SpaceX is reported to be massively oversubscribed, with more than four times the demand than the quantity of shares that are actually available.

Official pricing is today (at the fixed price of $135 per share) and trading in the shares should begin tomorrow.

At a $1.8 trillion valuation, it will be more valuable than Tesla (NSQ:TSLA) and Meta Platforms (NSQ:META) but not quite as valuable as the likes of Amazon.com (NSQ:AMZN) and Microsoft (NSQ:MSFT). It will be a top 10 stock in the US by market cap.

In terms of its historical importance, it’s a truly landmark event. Alibaba Holding (NYQ:BABA) had a market cap of $169 billion at its IPO price, which seemed enormous at the time (this was in 2014). Saudi Aramco was valued at $1.7 trillion at its 2019 IPO, although they only raised $29 billion.

SpaceX, by contrast, is raising $75 billion - and apparently could have raised a lot more.

If you want my opinion, we have moved into a stage of the long-term bull market where prices for popular shares are now entirely unmoored from the fundamentals. I’ve mentioned recently the price to sales multiples for SpaceX, which do not fit with any standard method of valuation. But maybe this time is different?

Overnight market movements:

The FTSE is set to open down 0.3% at 10,220

S&P 500 is up 0.4% at 7,300

Brent crude is up 0.4% at $93.30

Gold is up 0.6% at $4,100

Bitcoin is up 1.5% at $62,700

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Halma (LON:HLMA) (£17.6bn | SR69) | Revenue +15% to £2.58bn, Adj. EPS +21% to 114p, dividend +&% to 24.74p. Outlook: Positive start to the 2027 financial year, strong order book and order intake ahead of revenue and last year. Economic and geopolitical environment remains uncertain. Expect low double-digit percentage organic CCY revenue growth. Adj. EBIT margin in line with 2026. | AMBER ↓ (Graham) | |

Derwent London (LON:DLN) (£2.08bn | SR67) | Jonathan Murphy appointed as Chief Executive. Most recently Chief Executive Officer of Assura plc. | ||

Grafton (LON:GFTU) (£1.58bn | SR85) | Targets for 2030: Adjusted EPS CAGR 10%+ over the period 2025 to 2030. Cumulative FCF £850m+ over the five year period 2026 to 2030. ROCE 13%. Lease-adjusted net debt to EBITDA ratio of 1.0x to 2.0x. Dividend cover in 2.0x to 3.0x range. | ||

Sirius Real Estate (LON:SRE) (£1.54bn | SR88) | Placed €185.1 million nominal value of notes through taps of two of its existing corporate bonds, taking each bond to a total outstanding nominal amount of €500.0 million. | ||

Safestore Holdings (LON:SAFE) (£1.38bn | SR55) | H1 Revenue +5.6% to £120.6 (LFL +5%), u/l PBT +2% to £44.6m, Adj. EPRA EPS +2% to 19.4p. EPRA NTA ps -0.8% to 1,120p. FY 2026 outlook: Return to earnings growth with projected EPS at the lower end of consensus range largely reflecting the expected impact of higher interest rates in H2. | BLACK (lower end of consensus) | |

Great Portland Estates (LON:GPE) (£1.28bn | SR30) | Secures 12 new Fully Managed leasing deals totalling over 41,000 sq ft and delivering £8.0 million of annual rent at an average of £195 per sq ft. | ||

Serica Energy (LON:SQZ) (£1.06bn | SR92) | Acquisition from ONE-Dyas of a 10% interest in the Catcher Field and a 5.21% interest in the Golden Eagle Area Development has now completed. Adds around 2,500 boepd, and net 2P reserves of 3.0 mmboe. | ||

Wizz Air Holdings (LON:WIZZ) (£1bn | SR62) | Fleet +13% to 262, Revenue +8% to €5.691bn, EBITDA +16% to €1.318bn, Net profit -99% to €1.3m, Net debt flat at €4.941bn. “Not giving guidance for F27 at this time of the year given the lack of visibility across our trading seasons, uncertainty related to the ongoing conflict in Iran and the closure of the Strait of Hormuz.” | ||

International Personal Finance (LON:IPF) (£552m | SR88) | All conditions satisfied apart from Poland. IPF and Bidco currently expect the Polish Regulatory Condition to be satisfied before the Sanction Hearing, which is now expected to take place in late July 2026. | ||

Foresight group (LON:FSG) (£488m | SR89) | Agreed to sell its public markets investment division, Foresight Capital Management, to Guinness Global Investors, totalling £1.0bn AUM (7% of Group AUM) and 16 employees. No price given. | ||

