Good morning!

There has been no progress overnight when it comes to negotiations between Iran and the US, but it appears that other countries are losing patience with the situation. As a reminder, the (currently closed) Strait of Hormuz used to see one-fifth of the world’s oil supply passing through it.

India has a major interest in the situation, and has created plans to send ships through the Strait imminently, with the help of the Indian Navy. But it’s not clear yet if the US and Iranian forces blockading the Strait will let these plans succeed. I expect that fees may be payable to one or both sides.

In a similar vein, Bloomberg reports that some South Korean and Chinese tankers are now attempting to cross the Strait.

A South Korean oil tanker called “The Universal Winner” is currently in the Strait, attempting to bring Kuwaiti oil home, just behind two Chinese vessels that may have already succeeded in crossing the Strait.

While this is just a trickle of activity compared to before the war, it shows that other countries have run out of patience and are now willing to take calculated risks, to see what level of activity in the Strait is possible.

Overnight market movements:

The FTSE is set to open down 0.4% at 10,280

S&P 500 is unchanged at 7,360

Brent crude is down 75 cents at $107.45

UK Natural gas up at 128p per therm.

The Agenda is complete. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Experian (LON:EXPN) (£24bn | SR51) | Revenue +12%, pre-tax profit up 26% to $1,951m. Adj EPS +15% to 179.8c, at the upper end of expectations. Outlook: expect another year of double-digit adj EPS growth, supported by revenue growth and improved margins. | ||

Severn Trent (LON:SVT) (£9.1bn | SR42) | Revenue +16.6%, with adj EPS up 64.5% to 184.4p. Capital investment rose by 16.7% to £1.9bn. Outlook: “Upgrading 2028 adjusted EPS outlook to at least 250p, from 224p”. Plan £2.2-2.5bn of capex in FY27. | ||

Marks and Spencer (LON:MKS) (£6.8bn | SR48) | Sales excluding Ocado Retail +1.9%, with Food +7% and Fashion, Home & Beauty -7.7%. Adj pre-tax profit -23.8% to £671.4m, with adj EPS -25.4% to 23.8p. Outlook: profit growth is expected to resume versus 24/25. | ||

Ithaca Energy (LON:ITH) (£4.7bn | SR86) | Q1 production of 126 kboe/d (Q1 25: 127k boe/d), EBITDAX down 12.6% to $571m. Management reaffirms all previous guidance. | ||

British Land (LON:BLND) (£3.9bn | SR58) | Underlying profit +5% to £294m, underlying EPS +1% to 28.9p. EPRA NTAV up 4% to 590p per share, LTV 39%. FY27 Outlook: expect FY27 EPS of at least 30.5p, underpinned by LFL rental growth at the top end of 3-5% target range. | ||

RS (LON:RS1) (£2.9bn | SR84) | Revenue -1%, adj pre-tax profit -1% to £246m, adj EPS -1% to 38.7p - in line with expectations. “Building momentum in all regions”, gross margin improved through pricing and stock management. Outlook: “increasing confidence in delivering our medium-term financial targets”. | ||

Energean (LON:ENOG) (£1.6bn | SR33) | Q1 EBITDAX -34% to $184m due to shutdown, production averaged 152 kboe/d since April restart, “tracking original guidance” of 140-150 kboe/d. FY26 production now expected at 130-140 kboe/d to reflect impact of shutdown. Growth plans on track. | ||

Keller (LON:KLR) (£1.58bn | SR97) | Strong start to the year, particularly in North America, with order book of c.£1.7bn (FY25: £1.5bn). 2026 outlook in line with expectations. | ||

Coats (LON:COA) (£1.57bn | SR85) | Revenue up -1% on an organic, constant currency basis. Continued to win market share, but footwear revenue was -1% as “customer caution persisted”. Outlook: 2026 expectations unchanged. | ||

Integrafin Holdings (LON:IHP) (£1.12bn | SR57) | Closing FUD +18% to £77.8bn, with net inflows +14% to £2.4bn. Revenue +11% with underlying pre-tax profit +16% to £43.9m. Received c.25% share of fund inflows to adviser market. Outlook: remain on track to deliver cost guidance. | ||

