Good morning! I hope you had a relaxing weekend.

There are no big overnight moves to report. But there is reportedly a plan to reopen the Strait of Hormuz and end the war, that has been written up by Iranian negotiators. So perhaps this week will be a good one for macro news.

This is also a big week for interest rates: no rate changes are expected, but there will be decisions from the BoJ, Fed, ECB and BoE! So we should get some interesting commentary to go with those decisions.

The FTSE is set to open just below 10,400.

All done for today, thank you. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£216bn | SR73) | Saphnelo approved in the US for subcutaneous self-administration as a new autoinjector for the treatment of systemic lupus erythematosus. | ||

GSK (LON:GSK) (£82m | SR95) | The Delaware Chancery Court has granted the motion to dismiss filed by AnaptysBio, Inc. against TESARO's claim for anticipatory breach. The court’s ruling does not address the merits of the dispute between the parties; GSK and TESARO remain focused on pursuing the claim at trial. | ||

Yellow Cake (LON:YCA) (£1.52bn | SR58) | NAV per share rose by 5% to 634p on 31 March 2026. Holdings of U3O8 increased by 1.4m lb to 23,114,230 lb during the quarter, held in storage in Canada and France. Notes price volatility between mid-$80s/lb and >$100/lb during the period. Completed a $110m placing, proceeds will be used to fund a further 1.2m lb purchase at $86.15/lb from Kaztomprom. | ||

Molten Ventures (LON:GROW) (£924m | SR86) | NAV per share up 13% to 760p, driven by strong performance and funding rounds in the Core Portfolio, including Revolut. Share buybacks added 21p/share to the uplift. Gross portfolio value (GPV) to be c.11% higher at £1,520m. Realisations of £120m delivered at an average multiple of 3x invested capital. | ||

Harworth (LON:HWG) (£443m | SR13) | Leeds local planning committee has approved the Microsoft MCIO data centre planning application at Skelton Grange. Haworth is completing enabling works for Plot 2 and will receive £53.2m on completion of sale to Microsoft. | ||

Pensionbee (LON:PBEE) (£345m | SR32) | AuA has risen to approximately £8bn in April 2026 (31 Mar 26: £7.5bn), on behalf of more than 315,000 invested customers. | AMBER = (Graham) [no section below] We turned neutral on this last summer as it was well-funded after a £20m equity raise and was growing rapidly. Today's update is just a milestone announcement, with the company reaching £8bn of assets under administration (AUA). The recent Q1 announcement for Jan-March showed AUA growing 29% year-on-year to £7.5bn, positive Q1 adjusted EBITDA in the UK, and positive Group adjusted EBITDA for the trailing 12-month period. Expansion in the US will not be easy but perhaps the company might soon have some real UK profits to help fund the effort? They also have a strategic partner in State Street who "substantially funded" the US marketing expenditure in Q1. With the growth rates being achieved (38% revenue growth year-on-year) I can't possibly be negative on this, and I may ned to turn positive before too long. | |

Frp Advisory (LON:FRP) (£308m | SR63) | CEO and COO Geoff Rowley and Jeremy French, together with other existing and former Partners, have agreed not to sell shares until 1 September 2031, except through orderly sell-downs for former partners. This replaces the previous lock-in agreement from 2024 and covers 18.2% of FRP’s share capital. | ||

Vanquis Banking (LON:VANQ) (£286m | SR73) | Vanquis will not challenge the FCA’s redress scheme and is focused on implementation. Its previous £3m provision for this matter remains unchanged. Vanquis reiterates that it did not participate in discretionary commission arrangements or operate tied selling arrangements. | GREEN ↑ (Graham) [no section below] I studied the full-year results from Vanquis here and decided to stay moderately positive on the company then. Today’s news is just a footnote to the FCA’s financial redress scheme: the tiny provision Vanquis made is still thought to be significant. With VANQ shares currently trading c. 10% cheaper than they were in February, implying an even greater discount to TNAV (£358m), I’m happy to stick my neck out and rate this GREEN for value. The shares are trading at just over 6x forecast earnings, and are expected to rejoin the dividend list next year. | |

