Good morning!

There are no major overnight developments, but the price of oil continues to climb.

Brent crude futures are trading around $110, very close to the highs they reached in March and early April.

All done for today, thank you.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£217bn | SR76) | Breztri approved in the US for asthma as first and only triple therapy for patients 12 years of age and older. | ||

BP (LON:BP.). (£89bn | SR88) | Underlying replacement cost profit $3.2bn (Q125: $1.4bn). Without adjustments: replacement cost profit $662m (Q125: $569m). | ||

GSK (LON:GSK) (£82bn | SR94) | FDA has accepted for priority review a New Drug Application for bepirovirsen, for the treatment of adults with chronic hepatitis B. | ||

Barclays (LON:BARC) (£58bn | SR84) | ROTE 13.5% (Q1 2025:14%). EPS 14.1p (Q1 2025: 13p). “Another solid quarter… despite a one-off charge and impairments in the quarter… we remain confident in delivering all our financial targets across a range of environments.” | ||

Anglo American (LON:AAL) (£43bn | SR62) | Copper production +1% to 170,400 tonnes. Premium iron ore production down 2%. Production and unit cost guidance for continuing businesses remains unchanged for 2026. | ||

Coca-Cola Europacific Partners (LON:CCEP) (£32bn | SR76) | “Reaffirming full-year guidance.” Volume +8.5%, revenue per unit case +0.8%. Revenue +9.4% at constant FX. | ||

Greatland Resources (LON:GGP) (£5.0bn | SR95) | Quarterly production of 82,723 ounces of gold at AISC of $2,056/oz. “...we currently expect full-year production to be around, or slightly above, the upper end of the guidance range of 260,000 - 310,000 ounces, and full-year AISC to trend towards the lower end of the guidance range of $2,400 - $2,800 per ounce.” | ||

Howden Joinery (LON:HWDN) (£4.4bn | SR90) | Underlying revenue +3.7%, or +2.8% on a same depot basis. “We remain confident in our differentiated business model and we are on track with the outlook for 2026.” | ||

Taylor Wimpey (LON:TW.) (£2.9bn | SR73) | Net private sales year to date, excluding bulk sales, of 0.72 per outlet per week (2025: 0.76). “...more recently we have experienced some underlying pricing pressure.” Pricing 1% lower year on year. Also, as a result of rising energy costs, build cost inflation is now expected to be low to mid single digit for 2026. | BLACK? (AMBER =) (Roland) Taylor Wimpey is trading at a 30% discount to book value that could offer long-term value. But the near-term outlook suggests the discount may be fair – profit margins are under pressure, sales are lower than last year and 2026 earnings forecasts have been cut by 25% over the last 12 months. Consensus estimates prior to today suggested the business could generate a 6% return on equity this year. That’s insufficient to justify a return to book value, in my view. Overall, I think the valuation is probably fair at the moment so am remaining neutral. | |

WPP (LON:WPP) (£2.8bn | SR48) | Revenue down 4% LfL. Revenue less pass-through costs down 6.7% LfL. “Performance in the quarter is consistent with expectations and guidance… we continue to expect 2026 LFL revenue less pass-through costs to decline in the mid to high-single digits in the first half of 2026 with an improving trajectory in the second half and headline operating profit margin to be 12% to 13%.” | ||

Canal+ SA (LON:CAN) (£2.28bn | SR83) | Combined Group revenue broadly flat (down 0.2% like-for-like). Guidance reiterated for 2026. “A solid start to 2026”. | ||

Georgia Capital (LON:CGEO) (£1.4bn | SR83) | NAV per share +2.1% to 43.34p (or +0.1% to 154.82 Georgian Lari). | ||

Travis Perkins (LON:TPK) (£1.16bn | SR80) | Challenging trading conditions. Revenue down 1.7% like-for-like. “Looking forward the Group remains focused on managing its overheads and identifying further operational efficiencies, whilst ongoing capital discipline and incremental cash generation opportunities are continuing to enhance the Group's financial position.” | BLACK (AMBER/RED =) (Graham) [no section below] Travis Perkins was supposed to see revenue growth this year, and so a 1.7% like-for-like decline, with a 3.1% total decline, is not what the market wanted to see here. "Construction activity levels remain subdued" - an important but perhaps unsurprising warning for anyone invested in the sector. Recent full-year results for 2025 were poor with adjusted operating profit of £133m converting to an unadjusted operating loss of £97m after impairments and restructuring costs. At least there was no net debt once leases are excluded. Roland was moderately negative on this a year ago and with today's announcement amounting to a profit warning, I'll leave that untouched | |

