SpaceX IPO price: Reuters has exclusively reported the price of the SpaceX IPO as $135 per share, with 555.6 million shares offered at a $1.8 trillion valuation.

For those who believe that the demand for AI stocks is running at highly speculative levels, not tied to the fundamentals, the market is providing a natural solution: supply.

A tidal wave of new shares is going to hit the market to soak up the demand:

SpaceX: $75 billion of new shares at a $1.8 trillion valuation

Anthropic (creator of Claude) has started on the paperwork for an IPO this Autumn. Its private market valuation is $965 billion, recently raising $65 billion at this level.

OpenAI (creator of ChatGPT) is already widely rumoured to be planning an IPO this year. Its private market valuation is $852 billion.

Alphabet is setting up for the biggest fundraise of all time, looking to raise $80 billion to build AI infrastructure.

My view is that if investors are willing to pay absurd prices for AI-related shares, then it makes sense for companies to supply the market with as many AI-related shares as possible.

In the words of Ed Seykota: Win or lose, everybody gets what they want out of the market.

Overnight market movements:

The FTSE is set to open unchanged at 10,370

S&P 500 is unchanged at 7,600

Brent crude is up 2% at $97.80

Gold is down 0.7% at $4,460

Bitcoin is down 0.3% at $67,350

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Tritax Big Box REIT (LON:BBOX) (£4.1bn | SR45) | The sale to EQT Real Estate includes a mix of big box and urban logistics assets. They were sold in line with their respective book values and generate total contracted annual rent of £12m. Proceeds will support investment in higher-returning development opportunities. | ||

Howden Joinery (LON:HWDN) (£4.1bn | SR87) | Acquisition for an EV of £390m, with £292.5m in cash and £97.5m in Howdens’ shares. Valuation gives a multiple of 8.5x last 12 months’ EBITDA to March 2026. DIY Kitchens generated revenue of £136m and EBIT of £37m last year (a 27% margin, versus 14.7% for Howdens). No change to previously announced £100m buyback. | AMBER (Roland) [no section below] Today’s acquisition is priced in line with Howden’s own valuation (8.5x EV/EBITDA). It looks small enough to be manageable and should be margin accretive. However, it’s worth noting this is a new line of business for the group. DIY Kitchens sells online, direct to retail customers who want to design their own kitchen. Howdens sells only to trade customers. There’s limited overlap in production, too: DIY Kitchens operates “short production runs for a made-to-order offering”. Howdens manufactures for stock and has long production runs. For these reasons, I guess, DIY Kitchens will continue to run as a standalone business, albeit with some consolidation of raw material supplies, etc. This acquisition opens up a new customer base to Howdens and seems to be a nice business. But there’s very little overlap with the group’s core activities. We’ll have to see how it pans out. More broadly, I can’t help feeling Howden’s valuation is approaching an area where it could be interesting – this is generally a quality business with a strong track record of growth. We haven’t looked at this stock since 2024, so I’m going to open our coverage today with a neutral view, reflecting the StockRank. | |

B&M European Value Retail (LON:BME) (£1.71bn | SR55) | “Profits at the midpoint of current guidance”. FY26 revenue +3.6%, adjusted pre-tax profit -37.7% to £284m. Adj EPS -36.4% to 21.3p. Net debt down 15.9% to £656m, within 1.0x-1.5x target range. Outlook: Back to B&M Basics “on track”, targeting “medium term” return to double-digit EBITDA margins. | AMBER ↑ (Roland) Sales were flat last year in the core UK business and margins fell sharply due to the twin pressures of higher costs and price cuts to stimulate demand. But my impression is that CEO Tjeerd Jegen is correcting the operational issues in the business and has a sensible strategy to return to growth. I am also encouraged by his regular share purchases since taking charge, which have totalled c.£1.5m over the last year. With a FY27E P/E of 9 and c.6% dividend yield, I believe there’s probably an opportunity here. However, difficult market conditions and relatively high leverage mean I’m going to upgrade to a neutral view today, in the hope of turning positive over the coming year. | |

Currys (LON:CURY) (£1.61bn | SR77) | Tønnesen has been the CEO of Currys’ Nordic business since March 2023 (40% of group revenue) and has over 20 years experience with the group, starting as a sales assistant. | ||

