Good morning!

There was an exchange of fire overnight in the Strait of Hormuz, as the US retaliated with missile strikes following Iranian attacks on US warships transiting the Strait. But both sides appear increasingly desperate to maintain the fragile ceasefire, with President Trump claiming the arrangement is still “in effect” and Iranian state television reporting the situation as “back to normal”.

Closer to home, Labour is reported to have suffered significant losses in yesterday’s local elections, with corresponding gains for Reform. However, it’s too soon to be sure of the scale of any rout, as many key areas will not report results until later today.

European markets appear to be set to extend yesterday's declines, while oil remains below $100:

The FTSE 100 to open down by 0.7% at 10,220

S&P 500 to open up by 0.3% at 7,359

Germany's DAX is expected to open down by 0.8%

Brent Crude at $99.80 a barrel

Gold at $4,727/oz

Today's report is now complete. Thank you for reading and enjoy the weekend!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

International Consolidated Airlines SA (LON:IAG) (£17.7bn | SR81) | Revenue up 1.9%, with operating profit up 77.3% to €351m, “reflecting strong demand”. Currently see “no issues with fuel availability” but higher prices “will inevitably lead to lower profit this year than we originally anticipated”. | BLACK? (no updated forecasts available to us today) | |

Airtel Africa (LON:AAF) (£13.3bn | SR91) | Revenue up 29.5%, with after-tax profit up 147% to $813m. Adj EPS up 127.7% to 18.6c, in line. Leverage reduced from 2.3x to 1.8x. | AMBER/GREEN = (Roland) This looks like a very strong set of results to me, with double-digit profit growth in all regions. More importantly, there’s also strong operational growth, as Airtel reaps the rewards of being a leading operator in immature and rapidly growing markets. High quality metrics help justify the forward P/E of 20, but there’s no doubt the shares aren’t as cheap as they were a year ago. The CEO also warns that energy price inflation could put pressure on margins this year. I think significant long-term growth opportunities remain, but the valuation means the stock’s High Flyer styling is apt – any disappointment could prompt a de-rating. On balance, I'm going to leave my broadly positive view unchanged today. | |

Intertek (LON:ITRK) (£7.8bn | SR59) | Intertek has rejected the recent offer of £58 per share from EQT, concluding that it “significantly undervalues Intertek and its future prospects” and carries significant execution risk. The company also provides further details of its own ongoing Strategic Review, which is likely to result in a split. | TAKEOVER | |

Rightmove (LON:RMV) (£3.2bn | SR37) | Full-year guidance unchanged, with revenue growth of 8-10% and underlying EPS growth of “at least 5%” expected in 2026. Continue to see growth in ARPA and Core Membership. | GREEN = (Roland) Rightmove reiterates both its operational and financial guidance for this year. With the stock at 10-year lows and trading on a forward P/E of only 13, my view is that the risks to this business have been overstated and that there’s probably a buying opportunity here. | |

Greencoat Renewables (LON:GRP) (£746m | SR58) | NAV +0.5c to 99.5c per share. Q1 generation 10% below budget, but net cash generation was €45.5m, on budget and equivalent to 2.4x dividend cover. Q1 dividend of 1.70250c per share (€18.8m). | ||

Workspace (LON:WKP) (£674m | SR42) | Saba Capital ( | ||

VAALCO Energy (LON:EGY) (£471m | SR61) | Increasing full year 2026 production and sales NRI volumes by 8% and 12%, respectively at the midpoint, while maintaining 2026 capital budget guidance unchanged even with additional drilling in Egypt included. | ||

SRT Marine Systems (LON:SRT) (£242m | SR32) | Signed £5m one-year support contract for an existing SRT-MDA deployment with a longstanding customer. This is a renewal and expansion of a previous contract. No change to broker forecasts. | ||

