Good morning!

Markets are set to open little changed today. The FTSE is at 10,580.

The current US-Iran ceasefire has one week left until expiry.

Late last night, Bloomberg reported that the two sides are now talking about where they might hold face-to-face negotiations to extend the ceasefire. The US blockade of Iran's coastline is now in force.

With macro developments being quieter today, let's focus on company news...

Today's Agenda is complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BP (LON:BP.). (£91bn | SR87) | Reported upstream production in the first quarter is expected to be broadly flat compared to the fourth quarter 2025. The oil trading result is to be “exceptional”. Net debt to rise to $25-27 billion. | ||

Imperial Brands (LON:IMB) (£24bn | SR72) | SP -7% Reiterating full-year guidance. On track to deliver at least high-single digit earnings per share growth and at least £2.2 billion of free cash flow for the full year. | AMBER/GREEN = (Graham) There's no hidden profit warning contained in this update. What we do have are some amber flags: an H2 weighting, a potentially risky shift in strategy, and unimpresive growth from next-gen products. But in reality I think that little has changed. Full-year guidance has been reiterated, and I think it's natural that there might be some profit-taking after a very strong bull run and a lukewarm trading update. So I'll leave our existing moderately positive stance unchanged. | |

Intertek (LON:ITRK) (£5.9bm | SR43) | SP +12% Strategic Review initiated to evaluate the potential separation, either through a sale or demerger, of Intertek Energy & Infrastructure from Intertek. Trading statement: full year guidance confirmed. | AMBER = (Roland - I hold) [no section below] Intertek is considering splitting its business in two by separating its two lowest-margin divisions (2025: 11.1% & 8.7%) from its three higher-margin divisions (2025: 30.4%, 22.6% & 13.0%). The Industry & Infrastructure and Energy divisions both have significant exposure to cyclical sectors such as oil, shipping and automotive, so my feeling is that grouping them could be logical. Perhaps coincidentally, this strategic review follows an extended period of share price underperformance and sluggish revenue growth. My guess is that focusing on its core businesses (ex-infrastructure and energy) might help Intertek regain its previous premium share price rating. As a long-term holder my view on the suggested split is fairly neutral at this stage. From a value perspective, I think Intertek looks more attractive than in the past, but I would note the recent negative trend in earnings forecasts. Given today’s in-line trading update, I’m going to leave our neutral view unchanged today | |

Oxford Instruments (LON:OXIG) (£1.47bn | SR72) | Full-year performance in line with market expectations. Order intake up c. 8% organically, book-to-bill c. 1.07. | ||

Atalaya Mining Copper SA (LON:ATYM) (£1.24bn | SR94) | Q1 production impacted by unusually heavy rains. The Company plans to review its copper production guidance for FY2026 on an ongoing basis. Previously disclosed production guidance was 50-54k tonnes of copper. | AMBER ↓ (Roland) While weather-related disruption is outside the company’s control, I would argue that meeting full-year copper production targets now looks quite challenging without a strong recovery in grade. I don’t know how likely this is. We’ll have to wait until May for the company to provide updated full-year guidance. The other factor to consider is the copper price. Further gains could support higher profits even with lower production. I recognise the opportunity here, but I’d note that 2026 consensus had already drifted lower prior to today. On balance, I think this is a more speculative situation than it was in the past, so I’m moving my view down by one notch to neutral. | |

Pagegroup (LON:PAGE) (£435m | SR51) | Q1 gross profit falls 4.9%. “Resilient performance”, but “Ongoing subdued levels of client and candidate confidence impacting decision making”. CEO: “Whilst we have seen signs of a normalisation in trading in some of our markets, the increased geopolitical and macro-economic risks due to the conflict in the Middle East create a heightened degree of uncertainty in the outlook for the rest of the year.” | BLACK? | |

ACG Metals (LON:ACG) (£356m | SR46) | Revenue $135.6m, adj. EBITDA $76.3m. Net assets $49.8m. “The planned transition to copper production in the middle of 2026 represents an exciting and transformational next phase for the Company…” | ||