Origin Enterprises (LON:OGN) (£407m | SR93) | YTD Revenue +2.7% (+5% CCY), FY adj. EPS guidance €0.52-0.55. | ||

NCC (LON:NCC) (£401m | SR73) | Unaudited interim results & Conclusion of the Cyber Strategic Review | Escode sale completed on 29 May 2026, and NCC is now a pure-play Cyber business. Strategic review of the Cyber business is now complete. £170m tender offer + £15m share buy-back. H1 Revenue +5% to £151.3m, Adj. EPS +200% to 4.5p, Net debt excl. Leases at 31 Mar £10.2m. £230m net cash at 1 June following Escode disposal. | |

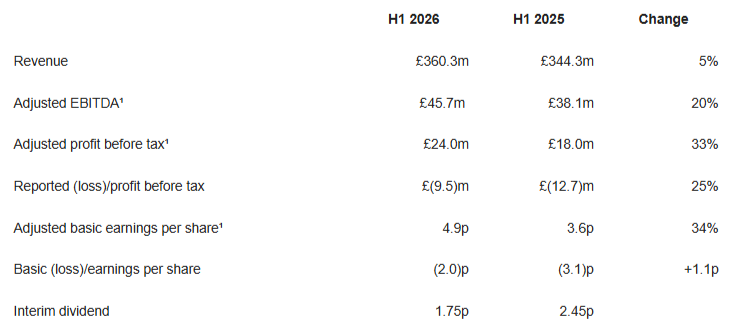

RWS Holdings (LON:RWS) (£381m | SR93) | FY26 Revenue +5%, Adj. EBITDA +20% to £45.7m, Adj. PBT +33% to £24m, reported LBT £9.5m. Interim dividend -29% to 1.75p. Net debt £32.5m (FY25: £25.4m). Good start to the second half; continue to trade in line with expectations for the full year. FX hit of £2.0m + £1.0m hit from Obviously acquisition. | AMBER/GREEN ↓ (Mark) On the surface, these are reasonable in-line results. However, the more I look into them, the less I like them. The single-digit P/E is based on heavily adjusted figures. Plus the dividend looks like it may come in a little below analysts’ consensus for the full year. With these in mind I think we should take a slightly more cautious view, at least until the gap between adjusted and statutory figures is narrower and the strategy concerns are shown to be overblown. | |

PayPoint (LON:PAY) (£335m | SR72) | FY26 Net Revenue +1.7% to £190.8m, u/l EBITDA +2.2% to £92.0m, u/l PBT +1.5% to £69.0m. Net debt £132.5m (FY25: £97.4m). “Overall, the Board remains confident in delivering further progress, exceeding the underlying profits achieved in FY26 and achieving results in line with market expectations.” | ||

Forterra (LON:FORT) (£281m | SR64) | CFO leaving the group after 20 years with Forterra and its predecessor organisations to pursue new challenges. Will remain as CFO until October to assist with an orderly transition. | ||

Social Housing REIT (LON:SOHO) (£279m | SR63) | Inclusion Housing Community Interest Company has received a compliant G2 V2 regulatory grading by the Regulator of Social Housing. Inclusion is SOHO's largest lessee, representing approximately 30% of its annual rental income. “…a positive development for the sector, providing further evidence that well-managed, lease-based providers can operate successfully within the regulatory framework while continuing to deliver high-quality homes and services for vulnerable residents.” | ||

Empire Metals (LON:EEE) (£250m | SR7) | Completed an integrated metallurgical processing flowsheet for the Pitfield Titanium Project in Western Australia. | ||

Serabi Gold (LON:SRB) (£239m | SR99) | NI 43-101 Technical Report for the Palito Complex and Coringa Mine | Publicly filed its detailed technical reports of its updated Mineral Reserve estimates and Mineral Resource estimates for its 100% owned Palito Complex. | |

Norcros (LON:NXR) (£237m | SR89) | Revenue +10.6%. Underlying operating profit +7.9%. Outlook: “Market conditions are likely to remain subdued, with the pace of any recovery in the new build sector still unclear. The mid-premium RMI sector currently remains more resilient and the Board's expectations for FY27 are unchanged.” | ||

Concurrent Technologies (LON:CNC) (£218m | SR43) | Four-year order worth c. £17 million from a major European defence equipment prime contractor. "More broadly, demand across our defence markets remains encouraging.” | ||

M&C Saatchi (LON:SAA) (£172m | SR63) | Like-for-like net revenue is in line with expectations and supportive of the market's full year outlook. | ||