CLS Holdings (LON:CLI) (£189m | SR26) | Sold The Brix for €60m, in line with 31 Dec 25 valuation. Completion expected in Q2. Proceeds will be used to pay down debt.v | ||

EKF Diagnostics Holdings (LON:EKF) (£106m | SR65) | Helen Jones FCA appointed as CFO with immediate effect. She has 20 years’ experience and joins from Surgical Science. | ||

Shield Therapeutics (LON:STX) (£95m | SR33) | Shield’s partner MEDLEAP Pharma has confirmed its first patient enrollment for the Phase II clinical trial for ACCRUFeR. | ||

Bango (LON:BGO) (£60m | SR17) | Revenue -2% to $52.2m, ARR +30% to $18.2m. Adj EBITDA +7% to $16.4m, “cash EBITDA” of $2.3m. Outlook: expects to see further improvements in profitability and cash flow. | AMBER/RED = (Roland) [no section below] | |

Power Probe (LON:PWR) (£55m | SR39) | Revenue +25.7% to $39.4m, adj EBITDA +6.7% to $9m, cash of $15.3m. Outlook: Q1 trading “encouraging” and in line with management expectations. | AMBER = (Roland) [no section below] This automotive diagnostic instrumentation specialist only floated on the London market in 2025. We are always cautious about recent IPOs as they often disappoint. One question I might want to ask management here is why the company opted for a UK (AIM) listing when it generates 95% of revenue in the US and reports in USD. Despite my caution, today’s results do show attractive profitability (12% operating margin) and positive cash generation, with free cash flow of $4.3m from $39.4m of revenue – a 10% free cash flow margin. The current valuation implies an adjusted forward P/E of 10.5x according to today’s note from Shore Capital. Based on this very quick initial review, I think it’s fair to take a neutral view here and monitor further progress. | |

Clean Power Hydrogen (LON:CPH2) (£50m | SR18) | Memorandum of Understanding with BKW Infra Services Europa SE subsidiary ABE GRUPPE GmbH for partnership exploring sale of 175MW of electrolyser capacity. | ||

Aoti (LON:AOTI) (£45m | SR38) | “The study demonstrated a high rate of complete durable healing utilising AOTI's intermittent TWO2® therapy as an adjunct to standard of care in hard-to-heal wounds that had failed to heal with other advanced wound care for an average of 7 months.” | ||

One Health (LON:OHGR) (£33m | SR67) | Continued growth, ahead of market expectations: FY March 2026 revenue +13% (£32m). The Company is expected to deliver growth at the revenue and underlying EBITDA levels for FY 26, ahead of market expectations. | AMBER = (Graham) | |

Zinnwald Lithium (LON:ZNWD) (£32m | SR30) | Subsidiary Zinnwald Lithium GmbH has been granted a permit to construct an exploration tunnel to access the Zinnwald ore body that underpins the Zinnwald Lithium Project. | ||

Christie (LON:CTG) (£31m | SR88) | 19.2% revenue growth from continuing operations, ahead of Board expectations. Op profit from continuing operations £6.9m (2024: £3.5m). “Absent of any major market disruption and assuming more normalised level of invoicing, we are confident of our ability to achieve similar business sales volumes in FY26 and believe we are well positioned to deliver another positive year.” Working towards a buyout of its pension schemes. | GREEN = (Roland) 2025 results from this professional services group were ahead of expectations, while broker forecasts for 2026 and 2027 have now been upgraded significantly from December’s pre-disposal levels. Christie’s decision to focus on its core and most profitable operations seems logical to me and is expected to drive medium-term growth. Although there’s no certainty the company will succeed, the valuation remains reasonable and the business is underpinned by a strong balance sheet. I think it’s fair to remain positive. | |