Telecom Plus (LON:TEP) (£1.14bn | SR58) | Organic net customer growth 10.3%. Total net customer growth 23.3%. Adjusted PBT at the bottom end of our previously guided range of £132m-£138m, following reduced energy consumption during an unseasonably warm winter. | BLACK (AMBER/GREEN ↓) (within the range, but at low end) (Roland) While customer growth remained strong last year, competitive pressures and the mild winter contributed to disappointing growth in energy and broadband demand. The Insurance business is also proving slow to rebuild following a pause in sales in FY25. Changes to the company’s shareholder returns policy also mean that a near-term dividend cut is likely, in my view, with the balance being directed into buybacks for the first time. I’ve moderated my previously positive view today to reflect the weaker outlook, but on balance I still believe Telecom Plus is likely to be attractively valued at current levels. For this reason, I am remaining somewhat positive ahead of June’s results and strategy update. | |

Conduit Holdings (LON:CRE) (£695m | SR88) | CFO intends to retire. | ||

Serabi Gold (LON:SRB) (£239m | SR99) | Proven and Probable Reserves at Palito Complex 228,400 ounces compared to 147,000 ounces in April 2025. Consolidated Measured and Indicated Resources of 730,800 ounces of contained gold, a 29% increase compared to 567,400 ounces in March 2025 for Palito and April 2024 for Coringa. | ||

Card Factory (LON:CARD) (£229m | SR53) | Revenue +7.4%. EBITDA -8.4% (£117m). PBT -31.5% (£44m). Adjusted PBT in line with revised guidance. “While we remain mindful of this external backdrop, the Board expects Adjusted PBT in FY27 to be in line with the current market consensus.” | AMBER/GREEN ↑ (Graham)

We’ve been neutral on this since the December profit warning, and I’m going to tentatively upgrade it by one notch today. Calculating the P/E multiple myself, at the midpoint of the range, I get 5.5x. Unfortunately, I find it difficult to resist multiples like this, even for companies with a little leverage. At 7-8x, I would probably stay neutral. At 5.5x, with two in-line updates and a buyback reducing the share count, I’m interested again. | |

Ferrexpo (LON:FXPO) (£194m | SR55) | An equity fundraise of at least $100m is the only viable solution to meet ongoing obligations and provide sufficient working capital for short-term operational requirements. The largest shareholder is supportive and would participate on a pro rata basis. Results will not be published before the 30th April deadline, so FXPO shares will be suspended on 1st May. | ||

Mkango Resources (LON:MKA) (£187m | SR12) | HyProMag subsidiary officially opens its rare earth magnet recycling and manufacturing plant in Germany today. When commissioned, will have an initial capacity of c.100t/yr of NdFeB. | ||

Tullow Oil (LON:TLW) (£171m | SR41) | Production down 22% to 40.4 kboepd, adj EBITDAX down 42% to $586m. Free cash flow of $99m, net debt reduced to $1,353m at year end (2024: $1,452m). Outlook: production expected to be at the higher end of 34-42 kboepd guidance range. FCF guidance of $70-175m at $70-100/bbl. Recent refinancing provides liquidity headroom of >$200m. | ||

Scancell Holdings (LON:SCLP) (£135m | SR24) | Receives FDA Fast Track Designation for iSCIB1+ in advanced melanoma. Potent and durable efficacy with iSCIB1+ of 77% progression free survival (PFS) at 20 months, in combination with ipilimumab and nivolumab, demonstrated in the Phase 2 SCOPE trial. | ||

