Good morning. Markets are expected to rise today, as it seems the TACO trade (Trump Always Chickens Out) is back on again.

The US President announced a deal with Iran on Sunday that will extend the current ceasefire by 60 days and see Iran reopen the Strait of Hormuz for toll-free commercial traffic. In return, Iran will receive some sanction relief and undertake not to develop nuclear weapons.

The thornier topic of the Islamic Republic’s 9,000kg stockpile of enriched uranium has been kicked down the road for future talks, according to press reports.

Iran’s regime has also survived this conflict intact and we might argue that Trump’s original pledge to deliver an “unconditional surrender” appears to have been watered down somewhat. Even so, this looks like good news for markets and for the wider global economy. Assuming traffic gradually starts to flow from the Strait, we should hopefully see commodity bottlenecks and inflationary pressures ease over the coming months.

Of course, to date the ceasefire has seen numerous military acts by both Iran and the US, so the current deal may not bring complete peace. There could be a period of uncertainty before commercial activity in the Strait and the wider region returns to normal.

It may also be worth noting that while the deal is said to support a broader peace across the region, Israel is not signing.

Finally, it would be remiss of me not to mention that SpaceX closed up by nearly 20% on Friday, at $160.95!

Overnight market movements:

The FTSE is set to open up 0.7% at 10,542

S&P 500 is set to open up 1.3% at 7,524

Brent crude is down 4.4% at $83.50/bbl

Gold is up 1.7% at $4,288/oz

Bitcoin is up up 2.1% at $65,698

Spreadsheet accompanying this report: link.

The agenda is now complete.

Companies Reporting

AstraZeneca (LON:AZN) (£209bn | SR79) | Truqap will be the first targeted treatment for PTEN-deficient metastatic hormone-sensitive prostate cancer, based on trial results which prospectively defined PTEN-deficient disease and showed Truqap combination reduced risk of radiographic disease progression or death by 19%. | ||

Frasers (LON:FRAS) (£3.55bn | SR88) | Frasers owns 22.9% of Australian retailer Accent (ASX:AX1) and has made an offer of A$0.65 per share (nil premium to Friday’s close) for the remainder. This would be equivalent to a consideration of A$316m (c.£166m). | ||

Big Yellow (LON:BYG) (£1.7bn | SR38) | Sale of industrial estate in Harrow, London for £38.4m. Proceeds will be used to build out 11 new stores and one replacement. The new stores are expected to generate £35m net operating income, representing a return of 16.5% on the £212m cost to complete. | ||

AEP Plantations (LON:AEP) (£631m | SR97) | Own FFB production -2.7% YTD, with CPO production -1.8% and PK production unchanged. Positive contribution from recent acquisition. Outlook: “... we remain confident of achieving market expectations” | AMBER ↓ (Mark) The similarities with MP Evans (reviewed last week) are striking. Both companies have delivered strong shareholder returns recently due to a recovery in production volumes and better commodity pricing. However, brokers are now forecasting EPS to fall due to forecasts for Palm Oil prices to peak. I have no idea if that is realistic or not. My reduced view is not a judgement against the company operationally, just that my neutral view reflects that the major multiple re-rating has already occurred and any future returns will be entirely dependent on where we are in the commodity cycle. As a commodity-price agnostic investor, I think we simply have to take a neutral view, despite the algorithms still liking the historical numbers. | |

Iqe (LON:IQE) (£607m | SR33) | Multiyear agreement with Tower Semiconductor (NSQ:TSEM) to supply InP epiwafers for “optical connectivity solutions serving AI-driven data centre infrastructure”. Under a separate agreement, Tower will also provide a broad and royalty-free licence to IQE for porous silicon patents, settling an ongoing IP dispute between the companies. | ||

Luceco (LON:LUCE) (£466m | SR93) | CEO John Hornby is retiring after 21 years leading the business. He will take a sabbatical until late August 2026 and remain CEO until 31 December. The search for a replacement is underway. Trading for the year to date remains consistent with commentary on 19 May. | AMBER ↓ (Mark) | |

