Good morning!

The most interesting story overnight has been the IPO plans for SpaceX, giving us a welcome reprieve from looking at the conflict in Iran.

If you’d like to read the original document, it’s available here.

The IPO is being set up to keep Elon Musk firmly in control: there will be Class A shares with 1 vote each, and Class B shares, with 10 votes each. Furthermore, the Class B shares (which are not being offered in the IPO) will have special powers:

Mr. Musk will be able to control the outcome of matters requiring shareholder approval. This includes the election of (i) a majority of our board, through his ownership of Class B shares (as Class B Directors)... and (ii) the remainder of our board, for so long as he holds a majority of the combined voting power of the Class A and Class B common stock… we intend to rely on exemptions from certain corporate governance requirements.

Bearing in mind that I’m a longtime Musk sceptic and former short-seller of Tesla shares, it’s possible that I might be a little biased against this IPO.

But it’s hard not to be, for anyone with value instincts.

The company’s mission: “to build the systems and technologies to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars”. They can’t be blamed for lacking ambition!

But the financials here are truly mind boggling.

The company is looking to raise $75bn and achieve a $1.75 trillion valuation.

Recent results:

Q1 2026 revenue $4.7 billion

Q1 2026 operating loss $1.9 billion

And for last year:

2025 revenue $18.7 billion

2025 operating loss $2.6 billion

Financially, this looks to me like an even more extreme version of Tesla.

Supporters would argue that Tesla eventually grew into its valuation.

Sceptics like myself would argue that Tesla still hasn’t done that - and that the company was dangerously close to collapse on multiple occasions (which I think Musk himself would agree with).

Like Tesla, it requires investors to accept unusual corporate governance practices that favour Musk.

And like Tesla, SpaceX offers multiple businesses packaged together, some of which have more substance than others.

Whatever the outcome, this IPO will be a landmark event in the markets generally. It will be particularly relevant for investors in certain UK stocks - Seraphim Space Investment Trust (LON:SSIT) and Filtronic (LON:FTC) spring to mind.

Overnight market movements:

The FTSE is set to open down 0.2% at 10,390

S&P 500 is unchanged at 7,430

Brent crude is up $1 at $106

Gold is unchanged at $4,530

Bitcoin is unchanged at $77,850

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BT (LON:BT.A).A (£23bn | SR70) | Reported revenue £19.7bn down 3% and adjusted revenue £19.6bn, down 4%. Reported profit before tax £1.4bn, up 8%. Updated dividend policy. | ||

Sage (LON:SGE) (£8.2bn | SR35) | Underlying total revenue increased by 11% to £1,363m. Sage Business Cloud revenue increased by 15%. Underlying basic EPS increased by 16% to 23.7p. Interim dividend up 8%. Renewal rate by value of 102%, ahead of last year. Now expects organic total revenue growth for FY26 to be above 9%. | AMBER/GREEN = (Ed S) Today’s H1 results from Sage show minimal signs of AI disruption. Revenue is up by a healthy amount and renewal rates have increased. A dividend hike of 8% suggests that management is confident about the future. After a big sell-off this year due to AI concerns, I see the potential for a recovery. | |

Smiths (LON:SMIN) (£7.5bn | SR57) | Organic revenue growth was flat in the third quarter, leading to +0.2% growth for the nine-month period. Now expecting FY2026 organic revenue growth of ~2% versus previous guidance of 3-4% excluding any impact from the conflict in the Middle East. | ||

Investec (LON:INVP) (£5.5bn | SR57) | Operating income up 4% up to £2,281m. Adjusted earnings per share increased by 4.8% to 82.9p. Customer deposits increased by 8.7% to £44.7bn. Dividend increased by 5.5%. | ||

ICG (LON:ICG) (£5.2bn | SR65) | Management fees of £685m, up 13% y-o-y. Performance fee income of £127m (FY25: £86m). Total ordinary dividend per share for FY26 of 87p (FY25: 83p). "Unaffected by challenges being faced by certain evergreen vehicles in the US." | ||