Eleco (LON:ELCO) (£104m | SR51) | Ahead of expectations: revenue up 20%, ARR up 29% to £34.3m. Adj pre-tax profit up 35% to £7.3m, with adj EPS up 24% to 6.3p. Outlook: challenging market conditions in some sectors, but confident of the financial outlook in 2026. Cavendish updated forecasts: - 2026E adj EPS: 6.7p (unch.) - 2027E adj EPS: 7.4p (new f’cast) | AMBER/GREEN ↑ (Roland) [no section below] I took a neutral view on this supplier of building management software in January, highlighting impressive long-term growth but recent cuts to EPS forecasts. I’m pleased to see this situation appears to have reversed today – the shares are still slightly lower than when I last looked, but 2025 results are ahead of expectations and broker forecasts suggest further growth in 2026 and 2027. There’s net cash on the balance sheet and quality metrics look decent too, with a continuing operating margin of 13% and ROCE of 14%. A forecast P/E of 19 isn’t cheap, but I think it’s fair to be slightly more positive here given progress, so I’m moving my view up by one notch today. | |

Tracsis (LON:TRCS) (£96m | SR62) | Revenue up 7%, adj EBITDA up 31% to £5.0m. Adj EPS up 34% to 10.2p. H1 performance “consistent with expectations”. Outlook: adj EBITDA expected to be in line with full-year expectations. | ||

Cake Box Holdings (LON:CBOX) (£85m | SR47) | Revenue expected to be up by 43% at £61.2m, with profit in line with market expectations. Excluding Ambala contributions, revenue to be up c.12% to c.£46.7m. Opened 37 new stores last year, taking total estate to 310 stores. | AMBER/GREEN ↑ (Graham) [no section below] This update doesn't spell out like-for-like growth, only saying that LfL sales at Cake Box were "positive". Both Cake Box and the acquired Ambala business are being rolled out which could potentially make this an interesting growth story. I would like more detail on underlying growth rates but even without that granularity I can see the potential attractions here with adj. PBT of £8.6m pencilled in for FY March 2026 and then £10m in FY March 2027 (thanks to ShoreCap for estimates). In that context, forecast net debt of £10.5m should be manageable. I'll upgrade to AMBER/GREEN on the basis that it's offering growth at a reasonable price (PEG ratio <1) along with an attractive dividend yield at this price (6%). | |

Orosur Mining (LON:OMI) (£73m | SR14) | Soil sampling completed at El Cedro south - prospectivity enhanced. Aeromag over El Cedro and APTA now completed. Pepas rig moved from Pepas West to new target. | ||

Likewise (LON:LIKE) (£61m | SR44) | Revenue up 9%, gross margin up 0.4% to 31.1%. Adj pre-tax profit up 56% to £3.1m. Outlook: Q1 sales up 15%, April seeing “similar momentum”. Global conditions make future months difficult to predict, but remain confident in medium-term objectives. Zeus 2026 forecasts unchanged today for adj EPS of 1.2p. This forecast was previously cut by 24% in November, when Likewise warned on profits. | AMBER/RED = (Roland) [no section below] It seems fair to follow-up on the performance of this flooring distributor after my comments on rival Headlam (LON:HEAD) yesterday. The implications for Headlam shareholders don’t seem that good – Likewise continued to expand sales and margins last year and is enjoying positive momentum so far this year. That’s a marked contrast to Headlam’s strategy of shrinking to rebuild margins. Having said that, checking today’s accounts presents a mixed view to me. While growth was strong last year, profitability remained low with a return on capital employed of just 4%. Cash generation also looks poor to me, with my sums suggesting a free cash outflow of c.£750k last year. In part, this is due to the company’s investment in building the infrastructure needed to support up to £250m of revenue (2025: £163m). But there was also a 26% increase in borrowing last year to £11.8m, driven mainly by higher use of invoice factoring. If Likewise can continue to gain market share and improve the utilisation of its growing capacity, then cash generation should also improve. But with such low profitability, I think any slowdown in sales growth could become uncomfortable. Today’s outlook statement includes a note of uncertainty, reflecting macro conditions. With the stock already trading on 20x forward earnings and November’s profit warning still relatively recent, I’m going to leave my previous AMBER/RED view unchanged for a little longer. | |

Poolbeg Pharma (LON:POLB) (£31m | SR30) | Cash of £7.7m at 31 Dec, “funded through to delivery of near-term clinical milestones into 2027”. Significant progress made in the first-in-patient POLB 001 clinical trial, titled TOPICAL, with interim data expected this summer. | ||

Everyman Media (LON:EMAN) (£30m | SR40) | Revenue up 8.8%, adj EBITDA up 10.6% to £17m. Pre-tax loss of £10.2m (FY24: £10.2m) with net debt up £3.5m to £21.6m. Market share increased to 5.8%, spend per head also improved. Outlook: Q1 2026 has started well. New CEO and CFO focused on deleveraging and growth. | RED = (Graham) | |

