Good morning!

It’s been a busy week and yet it feels like little has changed. The Middle East conflict remains unresolved and speculation around the Prime Minister’s future continues.

The groundwork for change may have been laid, though.

China’s Xi Jinping is said to have stressed the importance of reopening the Strait of Hormuz and achieving a peaceful settlement with Iran in his meetings with Trump.

At home, Manchester Mayor Andy Burnham has secured a seat he can contest in a by-election with the aim of returning to Westminster as an MP and launching a leadership challenge.

Financial markets are said to see Burnham as a riskier proposition than Starmer in terms of financial discipline. The pound fell sharply against the dollar last night when the news was announced and gilt yields are expected to rise today (which means bond prices will fall).

In markets, last night saw another storied UK plc go onto the chopping block when ingredients specialist Tate & Lyle (LON:TATE) reported a £2.7bn (up to 615p per share) takeover offer from US rival Ingredion (NYQ:INGR) .

Tate shares have been unloved since a profit warning last year and this looks a little opportunistic to me. But Tate & Lyles's performance (and profitability) has been humdrum for some time and the combination is said to offer attractive economies of scale.

Let’s see what markets have in store today – futures suggest a subdued opening for major indices:

FTSE 100 expected to open down 0.8%

S&P 500 expected to open down 0.6%

Nasdaq 100 expected to open down 1.0%

German DAX expected to open down 1.5%

Brent Crude is up at $107 a barrel

Gold is down at $4,568/oz

That's all for today - have a great weekend!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Centrica (LON:CNA) (£9.3bn | SR58) | British Gas has agreed to pay £20m to Ofgem’s Voluntary Redress Fund following Ofgem’s investigation into legacy prepayment meter practices between Feb ‘18 and Feb ‘23. The company will now undertake a comprehensive review of customer records for the relevant period, provide redress where possible and write off up to £70m in energy debt for vulnerable customers. | AMBER = (Roland) [no section below] British Gas (i.e. Centrica) will pay up to £90m to resolve a regulatory investigation into the way that pre-pay meters were force-fitted by debt collectors in the homes of customers who fell behind with their bills – often including vulnerable customers. The amount is equivalent to more than 10% of last year’s adjusted operating profit of £814m. It’s a poor look for British Gas, but CEO Chris O’Shea assures us that necessary changes have now been made and these problems are in the past. From an investment perspective I think the impact will be small, but as I commented in February, earnings forecasts are drifting lower this year and Centrica’s share price looks up with events to me. I’m staying neutral today. | |

Unite (LON:UTG) (£2.5bn | SR45) | Reservations remain in line with our expectations for the 2026/27 academic year, with 79% of beds let for 26/27 (FY26: 80%). FY26 adj EPS guidance 41.5-43.0p, in line with consensus. | ||

Grafton (LON:GFTU) (£1.57bn | SR93) | Average daily LFL sales were “broadly flat” in the first four months of the year. FY26 adj operating profit expected to be £190-200m, in line with consensus of £190.8m. Acquisitions in Spain and Ireland are expected to offset weakness in the UK. | AMBER (Roland) Unlike some UK building supply chains, Grafton operates in a number of European markets. This seems to be helping to smooth the group’s performance, with stronger results in some countries offsetting weaker performances elsewhere (especially in the UK). It looks like recent acquisitions are expected to support in line FY26 results, although without these I suspect today’s update might have been a profit warning. On balance I don’t see too much to dislike here, but returns have been unexciting over the last decade and my feeling is that the valuation is probably about right, hence my neutral view. | |

Glenveagh Properties (LON:GLV) (£1.00bn | SR94) | Closed and forward order book of €1.5bn, up from €1.3bn on 10 March, providing strong visibility for the remainder of the year and into 2027. Full-year EPS guidance of €0.21 reiterated, buyback programme increased by €25m to €50m. | ||

Frp Advisory (LON:FRP) (£293m | SR62) | Expect FY26 revenue +16% to >£176m, with adj EBITDA +9% to >£45m, in line with market consensus. Confident of further progress in FY27, notes increase in demand for debt advisory and restructuring services due to impact of Middle East conflict. | AMBER/GREEN = (Roland) FRP’s shares have eased recently and look potentially good value to me, on a forward P/E of 9.5. While end market conditions are somewhat mixed, FRP’s broad offering means it should be able to continue growing. However, such growth may not be that exciting unless it’s boosted by further acquisitions. The latest estimates from house broker Cavendish suggest earnings growth will fall to 4% this year, from 9% for the year just ended. There are also few signs of earnings momentum, with estimates having been largely unchanged for over a year. Despite attractive profitability, I’m going to maintain our practice of being cautious when it comes to valuing professional services businesses and leave our view unchanged today. | |