Londonmetric Property (LON:LMP) (£4.4bn | SR46) | Net rental income increased 16.6% to £455.3m. Total property return of 7.1%. EPRA earnings up 13.9% to £305.3m. Dividend up 3.8% to 12.45p. | ||

ConvaTec (LON:CTEC) (£4.2bn | SR31) | YTD organic revenue growth ex-InnovaMatrix of 4.8%. Broad-based growth across categories with product launches performing well and gaining share. FY2026 guidance unchanged. On track to deliver 5-7% organic revenue growth ex-InnovaMatrix for FY2026. Growth expected to increase in H2. | ||

Autotrader (LON:AUTO) (£4.0bn | SR32) | Revenue growth for the year was 4%. Revenue growth in H2 was 3% and lower in the fourth quarter, reflecting more difficult trading conditions. Basic earnings per share up 8%. The Board believes the prevailing Autotrader share price does not reflect the Company's fundamentals or long-term prospects and is updating its capital allocation policy. Expects to return over £1bn to shareholders over the course of 2026 and 2027. | (Graham) | |

easyJet (LON:EZJ) (£2.6bn | SR46) | H1 FY26 result was in line with April trading statement. H1 FY26 headline loss before tax of £(552) million. £4.7 billion of liquidity and net cash of £434 million. Passenger growth: +6% YoY. Load factor improved by 2 ppts to 90%. Not seeing any disruption to fuel supply. H2 FY26 Fuel CASK remains uncertain due to price volatility. 72% hedged at $726/MT. | ||

Tate & Lyle (LON:TATE) (£2.3bn | SR36) | Challenging market environment impacted financial performance. Group revenue down 3% reflecting muted market demand. Adjusted profit before tax down 5%. Full-year dividend in-line with prior year. For the year ending 31 March 2027, expects to deliver modest revenue growth and broadly flat EBITDA. | TAKEOVER | |

Qinetiq (LON:QQ.). (£2.3bn | SR45) | Record order intake of £3,573m. Book-to-bill 1.14x. Record year-end backlog of £4.8bn. Revenue increased 1.3% on an organic basis. EPS grew 21% to 31.5p. 24% increase in full year dividend. £200m share buyback extension of £100m p.a. through FY29. Record order intake and backlog provide “clear visibility of sustainable growth and strong multi-year cash flows.” | ||

AJ Bell (LON:AJB) (£2.1bn | SR70) | Revenue up 19% to £183.0m. Underlying profit before tax up 15% to £79.0m. Underlying diluted earnings per share up 18% to 14.61p. Dividend increased by 11%. Further share buyback programme of up to £15 million. Strong growth in customer numbers. Now expects full-year revenue margin, PBT and PBT margin to be higher than previously guided. | GREEN = (Ed S) | |

Hill and Smith (LON:HILS) (£2.1bn | SR86) | Trading in the period was positive and slightly ahead of its expectations, reflecting continuing robust demand for infrastructure solutions in the US. Group revenue was up 5% on an organic constant currency basis. | ||

Mitchells & Butlers (LON:MAB) (£1.5bn | SR93) | Like-for-like sales growth of 3.3% over the first half. Adjusted operating profit of £181m (HY 2025 £181m). Net debt reduced. | ||

Great Portland Estates (LON:GPE) (£1.23bn | SR27) | Executing our growth strategy (FY March 2026 results) | Diluted EPRA EPS of 8.5p vs 5.2p in 2025. Portfolio valuation of £3.0 billion, up 4.3%. FY'27 rental growth guidance of 4.0% to 7.0%. | |

| ZIGUP (LON:ZIG) (£970m | SR97) | Pre-close Trading Update | The FY2026 financial year ended strongly. Now expects the group's financial outturn for the year to be at the top of market expectations. | GREEN ↑ (Graham) |

Close Brothers (LON:CBG) (£693m | SR54) | Q3: “Resilient underlying profitability, benefitting from a robust NIM and modest growth in the core loan book.” “We have delivered a solid performance in the quarter and at this stage (and subject to current macroeconomic developments) remain on track to deliver the 2026 financial year in line with guidance.” | ||