Strix (LON:KETL) (£75.5m | SR92) | The new CEO was previously Group Chief Commercial Officer at A-SAFE Ltd, which makes traffic barriers and bollards. Was also Managing Director and Group Commercial Lead at AIM quoted Grosvenor Technology / Newmark Security Plc. | ||

Zephyr Energy (LON:ZPHR) (£63m | SR26) | Q1 production averaged 918 boepd net to Zephyr (vs 983 boepd in Q4). Q1 “exceeded management's forecast and reflects the expected natural decline rates of the portfolio.” | ||

Poolbeg Pharma (LON:POLB) (£53.3m | SR27) | The first site activation for the first-in-patient POLB 001 TOPICAL clinical trial has occurred. | ||

Palace Capital (LON:PCA) (£33m | SR52) | Adjusted loss before tax £0.1m. Actual loss before tax £5.4m. NAV per share falls 14% in H1 to 210p. | ||

Predator Oil & Gas Holdings (LON:PRD) (£30.8m | SR8) | Snowcap-3 long-lead well inventory build progressing on track. Oil storage tanks (capacity 1,200 barrels) to move to Snowcap-3 production facilities site. Various other updates. “We are very pleased with current progress given the unpredictable impact of the Middle East conflict on the global logistical supply chain.” | ||

Bezant Resources (LON:BZT) (£27.3m | SR32) | Definitive documentation for the US$7 million secured prepayment facility and offtake agreements with Hartree Metals LLC. | ||

Haydale (LON:HAYD) (£25.3m | SR-) | Expansion of its agreement with Lloyds Bank through its SaveMoneyCutCarbon platform. National launch targeted for June 2026. | ||

Panther Metals (LON:PALM) (£12.9m | SR22) | The first drill hole at the Awkward Conduit Target has completed successfully and drilling has now commenced at the Wishbone Prospect. | ||

Rockfire Resources (LON:ROCK) (£11.4m | SR16) | Appraisal of the historical underground mining access at the Molaoi project in Greece: “…The current condition of the underground, which was only observed from the entrance, did not exhibit visible deterioration of the existing support system.” |

Graham's Section

Halma (LON:HLMA)

Down 15% at £39.38 (£14.97bn) - Full Year Results - Graham - AMBER ↓

These 2026 results look good against expectations, but it’s the FY27 outlook that is more questionable.

Firstly, a brief overview of FY March 2026. (By the way, I find it easiest to read them on Halma’s website as the RNS itself is empty.)

Revenue +15% to £2,582m (StockReport forecast: £2,559m)

Organic revenue growth of 16%, far above their long-term target of 7% thanks to high growth in their photonics business.

Adjusted EPS +21% to 114.05p (StockReport forecast: £113p)

Halma’s US-based photonics business designs, develops and manufactures photonics equipment out of Philadelphia.

The results are clean with statutory EPS of 98.57p (up 26%).

The company calculates an “adjusted Return on Total Invested Capital” of 16.2%, up from 15% last year, which is also very encouraging.

The full-year dividend gets a 7% increase to 24.74p, which is covered several times over by EPS.

Leverage is modest at 1.16x, “well within operating range of up to two times”.

So what’s the catch?

Outlook:

We have made a positive start to the 2027 financial year, with a strong order book and order intake ahead of revenue and last year.

But…?

While the economic and geopolitical environment remains uncertain and our companies continue to experience varied conditions in their end markets, we currently expect to deliver low double-digit percentage organic constant currency revenue growth in this financial year, including premium growth of approximately five percentage points from our photonics business.

Adjusted EBIT margin is expected to be in line with the 2026 financial year (excluding the one-off from the Nuvonic transaction).

Graham’s view

Checking forecasts, I can see a £2.87 billion revenue forecast on the StockReport for 2027.

Granted that this number is not organic, but that’s an increase of 11% over the 2026 figure.

This seems to match well with the outlook provided today of “low double-digit percentage organic” growth.

Indeed, low double-digit organic growth, plus some inorganic growth from the 2025 acquisitions, perhaps could help to boost FY27 revenue over that £2.87 billion forecast?

None of this seems to justify a 15% fall in the share price.

I’ve also checked the forecast EBIT margins and can’t detect any major disappointment in the outlook on that front, either. The market already expected FY27 margins to match FY26 margins.

But I think I can put together some post hoc reasons for today’s fall in the share price.

1. FY27 EPS forecasts have been on a rising trend, and the market may have expected a continuation of that trend, with scope for another upgrade. Today’s outlook doesn’t provide that.

2. Instead, today’s outlook raises the spectre of a potential profit warning with talk of "uncertainty" and "varied conditions" in end markets.