Playtech (LON:PTEC) (£1.12bn | SR75) | “We have made an excellent start to 2026, with strong trading in the first four months of the year reflecting continued momentum in regulated markets, notably the Americas and certain European markets.” | ||

4imprint (LON:FOUR) (£1.03bn | SR90) | “Trading results for the first four months of the year are in line with the Board's expectations. This reflects solid operational and financial performance, with Group revenue consistent with the same period in 2025.” Order intake was down 2% due to a reduction in new customers. | ||

| M P Evans (LON:MPE) (£733m | SR97) | Indonesian Commodity Exporting (c.10.30am) | Notes today’s announcement by the Indonesian President regarding possible changes to the export of crude palm oil and other commodities. MP Evans sells all of its output locally in Indonesia but says that changes to export arrangements could have an indirect impact on prices available for the group’s output. | AMBER ↓ (Roland) [no section below] This Reuters story suggests the Indonesian government is considering centralising control of commodity exports in order to boost state revenues and improve control over the country’s natural resources. MP Evans says it sells all of its output locally, but I guess some of it may then be exported by a third party. Full details of the changes are not yet known so the impact on market pricing is impossible to predict. Commodity producers – especially in emerging markets – always carry some political risk and this is an example of what can happen. The fact that the market has sent this stock and peer AEP Plantations (LON:AEP) down by c.25% today suggests to me that investors do have serious concerns. Until more is known I think it’s prudent to cut our view to neutral, as there’s simply no way of predicting the likely impact (if any) of this change. |

Bloomsbury Publishing (LON:BMY) (£491m | SR71) | Revenue -9.7%, adj pre-tax profit up 6.7% to £44.9m. Net cash £29.2m. Outlook: two new Sarah J Maas novels due in 2026/27, pre-orders “exceptional”. Strong confidence in recently upgraded expectations. | GREEN ↑ (Roland) I’m upgrading this to be fully positive to reflect March’s upgrade and the improved profitability of the Academic & Professional division. I would like more disclosure on the contribution of inorganic growth, but the long-term growth record of this founder-led business leads me to give Bloomsbury the benefit of the doubt. With the company’s two top authors likely to enjoy new momentum this year, I think it’s fair to take a positive view. | |

Custodian Property Income Reit (LON:CREI) (£411m | SR67) | “Integration of recently acquired portfolios and active asset management continue to drive income growth and underpin fully covered dividend”. Q4 EPRA EPS of 1.5p, Q4 dividend of 1.5p. | ||

Mortgage Advice Bureau (Holdings) (LON:MAB1) (£310m | SR58) | Mortgage applications in the first 19 weeks of 2026 +15% year-on-year, in line with the Board’s expectations. | ||

Science (LON:SAG) (£243m | SR96) | Remains on track to deliver performance in line with expectations in 2026, despite “widely-reported challenges in UK defence contracting”. Considering a potential increase in the return of capital to shareholders. | ||

Integrated Diagnostics Holdings (LON:IDHC) (£241m | SR70) | Q1 revenue +31%, with adj net profit +36% to EGP214m. Branch network at 794 branches, from 641 at 31 March 2025. | ||

Essentra (LON:ESNT) (£233m | SR37) | Trading in line with expectations, full year outlook unchanged. Acquired Boteco, a manufacturer of mechanical components, for up to €9.9m (between 6.5x and 8.7x EBITDA). | ||

S&U (LON:SUS) (£226m | SR75) | “... the turnaround in our fortunes which began last year continues apace. Trading in the first quarter of 2026/27 remains healthily above budget.” | ||

Eco (Atlantic) Oil & Gas (LON:ECO) (£204m | SR31) | Navitas has taken a 37.5% working interest in Block 1 CBK and will become operator. Eco will receive $4m and up to $7.5m in carry for a planned work programme. | ||

Mkango Resources (LON:MKA) (£180m | SR10) | Asset purchase agreement with Heraeus Amloy Technologies GmbH, to acquire its Remloy rare earth magnet recycling business for €8 million (US$9.4 million) in cash. €5m upfront and €3m after two years. | ||

Stelrad (LON:SRAD) (£172m | SR84) | “Stelrad's trading in 2026 to date is in line with management expectations and the Group's full year outlook is unchanged from that given at the full year results on 13 March 2026.” | ||