TT electronics (LON:TTG) (£211m | SR48) | Year-to-date organic revenue -4.8%, reflecting softer EMS end-market demand. Book-to-bill was 107%, underpinned by Aerospace and Defence. Full-year profit guidance remains unchanged. | ||

LSL Property Services (LON:LSL) (£206m | SR49) | A positive start to the year, building on momentum from 2025. Despite a backdrop of uncertainty, “UK housing transactions continue to remain stable”, although pull-forward of refinancing seen in March/April has now moderated. Expect 2026 profits to be in line with expectations - no change to broker forecasts from Shore Capital. | AMBER/GREEN = (Roland) [no section below] This property services company provides products used by mortgage intermediaries and estate agents. Management says the growing regulation of the rental and home buying markets are playing to its strengths – LSL’s focus on data and technology supports standardisation and compliance, for example. Trading is said to be in line and slightly to my surprise, the company says that UK housing transactions remain stable, albeit softer in London (where LSL has limited exposure). We last covered this stock in 2024, since when the shares have fallen by around 25% to trade on just 7x forecast earnings. The macro backdrop obviously remains a concern and I think it’s worth remembering that forecasts were cut earlier this year. Even so, I think the stock's sell-off could prove to be a little harsh, given the net cash balance sheet and 5%+ dividend yield. I’m comfortable maintaining our previous AMBER/GREEN view today. | |

Sintana Energy (LON:SEI) (£140m | SR33) | Galp Energia announced 57% upgrade to 3C contingent resources at Mopane to 1.38 bn boe gross. Progressing new exploration activity. Reached $9m settlement with ExxonMobil, with $3m received and $6m expected before y/e 2026. Cash of $8.2m at period end. | ||

Volvere (LON:VLE) (£58m | SR97) | Revenue up 7.5% to £52.7m, pre-tax profit up 6.5% to £6.75m. Net assets per share up 15.1% to £19.80. Net cash and current investments up 19.3% to £33m. Shire Foods’ 2026 margin to be impacted by cost inflation and reduced volumes vs 2025. | AMBER/GREEN = (Roland) This is a solid set of results with few surprises following March’s comprehensive year-end update. Perhaps the main piece of news is that Shire Foods’ profits are likely to fall this year, due to a combination of cost headwinds and lower volumes. I don’t see this as a big concern in the context and my number crunching suggests Volvere shares continue to trade below a reasonable estimate of fair value. However, the lack of any other investments or tangible shareholder returns mean that I think Graham’s previous moderately positive view remains the most appropriate choice. | |

Logistics Development (LON:LDG) (£58m | SR70) | Underlying pre-tax profit -24.2% to £15.0m. As at 31 December 2025 LDG's unaudited estimated NAV per share was 26.7 pence. | ||

Kendrick Resources (LON:KEN) (£28m | SR18) | New 112m diamond drill hole at TK2 returned a weighted mean 3.03 wt% TREO, including more than 17m above 4.0 wt% from pXRF analysis. Surface sampling across TK1 to TK7 confirms strong average TREO grade of 3.12 wt% from 295 samples | ||

Prospex Energy (LON:PXEN) (£14m | SR21) | Revenue up 18.6% to £912k from Selva Malvezzi, closed Q1 with £907k of cash following CLN issuance during quarter. New CEO appointed. | ||

DSW Capital (LON:DSW) (£11m | SR64) | FY26 network revenue to be -11.6% at £22.8m, in line with expectations. Subdued M&A activity. FY26 adj EBITDA to be in line with revised expectations at c.£1.6m, with adj pre-tax profit of c.£1.4m. |

Roland's Section

Frp Advisory (LON:FRP)

Up 0.7% at 114p (£295m) - Full Year Trading Update - Roland - AMBER/GREEN =

We’ve been moderately positive on this business advisory group in past coverage, most recently in November.

FRP’s financial year ended on 30 April and today’s update covers the final four months of the year and confirms that full-year results should be “at least in line with market consensus”:

The Group expects to report FY 2026 revenues of at least £176m which is up 16% on the prior year (FY 2025: £152.2m), and adjusted underlying EBITDA of at least £45m, up 9% on the prior year (FY 2025: £41.3m).