Tharisa (LON:THS) (£346m | SR100) | Quarterly PGM production at 34.3 koz, PGM prices averaging at US$3 038/oz (previous quarter: US$2 208). Net cash $54.7m. Guidance: Production guidance for FY2026 is set at between 145 koz and 165 koz PGMs and 1.50 Mt to 1.65 Mt of chrome concentrates. | ||

Mortgage Advice Bureau (Holdings) (LON:MAB1) (£333m | SR73) | £1.4m acquisition of a “UK consumer platform attracting millions of web visits annually, providing guidance, tools, and services to homeowners and prospective buyers”. | GREEN = Graham [no section below] A £1.4m acquisition might not move the needle but this does look like a neat little acquisition of a trusted website. The synergies from acquiring an asset like HomeOwners Alliance Ltd (HOA) are pretty clear: MAB will get the opportunity to "engage with customers earlier in their homebuying journey" and "broaden MAB's role across the wider home-moving process". HOA is a trusted source of advice for home buyers and provides quotes for a wide range of related services - mortgages, conveyancing, etc. Recent full-year results from MAB disclosed a very modest net debt position of £3m (relative to adj. PBT of over £36m) so there are no balance sheet reasons for them to refrain from making a small acquisition like this. I retain my positive stance on this quality stock (QualityRank 85). | |

| Porvair (LON:PRV) (£336m | SR75) | AGM Trading Update | PRV has performed in line with expectations in the first four months of the year, delivering constant currency revenue growth of 5%. | |

Ab Dynamics (LON:ABDP) (£262m | SR49) | Revenue -16%, adj. operating profit -16% (£9.1m). “H1 performance reflects previously guided second half bias for FY 2026, with full year adjusted operating profit expected to be in line with current market expectations.” | ||

Petrotal (LON:PTAL) (£252m | SR91) | Group production averaged 14,907 bopd in Q1, down 2% QoQ. Total cash of $128.1 million as of March 31, 2026 ($104.2 million unrestricted). Development program at Bretana: in the final stages of securing a drilling contractor. Drilling activities targeted to resume by October. | ||

Serabi Gold (LON:SRB) (£242m | SR99) | Quarterly gold production of 12,042 ounces, a 20% increase from Q1-2025. Cash of $64.4m. Commenced installation of a 4th ball mill at Palito Complex; will increase annual processing throughput to 330ktpa in 2027. Two underground fatalities in January. Production guidance at 53,000 ounces to 57,000 ounces. | ||

Gulf Marine Services (LON:GMS) (£232m | SR87) | Revenue up 12%, adj net profit up 30% to $41.8m. Net debt down 22% to $157m (1.4x leverage). Events in the Middle East are causing some disruption and management are evaluating the impact on operations and outlook. | AMBER/RED ↓ (Roland) [no section below] Today’s results look fine to me and appear to be largely as expected. Revenue and day rates are up, debt is down and an additional leased vessel is helping to offset lower utilisation rates. However, I see little point in getting too far into last year’s numbers given the impact of the situation in the Middle East. Management says one customer has declared force majeure so far and that previous 2026 EBITDA guidance ($105-115m) is now under review – an update will be provided “when the situation becomes clearer”. While geographic diversification is a priority, I would speculate that it could become more difficult to secure higher day rates against a backdrop of falling fleet utilisation. Similarly, I can’t help feeling that the recent decision to acquire a new vessel may have been poorly timed. While there may still be some value on offer here, I’ve opted to downgrade our view by one notch to reflect the uncertain outlook and falling fleet utilisation – not an attractive combination, in my view. | |

SRT Marine Systems (LON:SRT) (£219m | SR35) | Further to last night’s placing announcement, SRT has raised gross proceeds of c.£16m, placing c.19.5m shares at 82p. Proceeds will be used to strengthen balance sheet, accelerate product development and support contract delivery. | ||

Mkango Resources (LON:MKA) (£146m | SR9) | Companies are included in a consortium to deliver “a full circular UK supply chain for rare earth neodymium-iron-boron ("NdFeB") magnets used in the automotive sector.”. | ||

Amcomri (LON:AMCO) (£115m | SR69) | 2025 revenue up 22%, pre-tax profit up 145% to £4.1m. Continued growth in both divisions “despite some weaknesses in certain end markets”. Outlook: 2026 has started well and is in line with expectations. | ||