Eden Research (LON:EDEN) (£29m | SR32) | Expects to be broadly in line with market expectations for the 15 months to 31 March 2026: revenue to be c.£4.9m with a pre-tax loss of c.£2.9m. | ||

Hardide (LON:HDD) (£28m | SR62) | SP +7% Received further £1.8m of new orders from its “large North American energy sector customer”. Expected delivery by end FY26. Additional to current forecasts, now expects revenue and financial performance to be materially ahead of previous expectations. | AMBER/GREEN (Graham) [no section below] I'm going to open with an AMBER/GREEN on this coatings company, noting that its EPS forecast has been boosted by nearly 15% at Cavendish today. With a new EPS forecast of 3.4p, the shares are trading at 11x earnings. I also note that the company is forecast to close the current financial year with £3m of net cash. Perhaps I should be fully GREEN on this but the company is still very small and was unprofitable for many years up to this point. There are signs of it coming to life now and for a small-cap momentum play, it looks very promising. A new CEO was appointed in June 2024, with deep expertise in the sector. | |

Kr1 (LON:KR1) (£27m | SR23) | 2025 revenue down 62% to £4.8m, year end net assets down 64.4% to £49.6m (27.93p per share), due to decline in digital asset valuations across the period. | ||

Headlam (LON:HEAD) (£24m | SR25) | Two largest shareholders (c.15% & 11%) have confirmed they will vote against FS resolutions to remove current directors. Board considers FS requests “disproportionate and destabilising” and says many concerns raised by FS are already being addressed. | Roland: see our comments from yesterday for the broader background to this situation. | |

Pebble Beach Systems (LON:PEB) (£24m | SR70) | Revenue up 7%, adj pre-tax profit up 173% to £3.0m. Adj EPS of 2.7p. Outlook: Q1 trading “encouraging”. The board believes Pebble is well-positioned to achieve 2026 objectives. | ||

Great Southern Copper (LON:GSCU) (£22m | SR4) | Final Phase III assay results confirm down-dip and along strike continuity of high-grade Cu-Ag mineralisation at Mostaza. Continuity of upper Pb-Zn+Ag mineralised breccia zone also confirmed. | ||

Symphony Environmental Technologies (LON:SYM) (£17m | SR12) | Further to Dec 25 update, FY25 revenue to be higher than previously guided at c.£5.7m, with an adjusted EBITDA loss of c.£0.9m. Outlook: sales momentum continued with revenue c.10% ahead of prior year period. Positive EBITDA in Q1 2026. | ||

Southern Energy (LON:SOUC) (£15m | SR37) | Y25 sales up 12% to $18m, average production of down by 21% to 12,039 Mcfe/d in 2025 (96% nat gas), due to a dispute with a pipeline operator. FY25 net loss of $3.7m. | ||

Xeros Technology (LON:XSG) (£13m | SR9) | Revenue up 50% to £0.24m, adj EBITDA loss reduced by 24% to £3.3m. Net cash of £5.5m. Secured launch agreement for XC1 with a “top ten global washing machine brand”. | ||

Nexus Infrastructure (LON:NEXS) (£10m | SR49) | Nexus expects H1 revenue up 6.6% to £32.2m, in line with expectations. Early signs of a market recovery were impacted by the conflict in the Middle East. | ||

Powerhouse Energy (LON:PHE) (£10m | SR3) | Recently started new project with Welsh battery developer with a contract value of c.£260k. Ballymena project continues to ”advance well”. New business development remains active. |

Graham's Section

Card Factory (LON:CARD)

Up 1% at 66.9p (£231m) - Preliminary Results - Graham - AMBER/GREEN ↑

It’s a mixed bag of results here, as expected.

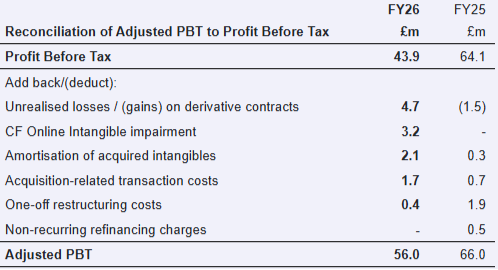

Adjusted PBT for FY January 2026 comes in at £56m, down from FY25’s £66m.