Checking with the latest note from house broker Cavendish suggests that today’s guidance is slightly ahead on revenue, but in line on profits

FY26E revenue: £176m (prev. £164m)

FY26E adj EBITDA: £45m (unch)

FY26E adj pre-tax profit: £4.02m (unch)

FY26E adj EPS: 11.7p (unch)

What this tells me is that margins have been slightly lower than expected this year, but price rises and/or greater volumes have offset the impact of this to leave profit expectations unchanged.

Trading performance: management commentary suggests to me that FRP’s business has performed fairly well in mixed conditions over the last year.

Restructuring: FRP “strengthened its market-leading position” as the top UK firm for administration appointments by volume. Notable wins included involvement in the Market Financial Solutions (MFS) group and Denby's Pottery.

Corporate Finance: a record revenue year, despite “challenging M&A markets where deals have taken longer to complete”. FRP’s mainly UK offering is focused in the lower mid-market, with half deals involving private equity, “a resilient and well-capitalised segment”.

Financial Advisory & Forensic: demand is described as “steady to buoyant”, particularly in financial due diligence and valuations.

Growth: a number of acquisitions were completed during the year and the group also continued to hire, with total headcount increasing by 12% to 894 last year.

It’s also worth remembering that corporate undertakers such as FRP can sometimes benefit when other types of business are suffering (my emphasis):

FY 2026 ended with the Middle East conflict impacting energy costs and beginning to affect supply chains. This is expected to add upward pressure on headline inflation and complicate central bank rate-cut paths, and the Group has already seen an increase in demand for Debt Advisory services and Restructuring Advisory services.

Balance sheet & dividend: this founder-led business has maintained a net cash position since its flotation and this continues. The company reports net cash of c.£26m at the end of April (FY25: £33.3m) and confirms its credit facility remained undrawn despite last year’s acquisitions. For me, that’s a likely sign the company’s acquisitions are creating value and positive cash flow.

In line with normal policy the company expects to declare a final dividend – Cavendish is forecasting a total payout of 5.6p per share this year, implying a final dividend of 4.6p. That gives a dividend yield of 4.9% at current levels.

Outlook & Estimates

FRP's diverse offering across the economic lifecycle of its clients ensures that the Board looks ahead to FY 2027 and beyond with strong current momentum and confidence.

Cavendish has also provided updated FY27 estimates today – our thanks for making these available.

As with the FY26 numbers, revenue estimates have been nudged higher but profit expectations are unchanged:

FY27E revenue: £180m (prev. £176m)

FY27E adj EPS: 12.2p (unch)

These estimates put FRP on a forward P/E of 10 at current levels – not too demanding.

Roland’s view

I don’t see any reason for shareholders to be unhappy about today’s update. While today’s revenue and adjusted EBITDA figures don’t give us a full picture of ‘real’ profitability or free cash flow, past performance has shown good cash conversion and attractive profitability:

The valuation looks modest here following recent share price falls:

However, it’s worth noting that today’s estimates from Cavendish suggest earnings growth will fall to c.4% in FY27, compared to 9% for the year just ended. These calculations may be revised if FRP makes further acquisitions in the current year, but right now, the outlook for organic growth seems fairly muted.

I also share Graham’s caution about overpaying for professional services businesses of this kind, especially as there have been no meaningful upgrades to forecasts for over a year. FRP does not seem to be outperforming expectations, removing one possible catalyst for a share price re-rating:

In my view, this makes the StockRanks Contrarian styling an appropriate choice here. I’m going to leave our moderately-positive view unchanged today, but for investors with an interest in this sector I think FRP could be worth a closer look. AMBER/GREEN.

Volvere (LON:VLE)

Down 4.5% at 2,530p (£55m) - Final Results - Roland - AMBER/GREEN =

This unusual investment company has been a standout success for patient long-term investors who rode out the period of pandemic uncertainty:

The stock has 12-bagged over the last 20 years and has risen by 75% over the last five years.