3. Halma’s share price has been on a terrific run in 2026, up over 30% year-to-date. As I’ve stated several times recently, “selling the news” is a common tactic on the day of results or trading updates, after a run like this.

4. The P/E multiple going into these results of 36x is at a level that tends to be especially fragile to any negative change or uncertainty around the outlook. The ValueRank here is only 5.

I believe that the new forward P/E multiple is about 31x, after today’s fall.

With photonics growth expected to recede, the total organic growth rate will shrink from 15% to maybe c. 11%, and the long-term target growth rate is only 7%. Personally, I expect higher growth rates than this, from a business trading at this sort of earnings multiple.

In December, I said that I wanted to find “any excuse” to downgrade our stance on Halma from AMBER/GREEN to neutral. The market cap today is higher now than it was in December, and I think I now have enough reasons to justify a neutral stance on this High Flyer. So I’m AMBER on this today.

Mark's Section

RWS Holdings (LON:RWS)

Down 13% at 88p (£381m) - Half-year Financial Report - Mark - AMBER/GREEN ↓

I have to admit to selling out of this still apparently cheap stock on the news that they were paying between £16.5 and £40m for a business that was founded two years ago which turned over £2.5m and lost £1.5m last year. Paying between 6.6 and 16x sales for a start up, just smacked of a certain desperation from management and I started to worry that this was not the behaviour of a company where everything was going well with its core business. In light of that, these figures don’t look to bad (at least on an adjusted basis):

Although they appear to have forgotten how to calculate a percentage when it comes to their declining dividend payout!

Adjustments:

These figures are not a surprise, though, as they already announced £360m revenue and £24m PBT in their HY trading update. How they got there is what is revealed in these results. Here is their description of those adjustments:

Group Transformation Programme - £3.3m - including costs related to transitioning our current on-premises infrastructure to a modern cloud-based environment

Strategic project costs - £0.3m - costs involved in corporate development opportunities.

Restructuring and integration costs - £7.5m - related to severance and termination payments related to the Group's cost reduction plans, and other corporate restructuring initiatives.

These categories aren’t necessarily out of place for many companies’ reporting these days. However, these are mostly cash costs and explain why the cash conversion has dropped from 92% last half year to 67% in this half. The IT costs really should be part of the normal investment a company makes into running their business in my opinion. And I have a natural revulsion towards companies that want us to give them the benefit of cost-cutting but ignore all the costs of doing so. After all, they booked £4.6m of restructuring costs in H1 last year, and £14.2m in H2. These costs are looking less and less exceptional.

In light of all this, it is hard to believe that the adjusted figures represent the economic reality of the business, at least until it is clear that they are through the current restructuring phase of the business.

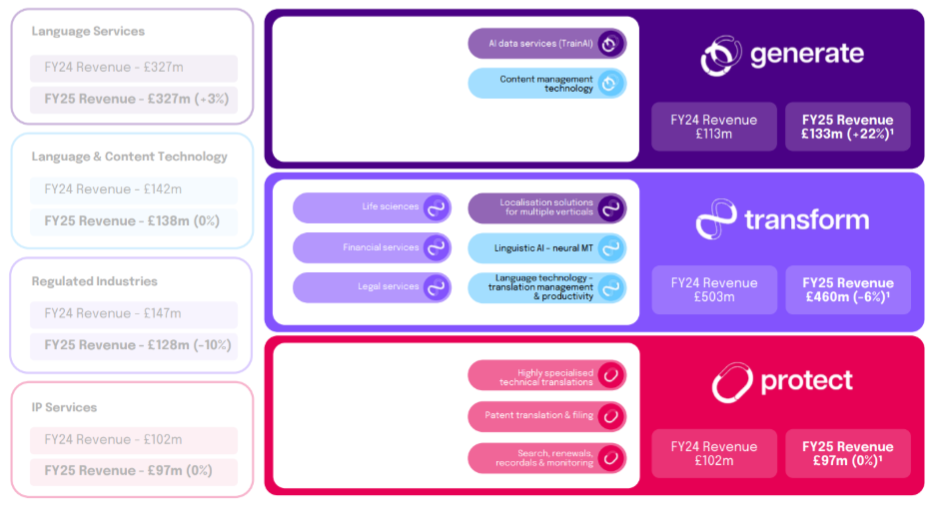

Segmental Reporting

The company recently changed their reporting segments. As a reminder here is how the old structure maps into the new one:

Generate:

This is the stand out performer in this half, although a declining profit margin takes the edge off:

They say this was due to “Exceptional revenue performance driven by TrainAI from programmes with existing clients and initial revenues from a new global technology client.”