VAALCO Energy (LON:EGY) (£425m | SR50) | Successfully completed and placed on production the Ebouri-5H development well in offshore Gabon. Achieved excellent initial flow rate of 8,000 gross bopd (4,700 net to Vaalco). Completed HE-9 well in Egypt, initial flow rate of 529 gross bopd. | ||

Metals Exploration (LON:MTL) (£379m | SR67) | This is a 440-hectare licence area in Barangay Balatoc, Northern Luzon, Philippines. Management believes this area is highly prospective, with previous exploration drilling showing “at least two porphyries”. | ||

Henry Boot (LON:BOOT) (£226m | SR43) | Arcadis has taken the whole 1st floor (10,300sq ft) of the Island office project in Manchester, at £48/sq ft. Including space under offer, Island is now 66% leased, with only three floors still available. | ||

Seeing Machines (LON:SEE) (£204m | SR22) | Has secured contract awards to supply its Driver and Occupant Monitoring System to two separate Japanese car manufacturers. In total, these programs are expected to generate an estimated lifetime value of c.$11m. | ||

Invinity Energy Systems (LON:IES) (£176m | SR23) | Sale of a 32 MWh battery system to Pacific Steel Group, a leading reinforcing steel fabricator in the United States, for installation at their Mojave Micro Mill project in Kern County, California. Delivery of the batteries is expected to commence in Q1 2027, with associated revenues recognised at that point. No figures given. | ||

Phoenix Spree Deutschland (LON:PSDL) (£157m | SR32) | €23.1m of condominium sales were notarised in the five months to 31 May 2026. Activity continued throughout the period and is tracking in line with the Company's full-year 2026 target of €55m. | ||

Beeks Financial Cloud (LON:BKS) (£137m | SR20) | Has secured a five-year software contract with an existing analytics customer for the deployment of Beeks Analytics and Market Edge Intelligence, with a total contract value of $3.0m. | AMBER = (Roland) Beeks’ share price has now retraced the losses seen in March, when the company’s half-year results left us speculating on the likelihood of an H2 profit warning. That risk now seems to have receded, although there’s no explicit mention of meeting FY26 expectations in today’s update. With the stock now trading on a P/E of >20 and no change to forecasts today, I’d like to see evidence of improving profitability before considering a more positive view. | |

Peel Hunt (LON:PEEL) (£119m | SR69) | Revenue +57% to £143.5m, PBT £21.1m (FY25: £2.5m LBT), Adj. PBT £32.0m (FY25:£0.8m). Capital base remains comfortably in excess of minimum regulatory requirements. “While markets remain supportive of high quality transactions, renewed global inflationary pressures, the volatile outlook for benchmark interest rates and increased domestic political uncertainty have all weighed on UK market confidence and therefore transactional activity since the start of our financial year." | AMBER/GREEN ↓ (Roland) Peel Hunt’s FY26 results look very strong and support Graham’s previous positive view on the company’s performance last year. However, the outlook for the year ahead remains uncertain. While we don’t have access to updated forecasts today, FY27 broker estimates prior to today suggested a big drop in earnings is possible this year. While market conditions may improve, visibility seems poor and I am not sure Peel Hunt can decouple itself from wider market conditions. On balance, I think a slightly more cautious view may be appropriate at this stage, so I’ve moved our view down by one notch today. | |

Brave Bison (LON:BBSN) (£102m | SR40) | Professor Mark Ritson, has exercised his full option for a total consideration of £2 million at 49 pence per Share. Now owns 7% of the company. | ||

Team Internet (LON:TIG) (£97.2m | SR58) | FY25 revenue -40% to $482m, Adj. EBITDA -54% to $42.7m, Operating Loss $49.9m, in line with or above analyst expectations. FY26 remains in line with expectations. Completed a renegotiation of its existing debt facilities with wider covenant headroom. Still engaging with a range of debt providers. | ||