Ninety One (LON:N91) (£1.49bn | SR86) | AUM +31% to £171.8bn with net flows of +£2.8bn, mainly from Asia Pacific. Pre-tax profit +2% to £207.5m with adj EPS +12% to 17.4p. | ||

Energean (LON:ENOG) (£1.44bn | SR37) | Company has been informed by seller Chevron that one of its JV partners plans to exercise its pre-emption rights in relation to the Energean’s planned acquisition of interests in Block 14 and 14K offshore Angola. The JV partner must now demonstrate its suitability for the ownership of this deepwater asset. | ||

ITM Power (LON:ITM) (£1.28bn | SR27) | Protium Green Solutions and ITM have formalised a partnership to develop, invest in and operate green hydrogen plants across the UK, with an immediate focus on the Cromarty Project in Scotland, which was recently acquired by Protium. | ||

Discoverie (LON:DSCV) (£757m | SR59) | Revenue +5%, adj pre-tax profit +4% to £51.9m with adj EPS +4% to 40.3p. Organic order intake rose by 5% (+14% in Q4) and three acquisitions were announced, totalling £95m. Outlook: “good start to the new year” with orders ahead of sales and improving industrial market conditions. | AMBER = (Roland) [no section below] Today’s results from this electronics business appear to be in line with consensus. Broker forecasts for the year ahead are also unchanged. The growth rate remains unexciting and Discoverie’s operating margin of 10% and ROCE of 9.3% suggest to me that this is an average quality business and/or that some of its past acquisitions have been made at a relatively high price – a point Mark flagged up in December. I’m going to maintain our neutral view here today. I don’t see any obvious problems, but the sub-5% free cash flow yield implied by today’s results suggests to me that the valuation is up with events. | |

Rockhopper Exploration (LON:RKH) (£663m | SR32) | Sea Lion Phase 1 sanctioned, Rockhopper funded for Phase 1. First oil targeted Q1 2028 with 110m bbls 2P reserves net to Rockhopper. Debt financing in place including $350m of RKH debt plus $142m raised through placings. | ||

Griffin Mining (LON:GFM) (£563m | SR74) | Reinstating buybacks, plans to purchase $15m/3.7m shares by 30 Nov 26, after which further buybacks may be considered. | ||

Intuitive Investments (LON:IIG) (£523m | SR53) | Discussions regarding the possible offer continue. IIG has requested and received agreement for a further extension of the PUSU date for Acceler8 Ventures to make a firm offer to 5pm on 1 July 2026. | TAKEOVER | |

Seraphim Space Investment Trust (LON:SSIT) (£497m | SR93) | NAV +24.8% to £421.3m (NAVps: 177.63p). Portfolio valuation +30.7% to £433.3m. Gains driven by increase in unrealised fair value of £102m, mainly due to ICEYE, Xona Space Systems and Tomorrow.io. Raised £136.5m through C Share issue in May. | ||

Boohoo (LON:DEBS) (£263m | SR19) | Gross Merchandise Value +0.5% year-on-year, improving to +8% in May. Growth strongest across the Debenhams and PrettyLittleThing brands. Gross margin improved, to 53.5% (52.1% prior year), while the returns rate fell by 5% supporting a material improvement in EBITDA margin. FY27 Outlook: confident in delivering double-digit adj EBITDA growth and free cash flow in FY27. | AMBER ↑ (Roland) Today’s update is essentially in line and broker forecasts are unchanged. But I think there are some positives here, especially reiterated guidance for improved margins and positive free cash flow in FY27. Boohoo’s valuation looks up with events to me, but the future of this business seems a little more assured than it was previously. To reflect this situation, I’m moving our view to neutral today. | |

Capricorn Energy (LON:CNE) (£229m | SR98) | Alamadiyaf al-Masiyyah continues to progress its funding arrangements and, accordingly, the Company has requested, and the Panel on Takeovers and Mergers has consented to, a further extension of the PUSU Deadline. | TAKEOVER | |

Aew UK Reit (LON:AEWU) (£173m | SR60) | AEWU has bought an interest rate cap to protect against the risk of higher interest rates when its fixed‑rate debt facility with AgFe expires on 20 July 2027. Covers 50% of the company’s current debt. One-off premium of £638k paid. | ||

