In what felt like deja vu, yesterday evening, Trump announced that an agreement to end the war with Iran was close, hours after cancelling a third consecutive night of strikes. His previous threat was that the US would strike Iran "very hard", but shortly afterwards that negotiators had "just made a great settlement" with Iran.

Presumably, his inner circle had just bought a lot of short-dated calls, as Iran poured cold water on the idea. Foreign ministry spokesperson Esmail Baghaei told state TV that reports of an agreement were "speculative" and "nothing has been finalised".

All this happened after the UK market closed and before the US market closed, but with oil down, gold up, and the major indices up since the UK market closed, we can expect a good day for UK equities.

Overnight market movements:

The FTSE is set to open up 0.9% at 10,390.

S&P 500 is up 0.1% at 7,395.

Brent crude is down 2.3% at $87.89.

Gold is down 0.7% at $4,180 (+2.7% from UK market close)

Bitcoin is flat at $63,400.

Spreadsheet accompanying this report: link.

12:30 - Report is complete

Companies Reporting

Name (Mkt Cap) | RNS | Summary | Our view |

|---|---|---|---|

GSK (LON:GSK) (£79.5bn | SR92) | Designations support development efforts and regulatory evaluations for medicines with potential to treat or prevent rare disorders. Phase II/III trial in VEXAS underway, advancing momelotinib's broader development programme. | ||

Kier (LON:KIE) (£878m | SR72) | To continue delivering vital maintenance and improvements across South West Water's network over the next two years, following a c.£140m extension to its role on the Network Services Alliance. | ||

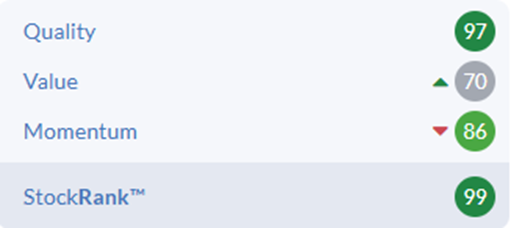

M P Evans (LON:MPE) (£784m | SR99) | 1st 5 months of 2026: Total Crop harvested +10% to 575kt, pricing strong CPO $880/t & PK $824/t. Has experienced some cost increases during the year, particularly for diesel used for transportation and for fertiliser applied to the Group's palms.Expect to achieve unit production costs for 2026 at a level similar to those for the previous year. | AMBER = (Mark) A reasonable update, highlighting production growth and higher pricing. So far, they see no impct form the recent changes to palm oil export policy. However, with the rating given to this commodity producer having doubled over the last few years, future returns will largely depend on one's view of where we are in the commodity cyle. Those who see tight markets for CPO, and in particular PK, will expect the company to beat expectations and will want to hang on. Those who see current pricing as towards the top of the cycle will use the current drop in Momentum as a signal to exit. In such situations, the commodity-price agnostics, such as myself, will take a neutral view. | |

Boohoo (LON:DEBS) (£328m | SR28) | Has completed the sublease of its distribution centre in the United States to ID Logistics, a leading global third-party logistics (3PL) operator. Total lease costs in the current year will be £13m, which will further reduce to £8m in FY28 and £6m in FY29 as the benefits of the $9.5m average annual rent income under the Sublease are fully realised. | ||

McBride (LON:MCB) (£290m | SR90) | Since April, has experienced sustained cost increases in petrochemical-derived and energy-intensive materials as a consequence of the current Middle East conflict. Impact on input costs has exceeded original expectations due to the continuing and prolonged period of the conflict, which has required a second phase of price recovery actions. Now expects FY26 and FY27 adjusted EBITA to be between 5 and 10% lower than current analysts' expectations. Acquisition of Eurotab to complete on or around 1 July 2026. | BLACK/AMBER (Mark) | |

Henry Boot (LON:BOOT) (£222m | SR43) | CEO Succession Update & Appointment of new MD at Stonebridge Homes | Edward Hutchinson will succeed Tim Roberts as Chief Executive Officer of the Company, effective as of 13 July. Warren Thompson as the new Managing Director for Stonebridge Home. | |

Trufin (LON:TRU) (£125m | SR86) | Intention to return £80 million to Shareholders following the completion of the Disposal of Playstack. £56.8m via 140p tender offer (5% premium to last night’s close) and £32.2m special dividend. | ||

