The stalemate in the Strait of Hormuz continues for now, with the ceasefire itself on shaky ground but with President Trump thought to be very keen to find a politically acceptable deal.

Elsewhere, Bloomberg reports that a merger between SpaceX and Tesla is “inevitable and only a question of timing”, according to influential SpaceX investor Peter Diamandis.

The motivation for this, according to Peter Diamandis, would be to give Musk voting control over Tesla, which he currently lacks but which he will retain at SpaceX. Musk currently owns 11% of Tesla.

Thinking more broadly about the SpaceX IPO, and the $2 trillion valuation (which I consider to be absurd), I do have to admire Musk. He has always been remarkably successful when it comes to monetising investor demand.

He’s an engineer, an entrepreneur and a product designer, yes. But I think what makes him stand out above all of these is his ability to sell a dream to his investors - at Zip2, PayPal, Tesla, Solar City and now SpaceX. I don’t think I’m reaching when I say that nobody else in the history of capitalism has been more successful than him, when it comes to motivating investors to hand him their hard-earned cash.

And in a world where US tech valuations are high and where passive money flows are constantly streaming into the US markets, he does what is financially logical: he gives these money flows something else to invest in.

Overnight market movements:

The FTSE is set to open down 0.6% at 10,430

S&P 500 is down 0.1% at 7,510

Brent crude (July delivery) is up 3% at $97.10

Gold is down 1% at $4,400

Bitcoin is down 3% at $73,000

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

SSE (LON:SSE) (£29.5bn | SR66) | Revenue approx. unchanged at £10.2 billion. Adjusted operating profit down 8% at £2.2 billion. Adjusted Earnings Per Share of 153.5p, down 5% year-on-year but towards the upper end of guidance. Earnings targets of between 168 - 193 pence for 2026/27 (adjusted for equity issuance) and between 225 - 250 pence for 2029/30 remain unchanged. | ||

Computacenter (LON:CCC) (£4.48bn | SR90) | Buys Government Acquisitions Inc, a Value-Added Reseller focused on the US federal government market, for an enterprise value of up to $92m. | ||

Johnson Matthey (LON:JMAT) (£3.66bn | SR53) | Revenue +14%, sales excluding precious metals down 10%. FY26 underlying operating profit +14% and in line with previously upgraded guidance. FY27 outlook: low to mid single digit percentage growth in underlying operating profit (at constant FX and metal prices). | ||

Harbourvest Global Private Equity (LON:HVPE) (£2.33bn | SR87) | Net Assets of $4.3bn (2025: $4.0bn). NAV per Share Return ($) +9.7%. Discount to NAV (£) reduced from 35% to 26%. At least $500m to be distributed to shareholders during 2026. Further investment commitments paused for the remainder of the year. | ||

Sirius Real Estate (LON:SRE) (£1.57bn | SR69) | SRE has notarised the acquisition of a light-industrial business park in Fulda, north east of Frankfurt, for €49.8m. | ||

Vesuvius (LON:VSVS) (£1.17bn | SR89) | Revenue and trading profit in the first four months of year slightly ahead of last year on a constant currency basis. “We confirm our guidance for FY26, with H2 trading expected to be stronger than H1.” | ||

PPHE Hotel (LON:PPH) (£675m | SR36) | Possible cash offer at £22 per share, a 47% premium to share price on 13th Nov (prior to investor meetings being held to discuss options). [Note by Graham: it’s a 36% premium to last night’s close]. From PPHE last night: “The Board… has evaluated the Proposal and determined that the Proposal represents fair value.” | TAKEOVER (Graham) Against PPHE's official asset value, this offer does not appear all that generous: it’s a 20% discount to the company's December 2025 EPRA NRV (real estate's equivalent to NAV). On the other hand, it could be argued that nobody believed that figure anyway. if you go back to last November, the share price was trading at a discount of ~50%. If we measure the offer against earnings, it looks better. The lesson, if there is one, is to not have blind faith in real estate NRVs - but also to get interested when there is a 50% discount and a clear catalyst. In this case, the catalyst came in the form of major shareholders looking for an exit. Congratulations to everyoneone who has made money out of this share. | |