Knights group (LON:KGH) (£149m | SR62) | Revenue +28%. Organic growth improved to double digits in H2, so full-year organic growth was in line with expectations. Underlying EBITDA +19% to c. £51m. Net debt £65m after spending £17m on acquisitions. | ||

Strategic Minerals (LON:SML) (£143m | SR38) | Revenues from Cobre were $4.2m, the second highest levels since 2017. “Profit before tax reduced to $0.7m from $2.1m primarily due to a non-cash share based payment expense ($0.6m), reduced Cobre profits ($0.3m), costs associated with the Board restructuring and increased Group wide activity levels…” | ||

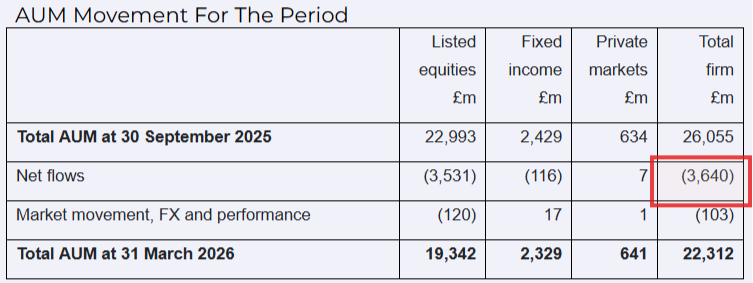

Impax Asset Management (LON:IPX) (£131m | SR77) | Net outflows £3.6bn. AUM falls from £26.1bn (Sep 2025) to £22.3bn (March 2026). Adjusted operating profit £11.3m (H1 2025: £20.5m). Cash reserves £46m. “We recognise that this has been a disappointing Period for Impax shareholders, but we continue to have strong conviction in Impax's resilience and long-term potential.” | AMBER/RED = (Graham - I hold)

In the short-term, I think AMBER/RED (a moderately negative stance) continues to make sense. The very severe profit warning occurred only last month, continuing the trend of disappointment. Today’s interim report, while not resulting in any real change to the headline figures, does still see a cut to the FY26 profit forecasts, after restructuring costs. On a longer-term view, I do still think this is sort of interesting. It has very high Quality and Value scores, making it a Contrarian play. | |

Helix Exploration (LON:HEX) (£78m | SR17) | First revenue-generating helium sales arrangement secured, marking the Company's commercial debut in the helium market following the commencement of production at Rudyard on 23 February 2026. “...a defining moment for Helix as a company.” | ||

Home Reit (LON:HOME) (£76m | SR15) | Loss £18m. Net revenues £7.9m. NAV decreased from £161m (August 2025) to £143m (Feb 2026). NAV falls 11% to 18.1p. | ||

4Basebio (LON:4BB) (£69m | SR1) | Final Results & Clinical Supply Agreement to Support Phase II Clinical Trial | Revenue £1.7m, loss £16.9m. Funded into late 2027. Clinical Supply Agreement with a leading cancer immunotherapy innovator to provide GMP-grade opDNA® starting material for its latest clinical programme. | |

Kavango Resources (LON:KAV) (£33m | SR4) | The metallurgical testwork programme achieved its objective of defining the optimal processing design, processing parameters, and reagent consumption rates for the 50 tonnes-per-day carbon-in-leach gold processing plant at Hillside, and for a future capacity upgrade. “All processing parameters are considered to be within a normal range.” | ||

Synectics (LON:SNX) (£31m | SR83) | EBT funded with £1.5m to satisfy future employee share-based compensation awards. | ||

Headlam (LON:HEAD) (£29m | SR30) | Four months to April 2026: revenue down 21%, “in part a reflection of the planned reduction in certain sales activity as the business implements its new core customer strategy”. Evaluating sale and leaseback of another property. Net debt rises from £31m to £40m. | ||

Lords Trading (LON:LORD) (£29m | SR49) | Revenue +8.3%. Adjusted PBT -26.3% (£2.8m). Actual pre-tax loss £5.2m. Net debt reduces to £13.4m. “Market conditions remain subdued in the near term, with ongoing uncertainty around inflation and interest rates. However, the Group is materially better positioned than a year ago.” | ||