Strangely, TrainAI seems to be lower margin than the rest of this segment, and they say that in H2 “TrainAI exceptional H1 revenue will continue to dilute margins.” I’m not sure why providing a lot of training data to LLMs isn't a very high margin business.

Transform

The revenue decline was in line with their previous guidance. This segment contains their own AI translation tool: Language Weaver Pro. This shows what we can expect, clients will pay less for AI translation, but the costs are lower too, driving higher profits on lower revenue.

Protect:

This is the most worrying part with the margin decline said to be due to product mix and an increase in overhead cost. This is where the Obviously acquisition sits and shows signs that one of the key contributors to historical profits is under pressure.

Strategy:

I continue to be worried about trainAI. This may be responsible for a return to revenue growth for the business as a whole. However, management have yet to give a convincing argument to me as to why they aren’t just giving away the crown jewels (a huge database of accurately translated technical documents) to competitors in return for a short-term payment.

Adding the pressure in Protect that appears to have led them to buy a loss-making start up on a high multiple of revenue, this shows that they may face technological competitive pressure throughout the business.

Outlook:

The outlook is said to be in line:

Expect mid-single-digit revenue growth on an OCC³ basis, improving profitability, and continued strong free cash flow conversion for the full year as we benefit from recent client wins, growth in Generate and Protect and our efficiency programme.

Mid-single digits aligns with the 5% revenue growth in H1, and would actually be above analysts consensus, but I would imagine the organic constant currency bit is doing the damage.

On profitability they add the line:

Current FX rates, after hedging, are expected to have a c.£2m adverse impact on full year PBT, alongside the anticipated £1m in-year impact from the Obviously acquisition which is expected to start contributing during FY27.

It is not wholly clear whether they consider themselves to be trading in line with expectations despite these factors. However, given the scale of the adjustments in these half year results, I wouldn’t be surprised if they are trading in line without these headwinds, i.e. slightly below.

Sadly, mere mortals such as us don’t have access to broker research, so it is hard to say if today’s share price drop is due to cuts to broker numbers, or if shareholders simply didn’t like the narrative.

Dividends:

Having failed to calculate a percentage for us, we fear the worst on the dividend payout. However, the cut to the interim dividend at 29% is less than the cut to the final dividend, which was down 56%:

To hit the FY forecast payout the company would need to raise the final dividend to 5.35p, which may be a stretch considering net debt has risen from £25.4m to £32.5m year on year. Post period end, they have spent £16.5m on the Obviously acquisition.

The leverage ratio remains modest at less than 1x EBITDA. However, we are used to this business running with net cash, plus they have cut the dividend and not bought back shares despite the share price dropping to a third of the price they last acquired stock in the market. This suggests that they are comfortable with the current debt levels, but not particularly keen to take on more, given the big shifts happening in their core business.

Mark’s view

On the surface, these are reasonable in line results. However, the more I look into them, the less I like them. Hitting the H1 trading figures required continued significant adjustments for IT projects and redundancy payouts. It seems that hitting full year guidance will need a similarly heroic performance from the accounts department. They are already flagging FX headwinds and the loss from their recently acquired business. The cynic in me thinks they will shortly be asking us to exclude these too.

Then there are the issues of strategy: does it really make sense to be taking (what appears to be low-margin) revenue to train competitors’ LLMs on your proprietary data? Are declining margins in Protect flagging serious competitive pressures?

However, the fact that the strategy here is open to debate, and the company loves its adjustments are not new information. Which makes today’s double-digit fall a bit of a mystery. I can only think that the market may have gotten a little ahead of itself. After all, the strongest Rank here prior to these results was the Momentum one:

Part of the recent rise appears to be due to the market liking the Obviously acquisition. However, to me paying between 6.6x and 16x sales for a loss-making startup was a sign of desperation rather than strategic brilliance.

Roland upgraded this to GREEN following last year’s final results when the share price was around 80p, citing the recovering fundamentals and mid-single-digit forward P/E. The shares briefly touched 110p, but with them now back below 90p, many of the positive arguments still stand.

However, I think there are also some reasons for caution. That single-digit P/E is based on heavily adjusted figures, and the company already seems to be flagging some extra adjustments required to make current trading in-line with expectations. The dividend also looks like it may come in a little below analysts’ consensus for the full year. With these in mind I think we should take a slightly more cautious view of AMBER/GREEN, at least until the gap between adjusted and statutory figures is narrower and the strategy concerns are shown to be overblown.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.