Orosur Mining (LON:OMI) (£78m | SR12) | Drilling 100m west of Pepas intersects “significant gold mineralisation”, including 26.4m at 2.85g/t AU and 14.45m at 8.27g/t Au. | ||

Agronomics (LON:ANIC) (£70m | SR53) | Received approval in Japan and Brazil to import and sell the world’s first non-browning banana variety. | ||

DP Poland (LON:DPP) (£66m | SR18) | Total system sales +18.2% in Poland and +28.8% in Croatia. Six new stores added; 141 stores at quarter end, plus 71 Pizzeria 105 locations. | ||

Hemogenyx Pharmaceuticals (LON:HEMO) (£63m | SR9) | Submitted Annual report to FDA under IND application for HG-CT-1. Includes details of ongoing Phase 1 study, stability information and updated trial plans. | ||

Zenith Energy (LON:ZEN) (£52m | SR37) | Tunisia has now recognised that the Robbana and El Bibane production concessions are held by Zenith’s fully-owned subsidiary, EPT. The authorities have also confirmed that c.3,987 barrels of oil produced from the concessions since 2022 and held unsold are owned by EPT. A further 8,000 barrels remain in storage at Robbana, where facilities have suffered “extensive vandalism and theft” and will be non-operational for at least a year. | ||

hVIVO (LON:HVO) (£51m | SR51) | Signed Clinical Trial Agreement to conduct a trial to test Traws’ tivoxavir marboxil ("TXM"), using the hVIVO Influenza Human Challenge Study Model. Majority of revenue to be recognised in 2026. | ||

Cobra Resources (LON:COBR) (£46m | SR13) | Reports results from 12 reverse circulation drillholes from the Blue Rose copper-gold-molybdenum discovery. Considers the “grade, width and depth profile of results to date to be highly encouraging”. | ||

Enwell Energy (LON:ENW) (£45m | SR85) | Production licences remain suspended. SC exploration planning continues. “The operating environment in Ukraine remains very challenging”. Cash of $93.3m, majority in Ukrainian Hryvnia. | ||

PROCOOK (LON:PROC) (£41m | SR79) | Full-year revenue up 23% to £85.5m, ahead of expectations. Outperformed wider UK kitchenware market by 20% across full year. Operating profit & PBT expected to be in line with expectations. | ||

PCI- PAL (LON:PCIP) (£36m | SR55) | Achieved various new compliance standards, enhancing its ability to support enterprise customers operating in highly regulated environments, particularly in the United States and the healthcare sector. | ||

James Cropper (LON:CRPR) (£27m | SR90) | Expects FY26 revenue up 4%, with adj EBITDA of £8.8m, approx 10% ahead of expectations and +30% versus last year. Net debt to EBITDA now <1x. Outlook: “confident in the medium-term prospects of both divisions”. | AMBER/GREEN ↑ (Roland) I’m upgrading our view today to reflect Cropper’s improved balance sheet and earlier-than-expected recovery in profitability. The main risk here seems to be a lack of visibility on FY27 – forecasts are unchanged today, but the company warns that the outturn for the Advanced Materials division (the group’s main profit engine) will be dependent on “customer demand patterns and broader market conditions”. | |

First Property (LON:FPO) (£20m | SR80) | FY26 pre-tax profit (y/e 31 March) is expected to exceed current market expectations. Group has benefited from one-off profits on the disposal of two properties. | ||

Cirata (LON:CRTA) (£19m | SR2) | Q1 2026 was cash flow positive, for the first time in the company’s history. Good momentum with Q1 FY26 closing annualised contract value of $4.9m. Outlook reaffirmed: targeting cash flow breakeven in FY26. | ||

Sosandar (LON:SOS) (£15m | SR68) | Revenue up 14% to £42m, pre-tax profit expected to be £0.4m, in line with expectations. Net cash of £8.4m. | ||

Block Energy (LON:BLOE) (£14m | SR33) | Executed agreement with Zhijiang Sanning Energy Co Ltd for the farmout of Project III. Will include up to $75m carry comprising appraisal drilling and early facilities construction. Sanning to acquire 51% of Project III, with Block owning 49% and retaining operatorship throughout appraisal. |

Graham's Section

Imperial Brands (LON:IMB)

Down 7% to £28.77 (£22.5bn) - Trading Update - Graham - AMBER/GREEN =

As a BATS shareholder, I note that BATS is also down today - by about 4%.