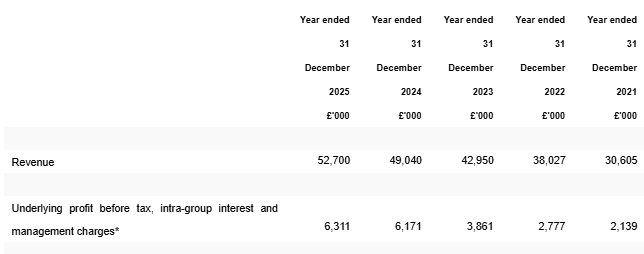

The headline financial figures in today’s results were included in March’s full-year trading update, but here’s the full set of numbers:

Revenue from continuing operations up 7.5% to £52.70m

Pre-tax profit from continuing operations up 6.5% to £6.75m

Earnings per share up 6.4% to 188.89p

Consolidated net assets up 15.1% to £19.80 per share (£47.2m)

Net cash up 12.8% to £28.3m

Volvere is technically an investment company, but it currently only has one investment, Shire Foods – “a renowned pie manufacturer” that’s a major supplier to UK discount supermarkets and foodservice groups.

In the absence – once again – of any new investments, it’s Shire Foods’ performance that’s of most interest to investors. Conditions appear to have been mixed over the last year, with adverse macro conditions:

As shareholders already know, in 2026 we have been seeing headwinds on a number of fronts - increased labour costs (driven principally by the above-inflation national minimum wage increase), raw material and distribution costs. The impact of higher oil prices will undoubtedly continue to impact us directly and indirectly. We do, of course, seek to mitigate these factors where we can but there can be a lag in increasing our selling prices, along with a reluctance to accept the full impact by our customers, who themselves are under similar pressures.

There have also been changes to demand from one large customer that have led to lower volumes and affected profitability:

In the first half of 2025 we had relatively high volumes of "value" products for one of our larger customers. Whilst incrementally productive for us, the lower yield for our customer (due to selling at low prices) has resulted in them scaling back those lines, impacting profitability in 2026 when compared to the comparative period in 2025. Shareholders will recall that the second half of the year is traditionally the stronger in terms of sales (due to the colder months).

As a result of these factors, it seems that Shire Foods’ profitability will be lower in 2026 than in 2025. This could break an impressive run of growth for the business, as this five-year summary highlights:

Source: Volvere FY25 results

Shire Dividend: Shire paid a dividend of £5m last year, of which £4m was paid to Volvere and £1m to minority shareholders in Shire.

Volvere says it has now received a total of £6.4m in dividends since its original investment. As a reminder, the company paid £0.54m for an 80% stake in Shire Foods in 2011. So even without selling Shire, this investment has already delivered a 1,000% return for Volvere, or around 18% annualised.

That’s an impressive result that gives credibility to the company’s strategy of patiently pursuing opportunities to invest in “undervalued and/or distressed businesses”.

Acquisitions and future strategy: unfortunately another year passed in 2025 without Volvere’s founding director Nick Lander being able to find any more of these undervalued opportunities.

We have considered a number of investment opportunities in the last 12 months, both in the food sector and in other sectors. For a variety of reasons, those discussions did not come to fruition. As shareholders know, if we cannot determine the right balance between risk and reward for an investment, we will not invest because our prospect of achieving attractive returns diminishes. It can be hard to walk away, especially when time has been invested in a potential transaction, but we take seriously our responsibility for protecting shareholder value.

On balance, I think more company leaders should probably exert this kind of discipline on their acquisition decisions.

Lander says the current macroeconomic picture could be “helpful in terms of the flow of new opportunities”. But he cautions that this situation also means that the subsequent performance of any new investment could be hampered by the macro environment. This makes it important to maintain a strong cash position in order to support any follow-on investment needed.

While this suggests no change to Volvere's policy on shareholder returns, today's commentary does include an intriguing comment suggesting the capital structure of the group might change:

We are, however, exploring ways to unlock further capital with targeted use of leverage.

Shareholder returns: Volvere doesn’t pay dividends but will continue to buy back its own shares “when it considers it of value to do so”.

Volvere repurchased 19,000 shares for a total cost of £428k last year, implying an average of £22.53 per share.

Valuation: these buybacks suggest management sees value in buying back shares at a premium to book value.

This is probably quite reasonable, as Graham has previously explained. Given the large cash balance and single investment, it makes more sense to value Volvere based on its share of Shire’s earnings than on its net assets alone:

Stripping out cash and available-for-sale investments from the market cap suggests to me that Volvere’s 80% stake in Shire Foods is currently valued at £22m.

I estimate Volvere’s share of Shire’s post-tax profit last year was c.£3.8m

That’s equivalent to a P/E of 5.8, which seems cheap to me, even for this sector.