Intercede (LON:IGP) (£67.4m | SR34) | An extension of its partnership with Swissbit to begin active development of an end-to-end FIDO2 Passkey offering the ability to utilise post-quantum cryptography. | ||

Zambeef Products (LON:ZAM) (£28.9m | SR94) | Basic Earnings per Share for the period ending 31 March 2026 is expected to be approximately 112% higher than last year. No change to the most recent market expectations. | ||

Rome Resources (LON:RMR) (£25.7m | SR24) | Commencement of a small-scale tin mining programme at its Kalayi project in the Democratic Republic of Congo. Mining operations are anticipated to generate modest revenues. | ||

Sealand Capital Galaxy (LON:SCGL) (£16.4m | SR-) | Revenue +12,700% to £1.55m, LBT £1.45m (FY24: £350k LBT). £9 million raised post period-end | ||

Mission (LON:TMG) (£16.1m | SR60) | Trading in the current financial year remains in line with the Board's expectations. | AMBER/RED ↓ (Mark) This is an inline update but it also seems we didn't get the chance consider our view once the FY results were released. Having now reviewed the FY numbers, I don’t think we were negative enough in the past. A large EPS miss, even on very heavily adjusted figures, and worrying working capital movements, leave me with little confidence that today’s in line statement will reflect underlying economic reality when the true figures are revealed. | |

Fusion Antibodies (LON:FAB) (£15m | SR3) | UK Research & Innovation has agreed to extend the project from its originally targeted completion date of 31 October 2026 to 31 December 2026. Total Grant funding is over £808K of which up to £545K of direct non-dilutive funding available to Fusion | ||

Quantum Helium (LON:QHE) (£11.2m | SR12) | Extended Production Test confirms helium-bearing gas of 2.5%, reservoir connectivity and commercial oil production from the Leadville Formation. | ||

Bradda Head Lithium (LON:BHL) (£10.7m | SR29) | Surface sampling assay results at the Whistlejacket Lithium Project: 18 samples exceeding 0.59 % Li2O out of 60 samples |

Roland's Section

Beeks Financial Cloud (LON:BKS)

Up 12% at 225p (£154m) - Third Market Edge Intelligence contract win - Roland - AMBER =

On Monday last week, I commented that it had been a tight race to meet FY26 revenue forecasts for the year ending on 30 June.

On Wednesday, Beeks announced further contract wins and I noted the broker’s view that Beeks was “largely on track” to meet FY26 revenue forecasts.

Today’s last-minute contract win will bring a further unspecified amount of revenue into FY26. However, at the risk of sounding cynical, the wording of the announcement does make me wonder if this is largely a renewal, with Market Edge Intelligence bolted on (my emphasis):

The customer, a leading North American exchange operator, has expanded its deployment of Beeks Analytics and will also deploy Market Edge Intelligence® in New York. Revenue recognition is expected to commence immediately.

A five-year deal with a total value of $3m implies $0.6m of revenue, annualised. Actual revenue recognition may not be on a straight line basis, but we aren’t given this information.

Indeed, given the proximity to the year end on 30 June, I can’t help wondering if the customer may have been offered favourable terms in order to bring some revenue forward into FY26.

Outlook: there’s no mention of FY26 expectations in today’s update, perhaps surprisingly at this stage.

In general, I would expect a company to reiterate its confidence in full-year guidance in a contract win announcement late in the year.

Roland’s view

Beeks’ share price has now retraced the losses seen in March, when the company’s half-year results left investors (including us) speculating on the likelihood of an H2 profit warning. That risk now seems to have receded:

Investors also seem excited about the prospect that Beeks’ new Market Edge Intelligence product could help the company become a higher-margin and more SaaSy business, potentially justifying a higher valuation multiple.

I can see this picture too, but I would like to see some concrete evidence first – Beeks has consistently been a low-margin and capital-intensive business in the past and we don’t yet have much information on the contribution Market Edge Intelligence is expected to make.