At first glance, I thought that this IMB update was fine, but the market was evidently hoping for more.

Headline:

Trading update: reiterating full-year guidance; positive start to 2030 transformation.

First half highlights:

H1 net revenue: low single digit growth in tobacco and next-gen products.

H1 adjusted operating profit: slightly higher compared to H1 2025. Growth to accelerate in H2, in line with previous guidance for an H2 weighting.

For the full year:

We reiterate our full-year guidance for FY26 of low-single-digit tobacco and double-digit NGP net revenue growth, three to five per cent Group adjusted operating profit growth and at least high-single-digit earnings per share growth, all at constant currency,

Free cash flow is to be “at least £2.2bn”.

Tobacco will have small net revenue growth even as volumes decline.

Next-gen products will see market share growth and “mid to high single digit” net revenue growth.

The next-gen category includes tobacco heated products, vape and “modern oral” (nicotine pouches).

So what’s the catch? Here’s one: the company is planning to give up some market share:

While market share remains important, we continue to balance share and value. Having successfully stabilised our aggregate share across our top five markets, we continue to evolve our approach to reflect changing market dynamics and our focus on more profitable segments, to deliver long-term, sustainable value creation. As such, we anticipate some overall modest aggregate share reduction across the top five markets in H1, alongside growth in tobacco adjusted operating profit.

There’s nothing inherently wrong with prioritising profitability over market share, but what’s the endgame here? IMB’s big strategic wins have been in the budget categories left behind by the other majors - the fast-growing budget cigarette brand Paramount already has 5% market share in the UK, for example.

A strategic shift towards profitability, at the expense of market share, will see IMB competing head-on with BATS and Philip Morris.

Again - there’s nothing inherently wrong with that choice. But as a potentially risky strategic direction, I can see why it might cause some IMB shareholders to bank their profits.

5-year chart:

Leverage: “to remain at the lower end of our 2.0-2.5 range for net debt to EBITDA”.

Graham’s view

There’s no hidden profit warning contained in this update. What we do have are the following amber flags:

An H2 weighting needed to hit forecasts (although this is not news).

A shift in strategy away from what has strategically worked, towards more direct competition with its peers.

Next-gen products, which are the only possible engine of volume growth, potentially only seeing mid single digit revenue growth, if they come in at the low end of the range.

On the bright side, it’s still not exactly expensive. The P/E multiple is about 8x, based on current-year earnings (FY September 2026).

And with buybacks, the share count is on the decline, gradually making dividends more affordable:

I’m a little biased when it comes to this sector. I’ve always thought, despite the ethical problems with it, that it was objectively-speaking a source of good investment ideas.

Therefore, despite the market’s dissatisfaction with today's update, I’m inclined to leave our existing AMBER/GREEN stance unchanged. The shares have had a great run, and it makes sense that there’d be profit-taking on a lukewarm update. But in reality, I think that little has changed here.

Indeed, I’d argue there’s more value on offer now than there was in November, when Roland covered it at a £25bn market cap. The market cap is only £22.5bn today - about ten times forecast free cash flow for this year

Roland's Section

Atalaya Mining Copper SA (LON:ATYM)

Down 1% at 796p (£1.2bn) - Q1 2026 Operations Update - Roland - AMBER ↓

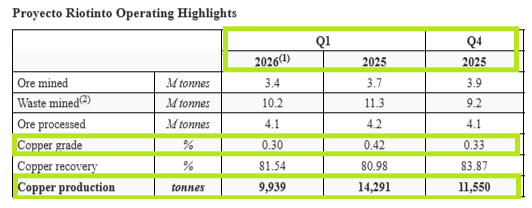

This Spanish copper miner has delivered a decidedly mixed update today. Copper production fell sharply during the first quarter and the company is reviewing its full-year guidance with a view to restating it with Atalaya’s Q1 financial results in May.

