Good morning! And welcome to Friday's report.

The Agenda is complete.

2pm: wrapping up the report there, have a nice weekend everyone!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£166bn) | EU approval for treatment of adult patients with previously untreated CLL (leukaemia). | ||

Canal+ SA (LON:CAN) (£1.99bn) | Confirmed 2025 revenue and EBITA outlook. 2025 cash flow from operations to exceed €500m. | ||

Assura (LON:AGR) (£1.57bn) | Meetings to implement Cash Offer adjourned until further notice. Reciprocal due diligence ongoing. | ||

Trainline (LON:TRN) (£1.17bn) | SP +3% Trainline selected as a technology supplier to support digital pay-as-you-go trials. This is "a strategic opportunity to to demonstrate the benefits of [TRN's] in-app solution in a live environment", ahead of pay-as-you-go's potential rollout around the UK. Another announcement will follow upon formal contract signing. | AMBER/GREEN (Graham) [no section below] The potential financial consequences of this development aren't spelled out - and I imagine they would be very difficult to predict. But if digital pay-as-you-go is rolled out around the UK, then clearly Trainline will want to be at at the heart of this important change in the sector. I've long admired the company's quality metrics and I'm happy to upgrade it to AMBER/GREEN today, although I suspect that my fellow writers might disagree with this stance. The shares continue to trade below their £3.50 IPO price (2019) and have never paid a dividend, but the company has made significant financial progress over the past six years and consensus estimates suggest that its profits will continue to grow. At a P/E multiple of 13x, I think it offers some quality and value. | |

Pinewood Technologies (LON:PINE) (£402m) | Buys 51% interest in US JV from Lithia Motors for $76.5m. New shares to be issued at 386.5p. | AMBER/GREEN (Graham) This is a High Flyer - an interesting growth story where the growth opportunity has just increased thanks to the buyout of its partners in North America. Not only will Pinewood shareholders enjoy the full benefit of their progress across the pond, but that progress should come more easily now that US auto dealers will not be buying Pinewood products directly from a competitor. | |

MHA (LON:MHA) (£296m) | SP +9% Trade strongly in H2 of FY Mar 25. Rev growth, margins, cash in line. Adj. EBITDA ahead. This is a very recent IPO, floating in April at 100p (see here). | AMBER (Graham) [no section below] I like to stay neutral on recent IPOs, due to the risk of overvaluation and hidden risks. I'd also bear in mind the general point that forecasts put out prior to IPO can easily be engineered to create an ahead-of-expectations "surprise" shortly thereafter. So personally I wouldn't get too enthusiastic about this one just yet. Let's see how much of the adjusted EBITDA gets converted into real, clean profits now that they've moved away from an LLP structure. | |

Intuitive Investments (LON:IIG) (£251m) | Positive momentum for Hui10, Chinese lottery tech company. NAV/share 153.2p (SP:122.5p). | ||

Camellia (LON:CAM) (£143m) | 215k shares were validly tendered (7.8% of shares in issue), less than max allowed. £11.6m value. | ||

abrdn Diversified Income and Growth (LON:ADIG) (£136m) | Objective: orderly realisation of assets, return of cash. NAV ps 68.42p as of 31st March 2025. | ||

Avacta (LON:AVCT) (£133m) | Phase 2 trials planned for H1 2026. Cash £17m (April), runway to Q1 2026. Pre-tax continuing losses for 2024 were £29m. Material uncertainty. | RED (Graham) [no section below] It's so very late to publish results for FY Dec 2024. Revenues so far are de minimis. The company's first drug program has ongoing phase 1 trials, with phase 2 planned for H1 2026. The cash runway goes as far as Q1 2026 and the footnotes in these results state: "...the Group and the Parent Company are dependent on raising funds to advance their key projects and investments to remain cash positive during the going concern period. There are currently no agreements in place and there is no certainty that funds will be raised within the appropriate timeframe." As the existing equity is unsafe, this is an automatic RED. | |