Applying a (still conservative) P/E of 8 to Shire’s earnings gives me an estimated fair value for Volvere of c.£63.4m, or around 2,890p per share.

On the basis of this quick estimate, I would agree that share buybacks at c.£22 probably did create value for shareholders.

Outlook

Volvere doesn’t have any broker coverage or provide financial guidance. But we do get this comment from Nick Lander:

For now, our primary focus is to ensure Shire's performance is as robust as circumstances will allow. Whilst the first half of the year is proving to be challenging, we remain confident in the company's long term potential.

As commented earlier, it looks like Shire profits may fall slightly in 2026. I suspect this will be a common trend across companies in this sector and don’t see it as a major concern given the macroeconomic context – see comments from restructuring specialist FRP above!

Roland’s view

I would personally like to see Volvere pay a modest dividend to shareholders from its growing surplus cash pile. One possible strategy might be to pass on the interest from the group’s cash pile. This totalled almost £1.1m last year – equivalent to a 2% dividend yield.

Despite this niggle, I think the company’s track record does suggest it is a responsible and successful steward of shareholder capital.

Based on my quick valuation estimate, I think it’s fair to suggest Volvere shares still offer some value. However, the uncertainty over the timing of any future investments means I am reluctant to be fully positive at the current price.

Graham was AMBER/GREEN on this stock (which he knows very well) in November and I cannot see any reason to change that view today.

Grafton (LON:GFTU)

Down 3.4% at 804p (£1.52bn) - Trading Update - Roland - AMBER

Grafton is an Ireland-based builders merchant group with operations in the Island of Ireland, the UK, Iberia and Northern Europe. In the UK, it trades under brands including Selco, Leyland SDM and T.G. Lynes.

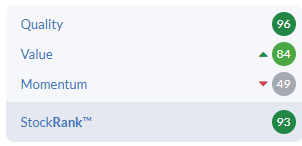

Checking back through the archives, this isn’t a stock we’ve previously covered in any depth, so let’s start with a look at some key elements from the StockReport.

A StockRank of 93 is currently styled as Neutral but looks close to Contrarian to be, with decent value and quality scores:

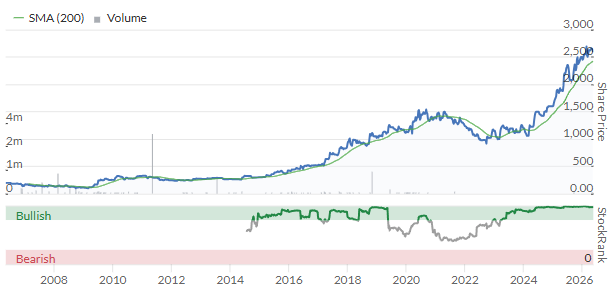

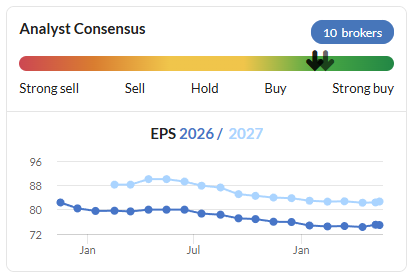

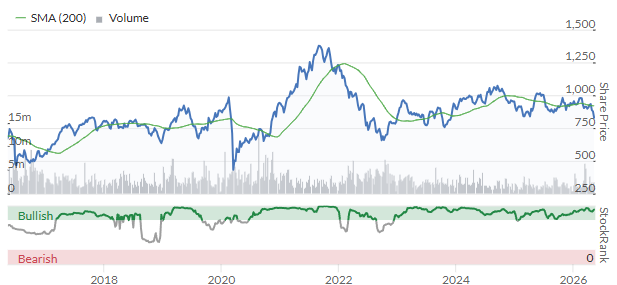

Recent share price action has been weak, presumably reflecting the macro outlook in at least some of Grafton’s markets:

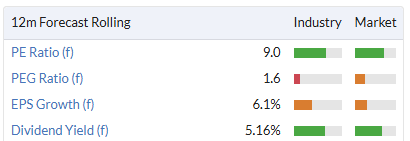

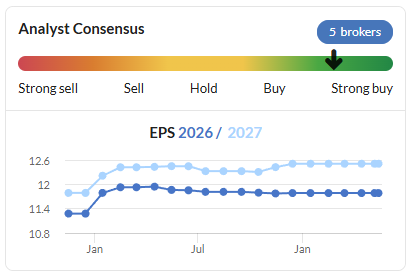

Broker earnings estimates have also been drifting lower, but not alarmingly so:

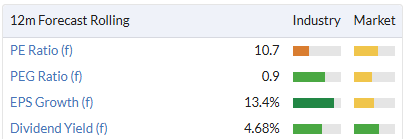

A cautious outlook is also reflected in an undemanding valuation, with a potentially useful 4.7% dividend yield:

With that quick background check, let’s take a look at today’s trading update.