Tungsten West (LON:TUN) (£482m | SR36) | Entered into a binding US$25.0 million bridging loan facility. Key terms: $25m, interest rate c. 8% (benchmark +4.5%), increasing 1% per quarter. Term 366 days. Related party transaction: lender is controlled by a major shareholder. | ||

Young & Cos Brewery (LON:YNGA) (£443m | SR85) | Revenue +4.6%. Adjusted PBT +2.9% (£53.1m). “It has been a good start to the new financial year…. We are very optimistic about the future. The business has strong momentum, like-for-like sales and profit are growing, and our operating margin remains industry leading.” | ||

Ashtead Technology Holdings (LON:AT.). (£432m | SR70) | Q1 was in line. “Whilst the duration and impact of the conflict in the Middle East, and the potential secondary effect on our broader operations and markets, remains hard to predict, the Board is cautiously optimistic in the outturn for the year, and its performance expectations are unchanged.” | ||

Sabre Insurance (LON:SBRE) (£388m | SR89) | Gross written premium +15% to £76.3m. Reiterates guidance given at full-year 2026 results. | ||

Ibstock (LON:IBST) (£382m | SR32) | “Whilst we are mindful of the potential impact of the Middle East conflict, the Board believes recent activity levels support the Group's capability to deliver a full year outturn broadly in line with current market consensus expectations.” Domestic brick volumes down 11% in Q1. | ||

Tharisa (LON:THS) (£372m | SR99) | Revenue +28%. Net profit after tax $46.6m (HY2025: $8.2m). “The past six months have seen Tharisa deliver robust operational and strategic progress, underpinned by the resilience of global commodity markets.” | ||

Yu (LON:YU.). (£290m | SR98) | Extends the structured trading agreement with Shell Energy Europe for additional three years to 2032. The extension includes a significant increase in volume capacity and “ensures Yü Group are well placed to deliver their ambitious stated growth plan to secure a 7-9% market share by 2028.” | ||

Niox (LON:NIOX) (£259m | SR43) | Trading for the year to date has been in line with management expectations. | ||

Capricorn Energy (LON:CNE) (£229m | SR98) | Year-to-date, production is tracking within guidance range of 18,000 - 22,000 boepd. Debt free with cash balance $132m. | ||

Henry Boot (LON:BOOT) (£213m | SR45) | Heavy H2 weighting, consistent with recent years. “...assuming market conditions do not materially deteriorate, we anticipate delivering profit before tax in line with consensus expectations for 2026.” | ||

Cab Payments Holdings (LON:CABP) (£207m | SR42) | Authorised by the Bank of Guyana to establish a permanent representative office in the country. The new office in Georgetown will create a permanent on-the-ground presence for CAB in South America. | ||

BTG Consulting (LON:BTG) (£188m | SR84) | Results for the year to be above the top end of market expectations. Revenue +10%. Adjusted PBT +6% (£25m). Net debt £1m after acquisition payments. Outlook: “A backdrop of increased macroeconomic uncertainty is expected to continue to drive demand for our restructuring and advisory services.” | (Graham) | |

Savannah Resources (LON:SAV) (£185m | SR38) | Priorities for the remainder of 2026: “completing the DFS in July, progressing the geotechnical fieldwork… advancing Front End Engineering & Design work, completing the RECAPE submission, and continuing to develop the Barroso Lithium Project's financing and commercial arrangements.” | ||

Helios Underwriting (LON:HUW) (£148m | SR47) | NAV total return 12.3%. NAV per share £2.63. PBT £20.5m (2024: £20.9m). Outlook: “...the insurance cycle is likely to moderate. As markets soften, returns on capital will naturally reduce. Our focus, therefore, is on cycle management…” | ||

Trufin (LON:TRU) (£130m | SR90) | Conditionally agreed to sell Playstack to VantageCo Limited (Integrated Media Company group) for net cash proceeds c. £112.4m. TRU intends to return £70m to shareholders. Proposed price for tender offer of 140p. | AMBER ↓ (Graham) | |

