On Friday afternoon, President Trump said he was making a “final determination” on a deal with Iran. Unfortunately, we did not get a clear resolution with Iran and the US said to be exchanging messages over the weekend on changes to the proposed agreement.

Iran wants “exclusive authority to determine the nature of transiting vessels” in the Strait of Hormuz, according to Iranian TV quoted by Bloomberg.

The proposed deal does allow $12 billion of frozen funds to be returned to Iranian banks within 60 days - that’s half of the total frozen amount.

Other major headlines:

The Israeli military has advanced deeper into Lebanon than it has for 26 years, planting its flag on the landmark Beaufort Castle.

In tech news, Nvidia is going to directly compete with Intel in the PC market, launching a new “RTX Spark Superchip” for laptops and desktops.

Overnight market movements:

The FTSE is set to open down 0.2% at 10,380

S&P 500 is up 0.3% at 7,600

Brent crude (August delivery) is up 2% at $93.30

Gold is down 0.5% at $4,500

Bitcoin is down 0.6% at $73,250

Today's Agenda is complete. Spreadsheet accompanying this report: link.

Companies Reporting

Endeavour Mining (LON:EDV) (£11.3bn | SR86) | A contractor passed away on 29 May following a heavy mining equipment incident that occurred during water drainage activities. An investigation is underway but processing operations continue uninterrupted. | ||

easyJet (LON:EZJ) (£3.0bn | SR44) | Further Statement re Possible Offer & Response to Possible Offer for easyJet | Castlelake confirms it is in the early stages of considering an offer for easyJet and reports that it currently holds 2.14% of EZJ stock. easyJet reports that it has not yet had any dialogue or received any proposal from Castelake and notes “the highly opportunistic timing”. | TAKEOVER (AMBER/GREEN=) (Graham) |

Pan African Resources (LON:PAF) (£2.8bn | SR71) | Gold production +40% to c.275koz, at the lower end of FY26 guidance of 275-292koz. Expect to meet FY AISC guidance of $1,870/oz, ended the year with a net cash position. FY27 production guidance of 280-302koz w/ AISC of $2,075-2,175/oz. | AMBER = (Roland) While today’s update indicates that Pan African’s performance should be within the range of guidance provided for FY26, the combination of production being at the bottom end of guidance and costs at the top end suggests to me that profits may be slightly lower than hoped for. A further double-digit increase in costs in FY27 seems likely to outweigh a smaller rise in production, suggesting to me that earnings may not improve next year unless the gold price springs back into action. Pan African’s management has done a good job of building a larger business while profiting from the bold boom. But at current levels I think the shares are effectively a play on the price of gold and thus quite speculative, so I’m leaving my neutral view unchanged. | |

Sirius Real Estate (LON:SRE) (£1.56bn | SR68) | Pre-tax profit +4.9% to €211.4m, with like-for-like annualised rent roll +6.4% to €224.2m. EPRA EPS -7.8% due to forex headwinds and finance fees. Adjusted NAVps +5% to 124.78c. Outlook: trading in line with expectations. | ||

Hunting (LON:HTG) (£712m | SR91) | Jim Johnson will retire by mid-2027. He has been with the group since 1992 and has been CEO since 2017. | ||

Applied Nutrition (LON:APN) (£609m | SR50) | SP +7% Strong trading so far this year. FY26 expectations upgraded. Revenue now expected to be c.£148m with EBITDA margin in line with current expectations. (revenue previously £140.3m, EBITDA margin 28.2%). Reports acquisition of “trade and majority of assets of Nutrablend Group” for $16m. Nutrablend is a US-based sports nutrition manufacturer. | GREEN = (Graham) We turned fully positive on this in March at the interim results, which had an in-line outlook statement despite very strong trading in H1. At the time I suggested that H2 might positively surprise - an H1 weighting is a little unusual - and we now have an upgrade to the full-year outlook for FY July 2026. Revenue is thought to be c. 5% better than expected, before any contribution from the $16m (£12m) acquisition in New York, which "will have the same vertically integrated model as the UK business". This RNS additionally includes news of a licensing agreement with Mondelez to manufacture Sour Patch Kids/Swedish Fish branded products for the US and Canada, to be stocked in 2,200 Walmart stores and 1,300 GNC stores. It's an excellent RNS from every angle and I'm glad to stay positive on this one - a sports supplements business that is truly delivering. EPS estimates at Panmure Liberum are raised 6% for 2026 (to 11.6p) and 8% for 2027 (12.8p). This is no bargain: it's trading at 20x next year's earnings. But I think it's right to stay positive while the good news continues to flow. | |