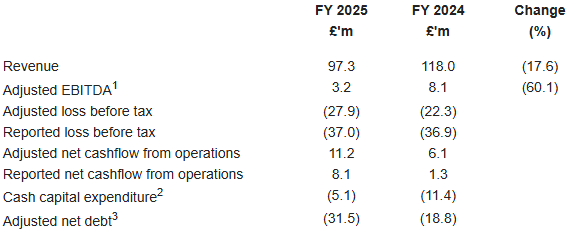

Iqe (LON:IQE) (£497m | SR29) | Revenue down 17.6%. Adjusted EBITDA £3.2m (FY24: £8.1m). Reported loss before tax £37m. Raised £81m in 2026. Outlook: Q1 trading in line. Revenue for FY 2026 is expected to exceed 20% growth year-on-year, with strong order book visibility into H2. This is expected to result in a high-single digit to low double-digit adjusted EBITDA position. [Graham: unusual phrasing!] | RED = (Mark) Poor results highlight that all of the current excitement about this company is based on future expectations of growth from AI data centres, for which there is little sign in current numbers. The recent placing at a 58% discount removes the immediate financial distress in the business. However, it makes the current proforma EV of around £640m look daft compared to a forward EBITDA of less than £12m. Investors can own the world’s best semiconductor fabs for less than half the rating IQE is on. I can’t help feeling a sense of déjà vu, where a decade ago a very similar excitement around a new use for IQE’s semiconductor fabrication led to the share price 10-bagging and the company raising money at the top, only to see years of ongoing losses leading to the shares losing 97% of their value. I’m not saying exactly the same is going to happen this time. However, there is enough of a similarity for me to keep our firmly negative view. | |

Property Franchise (LON:TPFG) (£304m | SR83) | Continues to trade in line with the Board's expectations. Renters' Rights Act in May 2026 creates a meaningful opportunity for professionally managed operators such as TPFG. “The Board remains confident in the Group's long-term positioning and its ability to deliver on strategic opportunities, whilst continuing to adopt a measured and disciplined approach in light of the broader macroeconomic environment.” | GREEN = (Graham)

This has performed well since my last review , so it's a little more expensive now. The ValueRank of 50 doesn’t see a compelling opportunity. Despite this, I’m going to leave our GREEN stance unchanged. After all, this is a quality, capital-light business with a faultless financial performance and that recently upgraded expectations. As I think a positive re-rating is possible from current levels, I’m happy to stay the course. | |

Pulsar Helium (LON:PLSR) (£150m | SR27) | Minnesota's new helium-specific rulemaking guidelines create a clearer pathway toward responsible helium production at Pulsar's flagship Topaz Project. | ||

GreenX Metals (LON:GRX) (£141m | SR9) | Exploration Target demonstrates potential for globally significant copper endowment at Tannenberg Copper Project, Germany. | ||

Roadside Real Estate (LON:ROAD) (£110m | SR19) | Delayed completion of the acquisition of DAR to the end of June due to the death of the major shareholder of the target. | ||

DP Poland (LON:DPP) (£70.8m | SR20) | Revenue +15% to £61.7m, Adj. EBITDA +29% to £6.2m (Pre-IFRS16 EBITDA £2.6m), Loss £4.3m (FY24: 0.5m loss) mainly due to increased impairment charges. Net cash (excl. leases) £.1.4m (FY24: £10.7m) after £5.8m acquisition. “expect double-digit system sales growth in 2026”. | ||

Ultimate Products (LON:ULTP) (£44m | SR93) | Q3 Revenue £34.8m flat on last year. Branded sales +3%. Currently expects the flat trading trends seen in Q3 to continue throughout the balance of the year, which would be slightly ahead of expectations. Profitability remaining in line with consensus, reflecting the change in sales mix. | AMBER ↑ (Mark) A lot has happened since we last reviewed this company following a series of profits warnings. In light of this, guidance for a small FY sales beat is well-received, even if the sales mix means that profitability stays the same. Also well-received by shareholders was the recent announcement of a new CEO, who comes from a much larger company. However, I’m not convinced that this in itself marks a turnaround in prospects, especially as the two previously key people are moved to non-exec positions. Still, with several in-line statements in a row now building confidence that forecasts are achievable, despite a difficult consumer backdrop, I feel we should take a more neutral stance. | |