Goldplat (LON:GDP) (£26m | SR98) | Combined operating profit for the quarter of £3,855,000 excluding listing and head office costs, finance cost and FX gains/losses. CEO: "Our operations continue to deliver excellent results, albeit in an uncertain environment with numerous variables, supported by increased volumes and increasing gold price.” | ||

Chesterfield Special Cylinders Holdings (LON:CSC) (£17m | SR74) | Revenue £6.4m (H1 FY25: £5.4m). Adjusted operating loss £1m (H1 FY25: £1.7m loss). H1 was “broadly in line”. “Profitable second half supports expected full-year revenue and adjusted EBITDA at similar levels to prior year… in line with 30 April 2026 trading update.” | ||

CT Automotive (LON:CTA) (£17m | SR52) | Revenues down 4.1%. Adjusted PBT +20.3% ($9.5m). Current trading is in line with management expectations. “...we enter FY26 with confidence in our ability to continue delivering improved performance." $47m of new wins secured in FY25 “changes the picture materially for FY27”. | AMBER/GREEN = (Roland) A strong set of results showing a material improvement in profit margins last year despite flat revenues and a tough industry backdrop. I don’t see any real reason for this business to be trading on three times forecast earnings, although I do note some risks relating to cash flow, competitive pressures and ambiguous guidance for the year ahead. I see this as a potential opportunity, but with some speculative risk. Hence I’m leaving our AMBER/GREEN view unchanged. | |

Fulcrum Metals (LON:FMET) (£13m | SR12) | Agrees to acquire surface rights at the Teck Hughes tailings project. Long-term access secured to key project and infrastructure areas. Price: CAD$220,000 in cash and the granting of a 1.5% Net Smelter Royalty. | ||

Medpal AI (LON:MPAL) (£10m | SR1) | Launches New Health, a dedicated consumer sub-brand focused on the GLP-1 weight-management and broader peptide medicines market opportunity. Related party transaction: the CEO owns the domain names. In six months, the Company will have the option to acquire them. |

Graham's Section

Impax Asset Management (LON:IPX)

Down 6% at 97.54p (£124m) - Interim Results - Graham - AMBER/RED

(At the time of writing, Graham has a long position in IPX.)

I wrote rather triumphantly about IG Group yesterday, so it’s only fitting that I write about this one, too.

I’m down over 60% on my investment here. Thankfully, my portfolio management instincts have served me well - I only made one small starter purchase, and then never topped up on the way down. So this has only ever been a rounding error in my portfolio.

Warren Buffett’s rule of investing is to “Never lose money”. I’m not quite able to manage that, but I’ve generally managed to do the second best thing: “If you do lose money, don’t lose much”!

Anyway, let’s get back to Impax and see why the share price is down yet again.

Please note that we already had a very large profit warning in April, which caused me to downgrade our stance on it to AMBER/RED.

That profit warning was caused by persistent heavy outflows continuing into Q2. The overall H1 outflow result is predictably bad: 14% of starting AUM left the business over a six-month period.

I guess it’s hard to sell environmental investing when the BP and Shell share prices are doing so well:

In addition to the surging oil and mining sectors, there is also of course the constant pressure from passive funds and from the many tech-focused funds that have continued to do well. The S&P and the Nasdaq have both recently made new highs.

Some figures from today’s interim report:

H1 revenue down 23% to £58.8m

Adjusted operating profit down 45% to £11.3m

Actual PBT down 56% to £8.2m.

Cash reserves are £46m.

They say you should never let an investment become a deep value investment, that didn’t start out as one.

Unfortunately, this is becoming that for me. Cash now covers 37% of the market cap.

Estimates: thanks to Andy and Paul at Equity Development for providing continued research coverage of this.

The adjusted operating profit forecasts haven’t moved much today: £14.9m for FY26 and £19.6m for FY27.

However, higher redundancy and restructuring costs have been pencilled in, which causes another blow to the net income forecast for FY26: it falls from £11.1m to £8m. Prior to the April profit warning, £22m had been expected.

For FY27, net income forecast is £14.3m, with an EPS forecast of 11.8p.

If we are willing to value the company based on the FY September 2027 forecast, the P/E multiple on the current share price is 8.3x.

If we are also willing to adjust out the cash reserves (which could be relevant in a takeover situation), the P/E multiple on the current share price falls to 5.2x.