My reading of this RNS is that it’s quite negative, but I can also see some positives that I will try and highlight. It’s worth remembering we’re in a strong bull market for copper at the moment – so even a weaker-than-expected production result could still support rising profits.

Here are the main points from today’s quarterly update, as I see them:

Q1 production affected by “unusually heavy rains”, also affected peers in the region;

Expect to recover “a portion of the production shortfall”;

Q1 copper production of 9,939t (-30% vs Q1 25 and -14% vs Q4 25);

Average realised copper price in Q1 of $5.87/lb (Q4 25: $5.10/lb, Q1 25: $4.26/lb);

No impact yet from events in the Middle East, but unit prices for key consumables such as explosives and diesel could be affected in the coming months. Some hedging is already in place.

Outlook

In my view, the highlights table at the top of today’s RNS is potentially misleading, as it includes details of Atalaya’s previous 2026 guidance for full-year copper production of 50,000 to 54,000 tonnes.

Only by reading further down do we discover that this guidance is now under review:

Following the impact of rainfall during the Period, the Company plans to review its copper production guidance for FY2026 on an ongoing basis and will provide further updates when the Company reports its Q1 2026 Financial Results in May 2026.

Doing the maths suggests that Atalaya would need to produce at least 13.3kt of copper quarterly for the remainder of the year to stay within the previous guidance range.

This appears to be theoretically possible, but I would argue that it’s highly dependent on a recovery in the copper grade of the ore being processed. Lower grades were a big factor in the fall in Q1 production:

The company says that lower grades in Q1 were exacerbated by the use of low-grade stockpiled ore due to mine access problems in heavy rainfall. However, I’d note that ore grades were already much lower in Q4 last year.

I don’t know enough about the company’s assets to understand whether a recovery in grades is likely.

Updated estimates: with thanks to broker Canaccord Genuity for publishing on Research Tree today, we can see that earnings estimates for FY26 and FY27 have been left unchanged.

FY26E adj EPS: €0.99

FY27E adj EPS: €1.31

I would guess these estimates will be revisited in May when the company provides updated guidance and information on Q2 trading.

Roland’s view

My interpretation of this update is that a cut to production guidance and earnings forecasts is relatively likely, unless rising copper prices save the day.

This may well happen – the red metal is currently trading at near-record highs after a multi-year bull run:

Another potential positive is that inventories of copper concentrate rose by 20% to 5,083 tonnes during the quarter. I’m not sure why sales were held back or slowed, but strong copper prices may give Atalaya the opportunity to sell down inventories at higher copper prices later in the year, supporting earnings.

Of course, I’ve no idea if or how the current geopolitical situation may impact copper demand and pricing as the year unfolds.

What I do know is that consensus estimates for Atalaya have already started to slip this year:

While the shares are looking cheaper than when I last reviewed this stock, I think the company’s High Flyer styling could come under pressure unless the price of copper continues to rise.

As I commented in January, I think Atalaya’s valuation is more directly linked to the price of copper than it was 12 months ago, when the shares were trading in line with book value (versus 2.4x today).

In my view, this has become a more speculative situation than it was in the past. When combined with today’s weak Q1 update, I think it’s appropriate for me to move our view to neutral. AMBER

James Cropper (LON:CRPR)

Up 25% at 350p (£33m) - Full Year Trading Update - Roland - AMBER/GREEN ↑

James Cropper plc (AIM: CRPR), the Advanced Materials and Paper & Packaging group, is pleased to announce a trading update for the financial year ended 28 March 2026 ("FY26").

Today’s full-year update includes details of improved trading and an upgrade to FY26 guidance.

The details are fleshed out in a broker update from Shore Capital that’s available on Research Tree. This explains why Shore’s analysts have translated today’s 10% upgrade to EBITDA into a 33% increase in FY26 EPS forecasts.

FY26 trading update

Revenue appears to have been stronger than expected during the second half of the year. The resulting operational gearing has resulted in a much-improved profit performance.

FY26 revenue up 4% to £103m (+6% versus previous forecast of £96.8m);

FY26 adj EBITDA up 30% to £8.8m (+10% versus previous forecast of £8m);

FY26 net debt of £8.3m (FY25: £12.9m), giving a net debt/EBITDA ratio of <1x.