ME International (LON:MEGP) (£553m | SR75) | SP -25% H1 revenue +2%, but revenue softened in April, with Photo.ME -18% in April and Wash.ME revenue +3%, versus +17% in H1. France was particularly weak, which the Board believes relates to the Middle East conflict. Board now expects FY26 pre-tax profit of £69 to £74m | BLACK (AMBER ↓) (Roland) Shareholders have been hit with a profit warning this morning that’s sent the stock tumbling. I estimate today’s guidance could equate to a c.11% cut to FY26 EPS estimates, but we will have to wait for updated broker estimates to be sure. I continue to have a mostly positive view of this business, but there’s been a lack of consistency from this business over the last year. As I explain below, I wonder if succession issues also might be a factor. For now, I think a neutral view makes sense – the stock doesn’t look expensive by historical standards. | |

Bluefield Solar Income Fund (LON:BSIF) (£467m | SR52) | BSIF has agreed an all-cash offer from Drax (LON:DRX) for 92.574p per share (£548m), a premium of 28% to the closing price on 4 November 2025. Shareholders will also be entitled to a second interim dividend of 2.25p, taking the total value on offer to 94.824p per share. | TAKEOVER (Roland) [no section below] | |

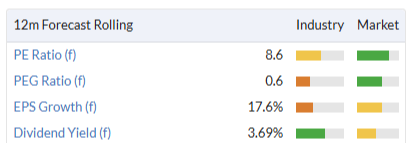

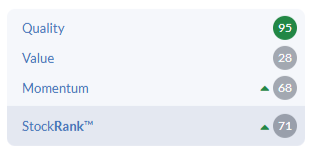

Cerillion (LON:CER) (£414m | SR39) | Revenue -14%, adj pre-tax profit -41% to £5.5m. Adj EPS -41% to 14.1p. New orders +102% to £39.6m, with new customer pipeline up 4% to £471m. “... well-positioned to deliver consensus market forecasts for the current financial year”. Broker forecasts unchanged: - PanLib FY26E adj EPS: 58.4p - Cavendish FY26E adj EPS: 60.2p | AMBER = (Roland) [no section below] Today’s full-year guidance from this telco software group is in line with expectations, but there’s clearly a deep divide between H1 adjusted earnings of 14.1p and full-year consensus of 58.8p. The company says this gap will be bridged in H1, aided by revenue recognition from the recent £42.5m Omantel win, presumably as high-margin software licensing revenue flows through. The StockRanks style this business as a Falling Star and I can see why – earnings growth has slowed, causing the stock to de-rate. Visibility also seems mixed to me and Cerillion’s multi-year contracts make for a relatively complex balance sheet, with substantial non-current receivables. None of this is really new though, and Cerillion has a good long-term track record and excellent quality metrics. I also agree with the company’s view (explained today) that its systems are unlikely to be displaced by AI-generated alternatives. The main question for me is over valuation. Consensus forecasts have edged lower over the last 18 months and the stock’s PEG ratio of 2.8 and ValueRank of 11 mirror my view that the shares are probably up with events. I’m going to stay neutral for now, but continue to see this as a high-quality business. | |

Avacta (LON:AVCT)(£362m | SR13) | Multiple confirmed partial and minor responses observed in patients with SGC. Continuing very good safety profile, with removal of the lifetime maximum doxorubicin limit based on highly favorable cardiac safety. | ||

Social Housing REIT (LON:SOHO) (£286m | SR67) | Targeting dividend of 5.79p per share for 2026, a 3% increase on 2025. Has declared a Q1 interim dividend of 1.4475p per share. Also secured a new £30m floating rate debt facility with Barclays. | ||