Ramsdens Holdings (LON:RFX) (£148m | SR96) | Revenue +62%. PBT up 173% to £16.7m. Resulting from the continued strong performance across our diversified income streams and the additional benefit of the sustained high gold price, the Board currently anticipates that profit before tax for FY26 is expected to be in a range of £30m to £33m, ahead of current market expectations” (prior consensus was £28.6m). | GREEN = (Graham) | |

Eleco (LON:ELCO) (£109m | SR47) | "The Board remains confident in the outlook and trading remains in line with market expectations for the full year." | ||

Avation (LON:AVAP) (£81m | SR38) | Signed an eight-year lease agreement, extending to 2034, at current market lease rates with FlyJaya, an Indonesian airline, for an ATR 72-600 aircraft. | ||

Venture Life (LON:VLG) (£69m | SR56) | Buys brands from OrganiCare Nature's Sciences, LLC for up to $28m. The brands are sold in Walmart, Walgreens, CVS and Target and generated net revenues of c. $12.1m for the 12-month period to March 2026. | ||

Frenkel Topping (LON:FEN) (£62m | SR72) | FCA Condition has now been satisfied. The Scheme of Arrangement remains subject to Court sanctioning. | TAKEOVER | |

Zenith Energy (LON:ZEN) (£29m | SR44) | Exclusivity agreements in connection with the potential acquisition of a combined shareholding of approximately 82% in Daybreak Oil and Gas. Daybreak is an independent, OTC-traded crude oil and natural gas company, active primarily in California. | ||

Tan Delta Systems (LON:TAND) (£24m | SR20) | Revenue flat at £1.22m. Adjusted loss before tax £1.55m (2024: £1.14m loss). Cash £1.49m. “The increased loss reflects increased overheads to support expanding customer trial support activities… we expect a number of ongoing evaluations to progress towards commercial rollout decisions during late 2026, with adoption expected to build thereafter.” | ||

European Green Transition (LON:EGT) (£23m | SR17) | Operating loss £1.36m (2024: £2.2m loss). Post year end, acquired the Wind Energy Services business for £3.5m. Raised £7.5m. “EGT has strong near and medium‑term revenue visibility, supported by a growing repowering pipeline, recurring revenue and maintenance contracts across its existing customers.” | ||

FIRST CLASS METALS (LON:FCM) (£12m | SR10) | Re: the monetisation of one of the company’s Ontario assets, “material commercial terms have now been agreed between the parties and the definitive transaction documentation is close to being finalised”. |

Graham's Section

Ramsdens Holdings (LON:RFX)

Up 8% at 492.4p (£160m) - Interim Results - Graham - GREEN =

These results are quite astounding and have led to yet another round of upgrades.

Analysts have struggled to keep up with how the business is performing:

I’ve been saying for a while now that it has turned into an almost pure-play bet on the gold price. This company has been in the right sector at the right time. Here are the interim highlights:

Revenue up 62% to £83.7m

PBT up 173% to £16.7m

Net assets up year-on-year from £55m to £70m.

Special dividend: the ordinary interim dividend increases from 4.5p to 6p, and the special interim dividend jumps from 0.5p to 3p. The total interim dividend has therefore almost doubled from 5p to 9p (H1 earnings per share were 37.9p, so this is easily covered).

One remarkable fact about these results is that the company has earned more PBT in H1 than they did in the entire previous financial year.

Precious metals purchasing: this is the standout performer with revenues up 141% and gross profit up 130%. The weight purchased was up 50% year-on-year.

I would like to give management credit for strong execution: while the high gold price does provide a windfall, it’s up to management to maximise the opportunity. This they have done:

While the high gold price, which has been well publicised in recent months, is one of the reasons for the increase in weight purchased, improved in store conversations, additional digital advertising following the launch of our new dedicated gold buying website www.ramsdensgoldbuying.co.uk and a TV advertising campaign have all helped too.

Pawnbroking: this is also supported by the gold price, and the Ramsdens loan book is up 30% year-on-year. They will lend 55% of the intrinsic gold value of an item, which they say is less than 40% of an item’s retail value as a pre-owned item. Pawnbroking gross profit is up 18%.

Jewellery retail: revenues here rose 26%, gross profit up 31%.

Currency exchange: the total value exchanged fell 0.5% and gross profit fell 9%. This sector is getting more competitive and Ramsdens themselves offer more competitive rates on their own currency cards.

Outlook is extremely strong as you might expect.