SDI (LON:SDI) (£74m) | £4.75m. Designer/manf’r of furnace systems for advanced material processing and testing. | AMBER/GREEN (Graham) A nice little bolt-on acquisition at a modest earnings multiple; this is the core of SDI's strategy. Opens new markets to the group and creates new cross-selling opportunities. Broker estimates have been adjusted higher. | |

Anexo (LON:ANX) (£72m) | Revenue -1% (£141.9m). PBT -35.7% (£14.8m). Trading since the year end has been in line. | ||

Bango (LON:BGO) (£72m) | 2024 loss $3.7m. Adj. EBITDA for 2025 in line. Modest increase of $1m vs. consensus for FY26. | AMBER/RED (Graham) [no section below] Another very late set of results, which I take as a red flag. The company again posts an operating loss, albeit a smaller one than the prior year, while the headline results rely very heavily on adjustments - another red flag for me. Net debt finished the year at $1.8m but as that was nearly six months ago it doesn't seem very relevant now. The company's debt facilities have since been restructured, as announced in a separate RNS. I am going to downgrade this to AMBER/RED as I note that Singer are now forecasting that the company will have net debt (excluding leases) of $10.6m at the end of 2025. This was previously forecast to be only $1.6m. Given the shakiness of the company's financial performance, I would not be comfortable investing in its equity while it manages outstanding debts. |

Our rating system - the last six months

While I've been away from writing duties, one of my projects has been to update the spreadsheet that accompanies this report.

The overall headline is that we've looked at 549 different stocks in the last six months, and more than half of these have been looked at more than once.

Something I particularly wanted to investigate was the companies that we were fully "GREEN" on, that subsequently issued profit warnings.

There were only five of these:

- Conduit Holdings (LON:CRE)

- Impax Asset Management (LON:IPX) (I'm long this one)

- Polar Capital Holdings (LON:POLR)

- RWS Holdings (LON:RWS)

- Van Elle Holdings (LON:VANL)

My main finding is that despite their profit warnings, these stocks haven't performed all that badly. Or more specifically:

Conduit Holdings (LON:CRE) - we were GREEN on this on 19th February. Share price at the time: 406p. It subsequently issued a profit warning on 31st March. Its current share price: 386p. So despite a profit warning, it is only down by 5% since we were last GREEN on it.

Doing the same for the other stocks that issued profit warnings:

Impax Asset Management (LON:IPX) is up 9% since we were last GREEN on it, despite issuing a profit warning since then.

Polar Capital Holdings (LON:POLR) is down 10% since we were last GREEN on it

RWS Holdings (LON:RWS) is the main casualty, down 55% since we were last GREEN on it.

Van Elle Holdings (LON:VANL) is down 3% since we were last GREEN on it.

As you can tell, the point of my analysis is not to say that companies we are GREEN on can't issue profit warnings - they most certainly can!

My point is that most of these companies have survived their profit warnings really well, which I think can broadly be attributed to their balance sheet strength and their fundamental cheapness when we were initially GREEN on them. More work is needed. I'm eager to learn more about how our rating system is performing!

Google's AI assistant, Gemini, assisted me in this. It required a lot of coaxing but once it understood what I wanted, it did a fine job!

Graham's Section

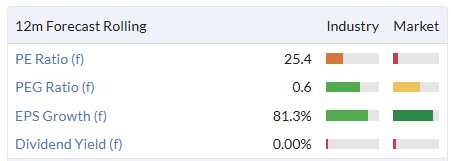

Pinewood Technologies (LON:PINE)

Up 13% to 451.7p (£454m) - Acquisition of Lithia’s Stake in North American JV - Graham - AMBER/GREEN

Formerly the car dealership group Pendragon, this is now purely the software business Pinewood.

Some interesting news this morning as it announces the buyout of its joint venture partner in North America.

The price is $76.5m (about £56.5m) for the entire 51% stake held by Lithia Motors ($LAD).

This does mean some dilution, as it’s going to be funded by the issuance of 14.6m shares at 386.5p.

Against 100 million shares outstanding, that’s 15% dilution.