Invinity Energy Systems (LON:IES) (£199m | SR23) | 2025 revenue and grant income of £17.8m (2024: £5.2m), with a pre-tax loss of £24.1m (2024: £(22.8)m). Year-end net cash of £28.8m. 2025 sales of 31.4 MWh and shipments of 24.9 MWh. Has now secured a 2 MWh battery system sale to a US government-backed microgrid project. | ||

Redcentric (LON:RCN) (£199m | SR60) | FY26 revenue from continuing operations -2%, recurring revenue c.88%. Adj EBITDA for the MSP business totalled c.£17.5m. This was ahead of expectations for £17.2m thanks to strong H2 trading and cost control. Net cash position of £78m following sale of data centre business in April. | ||

Mkango Resources (LON:MKA) (£184m | SR12) | Q1 2026 pre-tax profit of $52.5k (Q1 25: $2.5m loss). | ||

Arbuthnot Banking (LON:ARBB) (£135m | SR54) | Admitting existing non-voting shares to AIM with the ticker ARBN. (They are currently traded on AQSE). | ||

EnSilica (LON:ENSI) (£133m | SR50) | New 7yr manufacturing and supply contract to produce an ARM-based sensing chip for a German manufacturer of automotive components. Expected to generate c.$75m of revenue over seven years, with c.$4m expected in FY27. | ||

Brave Bison (LON:BBSN) (£92m | SR37) | “...Subject to a minimum share price hurdle of 150p, the Executives may earn up to 12% of value created for shareholders above an annual indexation of 8% per annum and subject to limits and caps…” | ||

Tpximpact Holdings (LON:TPX) (£50m | SR89) | £16 million, 2-year contract with the Ministry of Justice following a competitive tender process. The contract will support transformation programmes in the Legal Aid Agency and other service transformation programmes. | ||

Cobra Resources (LON:COBR) (£48m | SR12) | Fully funded diamond drilling programme comprising up to six drillholes for approximately 1,800m. | ||

Victoria (LON:VCP) (£43m | SR30) | CEO will step down on 30th June but remain a director of the Australian business and chairman of the UK flooring division. | ||

Rentguarantor Holdings (LON:RGG) (£41m | SR9) | Revenue +155% for the five-month period to May 2026. “...The Board expects similar levels of revenue performance to continue [H2], which would result in revenue for [FY26] being materially above market expectations.” “The Board currently expects for the Group's operating result for FY 2026 to be within the market expectations range for the period.” | AMBER/GREEN ↑ (Graham) It’s very unlike me, but I’m going to tentatively turn AMBER/GREEN on this. It goes against all of my value instincts. But we don’t often get to see companies more than doubling their revenues. This rent guarantee product appears to be gaining traction and to be very well-matched to the new regulatory regime, which in general makes tenancies riskier. There is a real logic behind the explosive growth that it’s achieving. | |

Zenith Energy (LON:ZEN) (£32m | SR43) | Revenue CAD $2.3m (FY25: $2.1m). Operating loss $13.7m (FY25: $6.4m). The continued expansion of the Company's solar development portfolio, the proposed spin-out of its uranium exploration business through Reveille Resources Plc, and the advancement of the ICSID arbitration proceedings, in which the Group's wholly owned subsidiaries are pursuing claims quantified at approximately US$572.65 million, each represent significant potential value drivers. | ||

Checkit (LON:CKT) (£27m | SR40) | The Board has appointed EC M&A as Joint Financial Adviser to manage discussions with interested parties. EC is a US headquartered M&A adviser. | ||

Zinc Media (LON:ZIN) (£15m | SR21) | £3m facility with Lloyds Bank. Option, subject to lender approval, to increase facility by £2m. Has also secured a further £1m of new business since the 21st May update. | ||

Block Energy (LON:BLOE) (£15m | SR22) | Revenue $6.1m (2024: $7.5m). Total operating loss $2.3m (2024: $0.2m loss). “The 2025 financial result reflects a materially lower oil price environment… With commodity prices materially stronger than the 2025 average, our focus in 2026 is execution: converting partnerships, assets and technical milestones into visible operational progress and shareholder value." | ||

Eco Buildings (LON:ECOB) (£15m | SR5) | Eco Buildings to establish Eco Buildings United Kingdom Ltd targeting the UK housing market. Expecting to target housing associations and others seeking economically viable housing. | ||