Global factors led to a sustained high gold price in H1, c.50% higher than H1 FY25. Many economists are predicting that the gold price will remain elevated for the remainder of 2026 and all through 2027…

We have a number of stores in their infancy which have capacity to mature and grow their profitability…

Should the gold price reduce, the Board believes that it will continue to deliver a strong performance, albeit with lower precious metal profits, and that it will remain capable of delivering further growth and rewarding shareholders with a progressive ordinary dividend.

As a result of the record H1 results and considering the macroeconomic backdrop and the continuing strength of the gold price, the Board is pleased to announce an upgrade to the Group's full year profit before tax, which is currently expected to be between £30m and £33m.

They helpfully provide a consensus PBT figure of £28.6m.

CEO comment:

"The Group is in a great position. While the gold profits grab the headlines, the Group has also delivered gross profit growth of 18% in pawnbroking and 31% in retail jewellery. Customer numbers in FX continue to be strong with total currency exchanged broadly flat…

Whilst the economic backdrop remains challenging with increasing employment costs, high interest rates and continued inflation, we remain highly confident in our opportunity to further strengthen the performance of our existing stores while adding new locations, executing against our established long-term growth strategy. Our balance sheet remains strong and our high level of cash generation provides options on how we allocate our capital to achieve growth.

Graham’s view

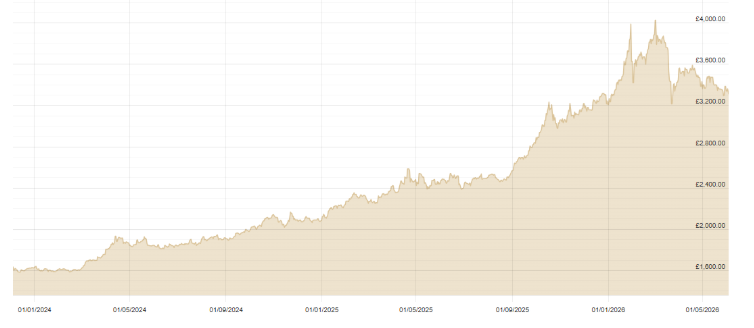

Let’s start with a gold price chart against sterling. Here’s a view from early 2024 with thanks to BullionbyPost:

My view on Ramsdens is entirely unchanged from what I said last time: this is a terrific way to gain access to gold exposure. I had a similar trade myself for many years, owning shares in a rival pawnbroker - the one that is no longer listed, sadly. But Ramsdens has picked up the mantle and now provides investors with that opportunity to get gold exposure away from the mining sector (which people like myself find to be a very difficult sector).

Since my comment on this in February, the market cap has increased from £130m to £160m.

And yet if after-tax net income comes in at somewhere around £23.5m (based on PBT of £30-£33m), then we are looking at a P/E multiple of only about 7x this year’s earnings.

It’s important to understand that market forecasts here assume that the gold price is going to fall, so if the gold price merely stays where it is, more upgrades will be coming.

Cavendish, for example, still uses the assumption that the 9-carat gold price in FY September 2027 will be £32/g. The current price is £40/g. As a result, they forecast that EPS will fall from 67p this year to 45.5p next year.

As something of a goldbug, I’m happy to roll with the idea that the gold price has a decent chance of not falling 20% from the current level. That’s not a prediction - but I do think it makes sense for us to stay positive on Ramsdens.

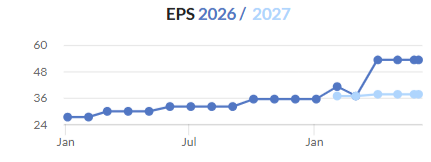

Two-year chart showing very strong Momentum:

And theStockRank is 96, making this a Super Stock:

Roland's Section

B&M European Value Retail (LON:BME)

Up 16% at 197p (£2.0bn) - FY26 Preliminary Results - Roland - AMBER ↑

We’ve been increasingly cautious about value retailer B&M since it ran into problems in 2024/5 and this view has paid off so far – B&M’s share price is 60% below historic highs and is still c.30% lower than it was one year ago – even after this morning’s gains.

However, today’s results suggest to me that the tide could be turning. Despite flattish sales and a slump in margins, cash generation was good last year and net debt fell.

Operationally, the business is also starting to correct the problems that crept in under previous leadership:

The past six months has seen us sharpen our pricing, improve on-shelf availability in best-selling brands and revamp our in-store promotions. We cleared discontinued lines well in Q4 and are now embarking on SKU count reductions across all our FMCG categories.