Severfield (LON:SFR) (£78.5m | SR66) | New three-year banking facility agreement with its existing lending syndicate. £60m RCF, £7.6m term loan +£30m accordion. | ||

Quadrise (LON:QED) (£38.1m | SR5) | Valkor's 500 barrel per day oil-sands pilot plant is now due to be commissioned in Q4 2026. Will not therefore deliver Multifuel Manufacturing Unit to site in Q2 as had been previously indicated, this will now take place during Q3 2026. No further licence fee payments have been received by the Company and US$0.95 million of the US$1.0 million licence fee payable by Valkor remains outstanding as Valkor await receipt of approved project funding. | ||

Virgin Wines UK (LON:VINO) (£15.9m | SR53) | Now expects FY26 revenue of £61m, EBITDA of -£200k and PBT of -£1.5m (Down from £63.25m, EBITDA +£100k, PBT -£1m. | BLACK/AMBER/RED ↓ (Mark) At the risk of playing stance ping-pong, I feel we have to go back to a broadly negative view. The company's cash balance, due to the cash it receives upfront from customers, gives it a significant cushion to turn things around. However, any company that has been listed for 5 years and still reports negative EBITDA has to have significant questions hanging over its long term future. | |

Medpal AI (LON:MPAL) (£14.1m | SR0) | Notes the announcement by the Medicines and Healthcare products Regulatory Agency granting UK marketing authorisation for the first oral GLP-1 receptor agonist tablet (oral semaglutide) for weight loss and weight management. | ||

Cizzle Biotechnology Holdings (LON:CIZ) (£11.7m | SR11) | Patent application covering the Company's core methods to measure the CIZ1B lung cancer biomarker has now been allowed by the U.S. Patent and Trademark Office. Follows the grant of a patent in Canada. | ||

Pennant International (LON:PEN) (£11.2m | SR23) | Canadian government has awarded a new IPS services contract to Pennant Canada Limited for the use and optimisation of Pennant's Auxilium suite of software to support maritime programmes within the Canadian Department for National Defence. Framework agreement for an initial five-year term, with annual options to extend for a further 6 years. at historical rates of DND usage of Pennant IPS services, the initial value of the five-year framework is estimated at C$15 million. | AMBER/RED ↑ (Mark) Today’s rise looks excessive for what appears to be a formalisation of an existing relationship and was already in forecasts. Plus, the broker’s preferred valuation method leaves little upside and is based on highly uncertain 2027 estimates. However, today’s contract news shows that they do have a product that is valued by end users and it no longer looks like it’s going under imminently (hence our previous RED view), so I think we can afford to be slightly more positive. |

* Market caps at previous trading day’s close

Mark’s Section:

Pennant International (LON:PEN)

Up 11% at 26p (£11m) - Multiyear Auxilium Services Contract Award - Mark - AMBER/RED ↑

This agreement sounds impressive at C$3m/year:

Whilst not subject to a minimum contract value, at historical rates of DND usage of Pennant IPS services, the initial value of the five-year framework is estimated at C$15 million (at fixed prices which include annual inflationary adjustments) and a value across a fully extended eleven-year term on the same basis of up to approximately C$35 million.

This is £1.6m/year or 12% of Pennant’s forecast revenue. However, reading the details from their broker (Cavendish), Pennant has had an ongoing relationship with the Canadian DND dating back over 20 years. This agreement appears to be more a formalisation of existing work.

Overall, Cavendish say:

The contract award helps build confidence over our current forecasts.

i.e. it was already in the numbers. They follow up with:

Pennant’s valuation remains at a discount to peers, trading on an FY27E EV/adj EBITDA multiple of 5.7x versus its UK small cap data and productivity software peer group on 6.5x.

However, that is hardly a big discount at 14%, and has virtually been closed by the share price rise in response to today’s news.

I would argue that this company should probably trade at a discount to peers, given that it has negative working capital and negative tangible assets. A situation that Cavendish don’t predict will change anytime soon.

Mark’s view

We’ve been highly negative about this company in the past. They used sale and lease backs of freehold property to fund ongoing losses, putting them in a particularly precarious position. Today’s rise looks excessive for what appears to be a formalisation of an existing relationship and was already in forecasts. Plus the broker’s preferred valuation method leaves little upside and is based on highly uncertain 2027 estimates.