Medpal AI (LON:MPAL) (£10m | SR1) | 42,250 prescription items dispensed in May 2026, the best-performing month since pharmacy operations commenced. | ||

LPA (LON:LPA) (£9m | SR83) | Revenue £13.8m (H1 2025: £9.5m). PBT £0.4m (H1 2025: £0.5m loss). Expects to deliver full-year results in line with current market expectations. | ||

Safestay (LON:SSTY) (£8m | SR49) | SSTY has exchanged conditional contracts for the sale of its freehold property, Safestay Glasgow Charing Cross. SSTY will no longer operate the hostel and it will not trade under the Safestay brand. |

Graham's Section

easyJet (LON:EZJ)

Up 9.5% to 435.8p (£3.3bn) - Response to Possible Offer for easyJet - Graham - TAKEOVER (AMBER/GREEN =)

On Friday, a US-based private equity investor called Castlelake, specialising in “asset-rich and cash-flowing opportunities in the private markets”, announced on its website that it was “in the early stages of considering a possible offer” for easyJet.

It acknowledged that it had not yet spoken with the easyJet Board.

That announcement went up as an RNS this morning.

This morning, they also announced that they and their funds now own 2.1% of the company.

Response to Possible Offer for easyJet: the Board of easyJet have been quick to respond.

The Board is clear in its duty of aiming to maximise shareholder value and will consider any proposal, should one be made. In any assessment, the Board will be especially mindful of its valuation and deliverability.

Valuation: the Board notes the highly opportunistic timing when easyJet’s share price is temporarily depressed due to the current situation in the Middle East and its impact on customer confidence and jet fuel prices.

Deliverability: the Board notes the considerable regulatory, financial and other execution challenges associated with a potential takeover of easyJet.

They also note their “investment grade balance sheet with a net cash position”, suggesting that they are under no financial pressure to agree to any takeover.

Graham’s view

On valuation, it's true that EZJ shares have had a rough year, underperforming the FTSE:

The Financial Times published a helpful article on Saturday, providing lots of context to the story.

A few nuggets from that:

Castlelake is profiting handsomely from a 2023 investment in the distressed Scandinavian Airlines (SAS), where it is now being bought out by Air France-KLM.

An experienced investor in the aviation sector, Castlelake is said to currently own some of easyJet’s aircraft leases.

Analysts believe that easyJet’s fleet is worth more than its market cap.

So it all adds up: Castlelake has an intimate understanding of easyJet’s fleet, and may see an opportunity that mirrors its SAS investment.

We don’t cover easyJet very often in this report, but here are a few observations I’d make from the interim results published 11 days ago:

- Net cash was £434m, calculated as cash of £3.4bn minus borrowings of £2.0bn and leases of £1bn.

- The fleet included 356 aircraft, average age 11 years, with 208 aircraft owned.

- Net assets on the balance sheet, excluding intangibles, were £2.9bn. easyJet's market cap as of Friday's close was £3bn.

So the company does appear to have a position of strength, in balance sheet terms, and its balance sheet is valued cheaply by the market.

Earnings are less impressive: the H1 headline loss was £552m, worse than H1 last year, despite a good load factor of 90%.

And the outlook statement said “there remains uncertainty over the FY26 financial outturn due to the current external environment with fuel prices remaining elevated and lower than normal visibility of forward bookings.”

Where I think the easyJet Board’s response to Castlelake is strongest is on the regulatory point: any takeover would face an enormous quantity of red tape. Even in a post-Brexit world, it’s very difficult - maybe impossible? - for a non-EU entity to buy a UK airline outright.

I’m therefore leaning towards the conclusion that a takeover by Castlelake alone is very unlikely. Castlelake themselves probably know this, but see enough value in the shares to make an investment worthwhile. Their purchase of a 2% stake looks more like a value investment to me, rather than a serious takeover attempt. They may also believe that their presence could trigger other parties to consider a takeover.

I’m therefore going to leave our AMBER/GREEN stance unchanged. The asset value at easyJet is interesting, but the market is right to be sceptical of the £1bn PBT target, which doesn’t seem to be on the horizon yet.