Headlam (LON:HEAD) (£23m | SR26) | Has received a notice “purporting to be a requisition notice” from First Seagull (FS). FS wants to remove the chair and two NEDs. | RED = (Roland) Norwegian hedge fund First Seagull controls 10% of Headlam stock and appears to want a change in boardroom leadership and perhaps strategy. I’m unsure about the recovery prospects here. Without further research, I don’t know enough to gauge whether Headlam’s plan to become smaller and more profitable is realistic, or simply a prelude to eventual failure. If the business is in terminal decline then a managed liquidation might secure more value for shareholders given the estimated remaining value in the group’s freehold property estate. While I can see this might be an interesting special situation, Headlam’s loss-making operations and weak balance sheet mean that I’m leaving our negative view unchanged today. | |

Braime (LON:BMTO) (£22m | SR58) | Revenue £50.9m (2024: £48.9m). PBT £4.1m (2024: £3.2m). Global economic background is significantly worse than 12 months ago, but the company has gained new customers:“Given the planned release of further new products for sale to similar end users, we remain confident that sales to these customers will continue. In 2025”. | ||

Europa Oil & Gas (Holdings) (LON:EOG) (£22m | SR21) | North Yorkshire Council planning committee decided not to approve EOG’s plan for a well on its Cloughton prospect. EOG disappointed; confident that on appeal the planning permission will be approved. | BLACK (but no impact on share price) | |

Ingenta (LON:ING) (£16m | SR99) | Revenue £10.3m. Adj. EBITDA £1.6m (last year: £1.8m), reflecting higher sales and marketing spending. Net profit £1.7m (2024: £1.3m). Outlook: The Board expects revenue in 2026 to be at least broadly in line with the prior year. Continued investment in sales and marketing. | AMBER/GREEN = (Graham) This is a microcap so it would be unreasonable to hold it to the standards of a larger company when it comes to broker estimates. I do still find it strange that there are no FY26 forecasts from the company’s broker. This says to me that visibility must be pretty poor for the current year. If it wasn’t for the strong cash balance and low market cap, I’d be inclined to take us back to a neutral stance on this stock today. The outlook - or lack thereof - makes me nervous, but the stock is cheap enough. | |

Kelso group (LON:KLSO) (£14m | SR37) | Bought 500,000 shares in Filtronic at 185p. The share price has appreciated (gain ~60%) and the holding now represents c. 10% of Kelso’s gross investments. | ||

88 Energy (LON:88E) (£14m | SR14) | V partner Burgundy Xploration at Project Phoenix in Alaska: 88 Energy has agreed to an extension of the funding milestone date, aligning the timeline to Burgundy's planned US IPO. |

Graham's Section

Ingenta (LON:ING)

Down 7% at 99.75p (£15m) - Final Results - Graham - AMBER/GREEN =

Ingenta plc (AIM: ING) a leading software and services provider to the publishing and media industries, announces its final audited results for the year ended 31 December 2025.

It’s a bit late to announce results for December 2025, no?

Let’s check them out anyway:

Revenue £10.3m (2024: £10.2m)

ARR slightly improves to 89% of total revenue (2024: 87%)

Adj. EBITDA £1.6m (2024: £1.8m). Higher spending on sales and marketing.

Net profit £1.7m (2024: £1.3m).

It’s noteworthy that net profit, without any adjustments, is higher than adjusted EBITDA. It’s usually the other way around. We’ll investigate that shortly.

Cash of £4.7m covers a chunk of the £15m market cap.

Full-year dividend is 4.5p (2024: 4.1p).

Current trading and outlook: let’s put this forward-looking section here in full, as these 2025 results are very backward-looking.

With emphasis added:

New sales and expansions of existing customer relationships in both Content and Commercial divisions expected to deliver significant additional revenue opportunities over the next 3 years.

Growing sales pipeline for all Ingenta products with deals expected to be awarded in early 2026.