MicroSalt (LON:SALT) (£26.9m | SR2) | Revenue +180% to $2.1m, Net Loss $3.2m (FY24: $5.8m), Net Debt $0.96m (FY24: £$2.49m) after £5.7m fundraise in period. Outlook: updating FY26 sales guidance to US$4.5m, (down from $7.0m guided in January) due to production timing associated with the 2027 launch schedule. | BLACK (RED) (Graham) [no section below] This company says that it can improve the flavour of salt, meaning that less consumption is required for the same effect. We’ve been RED on it and I believe that we should remain so after these full-year results. Recall that there was a 2025 revenue warning last August, when I listed seven reasons for caution. Looking back on those reasons today, one change has been the introduction of financial forecasts from the Nomad, Zeus. These forecasts get slashed today with 2026 revenues cut by 36% to £4.5m, and a larger loss is now expected. The company says that the downgrade is purely due to production timing issues, and is not demand-related. Meanwhile, it finished 2025 with a cash balance of $1.9m after raising $5.7m in new equity. While I do think that this story could get exciting as they gain traction, the risk of another equity raise keeps me on the sidelines and in the RED. | |

Skinbiotherapeutics (LON:SBTX) (£25.3m | SR-) | Investigation into, inter alia, the financial statements for the year ended 30 June 2025 is complete, but interims slightly delayed. Investigation findings and actions to be published with interims. Appointed Saffrey LLP as the Company's independent auditor. | ||

Touchstone Exploration (TSE:TXP) (£23.6m | SR69) | The FR-1835 and FR-1836 development wells on the WD-8 block were successfully completed and placed on production in mid-May 2026, averaging 175 bopd, in line with expectations. | ||

Petro Matad (LON:MATD) (£23m | SR15) | Production from Heron-1 and Gazelle-1 continues in line with forecasts (126 + 123 bopd, respectively.) | ||

Great Western Mining (LON:GWMO) (£17.3m | SR27) | Option Agreement signed with global copper producer KGHM whereby KGHM may earn a 100% interest through staged payments and a minimum exploration commitment of US$5m over 6 years. | ||

Prospex Energy (LON:PXEN) (£13.7m | SR21) | Loss £2.8m (2024:£46k loss) after £2.5m investment write-down. 31 Dec: Cash £39k after £1.2m placing. £2m CLN raised post-period-end. | ||

FIRST CLASS METALS (LON:FCM) (£10.7m | SR11) | Has completed the final cash payment and has now secured 100% ownership of the Kerrs Gold Project in northeastern Ontario | ||

GreenRoc Strategic Materials (LON:GROC) (£10.6m | SR35) | Mobilisation of drill contractors and Company personnel is scheduled for the second half of June 2026. |

Graham's Section

PPHE Hotel (LON:PPH)

Up 25% to £20.10 (£841m) - Update on Strategic Review and Formal Sale Process - Graham - TAKEOVER

We had an RNS from PPHE last night, at 5.10pm, and there is another this morning at 7am.

Last night’s announcement:

Following the announcement on 21 November regarding the commencement of the Strategic Review and Formal Sale Process… the Board of PPH… announces that it has received an indicative proposal from Fattal Hotel Group… regarding a possible cash offer for the Company at a price of £22 per share.

Importantly, “the Board, together with its Rule 3 adviser, has evaluated the Proposal and determined that the Proposal represents fair value.”

The Board intends to engage with the Company's major shareholders regarding the Proposal in order to assess its deliverability

This morning’s announcement from Fattal

Some background: Fattal is Israel's largest hotel group and it already owns 4% of PPHE.

Fattal says:

“As part of the Proposal, the Company announced that it is interested in discussing with the Board of Directors of PPHE and its representatives potential structures for such transaction. The Company announced it is willing to maintain the proposal for a limited period to allow for a constructive engagement with PPHE Board and its advisors, with a view towards announcing a firm offer within the next 4 weeks.”

The reference to “potential structures” presumably refers to the potential for a scheme of arrangement, takeover offer, etc, and not to the potential for any non-cash elements to be introduced. The proposal itself is pretty clear: £22 in cash for each PPHE share.

Premium: £22 is a 36.5% premium to last night’s close.