In further news:

Pinewood.AI is also delighted to announce that, subject to completion of the Acquisition ("Completion"), it will enter into a five year contract with Lithia to roll-out Pinewood.AI's software to all of Lithia's current and future sites across the US and Canada by the end of 2028 at the latest…

By the end of 2028, Pinewood anticipates $60m of annual revenue from Lithia in North America, including revenue from both their current product suite (expected to generate $40m) and additional applications.

Rationale: among many other reasons, it is thought that this deal will remove “the perceived ‘competitor overhang’” as rival dealership groups may be more willing to use software that is not so directly backed by their competitor, Lithia.

This mirrors the separation of Pinewood from Pendragon in the UK.

However, Lithia will remain “a key customer and committed long-term minority strategic shareholder”. I don’t think that any change has been signalled when it comes to Lithia 22% ownership of Pinewood itself. The change only relates to their ownership of the North American JV.

CEO comment:

"We are delighted to have reached an agreement with Lithia to acquire the majority stake of the North America joint venture. The US and Canada are central to our growth strategy, and through the Joint Venture, we have made significant progress towards commercialising the Pinewood.AI platform for the North American market. Assuming full control of the Joint Venture will strengthen our ability to fully capitalise on the opportunities available in a key strategic growth market…

I would like to take this opportunity to thank Lithia for their partnership in the joint venture and we look forward to working with them as a key customer long into the future."

Trading update - contained within today’s announcement is a reassuring update.

Trading in the current year has continued positively, and the directors of Pinewood.AI (the "Directors") remain highly confident in the opportunities ahead for Pinewood.AI.

Graham’s view

I understand that Pinewood shareholders are very excited about their North American opportunity - and so it makes sense that they would be excited about having 100% ownership of it. Accepting a modest amount of dilution for this makes good sense, in my view.

The deal seems to make long-term success in North America more likely and it doubles Pinewood’s ownership interest in that success.

So I’m finding very little to dislike in this news.

We last covered the stock in April when I upgraded my stance to AMBER/GREEN. Perhaps it’s worth another upgrade today, but bear in mind that you don’t get a cheap multiple here - you are buying into an interesting growth story.

I might be a little slow to act here but for now the AMBER/GREEN stance continues to make sense to me. For growth-oriented investors, I would say that it’s certainly worth a closer look.

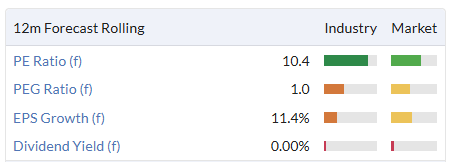

SDI (LON:SDI)

Up 9% to 77.25p (£81m) - Acquisition of Severn Thermal Solutions - Graham - AMBER/GREEN

We have news of a fresh acquisition from this buy and build group.

The new asset is Severn Thermal Solutions Ltd, which is “a designer and manufacturer of high temperature furnace systems and environmental chambers for advanced material processing and testing”.

The price: £4.75m, plus SDI will pay for the cash acquired of £3.6m.

SDI is still small enough that deals of this size can have the potential to move the needle for them.

Severn is said to have a “scientific niche in a growing market, blue-chip customer base and strong international revenues”. It gives SDI “expansion into the controlled environment market” with new, intra-group cross-selling opportunities.

Severn’s financial performance last year:

For the year ended 30 September 2024, Severn delivered revenue of £2.42m, adjusted EBIT of £0.88m (adjusted to reflect Severn's cost base as part of the enlarged Group) and a reported EBIT of £1.06m (all unaudited).

So it looks like SDI are paying 5x the EBIT that Severn would have achieved as part of SDI.

Estimates: the acquisition is earnings accretive and Cavendish have updated their forecasts for FY April 2026.

Forecast revenue up £2m to £75.4m.

Adj. EBITDA up £0.7m to £14.2m.

Adj. PBT up £0.4m to £9.8m (there are higher interest costs).

Graham’s view

The market cap is up by about £7m which is certainly a bullish response to the announcement of a £5m debt-funded acquisition. But SDI shares weren’t priced very aggressively to begin with:

I was AMBER/GREEN on this in May (see here) and am happy to retain that stance again today. The main negative for me has been the lack of organic growth, but if the company can successfully add bolt-on growth - which is its primary strategy, after all - then why complain?

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.