Gulf Marine Services (LON:GMS) (£230m | SR73) | Revenue down 10%, EBITDA down 24% to $19.5m. Average day rates up 8% to $37k/d. Backlog of $660m on 31 March 26. The reintroduction of a dividend has been deferred until the geopolitical situation stabilises. Full-year guidance for 2026 EBITDA of $105m to $115m is unchanged. | AMBER = (Roland) I upgraded GMS to neutral earlier this week following an update on the company’s order book and its move into two new markets. Today’s quarterly results show the impact of suspended operations on four vessels in the Middle East and suggest to me that average quarterly EBITDA for the remainder of the year will need to rise by 50% relative to Q1 to allow GMS to meet unchanged guidance. I think there’s still some risk of a cut to guidance at some point, but recognise that some caution is priced on a forward P/E of 6. I’m happy to maintain my neutral view, reflecting the mix of risk and opportunity I can see here. | |

Henry Boot (LON:BOOT) (£227m | SR46) | CEO Tim Roberts will step down later this year. Edward Hutchinson, interim MD of Boot’s Stonebridge Homes division, will be appointed as Tim’s successor. | ||

Colefax (LON:CFX) (£64m | SR96) | Trading in the core Fabric Division has been ahead of expectations since late January due to strong demand in the US. Like-for-like sales for the three months to 30 April rose by 7%. Full-year pre-tax profit is expected to be not less than £10.5m. | AMBER/GREEN = (Roland) I estimate today’s upgrade may equate to a c.20% increase in pre-tax profit expectations for the year just ended. If I’m right, this leaves Colefax trading on a trailing P/E of 10. However, past comments from Chair David Green suggest to me that US consumer spending may be linked to the health of the US stock market, so could be somewhat unpredictable and cyclical. I don’t have access to any updated forecasts for FY27, either. To reflect the small, illiquid nature of this business and our limited visibility, I’m leaving Mark’s previous AMBER/GREEN view unchanged today. | |

Arrow Exploration (LON:AXL) (£59m | SR63) | The Mateguafa HZ12 well (M-HZ12) has been completed on time and on budget, reaching a total measured depth of 13,824 feet. It’s currently on production at 564 bopd (282 bopd net) with a 60% water cut. | ||

Petra Diamonds (LON:PDL) (£57m | SR30) | Revenue up 39% to $68m, supported by the sale of the 41.82 carat Type IIb blue diamond. Pricing remains under pressure and net debt increased to $298m (31 Dec 25: $284m). Performance at Cullinan was affected by power interruptions and the impact of adverse weather. | ||

Tan Delta Systems (LON:TAND) (£23m | SR17) | Received c.£395k order for real time oil analysis sensor systems from a “world leading” manufacturer of large commercial and industrial engines. | ||

Earnz (LON:EARN) (£11m | SR9) | £5m, 2-year contract from Fortem, on behalf of Sanctuary Housing. Will include retrofit insulation, ventilation upgrades and renewable energy solutions. Potential 12-18 month extension. |

Roland's Section

Colefax (LON:CFX)

Up 9% at 1,345p (£70m) - Full Year Trading Update - Roland - AMBER/GREEN =

Mark flagged up a potential opportunity in this upmarket home decor firm in September last year. This has proved to be a good call; Colefax shares have been on a tear since then.

In today’s update, the company has upgraded its profit guidance for the year ended 30 April 2026 – the second such upgrade this year:

The RNS itself is extremely short, so I will reproduce it in full here:

Since we announced our interim results on 28 January 2026 trading in the Group's core Fabric Division has been ahead of expectations, following strong trading in the US, with like for like sales for the three months to 30 April 2026 up by 7.0% against a strong prior year comparative. As a result, the Group expects profit before tax for the year ended 30 April 2026 to be not less than £10.5 million.

Strong trading was already an established trend from H1 – January’s interim results disclosed an 18% increase in US sales during the first half of the year, or c.13% excluding tariff surcharges.

Tariffs were originally seen as a significant risk to sales growth in the US, but this fear faded as 2025 passed. Chairman (and 17.6% shareholder) David Green also made an interesting observation about the spending patterns of the company’s customers in January – is Colefax another beneficiary of the AI boom?

We believe that US trading is benefitting from the very strong US stock market. Sales in November, December and January have continued to perform well and unless there is a significant stock market correction, we expect this trend to continue through to the end of the financial year. As a result, the Group's profits for the year ended 30 April 2026 are expected to be ahead of current market forecasts. [January 2026]

Updated FY26 guidance (y/e 30 April 26): Colefax now expects to report FY26 pre-tax profit of at least £10.5m.