Rentguarantor Holdings (LON:RGG)

Up 12% at 32p (£47m) - Trading Update and Strategic Growth Opportunities - Graham - AMBER/GREEN ↑

I turned neutral on this one in April on the grounds that the company was “growing very rapidly, beating expectations, possibly turning a small profit, and holding a reasonable amount of cash”.

The share price is up by 37% since then, making the valuation on historic financials even more stretching. The ValueRank is only 4, and Stockopedia categorises it as a “Sucker Stock”:

Let’s review today’s trading update for the first five months of the year.

Revenue +155% to c. £2m

No. of applications +82% to 6,288

No. of contracts + 127% to 2,318 (with higher average contract value).

We already knew that Q1 revenues had doubled year-on-year, but this takes the growth to another level.

May saw another very sharp increase:

The Renters' Rights Act 2025 (the "Act") came into force on 1 May 2026. The Company has been anticipating the Act to cause a structural shift in demand for rent and property damage guarantees in the UK. In May 2026, the Group delivered record unaudited revenue of c.£700k during the month - a significant increase of approximately 115% compared to the average monthly revenue of c.£325k during the first four months of the year. This was driven by a material uplift in new guarantee issuances and higher adoption of the Company's solutions across core customer segments within the private rental sector.

Estimates: The company’s statement says that the 2026 profit result will be “within the market expectations range” as that range was quite wide (from a £0.5m operating loss to a £0.3m operating profit).

Looking at Cavendish’s estimates in isolation, they have upgraded their revenue and profit forecasts today as follows.

Revenues:

2026 revenue forecast raised 25% to £6m

2027 revenue forecast raised 28% to £11m

2028 revenue forecast raised 28% to £18.8m.

Profits:

New 2026 PBT forecast £0.2m (previous forecast was a £0.5m loss)

2027 PBT forecast £2.3m (previously £1.1m)

2028 PBT forecast £5.9m (previously £3.9m)

CEO comment:

“The Company's performance in May 2026 marks a clear shift in demand for our professional guarantor service. The structural changes to the sector resulting from the Renters' Rights Act are driving sustained growth across our core customer segments and reinforcing the relevance of our solution.

"I am also pleased to have officially launched our expanded service Offering, now including the ability to settle property damages, which I believe is a critical step in positioning RentGuarantor as a comprehensive service that simplifies the core aspects of securing rental accommodation in the UK.”

AI investment: RGG is accelerating various automation and AI tools, to meet anticipated volumes.

AI deployment in existing systems and document processing tools

Targeted hiring in data science and engineering

Upgrading IT infrastructure.

One of their NEDs is spearheading this, a Professor of computer science.

Graham’s view

The use of AI is positive but also mandatory in the current environment for almost every business. Listed businesses in particular are expected to demonstrate that they are on top of this trend.

What makes RGG really interesting is its positioning in the property market - and its explosive growth.

I’m relieved that I already switched to neutral. But after a big upgrade, perhaps this is not even enough.

It’s very unlike me, but I’m going to tentatively turn AMBER/GREEN on this. It goes against all of my value instincts. But we don’t often get to see companies more than doubling their revenues. This rent guarantee product appears to be gaining traction and to be very well-matched to the new regulatory regime, which in general makes tenancies riskier. There is a real logic behind the explosive growth that it’s achieving.

Hitting 2028 forecasts won’t be easy. They would have to hit current 2026 revenue forecasts (£6m) and then treble revenues over the subsequent two years. But if that is realistic, then these shares will no longer appear to be so expensive. The 2028 forecasts suggest that 3.6p of earnings per share is possible.

This might be my worst call ever, but I’m going to turn moderately positive on RGG, to reflect the possibility that it will grow into its current valuation over the next few years. Because if it does that, then I do not expect the share price to stand still.

Roland's Section

ME International (LON:MEGP)

Down 25% at 110p (£412m) - Trading Update - Roland - BLACK (AMBER ↓)

Commiserations to holders here – shares in this quirky founder-led business are down by c.25% in early trading this morning following a big profit warning.

What’s gone wrong?

ME Group says that the impact of the Middle East conflict has hit consumer confidence and “reduced demand for official photo ID amid ongoing travel uncertainty”.

Although the majority of the group’s H1 (Nov-Apr) was in line with expectations, trading softened in April, particularly in the French photobooth and laundry operations.