Sales recruitment ongoing to further support revenue growth targets.

FY26 revenue expected to be at least broadly in line with FY25, as revenue from new customer wins offsets anticipated attrition in legacy platform revenues with further guidance expected after the AGM.

“At least broadly in line” is unusual phraseology. It says to me that 2026 revenues might be slightly below 2025, although the company is hoping for better than that.

And it’s a little incongruent with the result of the outlook section, which is suggestive of impressive growth on the way.

CEO comment:

"The results posted here are an encouraging sign of the operational efficiency of the business and why the investment in sales should help accelerate growth and profitability in future years. Revenue growth in the year has been achieved mainly from the existing customer base, in many cases representing new contracts entered into with new divisions or geographical units of large international publishers.

New revenues have offset “the loss of legacy platform income at a higher rate than expected”.

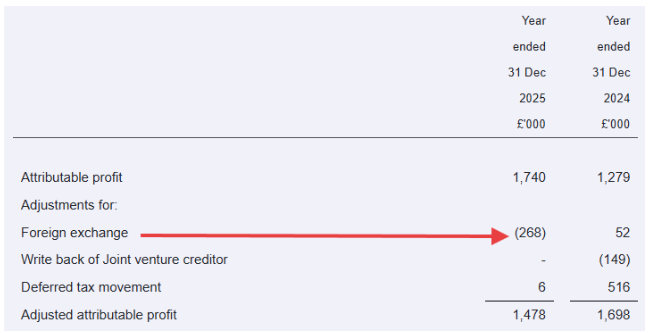

Adjusted earnings lower than reported earnings?

Dave in the comments has asked why adjusted EPS is only 10.2p, while reported EPS was 12p.

There is actually just one significant adjustment to profits, causing adjusted profits to be lower than actual profits:

The CFO describes this as “unrealised foreign exchange on intercompany balances”. And it’s actually a very reasonable adjustment, at least in my book.

Intercompany balances means some sort of liability between a subsidiary and a parent company. If that’s denominated in dollars or euros, for example, then changing currency rates can change the value of that liability. I have no objection to this being adjusted out of the earnings result.

It is worth noting that the effect of this item has a large impact on the overall result, suggesting that the intercompany balance could be pretty large. It’s the type of thing that would be worth asking a question to management about at an AGM. But for me it’s not really a red flag or something that would prevent me from investing here.

Estimates: Cavendish didn’t have FY26 estimates at the time of the January trading update, and they still don’t have FY26 estimates today.

Indeed, they used to have a BUY rating on the stock, with a price target of 260p. They have now removed both the rating and the price target, saying:

Given the moving parts around the size and timings of legacy revenues and pipeline conversion, we will await the further guidance post‑AGM before releasing forecasts for FY26E and put our price target and rating under review.

Graham’s view

This is a microcap so it would be unreasonable to hold it to the standards of a larger company when it comes to broker estimates. I do still find it strange that there are no FY26 forecasts from the company’s broker.

This says to me that visibility must be pretty poor for the current year, and that there are likely to be some pretty significant risks to the downside.

The company is evolving from legacy products over to new products, and beefing up sales and marketing efforts in order to carry out this evolution. That process is always risky in the short-term, and it sounds like sales and marketing spending could be a pretty big headwind to profit this year (S&M spending was £1.2m in 2025, vs. £0.8m in 2024).

Therefore, if it wasn’t for the strong cash balance and low market cap, I’d be inclined to take us back to a neutral stance on this stock today.

But I acknowledge the cheapness: the enterprise value is only ~£10m, so a cash-adjusted trailing earnings multiple is going to be pretty cheap (2025 PBT was £1.7m).

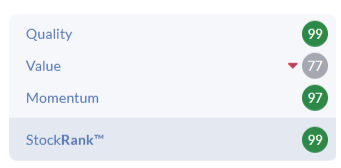

The StockRanks love it, too:

Mark (holding the stock) was AMBER/GREEN on it in January and I’m happy to leave that unchanged today. The outlook - or lack thereof - makes me nervous, but the stock is cheap enough.