AGM Trading Update (Jan-April 2026)

Here in the UK we are accustomed to gloomy news on housebuilding and are conditioned to see the whole construction market in this way. That’s not necessarily the correct lens to apply to Grafton though, which is continuing to benefit from a very strong housing market in its home market of Ireland.

Acquisitions are also boosting growth in stronger-performing markets. Today’s commentary highlights some of these trends:

Group revenue rose by 3.2% to £830m (+1% constant currency), including contributions from various acquisitions.

Average daily like-for-like sales were broadly flat in the first four months as growth in Iberia (+5%), the Island of Ireland (+1.8%) and Northern Europe (+1.6%) offset weak markets in Great Britain (-5%).

Acquisitions closed in two of Europe's fastest‑growing markets - Mercaluz (Spain) and Cygnum (Ireland).

No material supply chain disruption seen yet (as a result of the Middle East conflict) but “inflationary pressures evident”.

Outlook: full-year adjusted operating profit is expected to be £190-200m, with contributions from the Mercaluz and Cygnum acquisitions offsetting weaker trading in the UK.

Grafton provides a consensus estimate of £190.8m for adjusted operating profit, so today’s update seems to suggest that the full-year figure could be slightly above this with the benefit of recent acquisitions. Without these deals, my feeling is that today's update might have been a profit warning.

Checking back, both acquisitions seem sensible to me and are small enough to be considered as bolt-ons:

Mercaluz: Spanish air conditioning specialist with 2025 sales of €150m and adjusted operating profit of €22m. Acquired for up to €175m in March.

Cygnum: Irish timber frame home specialist with 2025 revenue of €45.6m and operating profit of €7.9m. The consideration wasn’t disclosed, but this looks a sensible bolt on with decent profitability and I don’t see an issue with this. Modular construction is said to be one of the fastest-growing building methods for new homes in Ireland.

Outlook

Grafton’s geographic diversity is expected to help mitigate the impact of some regional weakness:

Grafton's geographically diversified portfolio underpins its resilience, with over 75% of Group profits in 2025 generated outside Great Britain. Trading conditions remain supportive in the Island of Ireland and Iberia, while the timing of a material recovery in Finland and the Netherlands remains uncertain. In Great Britain, representing less than a quarter of Grafton's 2025 operating profit, the outlook has weakened, with independent commentators suggesting that total construction activity is now expected to contract in the current year.

As mentioned above, consensus estimates suggest an adjusted operating profit of £190.8m this year (FY25: £190.2m). I don't have access to any broker notes, but based on today’s commentary I would guess that consensus earnings forecasts will remain broadly unchanged.

Using the FY26 EPS estimate of 75p per share from the StockReport leaves Grafton trading on a forward P/E of 10.7.

Roland’s view

I don’t see anything much wrong with this business on this initial review. Grafton appears to have reasonable scale and to be active in some growing markets.

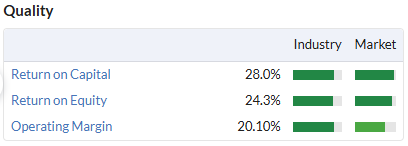

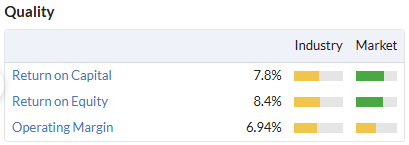

However, as might be expected in this sector, quality metrics are pretty average:

The near-term outlook is also a little uncertain and I think it’s fair to assume that profits would have fallen this year without the benefit of recent acquisitions.

Although Grafton has been listed a long time, its shares have only risen by 16% over the last 10 years despite the presumed benefit of a long-running housing bull market in the group’s home market.

While dividends have increased overall shareholder returns during that period, my instinct is that a P/E of 10-12 is about right for this business. Given the backdrop of macro uncertainty in some of Grafton’s markets, I’m inclined to open our coverage by taking a neutral view ahead of the company’s interim results later this year. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.