CEO comment:

"Investment performance improved meaningfully from January onwards, with 70% of AUM outperforming generic indices during the calendar year to the end of April. Our active thematic listed equities strategies (which account for 62% of total AUM) have benefitted from market broadening and our portfolio managers' stock selection…

We enter the second half of the year in a position of financial strength, supported by a robust balance sheet, healthy liquidity and a disciplined approach to capital and cost management. Our focus remains on delivering strong long-term outcomes for clients, maintaining operational resilience and positioning the business to benefit as conditions improve."

The point about recent outperformance is important: allocators tend to follow performance and so it makes sense that heavy outflows would continue even as performance had improved.

One year of outperformance might not make a huge difference, but it provides some hope that allocators might start to adjust their stance positively.

Dividends & Buyback

Impax is paying a reduced interim dividend of 2p (last year: 4p), “in light of the Company's lower earnings but resilient financial health”. Equity Development are forecasting 6p of dividends this year, which makes sense - a reduction of 50% on FY25. That would provide a 6% yield at the current share price, and should be covered by earnings even after this year’s restructuring costs.

No new buyback is announced today, but the company notes that the previous buyback completed in December: £10m was spent buying shares at an average price of £1.80..

Graham’s view

I’ll probably keep holding this as I don’t see it going to zero by any means - the balance sheet alone should put a floor on it. It’s a question of to what extent the business model is broken, with trends having moved against it financially and politically, and with customers having lost faith in its ability to outperform.

In the short-term, I think AMBER/RED (a moderately negative stance) continues to make sense. The very severe profit warning occurred only last month, continuing the trend of disappointment:

Today’s report, while not making any real change to the headline figures, does still see a cut to the FY26 profit forecasts, after restructuring costs.

Therefore, I’m staying AMBER/RED in the short-term.

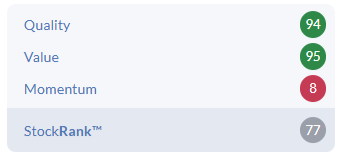

On a longer-term view, I do still think this is sort of interesting. Look at the very high Quality and Value scores, making this a Contrarian play:

I’ve noticed in recent months that Contrarian is my favourite style, as I’m usually open to the idea of looking past short-term momentum when making a long-term investment.

However, it’s a dangerous game to add to a losing position, so I’m not going to do that just yet. In a few months, I’ll reassess.

CT Automotive (LON:CTA)

Up 32% at 31p (£22m) - Final Results - Roland - AMBER/GREEN =

As a number of you have pointed out, this automotive interior trim specialist appeared to be amazingly cheap ahead of today’s results:

When Mark reviewed the company’s year-end trading update in February, he concluded:

Positive business momentum and strong cash flow with a sub-3x P/E just seem like a puzzle that has to be resolved one way or another, so I am sticking with our broadly positive view of AMBER/GREEN.

Today we have the full accounts for 2025 and a chance to review the situation in more detail.

2025 results summary

The opening remarks from founder and CEO Simon Phillips are cautiously encouraging (my emphasis):

FY25 was a year that tested the entire automotive sector, yet CT Automotive has continued to demonstrate resilience and strategic agility. Despite volatility in the market, we delivered a solid financial performance, with a third consecutive year of improved profit before tax. We strengthened margins and won the highest level of new business wins in the Company's history.

The numbers reflect this commentary, with a sharp rise in profit despite a small reduction in revenue:

Revenue down 4.1% to $114.8m

Gross profit up 5.7% to $35.0m

Gross margin: 31% (FY24: 28%)

Operating margin: 9.4% (FY24: 7.3%)

Adjusted pre-tax profit up 20.3% to $9.5m

Earnings per share up 23.9% to 11.4 cents

Net debt up 24% to $7.7m (FY24: $6.2m)

The latest note I can see from house broker Singer Capital (Feb 26) shows adjusted PBT of $10.0m and EPS of 11.9 cents. So it looks like these results are a slight miss, but not enough to be of any concern.

Given the valuation, I would agree with Mark’s previous view that the direction of travel here is more important than any slight variation versus forecasts.

The increase in both gross margin and operating margin last year looks very creditable to me. I think it’s worth stepping through the P&L to see what underlying factors drove these results.