How does this compare to previous forecasts? Unfortunately, I don’t have access to any broker coverage for Colefax.

However, we can see from the StockReport that January’s upgrade led to a significant increase in broker earnings forecasts to 106.4p (previously 76.7p):

Full-year earnings were 108.4p in FY25 from a pre-tax profit of £8.9m, so it seems fair to suggest that previous expectations for FY26 pre-tax profit were similar, perhaps slightly lower than £8.9m.

On that basis, today’s upgrade represents an increase of c.20%.

I estimate that this could be equivalent to earnings per share of c.130p, using the H1 average share count as a guide.

Roland’s view

Spending by Colefax customers clearly has a cyclical element that’s not always easy to predict. If stock markets slow next year, will spending slump?

Current forecasts show earnings falling next year, although it’s hard for us to know whether this outlook remains the most likely scenario.

However, while earnings may fall short next year, it’s worth remembering that Colefax has a very strong balance sheet, with net cash of £22m reported at the end of October (excluding leases) – nearly one-third of today’s £70m market cap.

Based on my 130p FY26 EPS estimate, Colefax is trading on a trailing P/E of around 10, but this falls to a P/E of 7 on a cash-adjusted basis.

I’m going to resist turning fully positive on Colefax because this is a small, illiquid and somewhat quirky business where we have limited forward visibility. But I am very comfortable maintaining Mark’s previous AMBER/GREEN view today.

Airtel Africa (LON:AAF)

Up 0.4% at 366p (£13.3bn) - Final Results - Roland - AMBER/GREEN =

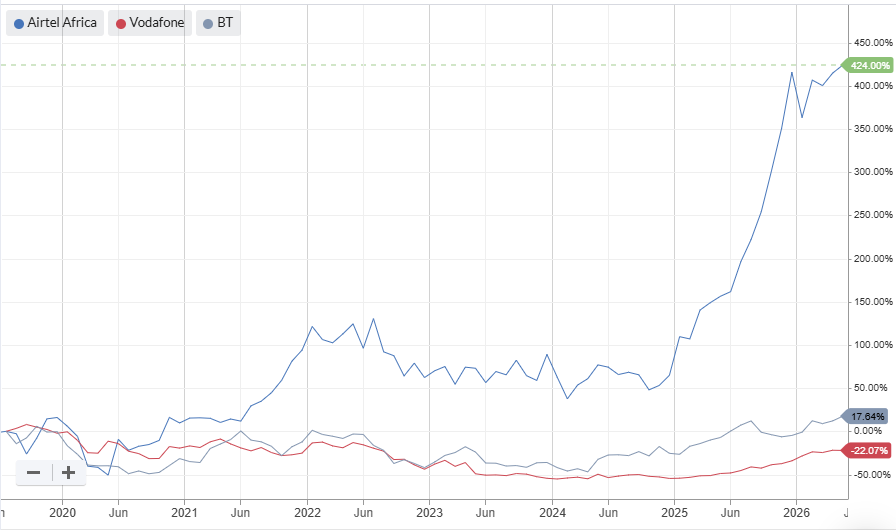

Airtel Africa’s multi-bagging performance since its IPO is perhaps a reminder of the opportunities available when investing in growth markets unencumbered by legacy assets and high levels of regulation.

This Africa-focus network operator and mobile money provider has outperformed BT and Vodafone by a country mile since its flotation in June 2019:

Today’s full-year results cover the year ended 31 March 2026 and show another period of very strong growth for this business, which operates in 14 countries in sub-Saharan Africa.