Invinity Energy Systems (LON:IES) (£128m | SR14) | Flexbase has selected Invinity to design a GWh-scale vanadium flow battery for deployment at the Technology Centre Laufenburg. | ||

FDM (Holdings) (LON:FDM) (£115m | SR68) | Trading for the first four months of the year has been in line with the Board's expectations. “While the Board remains mindful of current macroeconomic and political uncertainties, encouraging indicators continue to show… FDM is well placed to deliver improved performance as soon as market conditions permit.” | ||

SDI (LON:SDI) (£84m | SR85) | FY April 2026: full year earnings to be in line with current market expectations. | ||

Braemar (LON:BMS) (£78m | SR53) | FY26 results in line with expectations. Trading in the first two months of the new financial year has been strong. “...confident of further progress and of delivering annual revenue of £200m by FY30.” | ||

Vulcan Two (LON:VUL) (£71m | SR31) | Institutional placing for £40.0 million in March 2026. Then completed the acquisition of three ePharmacy businesses, max consideration £41.7m. “The early signs are encouraging.” | ||

Michelmersh Brick Holdings (LON:MBH) (£68m | SR58) | "Despite the prevailing trading conditions, while we currently expect the Company to deliver performance in line with full-year expectations, we are watchful of the continuing political instability..." | ||

Zephyr Energy (LON:ZPHR) (£65m | SR25) | Further divestment of undeveloped non-core acreage generating US$2.275 million. | ||

Seascape Energy Asia (LON:SEA) (£63m | SR33) | Operating loss £4.4m. Profit for year £5.4m reflecting proceeds from farm down of an asset. Year end cash £6.3m. Outlook: “Progress the Company's Temaris Cluster and DEWA through to FDAP submission during 2026, targeting first gas in 2028 and allowing Seascape to book initial 2P reserves.” | ||

Ilika (LON:IKA) (£60m | SR8) | FY April 2026: revenues of c. £1.1m, including £100k of commercial revenue from Stereax electrode sales (2025: £1.1m), and an EBITDA loss excluding share-based payments of approximately £6.2m (2025: EBITDA loss of £5.2m). Cash £5.3m. | ||

Software Circle (LON:SFT) (£59m | SR16) | New £25m facility with Santander used to refinance the Group's pre-existing facilities with Shawbrook. TU: “another year of strong progress, with revenue growth of 22%, a meaningful step-up in profitability with an 81% growth in Adjusted EBITDA and the continued successful execution of its acquisition strategy.” | ||

Nexteq (LON:NXQ) (£35m | SR93) | “As a result of the continuing uncertainty in the Quixant business, FY26 Group revenue is now expected to be approximately 15% below previous market expectations with a consequential impact on adjusted profit before tax.” | BLACK | |

Works co uk (LON:WRKS) (£34m | SR97) | Revenue +3.2%. LfL sales +3.3%. “...Confidence in achieving recently upgraded FY27 guidance” and medium-term EBITDA goal of at least £22.5m in FY30. | ||

Hardide (LON:HDD) (£30m | SR60) | Revenue +71% (£4.8m). Operating profit £1.3m. “...Well positioned to deliver full year performance in line with recently upgraded expectations.” | ||

Robinson (LON:RBN) (£21m | SR83) | Sales volumes +6%. Total revenue +6%. Underlying operating profit in the first four months of 2026 below the same period in 2025, reflecting the challenging trading environment. Outlook in line. | ||

Zinc Media (LON:ZIN) (£12m | SR15) | Commissioned to produce a major television series in the GCC, with a contract value of $6m. |

Graham's Section

Trufin (LON:TRU)

Down 2% at 135p (£127m) - Proposed Disposal of Playstack - Graham - AMBER ↓

This strikes me as a somewhat disappointing outcome and it ties in with my analysis in January of Trufin’s new management incentive plan.

First, an overview of today’s news:

£125m gross proceeds from the disposal of games publisher PlayStack

Net proceeds of £112.4m, including the repayment of a £15.6m loan.

The £15.6m loan between the parent company Trufin and its subsidiary PlayStack is not something that should show up in the consolidated group accounts. So from a group perspective, I’d expect to see a cash infusion of less than £100m.