However, today’s contract news, even if expected, shows that they do have a product that is valued by end users and embedded in defence systems. I don’t think they are completely out of the woods financially, so it is right to remain mostly negative, but it no longer looks like it’s going under imminently, so I think we can afford to be slightly more positive. AMBER/RED.

M P Evans (LON:MPE)

Up 1% at 1522p (£784m) - Trading Statement - Mark - AMBER

MP Evans has been a momentum favourite over the last few years, and appeared in Ed’s latest smooth trends article...until that smooth trend was broken:

The issue was an announcement by the Indonesian government of a change in the way that palm oil exports would be treated. The company address this head-on in this AGM update:

As reported in the Group's announcement on 20 May 2026, the Indonesian government is planning some changes to the way in which certain commodities, including palm oil, are exported from the country. The Group understands that changes will not be implemented until the start of 2027, and that the primary purpose of any change is to ensure that all exports are properly recorded and accounted for at the appropriate values. The Group does not export crude palm oil ("CPO"), but sells to domestic Indonesian refineries, and it continues to trade with its refining customers in the normal way. As discussed in the pricing section below, we have not seen any significant pricing changes from our customers within Indonesia following the announcement.

It seems the company expects no real impact from the changes to their business, which sells locally to refineries. This makes the recent share price move look like an overreaction. However, I am not immediately running out to buy shares in the company. Let me explain why.

Crude Palm Oil (CPO) and Palm Kernel Oil (PKO) are two distinct oils extracted from the same fruit of the oil palm tree.

Crude Palm Oil (CPO) is extracted from the red, fleshy outer layer of the palm fruit and is largely used in the food industry or as biofuel.

Palm Kernels (PK) are the hard seeds at the centre of the fruit. Mills crush these seeds to produce Palm Kernel Oil (PKO) and a high-protein byproduct called Palm Kernel Cake (PKC). These are used for personal care products, confectionery, or, in the case of PKC, as animal feed.