FY26 results summary

Here are the main financial headlines from today’s results:

Revenue up 29.5% to $6,415m (+24% at constant currency)

Pre-tax profit up 114.5% to $1,419m

Adjusted EPS up 127.7% to 18.6c

Full-year dividend up 9.2% to 7.1 cents per share

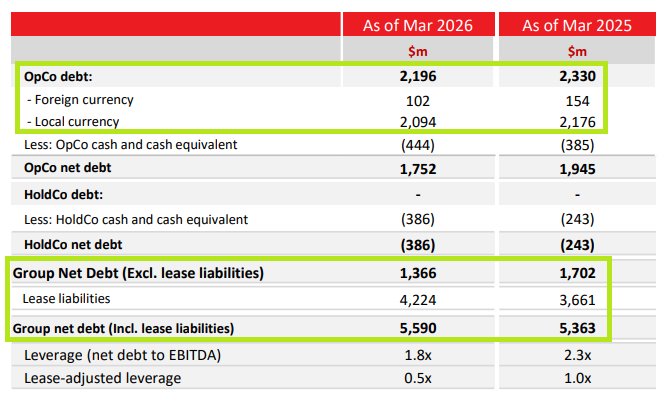

Net debt up 4.2% to $5,590m

Net debt to EBITDA leverage down 1.8x (FY25: 2.3x)

This improved result was driven by strong operational growth:

Average Revenue Per User (ARPU) up 17.8% to $3.1 per month (+12.8% at constant currency)