The January trading update confirmed that adjusted PBT would be within the range of £55-60m. That was the guidance given at the December profit warning.

Other key points from today’s results:

Revenue +7.4% (but this is not like-for-like, includes Funky Pigeon and wholesale partnerships)

Like-for-like store sales were minus 0.2%.

Unadjusted PBT falls 31.5% to £43.9m

27 net new stores were opened during the year.

Turning to the balance sheet:

Net debt is £68m (up from last year's £59m).

Adjusted leverage (excluding leases) is 1x, up from last year’s 0.7x.

For successful and predictable businesses, a leverage multiple of 1x would be considered very conservative.

For retailers, given their accident-prone nature I would suggest that it’s right to expect low leverage or ideally net cash.

Cardfactory aims to keep leverage below 1.5x at all times, which sounds sensible to me.

Dividend: gets an increase to 5p.

Buyback: new £15m buyback.

CEO comment: acknowledges “softer high street footfall” in H2, “particularly during our peak trading period”. But on the bright side:

The Group remains highly cash generative, and our 'Simplify & Scale' efficiency and productivity programme will continue to help mitigate inflationary headwinds…

Looking ahead, as widely documented, the external environment remains uncertain. We have robust plans in place for FY27 to deliver further progress against our strategic priorities and medium-term ambitions…

Outlook: in line with the current market consensus.

This is for adjusted PBT of £54.8m to £58.2m (FY January 2027), with a seasonal H2 weighting.

They expected adjusted leverage to be “between flat and 0.2x lower”.

Over the medium term, they remain “confident in cardfactory's ability to deliver mid-to-high single digit percentage Adjusted PBT growth per annum”.

In terms of strategy, they are aiming to grow market share in the broader “celebrations” market. This will mean selling more non-card products, at lower gross margins than cards, so their overall gross margin may gradually reduce.

There’s also an FX exposure worth mentioning, as half of products are bought from the Far East and are priced in US dollars. A hedging policy is in place.

Adjustments

Finding a clear breakdown of the adjustments took a little searching, but here it is.

As you’ll see, last year’s results were much cleaner (£66m adjusted PBT vs. £64.1m actual PBT).

This year, however, there is a meaningful difference between the adjusted result and the actual results.

The waters are muddied by a large (£4.7m) unrealised loss on derivative contracts - hedging contracts on the FX exposure I mentioned above.

Perhaps controversially, I would not automatically exclude this loss. I don’t want to get too into the weeds on this issue, but I’m just not convinced that this adjustment will, over time, actually help to smooth out the annual results. The hedge itself is supposed to smooth out the results over time, therefore excluding the hedge strikes me as potentially not smoothing out results.

The other items are typical. Excluding the impairment of intangibles is fine, but then we should probably assume that the company’s intangibles are worthless. If we do that, then the company’s balance sheet has negative tangible net assets (£355m net assets including £389m of intangibles).

My best guess of where “real” profitability lies is around £51m.

Graham’s view

We’ve been neutral on this since the December profit warning, and I’m going to tentatively upgrade it by one notch today.

The positives:

Two important “in line” updates since December.

Still highly profitable, even without adjustments, despite the profit warning.

Likely to remain highly profitable this year.

Cheap earnings multiple, with a ValueRank of 98.

The negatives:

Negative LfL store growth.

Overall profits may be lower again this year.

Massively exposed to unpredictable High Street/Consumer trends.

The leverage multiple of 1x is a little adventurous, with the company preferring to buy back shares and pay dividends rather than reduce it.

In conclusion, I do think this is priced to do well for risk-tolerant shareholders.

Calculating the P/E multiple myself, at the midpoint of the range, I get 5.5x.

Unfortunately, I find it difficult to resist multiples like this, even for companies with a little leverage.

At 7-8x, I would probably stay neutral.

At 5.5x, with two in-line updates and a buyback reducing the share count, I’m interested again.

This looks like a high-risk, high-reward type of situation:

Everyman Media (LON:EMAN)

Down 1% to 32.7p (£30m) - Full Year Results to 1 January 2026 - Graham - RED =

This recently got a new CFO, and it announced last week that the interim CEO had agreed to become permanent CEO.