One Health (LON:OHGR)

Up 6% to 254p (£35m) - Full Year Trading Update - Graham - AMBER =

This is “the independent provider of NHS-funded surgical procedures for patients referred from the NHS through 'Patient Choice”.

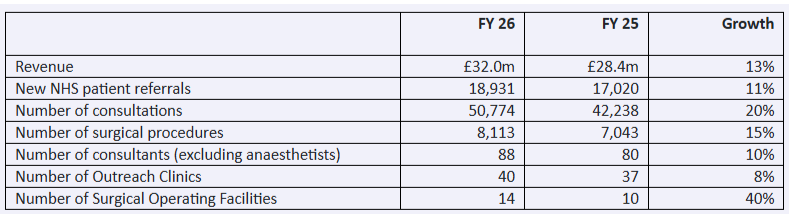

Today’s update for FY March 2026 is ahead of expectations.

Here are all the year’s highlights, as presented by the company.

The company is building an £8-9m Surgical Hub in Scunthorpe, Lincolnshire, which is “on track to be delivered within the one-year construction period”.

Additionally, “further locations in underserved areas with high NHS demand continue to be explored for preliminary assessment of suitability for future surgical hubs”.

Outlook:

The Company is expected to deliver growth at the revenue and underlying EBITDA levels for FY 26, ahead of market expectations. Cash at 31 March 2026 was £11.1m (FY 25: £11.4m) with the Company remaining well-funded to deliver further organic growth and execute the carefully planned delivery of the Group's first surgical hub to accelerate growth and improve profitability.

Existing market expectations: revenue £29.4m, underlying EBITDA £2.3m.

CEO comment:

…NHS national waiting lists remain very high, despite continued NHS efforts and recent modest reductions, and we are proud that One Health remains well-positioned to continue to reduce pressure on the NHS by providing free high-quality care across underserved areas."

Estimates

Thanks to Panmure Liberum for publishing on this today.

FY27 revenue forecast raised 8% to £33.9m (their FY26 forecast was beaten by 8%).

FY27 underlying EBITDA forecast raised by 4% to £2.6m (they estimate their FY26 EBITDA forecast was beaten by 9%).

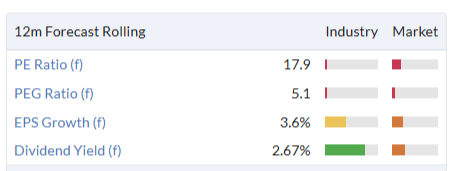

The new EPS forecasts are 13.6p (FY26) and 14.2p (FY27), putting the shares on a forward multiple of 18x.

Graham’s view

At first glance this is not standing out to me as a bargain. The StockReport feels the same way:

I note that this IPO’d last year at 180p. Market have been strong but it’s still a good achievement to trade above its IPO price:

Roland has been AMBER on this one and my instincts strongly point towards keeping that stance unchanged today.

It’s not even that I have any specific objection to the company’s performance. I’d even argue that OHGR is well-positioned, under the current government, to benefit from the priorisation of healthcare spending.

But I have an IPO rule which says that it’s important to be sceptical of freshly-listed companies until at least two years have passed, or the share price has declined by at least 50% (I’m assuming that IPOs are priced at double fair value).

There are always exceptions to rules, but with a ValueRank of 32, OHGR does not look like an instance where I should be making an exception.

Roland's Section

Christie (LON:CTG)

Up 29% at 155p (£41m) - Preliminary Results - Roland - GREEN

This family-owned professional services business has reported strong 2025 full-year results today, significantly ahead of recently-upgraded forecasts:

It seems that the company’s 2025 results were given a further boost by the completion of “several deals” in late 2025 that were originally expected to complete in Q1 2026.