Let’s take a closer look at today’s results.

FY26 results: key points

These figures cover the 52 weeks ended 28 March 2026 and highlight sluggish sales, rising costs and plummeting profits:

Revenue up 3.6% to £5,775m

Adj pre-tax profit down 37.7% to £284m

Reported pre-tax profit down 47.3% to £227m

Adj EPS down 36.4% to 21.3p (Stocko consensus: 20.1p)

Net debt (exc leases) down 15.9% to £656m

Dividend down 36% to 9.6p per share

Various adjustments mean that reported pre-tax profit is around 25% lower than the adjusted figure, but I don’t think the adjustments are particularly sinister or surprising:

£36m impairment charge: this relates to an assessment of “individual store profitability” across all three of B&M’s operating segments. It looks like B&M has impaired some store leases and other related assets to reflect reduced expectations for future profitability. This is disappointing, but relatively small in the context of the group’s c.£1.5bn in lease liabilities.

£7m: “significant infrastructure projects” (new warehouses/import facilities)

£7m: redomicile project (moving the plc domicile from Luxembourg to Jersey)

£4m: external costs relating to strategic business projects (planning the Back to B&M Basics project)

£4m: costs incurred in “strategic leadership reset”

Except for the impairment, these are all cash costs. However, I think it’s fair to say they are also one-off items – so investors can choose whether to include or exclude them.

Profitability: I prefer to include the bad news as well as the good news in my view of profits. Using statutory operating profit gives me the following view on profitability:

Operating margin: 6.5% (FY25: 10.2%)

Return on Capital Employed (ROCE): 12.2% (FY25: 18.8%)

Last year’s numbers are well below the levels achieved by B&M in the past, but they are still better than those achieved by Tesco, Sainsbury or Pets at Home over the same FY26 period.

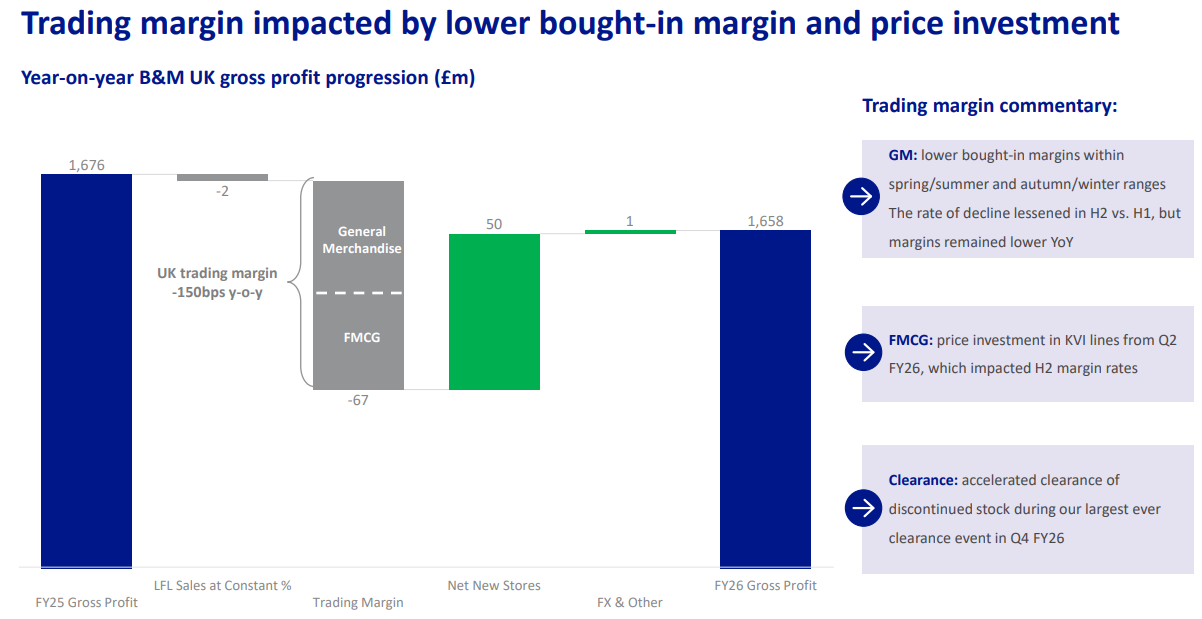

However, one thing that strikes me from today’s results is that the decline in margins seen last year could take some time to reverse, due to the twin pressures of lower bought-in margin and price cuts to stimulate demand in a tough consumer environment:

Cash flow & Balance Sheet: one of B&M’s main attractions as an investment historically was its strong profitability and resulting strong cash generation. Reassuringly, my sums suggest cash conversion remained excellent last year:

Free cash flow: £258m (FY25: £258m)

FCF conversion from net profit: 157%

The cash flow statement doesn’t flag up any one-off benefits that I can see last year, so this performance really is very good, in my opinion.