This is a “fundamental change of business”, so requires a vote.

But that shouldn’t be a problem: 32.8% of shares are already subject to “irrevocable undertakings” to support the sale, and there is also a letter of intent for another 11.5% of shares. So over 44% of shares are already lined up to vote for this.

The buyer: Integrated Media Company, which is part of TPG (formerly known as Texas Pacific, a US private equity group).

Tender offer: “the company intends to return £70m to shareholders”. The proposal is for a tender offer at 140p, slightly above the current share price (this is perfectly normal). But this is yet to be finalised.

CEO comment:

"We believe the disposal of Playstack represents a milestone for TruFin and a clear demonstration of our disciplined approach to capital allocation and value creation. We've thoroughly enjoyed working with the Playstack team over the last few years and look forward to them achieving future success.

Graham’s view

I should say now why I view this outcome as slightly disappointing.

Going back to my notes in January, there was a broker estimate for the value of Trufin’s PlayStack investment of £150m.

This was lowered to £137m as a result of a new bonus scheme for PlayStack’s management team.

This bonus scheme incentivised a disposal to happen as quickly as possible, as the “Hurdle” above which the options would have value was increasing at 12% per year.

To put it simply: the longer it took for a disposal to occur, the less valuable their options were.

Only four months later, a disposal has been announced and it seems to me to be at a pretty significant discount to the level at which the PlayStack investment had been valued.

On the other hand, several (presumably very well-informed) large shareholders are supportive of the proposal, so perhaps it’s a reasonable outcome.

Trufin will continue to own 85% of Oxygen and 80% of Satago.

Oxygen (early payment provider for the public sector): 2025 revenue £9m, EBITDA £4m.

Satago (cash flow software for businesses): 2025 revenue £1m after losing a major contract.

I’d value Trufin as:

£12m cash at year-end 2025

c. £100m cash infusion from the PlayStack disposal.

Plus whatever you think Oxygen and Satago is worth.

With a current market cap of £127m (pre-tender offer), and perhaps c. £110m in cash, it seems to me that Oxygen and Satago are being valued at less than £20m. That might be fair.

With no further upside from PlayStack investment, I think this becomes a less interesting share, so I’m taking us down to neutral on it.

It has been a big winner over the past year and has a StockRank of 90, but I think the company is now effectively cashing in its biggest chips.

ZIGUP (LON:ZIG)

Up 2% at 432.5p (£990m) - Pre-Close Trading Update - Graham - GREEN ↑

This used to have the less exciting name Redde Northgate.

It provides various “mobility solutions” - van rental, accident/claims management, replacement hire and bodyshop repair.

Roland liked the Interim Results published in December, leaving our AMBER/GREEN stance unchanged.

Today’s update is good, too: “we expect the Group's financial outturn for the year to be at the top of market expectations”.

The consensus range is helpfully provided: adjusted PBT of £154.5 - 159.3m.

Leverage is in line with guidance at 1.9x (I’m fine with anything below 3x).

CEO comment:

'Customers are clearly seeing significant value in our service-led offering, and I am very pleased with the contributions from across our divisions this year. Average VoH is up 4.9% for the year and we have secured a number of valued contract wins and renewals, underpinning this good momentum; Steady State Cash generation has stepped up materially and supports our ambition for further growth'.

[VoH = vehicles on hire]

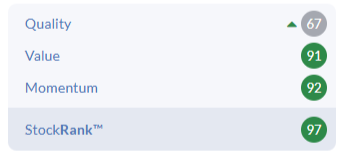

Graham’s view

This one is highly-ranked:

Quality is the only weak point. These metrics are lukewarm:

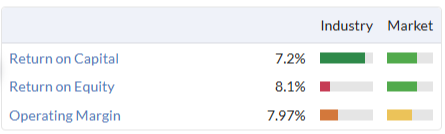

The company argues for having competitive advantages, mostly to do with greater scale, coverage and customer service levels. When it comes to accident management, for example, they say that their customers benefit from “the breadth and quality of services offered through its claims and services platform; the ability to fully connect into insurance partner systems; and efficiencies from scaling automated processes and self-serve portals for policyholders.”