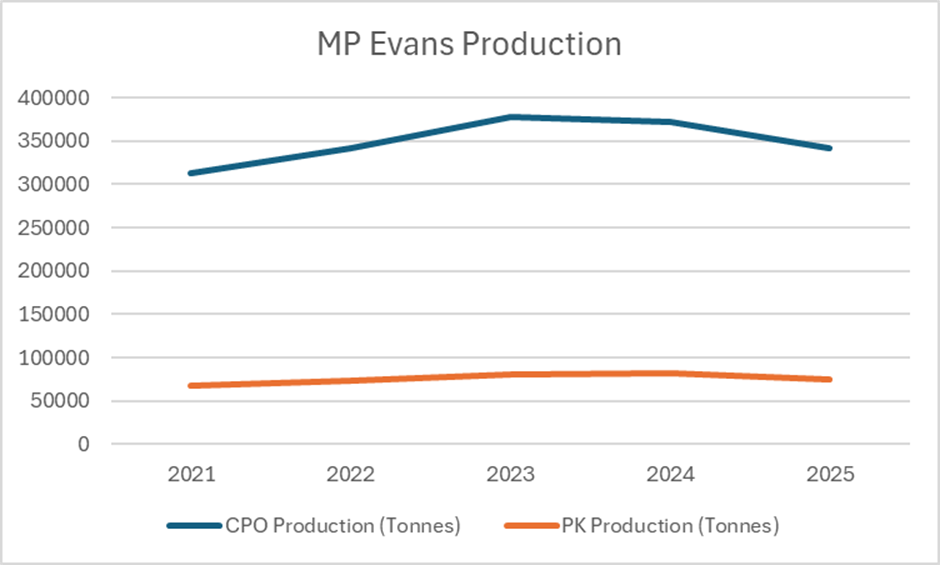

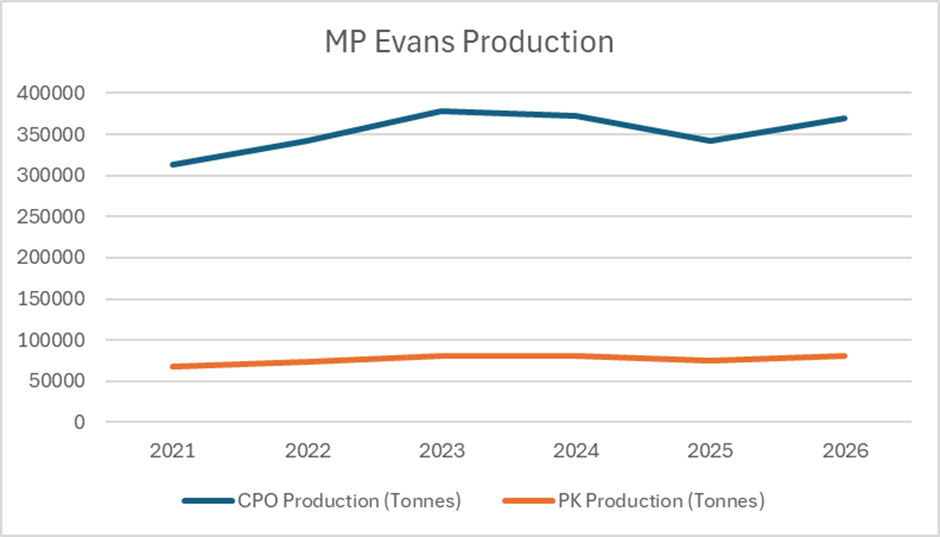

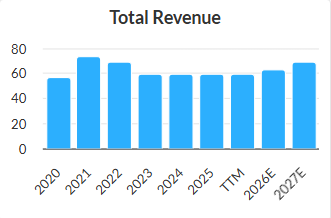

MP Evans produces both products, with CPO representing 82% of production by weight. Production of both has been relatively flat over the last few years.

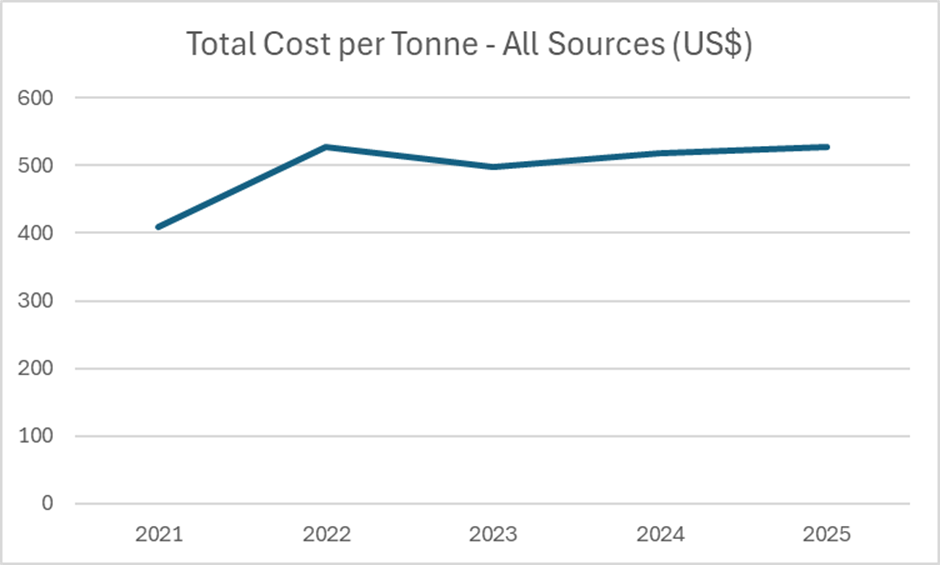

Costs have largely been flat:

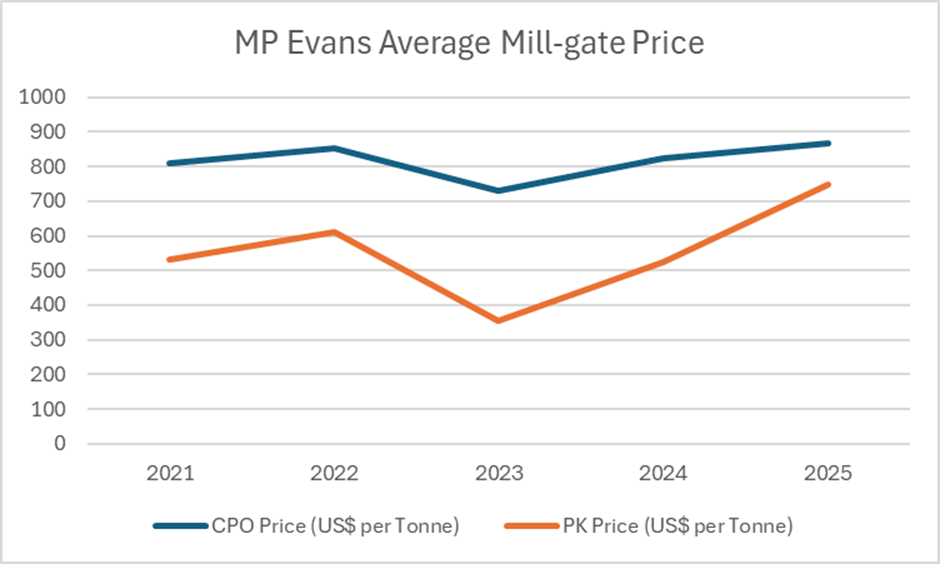

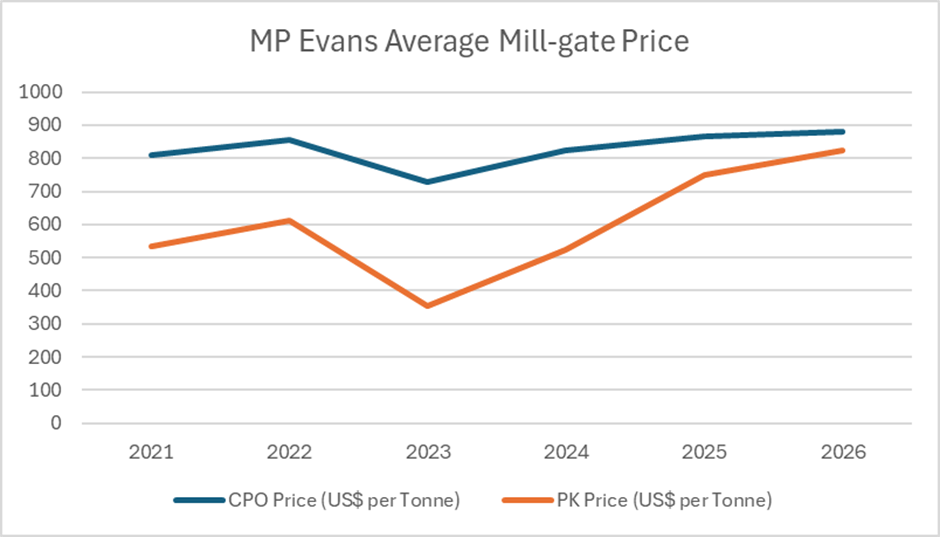

Mill-gate prices for CPO have also been largely flat. So, why has the MP Evans share price been on such a tear, making it a smooth-trends favourite? The answer lies in PK pricing:

Because PK is a secondary byproduct of harvesting palm fruit for CPO, its supply cannot easily be increased on its own. If global CPO production slows down, the supply of PK drops too. CPO prices are closely tied to the global food commodity and energy sectors. PK prices are tied to the consumer goods and chemical markets. Demand spikes with industrial manufacturing of household cleaning and personal care products.