They have a big job on their hands. Here are the 2025 results

Two new venues opened during the year.

Revenue +12.4% with admissions +6.1%, spend per head +5.9%.

Adjusted loss before tax £5.2m (previous year: £6.3m loss).

Statutory loss £10.2m (previous year: £10.2m loss).

Net debt creeps up to c. £22m.

Market share is thought to have increased from 5.4% to 5.8%.

Membership is up 18.5% to 66,910 - one of the few very encouraging metrics.

They have finally paused expansion efforts:

Prioritising optimisation rather than expansion, with no new venues opening in 2026 whilst planning is underway to invest in limited number of new venues for 2027 funded through free cash flow

Outlook:

Trading performance in Q1 2026 has started well. We are encouraged by a strong film slate this year, with highlights including Hamnet, Wuthering Heights, Michael, The Devil Wears Prada 2, Toy Story 5, The Oydssey, Spider-Man: Brand New Day, Avengers: Doomsday and Dune: Part Three

CEO comment:

"We enter 2026 with positive momentum and clearly defined priorities. The year ahead is about resetting to drive growth by building strong audience engagement, creating operational efficiencies, unlocking emerging new sources of income whilst reducing debt.

Through expert film curation, beautifully designed signature spaces and a differentiated hospitality offering in strategically located venues, the Everyman brand is well placed to meet the demand for premium cinema experience."

Estimates from the company’s Nomad, Canaccord, are “under review”.

Canaccord did have FY25 and FY26 estimates for Everyman until the December profit warning. While they have revisited the story a few times since then, they haven’t yet given new estimates. With only eight months left of the current financial year, and still no estimates, that's a red flag for me.

If you’re using the StockReport for this one, watch out - it might be looking at Canaccord estimates that are no longer in force.

Even with those stale estimates, the categorisation as a Value Trap rings true to me:

Graham’s view

We’ve been consistently RED on this, and I see no reason to change stance today.

Halting expansion looks like the right move - we can now find out how much cash and profits the existing venues can generate on their own.

And as a film fan, I agree that the releases this year are promising.

If they prove to be cash-generative, and if net debt starts to move in the right direction, perhaps I won’t need to be negative on this one forever.

Roland's Section

Telecom Plus (LON:TEP)

Down 13% at 1,238p (£1.0bn) - Year End Trading Update - Roland - (BLACK?) AMBER/GREEN ↓

Today’s trading update from Utility Warehouse owner Telecom Plus has received a poor reception. The company has reported strong continued customer growth, but energy consumption and profits appear to have come under pressure due to warmer winter weather and tougher competition.

As a result, adjusted pre-tax profit for the year to 31 March is now expected to be at the bottom end of guidance. This stops short of a profit warning, but it’s clearly not good news.

Having read through the RNS, I think the sell-off could be overdone, but I can also see some areas where shareholders (or potential shareholders) may want to pay attention.

I’ll split this review into three sections to reflect the content of today’s update – trading, financial guidance and strategy.

Trading

The headline figures here seem fairly strong:

Total customer growth of 23.3% to 1.43m, including 193k customers acquired from TalkTalk

Organic net customer growth of 10.3% to 1.26m

Total number of services provided up 12% to 3.80m (organic service number +7.6%)

Partner numbers (self-employed sales agents) up by 7% to 77k

However, there were some nuances in these figures that may have affected profitability last year.

The seemingly positive organic service growth rate of 7.6% masked a very mixed bag of growth rates across Telecom Plus’s service offerings:

Mobile: +29%

Energy: +1.8%

Broadband: +3.8%

Insurance: -8.3%

These figures seem to highlight two underlying issues:

Energy & Broadband: “strong competitive activity” has slowed service growth. I was interested to learn “the shape of the energy wholesale forward curve enabl[ed] competitors to offer fixed price energy tariffs meaningfully below the Ofgem price cap for much of the year.” Apparently customers have been voting with their feet to find cheaper energy deals – the customer churn rate increased to 14.2% (FY25: 13.7%).

Insurance: sales have been “slower than expected” to recover from the pause in new insurance sales in FY25 (for regulatory issues).

More encouragingly, the acquisition of customers from struggling TalkTalk appears to have been successful in economic terms:

The customers acquired from TalkTalk increased our broadband services by 193k. These customers are expected to generate a return above post-tax WACC, even without cross-selling any other services to them.