Both the company’s operating divisions appear to have performed slightly better than expected in terms of revenue, with Advanced Materials up by a “low double-digit percentage” and Paper & Packaging “broadly in line with FY25” despite the previously-reported loss of a major customer.

Overall group profitability improved thanks to these higher revenues. But I think there are some nuances worth noting relating to the profitability of each division.

Advanced Materials: “increased investment in operating costs to support medium-term growth” meant that adjusted EBITDA only rose by a “high single-digit” percentage, lagging revenue growth. While investment to support longer-term growth is important, in my view it’s crucial that this is done with clear line-of-sight to commercial opportunities. I think the trend here could be worth watching.

Paper & Packaging: this legacy business generated a reduced EBITDA loss for the full year, but returned to EBITDA profitability in H2.

Current trading & FY27 outlook

Trading momentum into the new financial year has been positive, with the Group's strategy and operational improvement programme continuing to track in line with the Board's strategic plan.

Management caution that the “ultimate impact on markets and input costs” of events in the Middle East remains uncertain. However, Cropper “is actively managing its position through hedging, pricing actions and procurement discipline”.

Cropper CEO David Stirling has stopped short of providing FY27 guidance today and has instead emphasised his confidence in “the medium-term outlook”.

Today’s commentary suggests to me that while performance in Paper & Packaging is expected to improve further, there’s some uncertainty about the outlook for Advanced Materials:

Advanced Materials: “... the Group expects growth in the current year to be linked to customer demand patterns and broader market conditions.”

Paper & Packaging: confident in delivering further improvements to performance, expect to achieve full-year positive adjusted EBITDA.

Updated broker forecasts

EBITDA is a useful metric for lenders. But as we often comment, the number of costs excluded from this figure mean it’s less useful for equity investors (who can only benefit from bottom line earnings).

For these reasons, we often see EBITDA growth translate into a smaller increase in EPS.

However, today we have an interesting and rare reversal of this pattern – the increase in Cropper’s FY26 adjusted EPS forecasts is three times larger than the rise in EBITDA forecasts (estimates from Shore Capital):

FY26E adj EBITDA +10% to £8.8m

FY26E adj EPS +33% to 45.4p

There are two reasons for the much larger EPS upgrade:

Cropper booked a £4.4m impairment charge against P&P assets last year (and a £7.2m charge in FY24). This means that depreciation charges are lower than in the past – the assets have already been written down. This is likely a one-off gain, unless further impairments follow.

The second reason is more positive – lower interest costs due to the reduction in net debt.

What about FY27?

Shore Capital has left FY27 forecasts unchanged today. The broker says that this is “erring on the side of caution” but acknowledges the obvious macro risks.

This introduces the risk that Cropper’s earnings growth could pause this year – current FY27 adj EPS forecasts stand at 44.1p, marginally below the revised FY26 estimate.

Roland’s view

James Cropper is an illiquid small cap stock with a large spread. With shares like this, upgrades (or downgrades) can result in disproportionate share price moves.

I would argue we’ve seen that this morning – early gains of over 30% have now pared back to c.25%, at the time of writing.

While this increase is below today’s upgrade to FY26 estimates, these are for last year’s earnings. The market looks forward and there’s no change to forward earnings estimates today.

I took a broader look at this business in a Stock Pitch at Christmas and my view of the opportunities and risks is largely unchanged following today’s update.

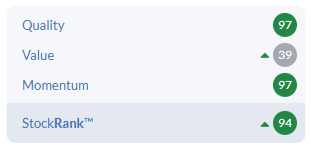

The StockRanks also remain fairly positive:

Despite some uncertainty around FY27, I am encouraged by the recovery in profitability suggested by today’s update – today’s adjusted figures suggest a FY26 return on equity of c.12% (although I would also like to see the unadjusted figures!).

The valuation also remains quite reasonable, in my view, on a forward P/E of around 8.

We’ve been neutral on this stock in previous coverage, but I think it’s fair to move up one notch today in reflection of the company’s improved balance sheet and profitability. AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.