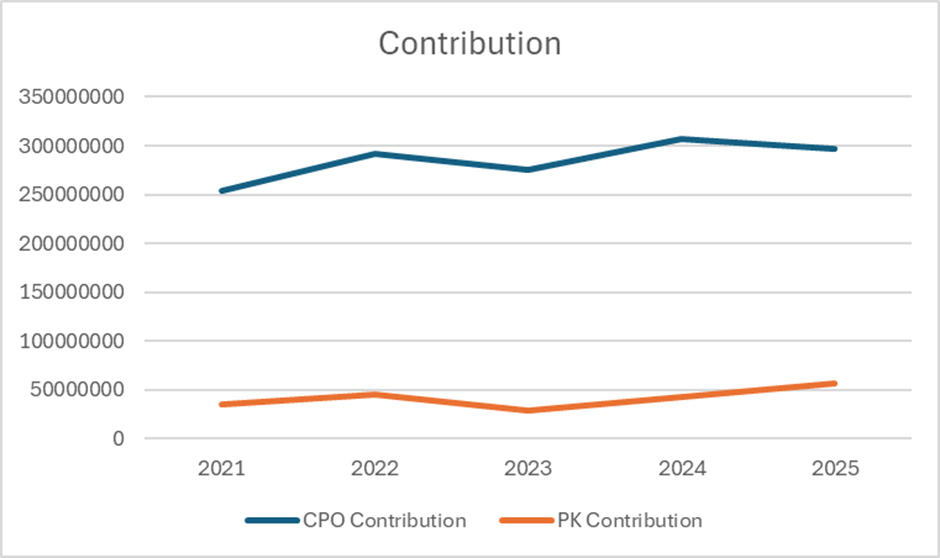

The difference between these market cycles makes PK pricing highly volatile. In 2023, PK prices were half those of CPO. Today, they are almost the same. The impact of this can be seen in the contribution to revenue from PK, which again has doubled off 2023 lows:

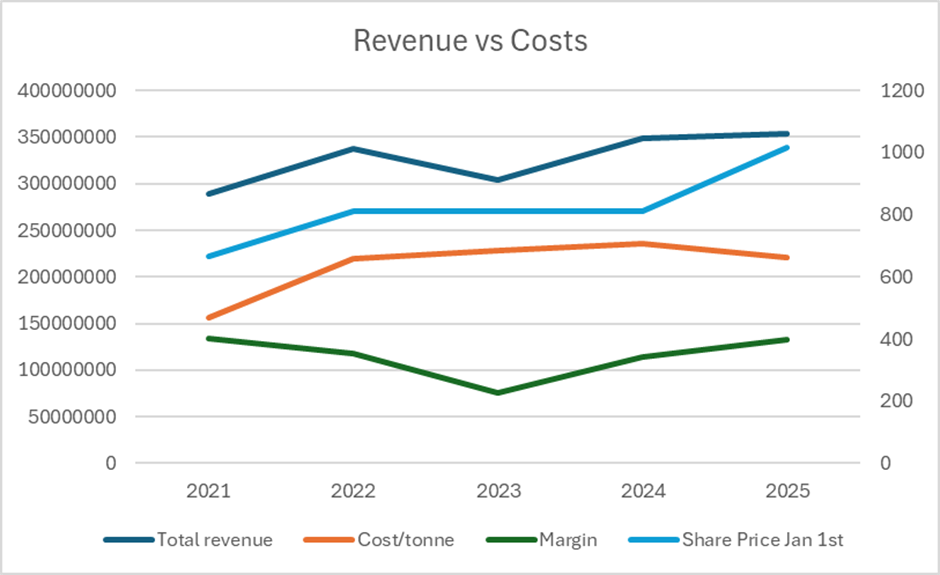

It is this strengthening PK price on a largely fixed cost basis, which means forecasts have been continually upgraded:

A widening gap between revenue and costs leads to much greater profitability. However, it is worth noting that, at least compared to 2021/2, the current share price strength is largely a re-rating of the multiple, rather than due to stronger profitability:

Of course, the market is forward-looking, and helpfully, in today’s update, they provide us with details of current trading:

CPO production up by 8% to 157,600 tonnes with 82% certified sustainable

Pricing remained strong, with mill-gate CPO prices US$880 per tonne, and PK prices US$824 per tonne.

Production costs are stable, with input increases mitigated by energy generation and a weaker Indonesian Rupiah

If I assume these trends are representative of the full year, I can add 2026 to my graphs.

Production is up, but only just returning to 2024 levels:

CPO pricing is stronger, but again, it is largely a story of the narrowing gap in PK pricing:

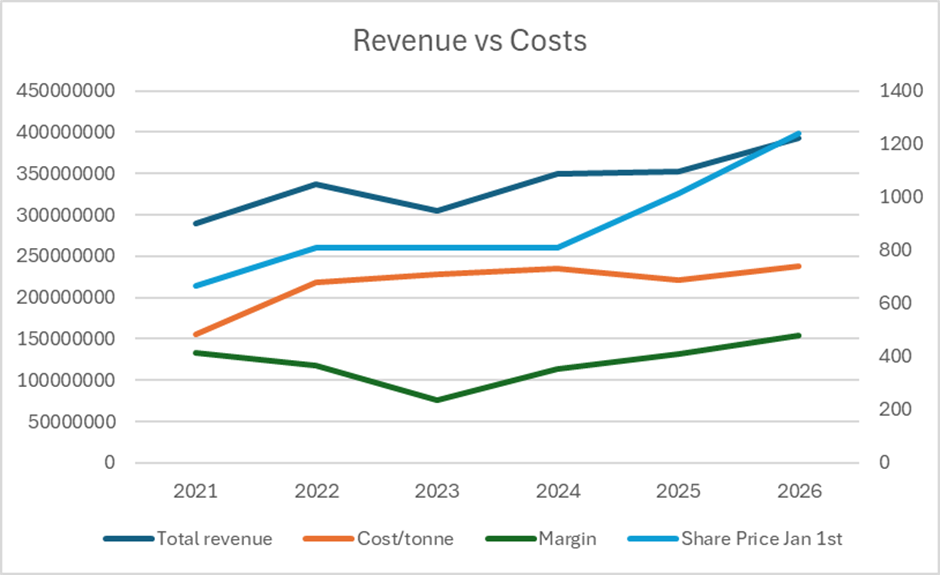

With flat costs, profits will be up, but then so is the share price:

With today’s share price higher still at around 1500p. Again, this appears to be a significant re-rating of the shares compared to previous periods when the profitability was at similar levels.

Conclusion:

TL; DR - The company has performed well largely because of the strength in PK pricing, rather than significant increases in production or CPO pricing over the long term. This has led to multiple upgrades and has led to strong Momentum. However, the multiple the market is willing to pay has now doubled compared to the last time production and pricing were at these levels.

The forward P/E is not expensive at around 10x, and it remains a Super Stock:

There is likely to be some production growth to come from the new estates they have bought and replanted. However, all three Ranks will still take a significant tumble if CPO and PK pricing drop in the future.

At the current share price, shareholders have to be confident of further price rises in what is, at the end of the day, a commodity product.

Shareholder Returns:

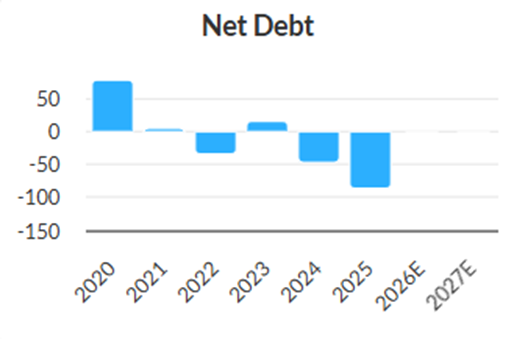

The good news is that the recent strength in PK pricing has led to strong cash flows, with the company building a cash pile and not being shy about returning it to shareholders:

Today they say:

An increased final dividend of 42p per share has been proposed in respect of 2025, which would result in total dividends in respect of the year being a record 60p per share, and it remains the board's intention to continue the Group's long-term trend to increase, or at least maintain, dividends for shareholders.

60p is around a 3.9% yield on the current price, which isn’t too bad. Plus, there is an ongoing share buyback program. To be fair to them, they have been consistent buyers of their own shares since 2022. However, with the shares on double the valuation than when they started, in a cyclical commodity industry, there is a risk that they are now buying back at the top of the cycle.

Broker’s forecasts:

Cavendish increases their price target this morning, but presumably due to the share price approaching the old one! Their valuation methodology is based on a per-hectare model. However, this is surely a factor where the productivity of the land and the pricing of the commodity matters.

They have firmed their future pricing assumptions, but still expect EPS to fall from around 205 cents this year to 175 cents in 2028. This puts the company on a forward EV/EBIT of around 9, which is perhaps a little punchy for a commodity producer. Of course, there is scope to beat (or miss) these numbers if commodity pricing rises (falls) further.

Mark’s view

Roland reduced his view to AMBER recently on the news of the change in Indonesian government policy on exports. While this doesn’t seem to have any obvious short-term impact on the profits of MP Evans, it means that the Momentum Rank is now falling. With the rating the market is willing to give this commodity producer, having doubled in the last few years, one has to question how much of the recent rise has been based on Momentum trading rather than a belief in the changing fundamentals.