It’s also a 47% premium to the share price last November, when we learned that the Founder (owning 33%) and President/Co-CEO (owning 11%) were intending to hold meetings to discuss various options, that could include “a potential partial monetisation of their stakes in PPHE”. A formal sale process involving the entire PLC board started shortly thereafter.

Graham’s view

I treat real estate takeovers differently. For a normal business, I expect at least a 25-30% premium against the prevailing share price. That has been achieved here. But in real estate, I mostly think about the premium/discount to asset value that has been achieved.

And against PPHE's official asset value, this offer does not appear all that generous: it’s a 20% discount to the company's December 2025 EPRA NRV (real estate's equivalent to NAV).

That NAV figure was £27.40 per share.

Moreover, the Board of PPHE are now on record saying that £22 represents fair value, which further undermines the notion that the shares were worth £27.40.

On the other hand, it could be argued that nobody believed that figure anyway. if you go back to last November, the share price was trading at a discount of ~50%. This, in hindsight, was too extreme.

If we measure the offer against earnings, it looks better. PPHE has earned 125p of EPRA (real estate) adjusted earnings per share in each of the last two financial years. £22 is a multiple of nearly 18x against that. Forecasts suggest it will earn 111p of EPS in 2026 and then 127p in 2027.

The proposed buyer is credible and makes sense given the Israeli connections at PPHE. I would assume the takeover has a strong likelihood of going ahead.

The lesson, if there is one, is to not have blind faith in real estate NRVs - but also to get interested when there is a 50% discount and a clear catalyst. In this case, the catalyst came in the form of major shareholders looking for an exit. Congratulations to everyoneone who has made money out of this share.

Property Franchise (LON:TPFG)

Unch. at 478p (£305m) - AGM Trading Update - Graham - GREEN =

I went GREEN on this in March, at 434.6p, thinking that an earnings multiple of 10x might not be a bad entry point. Earnings forecasts had just been upgraded, and I’ve been a long-term fan of this business.

Today’s AGM statement is in line:

TPFG continues to trade in line with the Board's expectations, with the Group benefiting from a resilient, highly cash generative business model underpinned by substantial recurring revenues across both its franchise and licensing divisions. This strong level of recurring income provides good visibility over future earnings and helps mitigate the impact of shorter-term cyclical movements in the housing market.

A few other points made in the statement:

The Renters' Rights Act came into effect this month and will increase the burden on self-managed landlords, thereby creating an opportunity for operators such as TPFG. They are “already seeing encouraging levels of enquiries from self-managed landlords seeking support with compliance and property management”.

Two investments were made this year (the acquisition of a mortgage broker and the purchase of a 25% stake in the parent company of Legal & General Surveying Services. These represent “strategic progress” against TPFG’s “platform development strategy”.

Estimates

No change to forecasts at Cavendish today:

2026 revenue £91.4m, adj. EPS 42.3p

2027 revenue £96.4m, adj. EPS 45.6p

2028 revenue £100.8m, adj. EPS 48.4p

The forecast earnings multiple is now 11.3x for 2026, falling to 10.5x for 2027.

Graham’s view

This has performed well since my last review , so it's a little more expensive now.

The ValueRank of 50 doesn’t see a compelling opportunity:

Despite this, I’m going to leave our GREEN stance unchanged. After all, this is a quality, capital-light business with a faultless financial performance and that recently upgraded expectations.

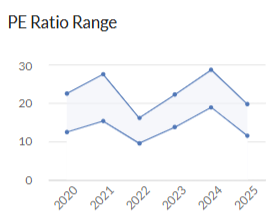

Here’s a chart of the historical earnings multiple range, most of this being prior to the Belvoir merger in 2024. It has achieved a much higher rating from time to time:

As I think a positive re-rating is possible from current levels, I’m happy to stay the course.

Mark's Section

Ultimate Products (LON:ULTP)

Up 2% at 51p (£44m) - Q3 2026 Trading Update - Mark - AMBER ↑

Here’s the headline:

Unaudited Group revenues during Q3 were £34.8m, in line with the prior year (£34.8m), reflecting continued subdued consumer demand for general merchandise and the planned reduction in non-core third-party clearance sales.