This raises an obvious question – will there be a shortfall in 2026 as a result? The answer seems to be probably not – I’ll return to the outlook shortly.

Improved focus: as we’ve discussed previously, Christie has been slimming down its operations to focus on its core and most profitable businesses. Two disposals have now been completed:

As part of the Group's ongoing strategy to enhance quality of earnings we were pleased to announce the divestment of Vennersys on 22 December 2025, following the sale of Orridge in 2024, the second of the Group's historically persistent loss-making businesses.

The sale of Vennersys appears to have eliminated a £1.5m operating loss last year. Today’s financial figures for Christie’s continuing operations show a significant improvement in profitability:

Revenue up 19.2% to £70.6m

Operating profit up 95% to £6.9m

Operating margin: 10.0% (2024: 6.0%)

Net profit up 86% to £5.0m

Adjusted earnings per share up by 88% to 19.4p

Full-year dividend up 56% to 3.5p per share

Professional & Financial Services (PFS): the improved result was driven by Christie’s largest division, PFS. This is a consulting and advisory business that acts as a broker for the sale and purchase of businesses and arranges other related services, such as financing and insurance.

Christie’s management reports a “strong recovery in transactional brokerage activity in the UK”, highlighting some impressive figures:

PFS revenue up 22.1% to £59.6m

PFS operating profit up 121% to £6.1m

1,164 businesses sold in 2025, totalling nearly £2.0bn in value

26% increase in average brokerage fee

Ancillary and non-UK revenue also improved:

37% growth in fee income from European offices

Finance brokerage revenues up 15% year-on-year

23% growth in the value of insurance brokerage renewals book and improved retention rate

Stock & Inventory Systems & Services (SISS): this smaller unit is built around Venners, “our market leading stock audit and consultancy business”. Its main focus is the hospitality sector, which has faced significant cost pressures over the last year.

The company says “new business growth was more challenging to achieve than in recent years”, with clients also “extending stocktaking cycles”.

Despite this, the division’s performance metrics did show some progress over the year:

SISS revenue up 5.4% to £11.0m

SISS operating profit up “marginally” from £748k to £753k

Total stocktakes and audits (jobs) carried out up 6% to 35,024

Average income per job down 1.6% (2024: +3.1%)

Average income per man day up 2.7% (2024: +6.3%)

Balance sheet: Christie has a conservative balance sheet, as I’d expect from a family-owned company with a long heritage (it’s been listed since 1988 and the Venners business was founded in 1896).

Today’s results show net cash of £9.4m, with no debt except some lease liabilities.

The group also reports that it has closed both its finail salary pension schemes to further accrual and is now seeking a full buy-out to further strengthen the balance sheet. Both schemes are said to have “healthy surplus” positions and to be “almost entirely” hedged.

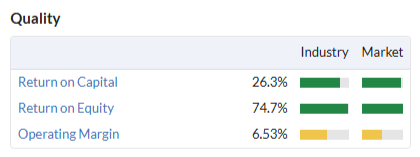

Profitability: last year’s interim results already hinted at a useful recovery in profitability for this business, with highly attractive ROCE and return on equity figures:

I don’t know exactly how the sale of Vennersys will have altered the balance sheet, but assuming a similar level of capital employed post-sale, I estimate that today’s results imply a return on capital employed of c.40% from continuing operations.

That’s an attractive figure, especially for a debt-free business.

The key question is whether the improved performance last year is expected to continue.

Outlook

Management commentary is initially positive:

2026 has begun encouragingly with good levels of ongoing demand for our services and strong pipelines. The value of our UK transactional pipeline was 9.6% higher on 1st January 2026 than a year earlier. Similarly, we commenced the year with increased pipelines on the prior year in both our international brokerage operations and our finance brokerage business, reflecting ongoing progress towards achieving our growth ambitions in both areas of the business.