At the current share price, the potential for future returns almost certainly comes from one’s view of the underlying commodity pricing. Those who see tight markets for CPO, and in particular PK, will expect the company to beat expectations and will want to hang on. Those who see current pricing as towards the top of the cycle will use the current drop in Momentum as a signal to exit. In such situations, the commodity-price agnostics, such as myself, will take a neutral view. AMBER

McBride (LON:MCB)

Down 10% at 149p (£290m) - Trading and Acquisition Update - Mark - BLACK/AMBER

As you would expect from an unscheduled Friday trading update, it is bad news:

…the Group now expects FY26 and FY27 adjusted EBITA to be between 5 and 10% lower than current analysts' expectations

The blame is put on the delays in being able to pass on rising input costs to customers. With gross margins in the mid-30s anything like this will have an outside effect.

This seems to have caught some of the brokers by surprise, as I can’t see any updated coverage, nor does Zeus give us a specific EBITA figure. The company do give us a consensus, though:

Group-compiled consensus for adjusted EBITA for the year ending 30 June 2026 of £64.2m and for the year 30 June 2027 of £70.6m

Some quick guesstimates suggest to me that mid-case EPS is probably down around 10% making the 10% fall in share price in line with that.

Strangely, it appears that the market hadn’t been pricing in this rather obvious commodity price concern, with the shares rising off April lows:

Valuation:

With me guesstimating the same EPS fall as the share price, many of the valuation metrics remain about the same. And the shares look cheap on a P/E of around 7. However, there is also around 1.5x EBITDA of net debt, and EV valuations don’t make it look that cheap for a relatively low-margin business unless (previous) broker forecasts for accelerating growth in 2028 come to pass.

If the business can grow again, with a ROCE of around 30%, then things may look interesting. However, it is worth noting that the high ROCE is achieved through having a negative working capital model. If recent weakness is a sign of more to come, the combination of net debt and negative working capital makes this quite risky.

Mark’s view

We take the impact of profit warnings seriously on Stockopedia, as the evidence suggests that the first cut is rarely the deepest. However, in this case, the impact is relatively minor and largely due to cost-pass-though timing. Hence, it makes sense to maintain our neutral view, balancing the possible upside from the current valuation if things go well with the obvious risks if they don’t. AMBER

Virgin Wines UK (LON:VINO)

Down 13% at 29p (£15.9m) - Trading Update - Mark - BLACK/AMBER/RED ↓

Staying with the theme of unscheduled Friday updates mostly being warnings, after some extensive pre-amble about warehouses, Virgin Wines finally get to the crux of the matter:

The Company now expects FY26 revenue of c.£61m, FY26 EBITDA1 of -£200k and FY26 PBT of -£1.5m.

If it isnt already clear from the tone, the footnote makes it explicit that this is below previous expectations for £63.25m in revenue, EBITDA of +£100k, and PBT of -£1m.

The blame has been put on rising costs and weak consumer sentiment:

The current macro environment, exacerbated further in recent months by the effects of the war in the Middle East, continues to exert pressure on consumer confidence and discretionary spend. Whilst the business has worked hard to mitigate the material increases in costs, particularly with regards to increased duty and EPR, it has proved difficult to eliminate these completely when partnered with a worsening consumer environment.

It looks like Graham may have been a bit premature going neutral on this company at 50p in October 2025. Although, to be fair to him, he can’t have been expected to predict a Middle East war.

On the plus side, they did report significant net cash of £10.6m at 2nd January in their Interim Results released in March. This compares favourably to a now £13.8 m market cap if we exclude shares in treasury. However, the company hasn't exactly “return[ed] over £2.7m to shareholders via share buybacks” as they claim in their Interims. They have bought back shares at a premium to the current price and not cancelled them, suggesting that these will appear as management LTIPS at some point.

It is also worth noting that the source of their cash is largely customer pre-payments for wine yet to be delivered. NTAV is around £9.7m at the half-year, so this isn’t an asset play.

The company says that the losses are due to its growth strategy, but there is little sign of that in the figures:

We always worry when a company fails to generate positive EBITDA figures, as is now the guidance following today’s update. This would seem to be a bare minimum for a sustainable business, especially for a company that has now been listed for 5 years.

Mark’s view

At the risk of playing stance ping-pong, I feel we have to go back to a broadly negative view. The company's cash balance, due to the cash it receives upfront from customers, gives it a significant cushion to turn things around. However, any company that has been listed for 5 years and still reports negative EBITDA has to have significant questions still hanging over its long term future.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.