Total customers up 10.5% to 183.5m

Data customers up 14.8% to 84.2m

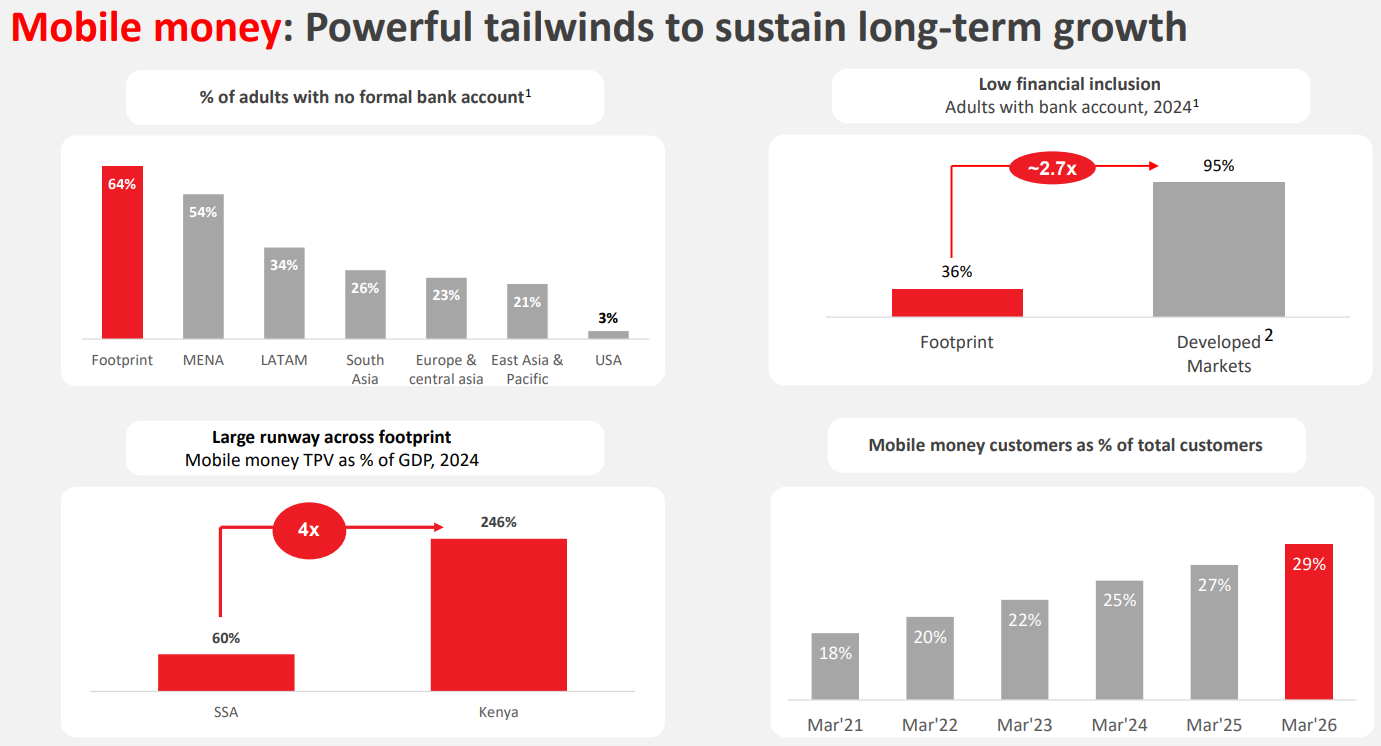

Mobile money customers up 21.3% to 54.1m

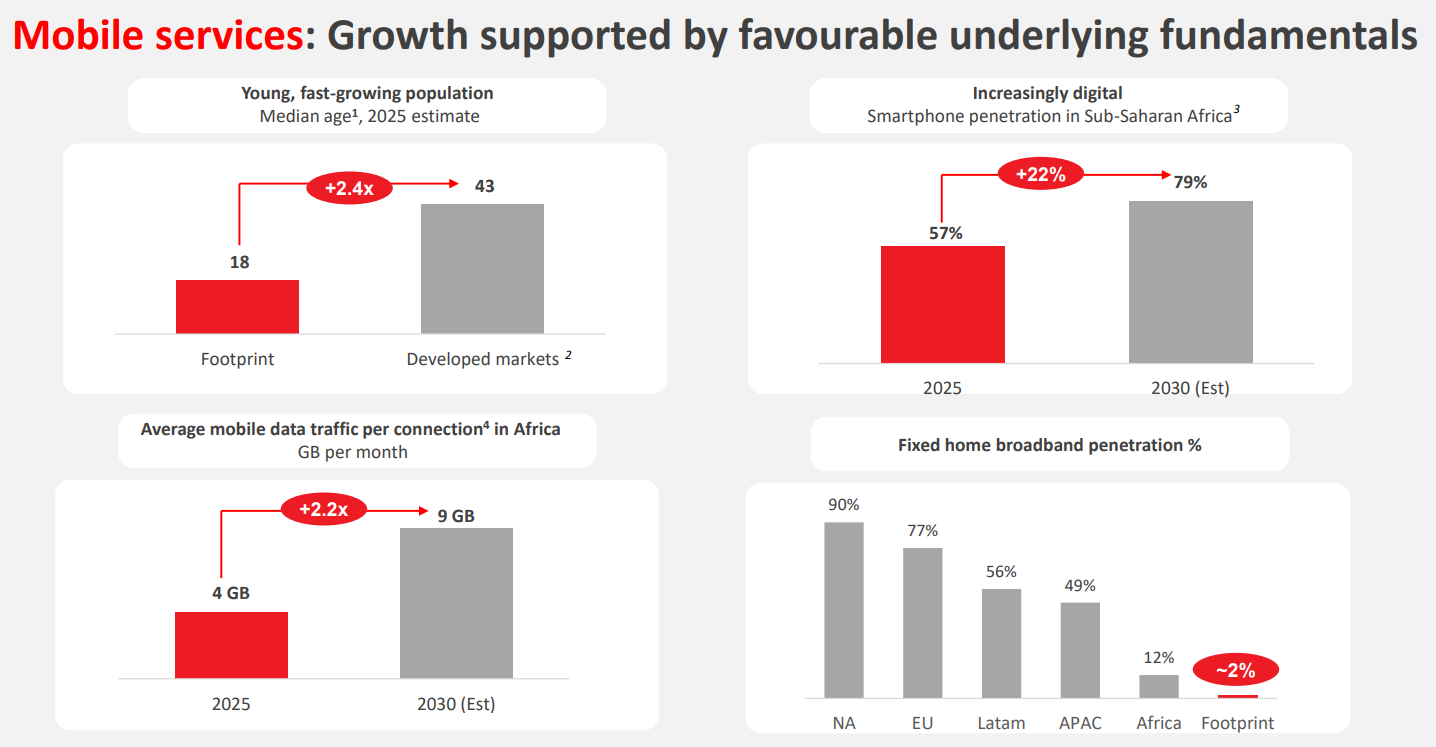

To give an idea of the relative immaturity of Airtel’s markets, smartphone penetration rose by 4.7% to 49.5% last year, with average data usage per customer increasing to 8.9GB per month.

Compare that to western markets. Smartphone penetration is around 96% in the UK and operators such as Vodafone and EE must rely on poaching customers from rivals to gain market share.