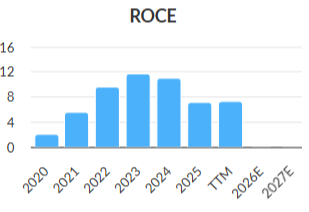

Maybe this is true but as someone who doesn’t specialise in the sector, it doesn’t strike me as the type of business that would be expected to earn sustainably high returns over the long-term. What are the barriers to entry? This is borne out in pretty average ROCE over time:

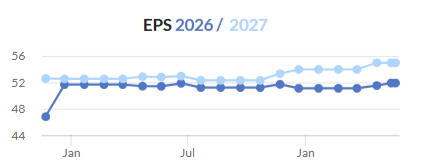

However, at the same time, it has developed a nice track record of maintaining its earnings forecasts:

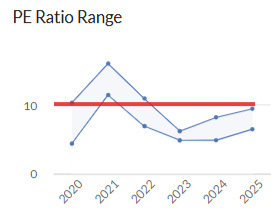

I’ll give this a boost to GREEN today, on the basis of the strong momentum and sturdy performance. I wouldn’t do this if it was already at a P/E of about 10x - and I’ll want to take us back to AMBER/GREEN if it gets there.

Ed S's Section

AJ Bell (LON:AJB)

Up 12% at 598p (£2.4bn) - Interim results for the six months ended 31 March 2026 - Ed S - GREEN=

The team has been GREEN on this investment platform company for a while now and they were right to be. Today, we have strong interim results and the share price has popped by around 12% to record highs!

Key numbers:

Revenue up 19% to £183.0 million (HY25: £153.2 million)

Underlying profit before tax (PBT) up 15% to £79.0 million

Underlying PBT margin of 43.2% (HY25: 44.9%) reflecting increased investment in brand and propositions, which drove record business growth

Statutory PBT up 35% to £92.8 million

Statutory diluted earnings per share up 39% to 17.13 pence, reflecting a net exceptional gain of £13.8 million

Underlying diluted earnings per share up 18% to 14.61 pence

Dividends/buyback:

Interim dividend of 5.00 pence per share, up 11% versus prior year

A further share buyback programme of up to £15 million, in addition to the previously announced £50 million programme

Operational highlights:

The platform business added a record 79,000 customers to close at 723,000, up 12%

Platform AUA up 5% in the period to £108.7 billion, driven by record net inflows of £4.2 billion and favourable market movements of £1.2 billion

Investment business AUM increased by 10% in the period to close at £9.8 billion

Outlook:

We now expect full-year revenue margin, PBT and PBT margin to be higher than previously guided. Excellent returns from our investment in brand and marketing give us confidence to invest more than originally planned in the second half of the year, while still expecting to deliver materially higher profitability.

The platform market presents significant long‑term growth opportunities, and our continued business investment positions us well to capitalise on these. We remain confident in the outlook, with strong momentum continuing into the second half of the year.

Ed S’s view:

There’s a lot to like here from an investment perspective. The key theme is scalability. With people continually saving and investing for retirement, and global equity markets continually moving higher, there’s potential for this company to get much bigger over time (could Savvy the Squirrel help?). In its H1 results today, the company points out the UK platform market continues to present “significant structural growth opportunities,” with an estimated £2.4 trillion being held off platform.

Looking beyond the theme, I like the financials – there’s a lot of quality here (the Stockopedia quality rating is 93). This is a company with a good growth track record and a very high return on capital employed (ROCE). It also has a growing dividend (the yield is close to 3%). The fact that the company has hiked its payout by 11% today suggests that management is confident about the future.

In terms of risks, competition from rivals is one to monitor. I don’t think we need to worry too much about Hargreaves Lansdown for now – I suspect the company is winning customers from them due to Hargreaves’ recent fee changes (which didn’t go down too well with investors). I’m more concerned about the likes of Vanguard (and the rise of passive investing) and the zero-commission trading platforms like Robinhood (disclosure: Ed S has a long position in $HOOD). Some of these newer players are very innovative with their offerings and are very appealing to younger investors.