This result also allowed B&M to reduce net debt (excluding leases) by £125m to £656m last year. However, it’s worth pointing out that the fall in EBITDA last year means that overall leverage still increased:

Net debt to EBITDA (exc. leases): 1.4x (FY25: 1.3x)

Net debt to EBITDA (inc. leases): 2.9x (FY25: 2.6x)

I don’t see these multiples as being too concerning given the fall in net debt last year and strong underlying cash generation. But I would like to see bank debt fall further – gross borrowings were still c.£1bn at the end of the year.

I see most large retailers as businesses that should have low levels of bank debt, in order to offset high levels of lease liabilities and supplier credit.

Looking at peers, Pets at Home recently reported a FY26 net debt to EBITDA multiple of 0.1x excluding leases. Currys expects to report net cash excluding leases for FY26.

Trading commentary

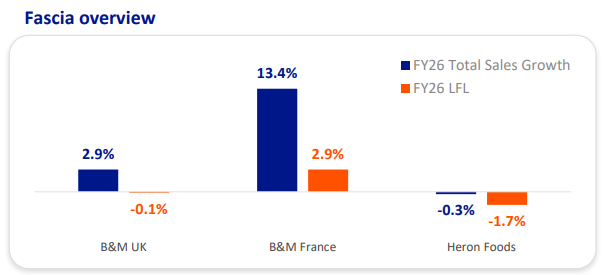

Performance across the group’s businesses was mixed last year. The star of the show was the smaller but fast-growing B&M France division:

Source: B&M FY26 presentation

B&M UK: “positive value and volume LFL performance” in General Merchandise offset by a continued decline in FMCG LFL sales (branded consumer goods). This is said to be improving as stock availability and ranging choices improve. 41 new store openings and 19 closures (+22 net), taking the total to 799. The company has reiterated its target of growing the UK store estate to c.1,200 stores, opening c.23-35 new stores annually.

B&M France: total sales growth was supported by 12 new store openings, taking the total to 147. The business gained market share to 8.4% of the discount market (FY25: 8.1%). With a store estate <20% of that in the UK, management see a strong runway for growth in France and are targeting at least 15 new stores per year.

Heron Foods (also operates under B&M Express): a poor result from this discount convenience grocery format (a kind of mini-Iceland). Despite having 342 stores, this business contributed <10% of sales and almost no profit last year. I wonder if it could become a candidate for disposal (B&M acquired Heron in 2017).