While I’ve seen estimates that average mobile data consumption in the UK is typically 12-15GB per month, this is in addition to far higher levels of home broadband data usage.

In many African markets, fixed line infrastructure doesn’t exist and mobile provides users’ sole internet connection – clearly data consumption could rise significantly over time.

Despite the differences in GDP and spending power between western markets and Africa, I think it’s reasonable to believe Airtel still has big opportunities to benefit from new customer adoption of its services and growing smartphone usage.

The group’s Mobile Money business also benefits from similarly attractive market fundamentals in markets where much of the population has no access to banking facilities. This unit is being prepared for an IPO, potentially in the second half of this year:

Trading commentary: Airtel’s business is spread across a number of large markets with varying fundamentals. All of these saw strong growth last year:

Nigeria: customer numbers rose by 9.4% to 58.3m, with revenue up 47.5% to $1,603m (this partly reflects inflationary price rises). Underlying EBITDA rose by 70.5% to $922m, 29% of the group total.

East Africa (Kenya, Rwanda, Uganda, Tanzania, Malawi & Zambia): customer numbers rose by 8.7% to 84.3m, supporting a 17.8% rise in revenue to $3,015m. Underlying EBITDA rose by 17.3% to $1,602m – around half the group total.

Francophone Africa (Niger, Chad, DRC, Congo, Gabon, Madagascar, Seychelles): customer numbers rose by 16.3% to 40.9m, supporting a 17% increase in revenue to $1,786m. This supported a 19.4% increase in underlying EBITDA to $786m, making this the lowest margin geographic grouping within Airtel’s business.

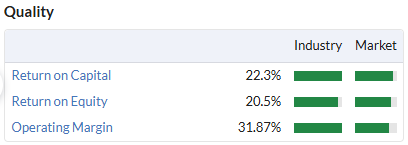

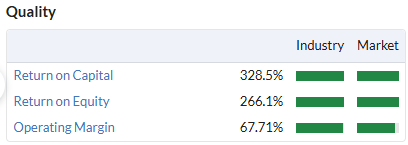

Profitability: Airtel Africa’s profitability has been consistently superior to the legacy UK operators since its IPO. The Quality snapshot on the StockReport highlights some very appealing numbers:

Crunching the numbers on today’s results suggests that this level of profitability was maintained last year:

Operating margin: 32.8%

Return on Capital Employed (ROCE): 23.6%

Balance sheet & Cash Flow: Airtel Africa’s debt position has evolved significantly over recent years. In short, the company has refinanced much of its debt from dollar-denominated group-level debt into local currency debt held by its operating subsidiaries. One benefit of this is that it has reduced the parent company's exposure to currency inflation – a big factor in some developed markets. Nigeria is the obvious example of this in the last couple of years.

Although reported net debt rose slightly last year, financial net debt fell. The increase in overall net debt reflects higher lease liabilities following contract renewals on some of the group’s mobile towers.

Overall reported leverage fell by 0.5x to 1.8x EBITDA last year due to the growth in profit. For a business of this kind, leverage of under 2x looks fairly comfortable to me, especially as cash generation remained good.

My sums suggest FY26 free cash flow of $1.1bn. This represents an excellent >100% conversion rate from reported net profit of $813m.

This level of cash generation also provides very comfortable cover for the $260m dividend.

Outlook

There’s no specific forward guidance in today’s results, but CEO Sunil Taldar does sound a note of caution relating to the impact of energy prices on margins:

The recent increase in energy costs arising from the ongoing geopolitical events will likely lead to increased cost inflation, resulting in EBITDA margin pressure in the near-term. However, with a strong growth outlook, and an enhanced focus on cost efficiencies, we will look to limit the overall impact on our business.

Capital expenditure is also expected to rise to $1.1bn in FY27. Lower margins and higher spending could see free cash flow come under pressure. However, given the high level of cash flow coverage for the payout, I don’t see this as a big risk to the dividend.

