10.2%).

Investing for the future: Last year’s £2m reduction in inventories was enough to offset most of the £2.5m in capital expenditure for the year. As a result, the group’s year-end net cash position improved – not a bad result in the circumstances.

Despite the current cyclical slowdown, the group is continuing to invest heavily in new technology to cut energy usage and increase automation. This should leave the business well positioned for a return to sustainable growth in the future. Among the changes made this year were:

Completed commissioning of new plate making equipment “which is both more agile and energy efficient”.

Replaced “two more gas fired glazing pre heat units” with electrical units, delivering a 4% reduction in energy consumption (and carbon emissions) and improving yields.

Automated “a large proportion of our packing process leading to significant cost saving”.

Planning further equipment replacement and modernisation.

Lower inventories didn’t impact the company’s strong stock availability and “market leading reputation for service”. According to management, 98% of orders were delivered within 48 hours in 2025, with more than 70% of European orders fulfilled within 24 hours.

Leveraging its distribution network: to drive growth and take advantage of its strong distribution and sales network, the company says it’s “reviewing opportunities to distribute non-ceramic products in the same product areas”.

Management says this could be done through an acquisition or through exclusive distribution agreements with other suppliers, creating “an additional growth path”.

If it’s well executed, I think this could be a positive strategic move for the group. I’ll be interested to learn more in due course.

Valuation: too cheap?

Using today’s results, my sums give a return on capital employed of 8.1% and a return on equity of 7.2%. Both figures are likely to be below the level needed to cover the cost of capital for a small manufacturing business of this kind.

Although the shares look cheap on a P/E of around 8, it’s important to consider the risk that Churchill will not be able to rebuild margins sufficiently to generate attractive returns.

This risk is reflected in the stock’s deep discount to book value, but I think this could also represent an opportunity if profitability does recover over time.

My sums give a net asset value of 560p per share based on today’s result. This falls to 486p if I take a more conservative approach and strip out intangibles and the £7.7m pension surplus.

With the shares trading at 325p as I write, Churchill is trading at a discount of between 33% and 42% to its book value.

This can be an important consideration for investors in value situations, because buying at a discount to book value increases the return on cost of equity achieved on an investment:

Paying 325p for shares in a business with earnings of 40p per share implies a return on cost of equity of 12.3%;

This is substantially higher than the 7.2% return on equity that would be achieved if the shares traded at book value.

Outlook

Perhaps understandably, given the situation in the Middle East, Churchill has not included any concrete guidance for 2026 in today’s outlook statement. However, management did include a comment on energy costs, suggesting that a material impact remains unlikely at this stage, or at least is not imminent:

The outbreak of the Middle East conflict has created uncertainty in the energy markets and, as an energy intensive company, Churchill has exposure to increasing prices. The Group manages its risk exposure and is materially hedged for the year-ahead. In 2026 the Group has open exposure to circa 16% of its gas costs and has forward purchased 64% of its gas requirements for 2027. The Group has modelled the impact of rising costs under a number of scenarios and, whilst profitability would be impacted, it is anticipated that it is only in a prolonged conflict with dramatically increased pricing, that this would materially impact the expected results.

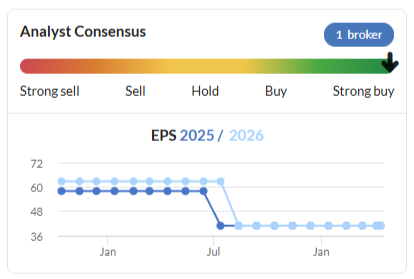

Unfortunately we don’t have access to broker notes for this business, so are left in the dark regarding earnings forecasts.

Prior to today, the consensus figures shown in Stockopedia were for a flat result in 2026, but I would guess these estimates may evolve as the year unfolds:

Roland’s view

Today’s results emphasise the company’s long-term culture and strategy on a number of occasions:

As a company with a long history, our values are well defined. Innovation, cooperation, uncompromising customer service, trust and honesty are the core values that drive our behaviours on a day-to-day basis.

In ESG, Churchill states that its strategy is “to be doing the right thing”:

As a high energy use company and one of the largest employers in the Stoke-on-Trent area we are aware of our responsibilities to the wider community and have made this a part of our DNA.

Investment in areas such as automation and electrification are seen as being a good fit with environmental strategic goals for the group, supporting future profitability and sustainability.

In my view, this strategy reflects the company’s long history as a family-controlled business and perhaps provides some clues as to why Churchill has outlasted so many other storied Stoke-on-Trent potteries.

As someone who hopes to be a long-term shareholder in Churchill, I’m encouraged by the company’s continued commitment to this approach.

Even so, I do remain concerned by the risks that structural high energy costs in the UK could mean that profitability remains persistently challenged at Churchill. With consumer spending remaining under pressure in the UK and elsewhere, I don’t see much hope of a near-term recovery in demand.

We’ve been neutral (AMBER) on Churchill China recently, but today’s results are in line with expectations and show the 7% dividend yield underpinned by cash generation and a strong balance sheet.

Given the discounted valuation on offer, I’m going to tentatively move our view up by one notch to AMBER/GREEN. I note this view is also reflected by the StockRanks, which see this pottery producer as a potential Contrarian stock – a winning style:

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.