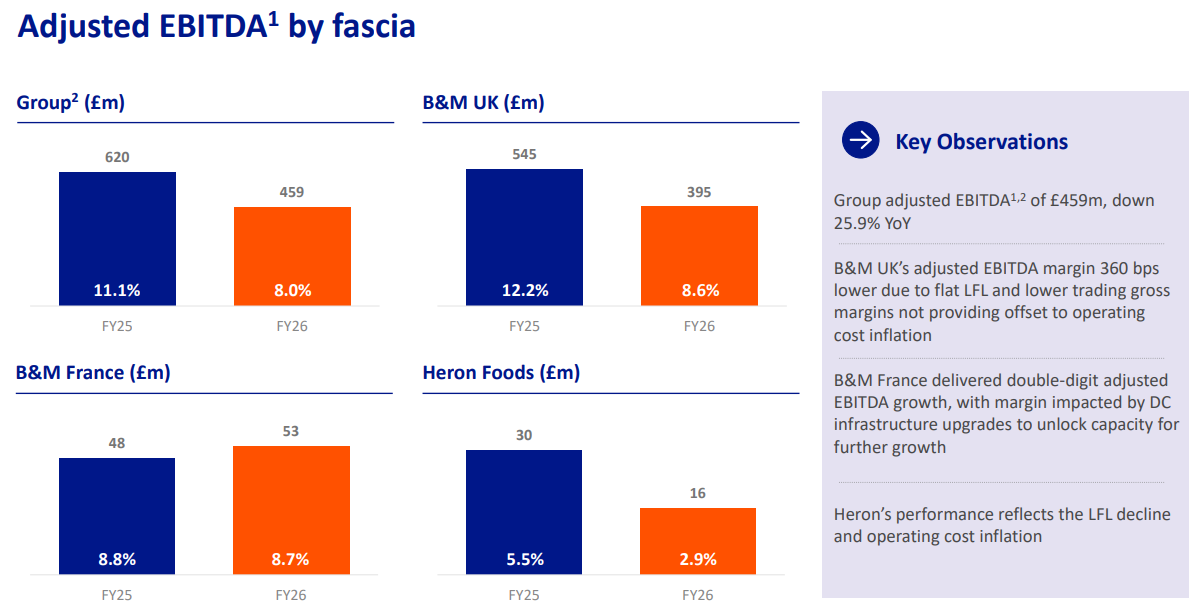

The French business was also the only division to generate an increased profit last year::

Source: B&M FY26 presentation

Interestingly, even though it's much smaller, the French business generated a return on segment assets of 18.9%, ahead of the 15.4% figure achieved by the much larger UK business. I'd normally expect the larger business to benefit from more favourable economies of scale. This suggests to me that the profitability of some B&M stores in the UK may be a little sub-par.

Outlook

Forward guidance is perhaps the only weakness in today’s results. Turnaround CEO Tjeerd Jegen is not rushing to commit to any near-term financial targets (albeit understandably). Instead, his outlook commentary emphasises near-term cost pressures and his medium-term target for margins:

One certainty of retail is that costs will always rise. In the past year, it was statutory costs in wages and environmental charges that challenged us. In the year ahead, the Middle East conflict will place upward pressure on our international freight, fuel and energy costs.

We are confident we have sufficient levers to offset this impact with cost mitigation. Over time, these benefits will flow through to our bottom line once we have returned B&M UK LFL sales to growth. In the medium term, we continue to see no reason why B&M UK cannot return to double-digit EBITDA margins.

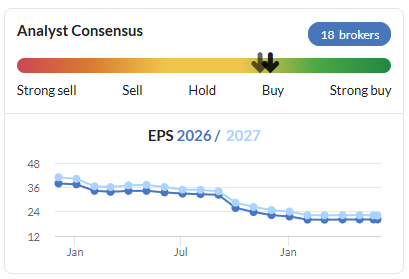

Broker consensus ahead of today’s results suggested B&M’s earnings growth could be minimal in FY27:

I am inclined to think these forecasts might be nudged up slightly following today’s results, given the 16% share price rise at the time of writing.

However, without any access to broker forecasts, I can't be sure.

Roland’s view

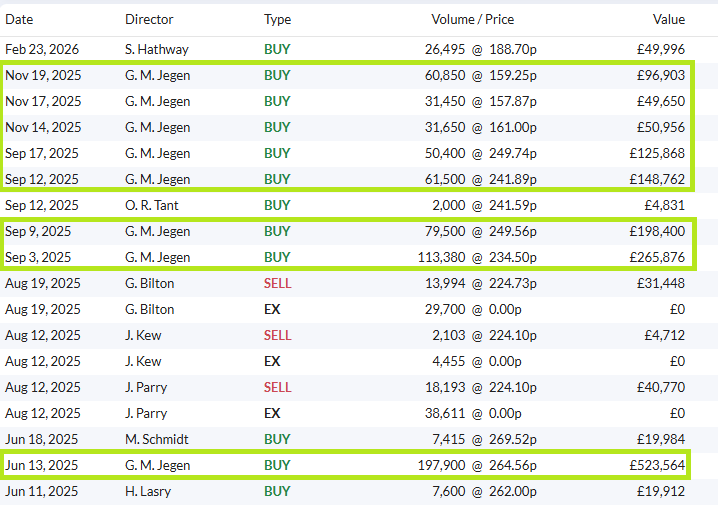

Tjeerd Jegen was appointed CEO with a strong track record in retail at companies including Ahold Delhaize and Tesco.

He has also been a regular buyer of shares since taking charge, investing c.£1.5m over the last year:

We often say that significant buying by CEOs and CFOs can be a positive leading indicator. No one knows the business better, after all.