Revenue: conditions are challenging across the automotive sector and this has been reflected in the performance of a number of UK-listed companies. Against this backdrop, today’s commentary from CT Automotive does not seem worrying to me:

Production revenue declined marginally to $101.4 million (2024: $107.8 million) in part due to the macro-economic conditions and a number of programs reaching end of production in FY24.

In contrast, tooling revenue rose by 12.5% to $13.4 million, up from $12.0 million in FY24, boasting a favourable margin. Continued growth in tooling ensures CT Automotive is well established for future years as those tools are used for serial production of the vehicle component.

Profit: achieving a 20%+ increase in profit on flat revenue is not an easy challenge, especially for a capital-intensive manufacturer. Here’s how the company says this was achieved.

Gross profit: “During 2025, we continued to focus on the integration of AI, automation, robotics and digitisation, improving our production facilities to remain one of the most technologically advanced suppliers in our industry.” This led to a 2.95% improvement in gross margin, to c.31%.

Operating profit: greater automation and use of AI allowed CT to reduce its direct workforce by 9.74% in 2025, driving cost savings. The accounts show administrative expenses falling by 4.5% to $22m last year, presumably reflecting lower payroll costs.

While distribution expenses rose by 9% to $2.4m, this reflected the launch of six new programs in Mexico “on a challenging time scale”. This increase is expected to unwind in 2026 and doesn’t seem a problem to me – CT’s ability to nearshore some of its operations from China to Mexico appears to be providing some degree of competitive advantage for supplying US-based manufacturers.

It’s worth noting the main adjustments to profit here related to the impact of exchange rates, so in this case I think the adjusted measures are probably a good guide to underlying progress.

Balance sheet & Cash Flow: operating cash flow before working capital movements was flat last year, at $14.9m (FY24: $15.2m). However, there was a working capital outflow of c.$5.5m, alongside $5.6m of capital expenditure on manufacturing capacity, mainly in Mexico.

It maybe worth noting that the increase in working capital appears to reflect a move to more generous credit terms with some customers:

Additionally, an increase of approximately $6.4 million in net trade receivables was primarily due to higher sales to one customer on longer credit terms in Mexico and the receivable profile changing for another major customer from 15 days to 30 days from December 2025.

My sums suggest the net result was an overall free cash outflow of around $0.5m in 2025. This is one of the factors behind the $0.5m increase in net debt to $7.7m.

Net debt also rose as a result of the withdrawal of invoice financing from major customer Marelli Corporation, which went into administration.

While I like to see good conversion from net profit into free cash flow, this performance appears to be in line with expectations – February’s Singer note shows free cash flow turning positive from 2026 onwards. The circumstances that led to last year’s free cash outflow do suggest to me that performance could improve from hereon – assuming no further customers extend their payment terms – so I’m happy to accept this given that leverage remains modest.

Accounting restatements: as we’ve mentioned previously, the CFO departed abruptly recently. Today we have details of the accounting issues that presumably led to his departure.

The overall impact is limited and doesn’t affect the 2025 results:

These restatements have a non-cash impact on the FY24 Financial Statements, by increasing administrative expenses by $0.8 million and reducing total net assets as at 31 December 2024 by $5.0 million, to $21.2 million. FY24 adjusted profit before tax has therefore been restated to $7.9 million (from $8.7 million).

Full details of the restatements are provided in today’s results - I won’t go into details, but the impression I get is that they all relate to avoidable errors over the period 2021-2024. I guess this explains the departure of the CFO, but I don’t think there are any smoking guns here.

Trading: today’s results emphasise good progress with new business wins, suggesting we should see a return to revenue growth fairly soon:

These programs are expected to deliver approximately $47 million of annualised revenue when all 15 new program awards are fully operational over the next three years.

The company also reminds investors of its OEM customer base, which currently stands at 21. CT says it was pre-qualified to supply two new OEMs last year, but I’m not sure if they are included in the 21.

Management notes the recent gain in market share for Chinese OEMs in export markets, such as the UK. CT doesn’t supply Chinese OEMs “due to the structural characteristics of that market” but says it’s “increasingly cost-competitive” positioning means it is well positioned to help “our legacy OEM customers” cut costs across their supply chain.