Group-level revenue figures provided today suggest a sudden slowdown in April:

H1 group revenue: +2%

PHOTO.ME revenue -17% in April (H1: -6%)

WASH.ME revenue +3% in April (H1: +17%)

H1 revenue from equipment sales: -14%

The photobooth and laundry businesses generated 88% of revenue and 93% of operating profit last year, so are effectively the whole business.

Outlook

Management report “an improvement in trading through May” but do not expect trading patterns to normalise while the Middle East situation remains unresolved.

Profit guidance for the full year has been cut:

Consequently, the Board is taking a more cautious view to the full-year outlook, and it now expects FY 2026 profit before tax to be in the range of £69 million to £74 million.

Using last year’s results as a guide, my guesstimate is that this could give a revised adjusted EPS figure of c.14p, at the mid-point. Previous consensus on Stockopedia was for 15.7p, so this would be a cut of 11%.

Sadly, ME Group’s management hasn’t included details of previous expectations in today’s RNS. Broker notes for ME Group are also no longer available on Research Tree. This means we’ll have to wait for revised EPS estimates to filter through to Stockopedia in the coming days to see if my estimate is correct.

Roland’s view

On the face of it, today’s c.25% share price drop seems quite harsh, if my estimate of an 11% cut to EPS is broadly correct.

However, this is the second profit warning in six months.

A look at the bigger picture has also left me wondering if the management of this business has faltered slightly over the last year:

The publication of last year’s results was delayed to give the auditors more time, resulting in its shares being suspended – I think this is poor for a FTSE 250 company.

When the results were published, we then learned that ME Group had previously incorrectly accounted for the cash in its vending machines – surely a well-established procedure?

Family members involved in the management of the business have been reshuffled somewhat this year, with founder Serge Crasnianski’s son Vladimir promoted to Deputy CEO.

A professional chief operating officer was appointed in March, taking over the duties of the founder’s daughter.

I might be reading too much into these events, but founder-led businesses can sometimes have issues with management succession. Given that CEO Serge Crasninanski is 83, I think ME’s future leadership could be a factor investors might want to consider.

With this caveat aside, I think it’s fair to say that ME Group shares still look quite decent value following today’s warning. I estimate the forward P/E a c.8x, with a potential dividend yield of 6%-7%.

There’s also presumably some recovery potential if the Middle East conflict is resolved fairly soon.

In principle I think this remains a good, cheap business, but given the headwinds reported today and the lack of consistency from this business over the last six months, I think a more cautious view is prudent.

I’m going to downgrade our view to neutral today, to reflect this profit warning and my more mixed view on this business.

Pan African Resources (LON:PAF)

Down 11% at 122p (£2.5bn) - Operational Update ahead of year ending 30 June 2026 - Roland - AMBER =

Today’s full-year update from South African gold miner Pan African seems a little disappointing to me. The market clearly agrees – the shares are down by c.11% as I write.

FY26 update (y/e 30 June 2026)

Today’s update which shows costs at the top end of guidance but production at the bottom end:

FY26 gold production to be c.275,000oz, at the lower end of FY26 guidance of 275-292koz.

FY26 All-In Sustaining Costs (AISC) to be $1,870/oz, at the top end of FY26 guidance for $1,820-$1,870/oz.

This leads me to expect that FY26 profits are likely to be at the lower end of expectations, perhaps slightly below consensus.

Lower production last year appears to relate to the ramp-up of production at Tennant Mines:

Excellent production performances from the Elikhulu Tailings Retreatment Plant (Elikhulu) and Mogale Tailings Retreatment (MTR) surface operations and the Evander and Barberton Mines underground operations offset slower than anticipated ramp up of production from Tennant Mines

Some of the other news in today’s update is more positive – the company confirm it has moved to a net cash position and has secured

FY27 Outlook

Output from Tennant is expected to “increase significantly” in FY27, but the overall impact on group production is only expected to be modest. Costs are also expected to continue rising:

FY27 production guidance of 280,000oz to 302,000oz, an increase of 6% at the mid-point.

FY27 AISC up 13.6% (midpoint) to between $2,075/oz and $2,175/oz.

FY27 capital expenditure revised upwards to $324m (+21% vs $267m previously).