Jegen’s record of buying since taking charge reminds me of the regular purchases by Rolls-Royce CEO Tufan Erginbilgic shortly after he started at the industrial group. Those purchases proved to be a signal worth following, although of course there’s no guarantee this will happen at B&M.

Even if FY27 forecasts are unchanged today, B&M shares are still only trading on a P/E of 9 after today’s results, with a prospective dividend yield of perhaps 6%.

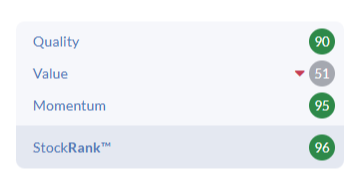

I am inclined to think this could be an attractive entry point and I share the StockRanks’ view that B&M could offer a contrarian opportunity:

However, I can still see some risks relating to cost pressures and limited pricing power in the UK, overlaid by B&M's relatively high leverage.

I'm going to upgrade our view on this retailer to neutral today, in the hope that I'll be able to turn positive over the coming year.

Boohoo (LON:DEBS)

Up 25% at 23.5p (£308m) - Q1 FY27 Trading Update - Roland - AMBER ↑

Today’s update from Boohoo is only in line with expectations, but it’s generated a very positive reaction from the market. When I see this combination, I usually assume the market was expecting bad news and is expressing relief.

There is certainly some good news in today’s update, which covers the three months to 31 May:

Group Gross Merchandise Value +0.5% - “returned to growth”

May trading particularly strong, with GMV +8%

Gross margin improved to 53.5% (prior year: 52.1%)

Customer return rate fell by c.5% during the quarter

All of this should add up to an improvement in profit margins and Boohoo confirms this, at least an adjusted EBITDA level:

Adjusted EBITDA margin expanded materially year on year, delivering a substantial increase in Adjusted EBITDA in the period.

The company also reports a decline in exceptional costs (-72%) and capital expenditure (-54%) during the quarter, “keeping the Group firmly on track towards free cash flow generation”.

Outlook

Today’s commentary relates to the FY27 financial year, which ends on 28 Feb 2027. It’s still early in the year, but today’s guidance addresses several key concerns:

Confident in delivering “double-digit adjusted EBITDA growth” relative to the £53m guided for FY26.

Reduction of net debt to less than 1.0x EBITDA is “on track” for the current year. This will be aided by property disposals.

On track to achieve £100m of cost savings through 2027. This would take the cumulative total to c.£200m since the new management team was appointed.

Capex will be 50% lower this year, continuing a trend of reduced spending (FY25: £27.5m, FY26: 16m)

The overall result is expected to be a return to positive free cash flow in FY27.

Broker forecasts from Zeus and Panmure Liberum are unchanged today. Both reiterate a much-improved outlook for FY27, compared to the consensus estimate for a loss of 1.5p per share in FY26:

Panmure Liberum: FY27E adj EPS: 1.6p

Zeus: FY27E adj EPS: 0.9p

There’s quite a wide range between these two estimates, but averaging them gives me a FY27 EPS estimate of 1.25p per share, well ahead of the 0.6p shown in the StockReport.

Based on this morning’s 23p share price, that implies a forward P/E of 18x for the current financial year.

Roland’s view

I’m impressed by the level of cost that’s being stripped out of this business. Assuming the new management team aren’t cutting too deep, I think today’s update adds credibility to the company’s aim of becoming a more profitable and capital-light operation, built around the Debenhams brand and various fast-fashion labels.

If this transition is successful and the business does return to sales growth, then margins could improve quickly due to the beneficial effect of operating leverage on a lower cost base.

I would imagine this is the assumption behind Zeus and PanLib’s medium-term price targets of 56p and 60p respectively.

However, even today’s share price of 23p looks relatively full to me, based on near-term prospects.

Whether Boohoo – or Debenhams Group as it would like to be known – can achieve the hoped-for potential of its changing business model isn’t clear to me.

The eventual outcome for the business is also complicated by the 23% shareholding controlled by Frasers group and the large block of shares owned by the co-founding Kamani family.

We’ve been AMBER/RED on this stock until recently, but I think it’s probably fair to move to a neutral view today to reflect the stabilisation of sales and expected improvements in profitability and free cash flow. AMBER ↑

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.