Flat sales in an inflationary environment doesn’t sound great. However, given that H1 sales were down 6.3%, this is a modest recovery. For the full year, they say:

Notwithstanding the subdued macroeconomic backdrop and the unpredictable geopolitical environment, the Board currently expects the flat trading trends seen in Q3 to continue throughout the balance of the year. This means that, while the general merchandise market remains soft, particularly in the UK, Group sales are expected to be marginally ahead of market expectations, with profitability remaining in line with consensus, reflecting the change in sales mix.

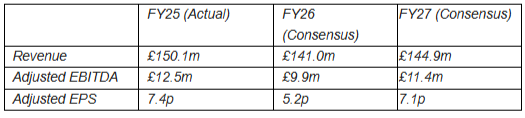

25H1 revenue was £79.5m, and the FY £150.1, so if 25Q3 was £34.8m then 25Q4 was £35.8m. If they do the same in 26Q4 then we get £145m, compared to the previous consensus:

Unusually for such a small company they have four brokers, who have all done similar maths and come up with similar results. All the brokers have increased their FY27 sales estimates by a similar amount to the FY26 increase, but kept EPS forecasts the same. Sales mix is blamed for the difference. To understand this I think we need to delve into the recent management history.

History:

There’s been quite a lot going on behind the scenes since we last reviewed this on the DSMR. Cavendish helpfully summarises this in their latest note:

Earlier this week Ultimate Products announced the appointment of a new CEO, Simon Harrison. Simon is currently the CEO of Princes Group PLC (LSE: PRN), the international food and drink company, and he will join Ultimate Products as CEO designate on 5 September 2026 before replacing Andrew Gossage on 26 October 2026. After a short sabbatical, Andrew will continue as a non-executive director from 1 May 2027. Simon Showman will also move to a NED role with effect from 1 June 2026, while continuing as President and Founder. In February 2024 Andrew moved to CEO from MD while Simon Showman moved from CEO to Chief Commercial Officer. In August 2024, Simon moved to the role of President and Founder and the operating board was restructured, with five management changes announced, to allow the team to play to their strengths.

It won’t have escaped investors attention that even prior to these management changes, it was Andy Gossage who almost always presented the company to investors. The history of the company was as a third-party clearance business. It is widely thought that founder, Simon Showman, was the key figure in sourcing this stock. This part of the business has always been profitable, but very variable, and not really able to grow consistently. So as a listed company looking to scale, it makes sense for this part to shrink, and Showman’s role in the business with it. With the company increasingly moving towards branded products, and clearance described as non-core, it made sense that Gossage took the CEO title.

However, things have not worked out well during that period. In February 2024, the share price was 150p, today it is around 50p. A series of profits warnings meant that FY26 EPS dropped by 70%:

When you consider that the company also has net debt, the share price managed to drop by over 60% and still became more expensive during this time.

I don’t think this is entirely Gossage’s fault. These have been difficult consumer markets in their key geographies, and this sort of business with typically single digit operating margins is very sensitive to changes in sales.

They also benefited significantly from the boom in air fryer sales in 2022, as rising energy costs and inflation drove consumers to seek cost-effective cooking alternatives. Management didn’t foresee the impact a reversion to more normal air fryer sales would have, though, as they kept buying back shares at levels that now look very elevated. [Although it is possible that a post-IPO Management Incentive Plan (now expired) that would have seen them awarded 6.25% of the company if they got the share price above a certain level may have contributed to that enthusiasm!]

New CEO

The recent bounce in the share price has been due to the announcement of a new CEO. This seems slightly harsh on Gossage, but perhaps the larger shareholders made it clear that something had to change. The new appointment is a relatively big-hitter:

Simon is currently the CEO of Princes Group PLC (LSE: PRN), the FTSE 250 international food and drink company

For a CEO to leave a £500m market cap company for a £44m market company means he must see a lot of potential. However, there are a couple of potential pitfalls:

He doesn’t appear to have direct experience of branded sales of the types of products Ultimate produce. Going from a company with £2bn turnover and 7k+ employees to a much smaller business can be a culture shock.

His salary at Princes was £500k. While Showman and Gossage were not badly paid on £300-400k each base salary, if the company matched his current package, this could add to costs. (They could offset these costs by halving the number of brokers that cover the company, though!)