160k of these had been migrated onto our systems by year end, with the remainder expected to migrate by the end of the first quarter of FY27. Initial cross-sell results are continuing to perform strongly, with 14.5k customers upgraded and cross-sold during the year.

Financial outlook

Profit guidance: CEO Stuart Burnett now expects to report adjusted pre-tax profit at the bottom end of the (unchanged) guidance range of £132m to £138m. I don’t have access to updated earnings forecasts today, but my impression is that previous consensus was c.£135m. If brokers accept today’s new guidance, this may only be a c.3% downgrade – smaller than today’s share price drop implies.

Year-end leverage is expected to be c.1x EBITDA – I don’t see this as a serious concern.

The other piece of financial news today relates to shareholder returns. I suspect that it signals a dividend cut is likely.

Telecom Plus has a longstanding policy of paying out 80% of adjusted after-tax profit to shareholders. Until now, this distribution has been made entirely through dividends – the payout hasn’t been cut for 20 years.

However, “in response to feedback from many shareholders”, this will now change:

We intend to maintain a total payout ratio of at least 80% of adjusted profit after tax, but this will, from our upcoming full year results in June, now be split between both dividends and share buybacks, with at least 50% of the total payout each year being allocated to ordinary dividends and the remainder being allocated to either share buybacks or special dividends, depending on whether the Company is able to repurchase shares at below their fair value.

How might this work? Telecom Plus doesn’t specify its criteria for gauging fair value today, but the approach used by Next requires an 8% pre-tax return on investment to justify buybacks:

Based on this method, I estimate fair value for TEP shares could be around £20 – significantly above today’s c.£13 level;

Assuming FY26 earnings of c.97p per share, I estimate this year’s dividend could be cut to c.49p, with the remaining c.29p per share returned through buybacks. That would give a dividend yield of around 4% at current prices. Prior to today, the forecast yield was over 7%.

Assuming fair value is calculated in a realistic and consistent way, then I think the narrow financial logic for buying back shares below fair value is sound.

However, today’s share price drop suggests to me that some investors may share my disappointment at the potential loss of income from this previously reliable payer.

Strategy update

The Utility Warehouse business has always relied on an unusual word-of-mouth direct sales approach, with self-employed agents recruiting networks of customers and other agents, from which they earn commission.

However, there are signs this may be changing. The acquisition of nearly 200k customers from TalkTalk is one example, as was the rumour in December that Telecom Plus was considering a bid for Ovo Energy’s retail business.

Any approach to Ovo seems to have come to nothing, but comments in today’s update suggests the intention to find new growth routes is hardening into a firm plan:

Our focus is on progressively increasing services per customer, reducing churn, growing contribution per customer, and enhancing customer lifetime values, in order to maximise long-term shareholder value. As a result, we are currently considering a number of potential initiatives to achieve these goals; we will provide an update on the outcome of this review together with our full year results for the financial year ended 31 March 2026, which we expect to announce on 23 June 2026.

Roland’s view

While Telecom Plus always reports H2-weighted profits due to the nature of its business (domestic gas and electricity consumption is higher during October - March), the company’s previous guidance suggested a heavier-than-usual weighting this year. With hindsight I should have been more sceptical about this than I was when this was first flagged up in November.

While this business has delivered double-digit customer growth in recent years, longer-term progress hasn’t always been in a straight line. Variations in commodity pricing and market conditions mean that growth rates and profits are sometimes lumpy and unpredictable over shorter periods.

Despite the headwinds reported today, I’m inclined to view the current weakness as a potential buying opportunity. In my view, the company’s quality and durable model is demonstrated by its unbroken 20-year dividend record and strong quality metrics:

I think the valuation remains very reasonable, even allowing for a modest cut to expectations:

A caveat to this is the as-yet unknown strategic changes the company may be planning. They could end up having a positive or negative impact on the investment case.

I’d also be interested to know more about the underperforming Insurance business – this effort to expand into financial services has not (yet) been very successful, although I think it could have potential.

I’m going to move our view down by one notch to AMBER/GREEN today to reflect the downgrade to guidance, but I’m reluctant to go any further at this stage. I’ll aim to review this situation again when the full-year results are published in June.