The bulk of next year’s capex is aimed at expanding production and cutting AISC “over the next years”. Management says most of the increase is due to plans to expedite the development of the White Devil open pit and install a fixed crusher circuit and filter belt at the Nobles plant to support future production growth.

Pan African’s efforts to continue expanding production could pay off if the gold market remains strong – even at current levels the profit margins on offer look very attractive to me.

However, the risk is clear enough – the price of gold is falling, but spending is continuing to rise.

Consensus forecasts prior to today suggested earnings would continue to rise in FY27, despite these headwinds.

However, today’s guidance suggests to me that the earnings picture is now likely to be broadly flat next year – unfortunately I don’t have access to any broker notes:

Roland’s view

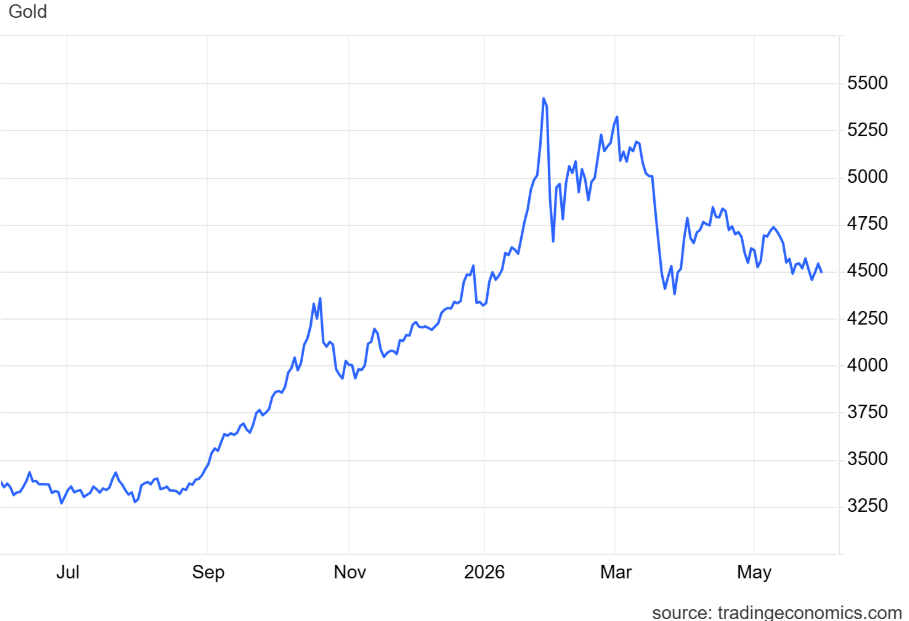

Personally, I can’t help feeling the gold bull market may have peaked. The gold price is down by 17% from the $5,420 high seen in late January and the chart suggests to me that recent lows could be tested if no further catalyst emerges:

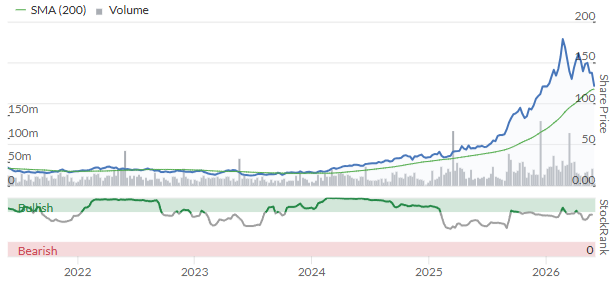

Miners tend to be a leveraged play on the underlying commodity and we can see this with Pan African. The company’s share price has fallen by 32% from the 180p high seen at the end of February – roughly double the decline in gold over the same period:

Taking a broader look, I think Pan African’s management deserves some credit for building a much larger business and timing their efforts to profit from the strongest gold market for many years. On a five-year view, this stock is still a five bagger:

I’m also pleased to see the business has now moved into a net cash position. Assuming this is maintained, it should help to de-risk the business if the gold price does continue to fall.

Looking ahead, my assumption is that the forward valuation of c.8x earnings remains largely unchanged. That seems about right to me.

The StockRank of 71 and High Flyer styling also suggest to me that further gains could be dependent on the price of gold, making the shares somewhat speculative in my view:

To reflect this situation, I’m going to leave my previous neutral view unchanged today. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.