Outlook

There are no major surprises in this statement:

Trading in the first quarter of 2026 was in line with management expectations, despite ongoing market uncertainty, including the recent events in the Gulf, that are making trading conditions challenging. Input costs are increasing, but cost escalation clauses in our agreements allow these to be recovered, albeit in some cases with a time lag.

The company doesn’t make any explicit comment on 2026 expectations, perhaps understandably at this early stage. However, management does appear confident of further progress:

… the Board continues to expect profitability to be modestly ahead of FY25

Broker forecasts on Stockopedia prior to today suggested adjusted earnings could rise to 12.6 cents per share this year.

Following this morning’s price rise, I estimate this would be equivalent to a forward P/E of 3.2.

Roland’s view

There are certainly some risks inherent in this business. Credit terms for some major customers appear to have been extended last year, putting cash flow under pressure. I’ve no idea if this was exceptional or if other customers are likely to follow.

The growing market share of Chinese OEMs (who are far more brutal on supplier costs than European/US firms) is also a potential threat. My working assumption is that the growth of Chinese manufacturers will follow a similar path to the historic progress of first Japanese, then Korean OEMs.

In other words, they will steadily gain market share and their vehicles will eventually compete on equal terms with established ‘legacy’ OEMs. If CT doesn’t feel it can compete for business with Chinese OEMs, then this could limit future growth potential.

These may be issues to watch for the future, but I don’t think they are serious enough to justify pricing this business on three times forecast earnings.

Today’s 30% rise will be a welcome relief for shareholders, although this still only takes the stock back to the level last seen in at the start of this year – if progress continues, I think there could be plenty more upside here:

I’m holding back from taking a fully positive view today, due to the small size of this business, its short history as a listed business (2021 IPO) and the risks I’ve mentioned above.

But I don’t see any reason to change our previous AMBER/GREEN view.

Bloomsbury Publishing (LON:BMY)

Unch at 595p (£481m) - Preliminary Results - Roland - GREEN ↑

Bloomsbury’s share price is flat today as the good news was already in the price here following the publisher’s trading update in March, when guidance was upgraded:

The big news of course was the confirmation that hit ‘romantasy’ author Sarah J Mass will be publishing two new books during Bloomsbury’s FY27 financial year:

Bestselling author Sarah J. Maas has announced the publication dates of the next two novels in her A Court of Thorns and Roses ('ACOTAR') series which will be published on 27 October 2026 and 12 January 2027.

In today’s results we learn that “pre-orders of our major titles are exceptional” and are also reminded that a Harry Potter television series will be launched on HBO Max at Christmas. This is expected to “bring the series to a dramatically expanded readership” since its original launch 29 years ago.

The reality of publishing is that many books are unprofitable, while hit authors (like films and music) generate disproportionate profits.

My belief is that Sarah J Mass and JK Rowling continue to account for a surprisingly large (but undisclosed) proportion of Bloomsbury’s consumer division profits. However, they aren’t the only game in town and the business has made efforts to grow and diversify in recent years, notably by expanding its Academic & Professional publishing business.

Today’s group results highlight the benefit of this strategy, with profits up despite a slump in consumer sales:

Group revenue down 10% to £325.9m

Adjusted pre-tax profit up 7% to £44.9m

Adj earnings per share up 8% to 44.57p

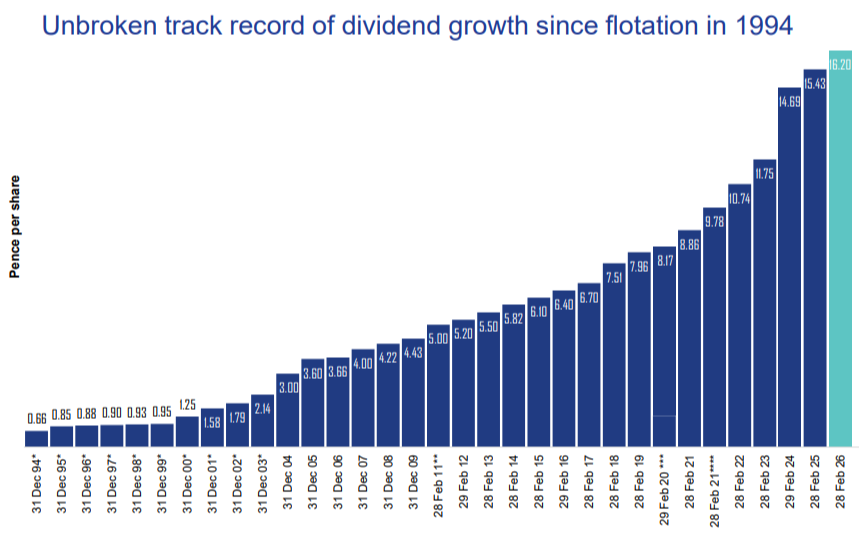

Dividend up 5% to 16.2p per share

Net cash: £29.2m (FY25: £17.0m)

Profitability boost: revenue fell, but profits rose, flagging up a useful increase in operating margin to 10.9% (FY25: 9.2%), or 14.1% on an adjusted basis (FY25: 11.9%).

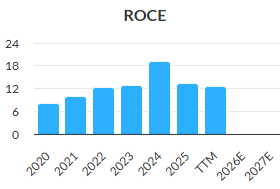

This improved performance translates into a return on capital employed of 14.4% and a return on equity of 12.5% (unadjusted). Both figures are respectable if not spectacular, and are in line with past performance.

Divisional results

The group’s strategy in recent years has been to expand the A&P business so that its profits help to smooth out the greater volatility of the consumer business. Today’s results illustrate how this approach is starting to deliver results.

Consumer Division: despite some top sellers, the consumer business was badly affected by a lack of new titles from the company’s star author Sarah J Maas:

Consumer revenue down 21.4% to £218.2m

Consumer adj pre-tax profit down 32.3% to £20.5m (9.4% margin)

Academic & Professional: the company completed the integration of its Rowman & Littlefield acquisition last year and signed an AI licensing agreement to monetise the value of its intellectual property. Management reports “encouraging signs of recovery with good growth in all territories in the current financial year”.

A&P Revenue up 29.3% to £107.7m

A&P adj pre-tax profit up 100% to £25.0m (23% margin)

It’s worth noting this wasn’t all organic growth.

Rowman & Littlefield was acquired for £65m in May 2024, so made an increased contribution last year.

Last year’s AI agreement may also have provided a material and high-margin boost.

I’d consider both of these factors to be inorganic growth – it would be interesting to know how the underlying business performed excluding these one-off changes. Unfortunately, Bloomsbury doesn’t seem to disclose this information. This means it’s unclear how well acquired businesses – or legacy operations – are performing, so it’s hard to gauge how much value has been created by some past acquisitions.

Outlook

Today’s outlook statement is in line with expectations:

Bloomsbury has a strong wider publishing list in 2026/27, including two new Sarah J. Maas novels. These led to a trading update upgrading our profit expectations for 2026/27. Pre-orders of major titles are exceptional. The Board looks to the current year with strong confidence in delivering results in line with these recently upgraded expectations.

Guidance was upgraded in March so there is no logical reason to expect a further upgrade today, ahead of the publication of these exciting new titles.

These forecasts leave the shares trading on a FY27 forward P/E of 13, with a possible 2.8% dividend yield. That seems quite reasonable and is at the lower end of the valuation range we’ve seen in recent years:

Roland’s view

I’ve long had a slightly ambivalent view about Bloomsbury. On the one hand, it is clearly a successful, founder-led business with an impressive long-term record of growth.

Revenue has tripled since 2014 and today’s dividend increase marks the 31st consecutive year of growth:

On the other hand, I’ve never quite been persuaded to buy the shares. This may be my mistake. But the average profitability of and dependence on a handful of hit authors. The slump in consumer division profits last year highlights what can happen when there are no big-name releases in a year.

I also have some niggling concerns about the profitability of some parts of the Academic & Publishing business. This unit has made multiple acquisitions in recent years, but I don’t feel there’s much transparency on how these perform.

I’d particularly like to have seen a breakdown of the 100% profit growth achieved in the A&P division last year.

We’ve been AMBER/GREEN on this business in recent times, but given the scale of March’s upgrade and the improved profitability of the A&P business, I think it’s fair to move up one notch to be fully positive today. GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.