However, CEO Dan Prickett admits that 2025 results were boosted by “several deals” originally expected to complete in Q1 2026 but warns that macro conditions could impact trading:

While we continue to see deal times elongate slightly and are mindful of the potential for current geopolitical events to dampen confidence, our activity levels, coupled with seemingly robust investor and lender appetite for our sectors, bodes well for the year ahead.

Absent any market disruption, Christie expects to achieve a similar level of business sales to the previous two years (around 1,150).

However, Prickett’s financial guidance is rather more oblique, at least for anyone who is not very familiar with this business:

As a result, and assuming a more normalised level of invoicing, the Board anticipates another positive year and one which we currently consider ourselves well-positioned to deliver.

Updated estimates: fortunately we have an updated note from house broker Shore Capital this morning to help us translate this commentary – many thanks.

Shore’s analysts have reinstated forecasts for outer years with significant upgrades following the sale of Vennersys. Forecasts have also been introduced for FY28:

2025 actual EPS: 19.4p

2026E adj EPS: 13.6p (previously 8.2p in Dec ‘25)

2027E adj EPS: 16.3p (previously 11.8p in Dec ‘25)

2028E adj EPS: 19.2p

While Shore expects revenue to continue rising by c.£5m per year over the forecast period, profitability is expected to fall sharply in 2026. This reflects the broker’s expectation of “investment in 50/60 new heads” this year to drive medium-term growth in the UK and Europe.

These revised estimates put Christie on a FY26E P/E of 11.4, falling to a P/E of 9.5x for 2027. That doesn’t seem too expensive to me.

Roland’s view

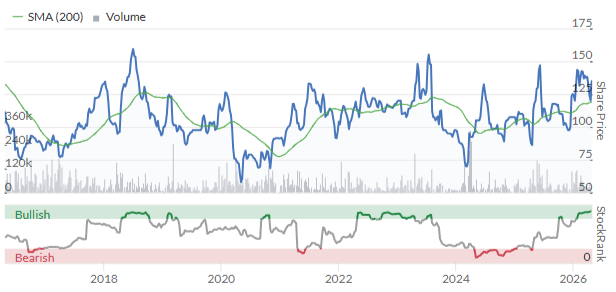

ISA millionaire and well-known private investor Lord Lee is Christie’s second-largest shareholder, controlling a stake of more than 6%. Lee is known for his patient long-term approach and this appears to have been a necessary ingredient here – Christie shares have been rangebound for the last decade:

Today’s newly-introduced forecasts for 2026-2028 suggest Lee’s patience could pay off. If Christie can successfully expand its core business having removed loss-making subsidiaries, it could become a larger and more valuable business than over the last decade.

Graham was GREEN on this business in January. With forecasts upgraded significantly today and a still-reasonable valuation despite today’s 20%+ share price gain, I’m going to leave our positive view unchanged.

Headlam (LON:HEAD)

Up 3.5% at 29p (£24m) - Receipt of notice from shareholder - Roland - RED =

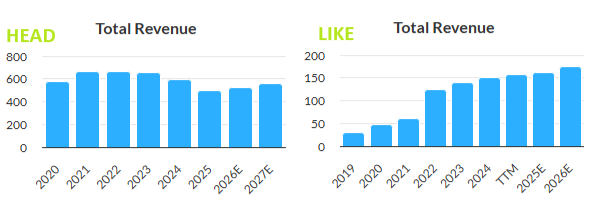

This previously well-regarded flooring distributor has suffered a painful decline, with c.£100m of combined operating losses in 2024 and 2025. Headlam shares have now shed more than 90% of their value in five years.

Boardroom ouster? Today the company confirms that it has received a requisition notice from 10% shareholder First Seagull AS, a Norwegian hedge fund with a focus on special situations. First Seagull has proposed resolutions to remove the chair and two non-execs and appoint FS nominees in their place.

Headlam’s current board naturally disagrees with this suggestion, believing it unnecessary:

The Board is confident that the recently refreshed Board (including a new executive team and two new non-executive directors) has the right experience to implement the Company's strategy and turnaround, and is getting on with doing so at pace.