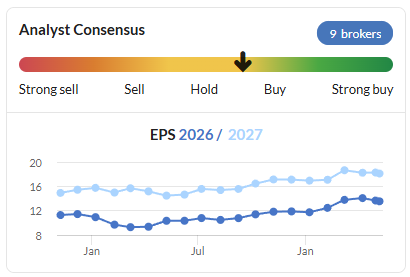

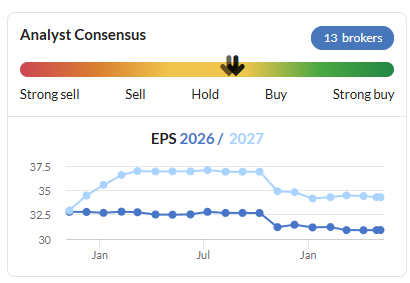

Consensus forecasts on Stockopedia ahead of today’s results suggested earnings could rise by a further 30%+ this year, to 24.5c per share:

Roland’s view

I think Airtel Africa is a good quality (if complex) business. The real question for me is over valuation, which has risen sharply over the last couple of years.

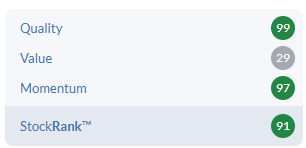

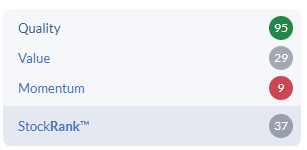

The StockRanks style the stock has a High Flyer with very strong Quality and Momentum metrics, but much weaker value:

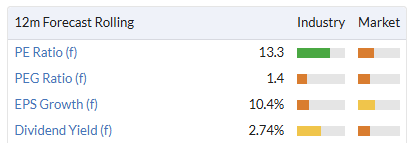

With a dividend yield of just 1.4% and a forward P/E of 20, I think the valuation does carry some downside risk as well as opportunity. In my view, the High Flyer styling is very apt here.

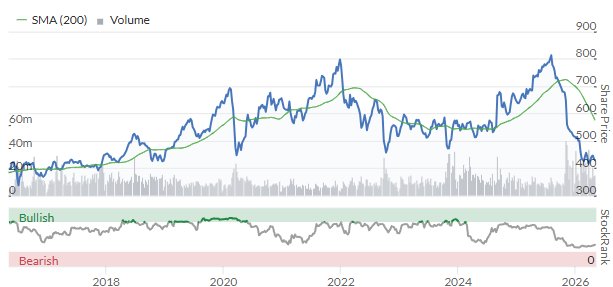

Airtel’s share price has risen by 35% since I last covered the stock in October 2025. At that time I took an AMBER/GREEN view.

Although it seems inflationary pressures could affect near-term margins, I think the strong progress and continued growth outlook justify leaving my broadly positive view unchanged today.

Gulf Marine Services (LON:GMS)

Up 0.2% at 20p (£230m) - 1st Quarter Results - Roland - AMBER =

I upgraded GMS to neutral earlier this week following an update on the company’s order book and its move into two new markets.

Today’s quarterly update provides further positive news, with crews apparently returning to the four vessels in Qatar that were evacuated at the start of the Middle East conflict. However, there’s not yet any confirmation on when these vessels will return to operations and start generating revenue again.

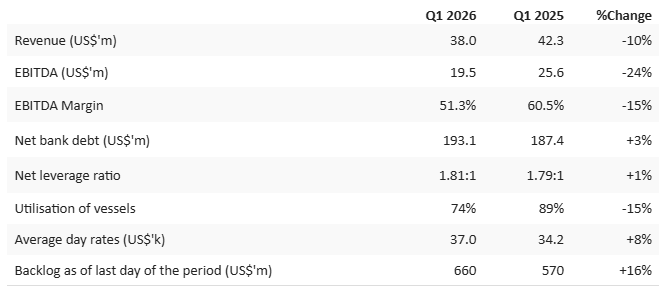

In the meantime, the Q1 results show the impact of these offline vessels, with utilisation down to 74% and EBITDA down by 24% versus the same period last year:

Source: GMS 1st Quarter 2026 results

Outlook: management’s decision to leave 2026 EBITDA guidance unchanged at $105m to $115m implies a material improvement in performance over the remainder of the year. I estimate that to meet the mid-point of guidance, quarterly EBITDA will need to average $30m, 50% higher than in Q1.