Incoming CEO’s tend to do a thorough review of prospects and re-base targets. There may be a final “kitchen-sinking” to come.

Valuation:

All of the brokers are keen to point out the low valuation, perhaps keen to be the ones to avoid a possible upcoming broker cull! For example, Cavendish say:

Our 85p target price remains based on 9.4x EV/EBITDA and 3.0% FCF yield (adj.) for FY26E. The 5.5% FY26E dividend yield is attractive.

Certainly if one is confident of them hitting FY27 forecasts, this is looking good value:

However, we can’t completely ignore the debt, which is forecast to be around £14m at year end, and Cavendish’s price target of 9.4x EV/EBITDA looks punchy to me. After all, this is a relatively low margin business, which designs and distributes Chinese-made goods, with a very volatile performance, as products go in and out of fashion. Apart from occasional periods of irrational exuberance, this has never been a highly rated stock. And while that exuberance may return, I’m not sure anyone should be investing on that basis.

Mark’s view

Last time we reviewed the company on the DSMR it was after one of the profit warnings and we rated it AMBER/RED. We were right to be cautious, as the share price declined pretty much constantly since then:

I’m not sure simply appointing a new CEO, even one from a much larger company, suddenly changes the prospects here. There is much to prove, including whether he chooses to “kitchen-sink” the numbers, or completely exit the clearance part of the business, when he finally gets his feet under the table. However, they have now had a few in-line statements in a row and they appear to be weathering the poor consumer backdrop well (or at least slashed forecasts enough that this is now the baseline). At this stage, I think a more neutral view of AMBER would be more appropriate.

Iqe (LON:IQE)

Down 6% at 47.7p (£467m) - FY 2025 Financial Results - Mark - RED =

IQE is a fascinating stock. A British tech company operating in the global semiconductor industry. Perhaps today’s results are best-placed to be understood in the context of some history.

A long, long time ago….

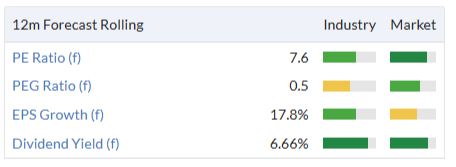

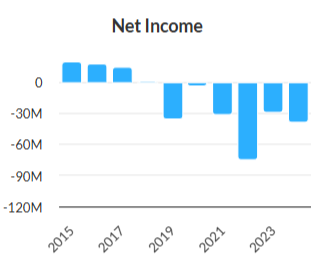

I have bittersweet memories of investing in IQE in the past. It was a decade ago, the share price was 18p, the market cap was £125m and the metrics looked like this:

I actually ummed and aahed for quite some time before investing. The reason being that the global semiconductor business is highly cyclical, and it was certainly very possible that I was buying into a value trap. So it was with great delight that I sold less than a year later having trebled my money. The smug look was quickly wiped off my face as the shares continued to 3x again, peaking at around 150p.

The story that generated such great excitement at the time was that Apple were using IQE’s products. The company was quick to take advantage of the sudden exuberance for their equity and raised fresh capital. This mostly marked the peak in the share price, and the company fell into losses for close to the next decade, raising more money along the way to keep them going:

Perhaps rarely has a UK share promised so much but delivered so little.

Bring us up to date…

Fast forward a decade, and their Interim Results to 30th June 2025, showed that they needed covenant waivers:

The Directors remain in discussion with the Group's bankers, HSBC Bank plc, to secure the banks continuing support for the Group and have obtained formal waiver of the 30 September 2025 minimum EBITDA financial covenant test.

The going concern statement revealed that if they grew revenue by 31% yoy in 2026, they will still breach their liquidity covenant and that as things stood, both the sale of IQE Taiwan sale and continued forbearance from HSBC was required to keep them going:

Whilst the Directors are confident that the divestment of either the whole Group or IQE Taiwan is progressing as planned and will realise sufficient cash, they acknowledge that either a decision by HSBC Bank plc to withdraw its on-going support of the Group, or a delayed outcome of the potential sale of the whole Group or IQE Taiwan could impact the availability of sufficient funding for the Group's needs in the going concern period from 31 December 2025 onwards.