The two new non-execs (announced on 14 April) do appear to have plenty of relevant experience – they are the former chief executives of Norcros (LON:NXR) (from 2011 to 2023) and Carpetright (from 2014 to 2021).

Headlam’s management is also keen to emphasise that it has been talking to shareholders:

The Board also wishes to highlight the extensive engagement with its shareholders including FS over recent months and intention to maintain that dialogue.

Roland’s view

Commenter Mark has suggested that First Seagull’s ambition may be to secure some value from Headlam’s remaining freehold property, while stemming its operating losses. He points out that recent results from rival Likewise (LON:LIKE) have been much stronger, implying that Headlam’s problems are company specific.

It certainly seems to be that Likewise may have been taking market share from Headlam (Likewise FY25 results are due on 28 April – they could provide useful insight into market conditions):

Poor trading in recent years has seen Headlam’s previously strong balance sheet hollowed out by rising debt and sale-and-leaseback transactions. Cash has been used to support the business. This left the group with a diminished freehold property estate, £31m of net bank debt and c.£65m of lease liabilities at the end of 2025.

Despite this, Headlam’s 2025 results indicated the company still owned freehold and long leasehold property valued at £75m at the end of 2025.

Graham discussed the potential for this to become a deep value play in his review of the annual results in March.

I think it’s worth pointing out most of Headlam’s remaining property estate is now encumbered, following a switch to a secured lending facility last year (my emphasis):

As at 31 December 2025, the Group owned freehold and long leasehold property in the UK valued at c.£75m. Of this, property valued at c.£54m is included in the ABL at an initial 60% loan-to-value, amortising over 15 years.

Of the remaining c.£21m of unencumbered property, most is already under offer:

The remaining properties (valued at c.£21m) are outside the ABL and unencumbered; three of these properties, representing the significant majority of the value, are currently on the market for sale, are under offer, and are expected to complete in the next few months.

The implication seems to be that Headlam will continue to use the proceeds from property sales to prop up its loss-making operating business.

Investors need to decide whether the business can be returned to profitability – or whether it would be more logical to wind down operations and realise as much value as possible from a liquidation.

We don’t know what First Seagull’s proposed strategy might be.

But we do know that Headlam’s current board is proposing a turnaround that will involve a focus on value over volume while continuing the current business model.

Some of the measures being proposed by the company are:

Reducing low-margin revenue.

Focusing on the more profitable categories and actively deprioritising low gross margin categories.

Reducing our trade counter network whilst migrating some profitable category sales to adjacent trade counters or switching this revenue from "collection sales" to "delivered sales".

The combination of the above enables us to reduce our fixed costs and infrastructure requirements, such as distribution centres and vehicles.

Management guidance indicates a “material planned reduction in revenue over 2026 and 2027”.

Focusing on profitability seems sensible enough, but without further research, it’s not clear to me if Headlam can realistically achieve improved profitability at a smaller scale than in the past.

If I was a shareholder, I would be a little nervous about this. Making more money from fewer sales is sometimes possible, but it’s not easy and could be a prelude to the eventual failure of the business.

New CEO/CFO: Headlam’s new chief executive Rob Barclay joined the Board in March and will take over the role of CEO on 27 April, when the current interim executive chairman will return to a non-exec role.

Barclay is said to have 25 years in the building materials sector, most recently at Batt Cables (which went into administration in January).

Headlam has also appointed an interim CFO whose previous role was at HSS Hire Group (since 2024).

Together they appear to have plenty of recent experience of struggling businesses in the building sector. We can only hope this experience will translate into an understanding of how best to turnaround Headlam’s fortunes.

Personally, I don’t have enough knowledge about this business and its competitors to judge whether a recovery is possible, so I’m viewing this as a special situation. Given the group’s debt burden and lack of profitability, I’m going to leave our RED view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.