I believe recent contract wins and the improved order book could support this result, if a peace deal is achieved in the Gulf. But I do think there’s still some risk of another profit warning later this year.

Some caution is already priced on a P/E of 6. I’m happy to maintain my neutral view, reflecting the mix of risk and opportunity I can see here.

Rightmove (LON:RMV)

Down 0.4% at 427p (£3.2bn) - Trading Statement - Roland - GREEN =

Today’s trading update covers four months to 30 April and leaves 2026 guidance unchanged. Investors appear unmoved too, with the shares trading largely unchanged this morning.

The update itself is slightly unusual - there is very little specific trading information. Instead, Rightmove leads by reiterating its guidance and then providing an update on key initiatives, strategy and property market conditions.

Here are some of the main points, together with my conclusions.

Current trading and outlook

Management confirm that expectations for the core business and strategic growth areas are unchanged:

The core business (estate agents and new homes) continues to deliver “product-led Average Revenue per Advertiser” growth.

Core Membership has increased since the year end and supports expectations for full-year growth of c.1%.

Strategic Growth Areas of Commercial Property, Mortgages and Rental Services are on track to deliver 20% to 30% revenue growth this year.

2026 financial guidance is also unchanged from the 2025 results:

2026 revenue growth of 8% to 10%;

2026 underlying operating profit growth of 3% to 5%;

2026 underlying EPS growth of “at least 5%”.

As previously reported, growth in the second half of the year is expected to be stronger due to the timings of new home developments and a tough comparator for mortgage activity versus last year.

Given the recent mixed news and poor sentiment from listed housebuilders, there could be some risk of an H2 downgrade if new home volumes ease. But I don't see this as a major concern.

Strategy & Initiatives

The company reiterates that 80% of time spent on UK property portals is spent on Rightmove, with over 85% of traffic “organic and direct”. This is hugely valuable; it tells us that most users go directly to Rightmove’s website and app, without relying on search activity or AI prompts.

The company confirms that just 0.5% of its traffic comes from AI services.

To maintain brand awareness, Rightmove is launching a new advertising campaign today that’s expected to reach 90% of target UK adults by the end of the year.

Investment in technology and new tools continues in the background, with a view to gaining a footprint in AI chat and providing new tools in areas such as online valuations, new home sales, rental leads and mortgage quotes.

Current property market trends

House price growth is said to remain positive, while listing volumes are said to be at an eleven-year high.

However, checking the latest Rightmove House Price Index report suggests to me that this situation is more marginal:

Asking prices rose by 0.8% month-on-month in April, but are down by 0.9% year-on-year;

Buyer demand in April (as of 20 April) was 7% lower than the same period in 2025. So perhaps the high level of listings reflects a growing burden of unsold property, with buyers and sellers failing to agree on price?

The company also notes that mortgage rates have risen this year, with the average two and five-year fixed rates both currently at 5.1%, compared to 4.3% and 4.4% respectively on 31 December 2025.

Roland’s view

Graham covered Rightmove’s 2025 results in some detail in February. I don’t think that much has changed since then.

The business remains a clear market leader, with fantastic profitability and strong fundamentals.

The shares are also trading more cheaply than I can ever remember seeing:

However, Stockopedia’s Falling Star styling suggests some caution may be warranted, flagging up extremely low momentum:

We should also remember that the company did issue a profit warning last year, albeit only a small one:

Logically, I think there are only two real possibilities here:

Rightmove’s business model is about to be disrupted, either by competition (e.g. here) or by technological change such as AI. In this scenario, the current valuation might be fair.

OR:

The business will retain most of its current advantages, even if it's forced to become more competitive on price. In this scenario, I can only conclude that Rightmove shares look too cheap at the moment and could be a logical candidate for a top up or a new purchase.

I can’t be certain that Rightmove isn’t about to be disrupted. But my feeling is that it’s unlikely to lose its overall lead – or its front-of-mind position for UK home hunters.

I don’t think ChatGPT and similar will result in a loss of market either. Properties need to be listed somewhere and Rightmove offers many value-added services that won’t be available through an AI service that’s simply scraping other listing websites.

With the shares trading at 10-year lows, I think it’s logical to be positive here, so I’m leaving Graham’s GREEN view unchanged.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.