Is the valuation risky? I’m comfortable with it given the company’s quality, strong track record, and scalability potential. That said, one does need to be prepared for share price volatility with this stock. Over the last five years it has had some big dips.

As for the rating, I’m going to keep it on GREEN given today’s upgrade to guidance. In my view, there’s potential for further gains here in the medium term.

Sage (LON:SGE)

Down 2% at 875p (£8.0bn) - Results for the six months to 31 March 2026 (unaudited) - Ed S - AMBER/GREEN =

Accounting software firm Sage (which I hold) has posted its half-year results today and they look very solid to me. Here are some highlights:

Underlying total revenue increased by 11% to £1,363m, reflecting broad-based growth across the business underpinned by strength in cloud solutions

Underlying annualised recurring revenue (ARR) up 11% to £2,727m, with growth across all regions balanced between new and existing customers

Sage Business Cloud revenue increased by 15% to £1,162m

Renewal rate by value of 102%, ahead of last year (H1 25: 101%), reflecting higher sales to existing customers, including the growing adoption of AI-powered features, supported by strong retention rates

Underlying operating profit grew by 15% to £326m, driving a margin increase of 80 basis points to 23.9%

Statutory operating profit increased by 15% to £293m

Underlying basic EPS increased by 16% to 23.7p, whilst statutory basic EPS increased by 14% to 20.7p

£1.1bn of cash and available liquidity; net debt to underlying EBITDA of 2.0x

Interim dividend up 8% to 8.05p, in line with progressive policy

Outlook:

Building on strong momentum in the first half, we now expect organic total revenue growth for FY26 to be above 9%. We continue to expect operating margins to trend upwards in FY26 and beyond, as we focus on efficiently scaling the Group.

With our trusted scalable platform, growing agent portfolio and strong momentum supported by investment across the business, I am confident in Sage's ability to deliver growth and long term value for all stakeholders.

Ed S’s view:

This tech stock – which I hold – has been dragged into the AI-related SaaS sell-off recently. Year to date, it’s down about 15%.

’ve always thought that the heavy selling activity here isn’t really justified. My reasoning is:

Small business owners tend to be really busy running their businesses. Do they have time to sit around ‘vibe coding’ new accounting software?

There’s a lot at stake with accounting software. Get it wrong (as AI often does) and a business could be looking at loss of revenue, fines, reputational damage, and more.

Now obviously, it’s still very early days in terms of the AI disruption story. But today’s results from Sage suggest that the company isn’t seeing much disruption.

One figure that stands out to me is the renewal rate by value of 102%. This was up year on year thanks to higher sales to existing customers and the growing adoption of AI-powered features.

Another is the 15% growth in Sage Business Cloud revenue. This represents an acceleration of growth – last financial year growth here was 13%.

There’s also the increase in the dividend (+8%). This suggests that management is confident about the future.

Small and mid-sized businesses trust Sage to run their mission-critical finance, payroll and HR workflows, where accuracy and compliance are non-negotiable.

It’s worth noting that in the results, CEO Steve Hare talks about how Sage’s AI features are helping customers:

Our intelligent agents are already helping finance teams accelerate cash flows, close the books faster, plan more effectively and turn insight into action, without compromising control or accountability.

By embedding AI directly into our customers' day-to-day work, we are making our solutions more valuable, reinforcing our competitive advantages, and driving efficient, sustainable growth.

Looking at today’s figures and the commentary from management, I remain relatively bullish on the stock. To my mind, there is upside potential from here given the growth and the valuation.

Note that this morning, analysts at Peel Hunt have upgraded to the stock to Buy from Hold. Their price target is 1,165p (down from 1,187p).

They point to the margin expansion. They believe that this will be a source of earnings upgrades.

Putting this all together, I’m going to leave the stock on AMBER/GREEN. There is obviously some uncertainty around AI disruption but at current levels, I like the risk/reward skew.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.