In light of this, it is perhaps unsurprising that the shares bottomed at less than 5p, giving a market cap of less than £50m. They say that history doesn’t repeat itself, but does rhyme, so perhaps I should have been less surprised that a sudden interest in the idea of photonics being used in AI data centres and space applications led to the shares in the close to insolvent business being bid up as high as 70p for a £700m market cap.

At this point, the management did what any business finding itself with net debt at 10x Adj. EBITDA, and a soaring share price would do and conducted a large equity raise. The price was at a 58% discount:

The Issue Price represents a discount of approximately 10.1% to the 12 month VWAP ending on 24 April 2026, being the latest practicable date prior to the publication of this announcement, and a discount of approximately 58.4% to the closing mid-market price of 47.6 pence per Ordinary Share on 24 April 2026, being the latest practicable date prior to the publication of this announcement.

Strangely the scale of the discount doesn’t appear to have dampened enthusiasm for the stock. One of the possible reasons for optimism is that MACOM Technology Solutions contributed £30 million in equity and £15 million in convertible loan notes, giving them a 11.5% stake as part of the placing. MACOM and IQE work together on epitaxial services across multiple compound semiconductor technologies. Under their partnership and long-term supply agreements, IQE acts as a critical foundry supplier, manufacturing advanced wafer materials that MACOM uses to build hardware for the AI data centre, telecommunications, and aerospace/defence markets. While this may be a vote of confidence in IQE, given that MACOM have a $22.7bn market cap, they may well have seen this as a price to pay to keep their supply agreements in place.

FY25 Results

After all the context, it is again unsurprising that we have some pretty poor results:

The Photonics part of the business that the market is currently excited about, is doing ok, growing by 15% but more than offset by a large decline in Wireless:

Wireless revenue of £40.1m (FY 2024: £67.3m) decreased 40% year-on-year reflecting uncertain macroeconomic conditions in the first half of the year and softness in mobile handset demand with some end customer requirements met from existing inventory.

Outlook:

This is the key line:

Revenue for FY 2026 is expected to exceed 20% growth year-on-year, with strong order book visibility into H2. This is expected to result in a high-single digit to low double-digit adjusted EBITDA position.

+20% revenue gives £117m, roughly where they were in 2024. The EBITDA margin sounds a lot like 10%, so that’s about £11.7m EBITDA. Up nicely on both FY24 and FY25. However, there has typically been around £30m between Adj. EBITDA and Adjusted Profits, so this is likely to remain heavily loss making.

Valuation:

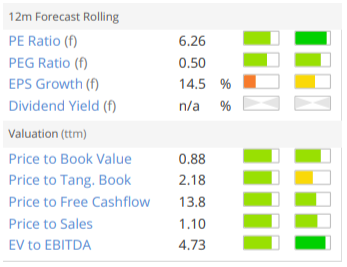

I can’t see Peel Hunt’s forecasts, nor any update from Panmure Liberum, so it is hard to make assumptions about future years. After all, this is a highly cyclical industry, where trends are difficult to forecast. Using my FY26 forecast numbers, and assuming EBITDA is an appropriate measure for a capital intensive business, we have £11.7m EBITDA and a current market cap of around £650m post dilution. Net cash is around £11m, giving an EV of roughly £639m and a valuation metric of roughly 55x EV/EBITDA.

Frankly, this seems bonkers to me. To be fair, it doesn’t seem out of place to some of the US-listed AI data centre plays. However, those companies don’t come with decades of failure to profitably exploit their technology.

Mark’s view

Perhaps I’m jaded, given my history with the company and this time really is different. However, the company’s track record of losses give little confidence that the current enthusiasm for the stock will not be dashed on the rocks of cyclical reality in a few years time. The recent raise may solve the going concern issues for the moment, and the support of MACOM suggests that their partnerships are real and valuable to them. However, that doesn’t mean that there is an obvious pathway for IQE to grow into its current valuation, and as such I think we have to keep our negative RED view.

Investors who are excited about the positive impact that AI data centres will have on global semiconductor volumes and pricing can invest in Taiwan Semiconductor Manufacturing Co (NYQ:TSM) or GLOBALFOUNDRIES (NSQ:GFS) for less than half the valuation.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.