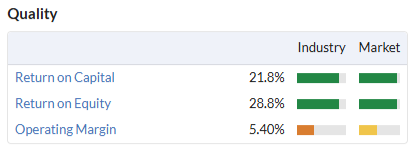

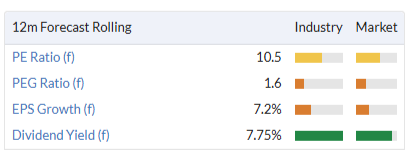

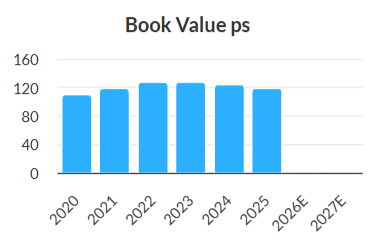

Taylor Wimpey (LON:TW.)

Down 3% at 80.5p (£2.8bn) - Trading Statement - Roland - (BLACK?) AMBER =

It’s not good news: this FTSE 250 housebuilder is reporting slowing sales and increased pressure on profit margins.

The relatively modest share price fall today is probably a reflection of the reality that today’s update isn’t particularly surprising and has already been at least partially priced into the stock over the last year:

Year-to-date trading summary (to 26 April 2026):

Net private sales rate of 0.72 per outlet per week (2025: 0.77);

Total order book value down 5% to £2,229m;

Total order book volume down 6% to 7,689 homes;

Average price reduction of 1% vs last year, with most pressure in South of England;

Operating from 218 outlets (2025: 201);

Land purchases slowing: 1k plots purchases so far this year (2025: 1.7k).

In short, Taylor Wimpey is selling fewer houses at lower prices. That’s not good news in an environment where cost inflation is becoming a growing problem:

As a result of rising energy costs, build cost inflation is now expected to be low to mid single digit for 2026, with cost pressure and surcharges starting to come through from our supply chain.

The company’s previous guidance for build cost inflation in March was “low single digit”.

Profit guidance: there’s no updated profit guidance in today’s statement, but March’s 2025 results included guidance for a 2026 adjusted operating profit of around £400m.

I’d guess this figure will be slightly lower now.

It’s also worth noting that Taylor Wimpey has previously guided for an H2 weighting this year, with only 40% of completions expected in the first half. In my view, this adds to the risk that forecasts will be held until H2 and then downgraded later in the year if trading doesn’t improve.

Dividend & Buybacks: slightly unusually, Taylor Wimpey’s policy on shareholder distributions is based on returning a fixed percentage of the company’s net asset value each year. Current guidance, reiterated today, is for:

c.5% of NAV to be paid as dividends;

2.5% of NAV to be returned through dividends or buybacks, at the discretion of the board.

With the shares trading at a discount to NAV, buying back stock makes sense and Taylor Wimpey has now repurchased £39m of the £52m of shares it plans to repurchase during the first half of the year.

However, crunching the numbers on the dividend suggests to me that a further reduction in the payout may be likely this year if the discount to NAV persists.

A payout of 5% of 2025 NAV (118p) would be 5.9p, 23% below last year’s 7.62p payout.

That implies a forecast yield of about 7% at current levels – still very attractive, but lower than the 9% yield suggested by consensus forecasts.

Roland’s view

Taylor Wimpey shares now trade at a 30% discount to their 2025 year-end net asset value of 118p per share:

Unfortunately, housebuilders are struggling to generate suitable returns on the book value of their equity at the moment.

Forecasts prior to today implied a return on equity of just 6% this year – almost certainly below the group’s cost of equity. Given this, it’s logical for the stock to be trading below book value as this improves the return on cost of equity available to shareholders.

In my view, there’s also a risk that Taylor Wimpey’s NAV could fall further this year, continuing the trend of the last couple of years.

As I’ve discussed previously, the problem for housebuilders is that costs are rising but house prices and volumes are flat or falling. For Taylor Wimpey, this situation has resulted in a 25% cut to 2026 EPS forecasts over the last 12 months alone::

While I think there is probably value on offer at current levels, it’s not clear to me when or where a catalyst will emerge to support a recovery in profitability. There’s a mix of political and economic factors that could influence the outlook at some point, but predicting these is beyond my paygrade.

On balance, my feeling is that the shares are probably fairly priced at current levels on a near-term view. I’m going to leave my previous neutral view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.