With a forward P/E of c.22 and no change to forecasts today (that I can see), I am leaving our neutral view changed. The StockRanks also remain cautious:

Peel Hunt (LON:PEEL)

Up 3% at 99.4p (£122m) - Full-Year Results for the year ended 31 March 2026 - Roland - AMBER/GREEN ↓

This City broker is on Graham’s watchlist. He took a positive view on the company’s trading update in March when Peel Hunt upgraded its FY26 guidance – albeit seemingly at the expense of FY27:

Today’s full-year results confirm an impressive recovery in revenue and profitability last year, but strike a more cautious note about the year ahead.

Of course, the company’s outlook commentary was probably written before news of an Iran peace deal was confirmed. It’s possible that today’s geopolitical news will encourage animal spirits among would-be acquirers and IPO candidates. This could boost demand for Peel Hunt’s services, particularly in its recently-opened Abu Dhabi office.

Results for y/e 31 March: key points

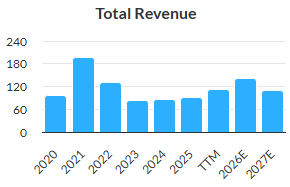

Peel Hunt’s financial performance improved dramatically last year:

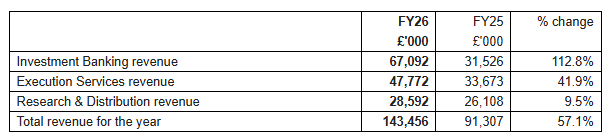

Revenue up 57% to £143.5m

Pre-tax profit of £21.1m (FY25: £(3.5)m

Adjusted pre-tax profit of £32.0m (FY25: £0.8m)

Earnings Per Share: 12.9p (FY25: (2.3)p)

Dividend: 4.9p (FY25: none)

The balance sheet also remains strong – asset backing and strong cash generation are notable attractions here:

Net cash up 136% to £26.9m (exc. leases)

Net assets up 22.3% to £108.5m

Balance sheet assets are almost all tangible and largely consist of securities held for trading and very large debtor/creditor positions (clients and market counterparties):

Market and client debtors: £642.3m

Market and client creditors: £575.3m

I would argue that Peel Hunt’s balance sheet strength and liquidity are an integral requirement of this business model, so the group’s net cash isn’t all surplus to requirements.

For businesses of this kind, I generally see dividends and buybacks as a more useful indicator of truly distributable cash.

For example, the 4.9p dividend declared today will cost around £6m, or about 40% of last year’s earnings.

One exception to this might be if Peel Hunt was acquired by a larger peer, when it might be possible to free up some additional distributable cash by combining two companies’ assets.

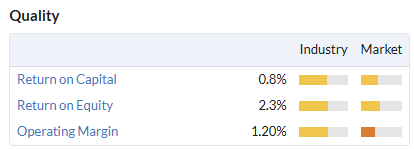

Profitability was very respectable – a characteristic of this type of business in good years:

Operating margin: 16.3%

Return on equity: 13.7%

Trading commentary

The biggest winner of the year was Peel Hunt’s investment banking business:

Investment Banking: although the company’s client base remains unchanged at 147 companies last year, the average market cap of its clients rose by 30% to £1,130m. This reflected the addition of one FTSE 100 firm and seven FTSE 250 clients to its roster, taking the total number of FTSE 350 clients to 62 (FY25: 52).

A number of clients appear to have been lost through the impact of M&A activity, although Peel Hunt also benefited from such activity, with “exceptional performance in our M&A advisory franchise”.

IPOs also made a positive contribution. While general IPO activity remains “relatively subdued in the UK”, Peel Hunt acted on the UK’s largest IPO last year (I think this may have been Princes (LON:PRN) ) and sounds confident about its ability to win future opportunities:

We are confident that our deep relationships with relevant private companies and their owners, as well as our ability to connect with a broad range of UK and international investors, will enable us to play a leading role in the revival of the UK IPO market over time.

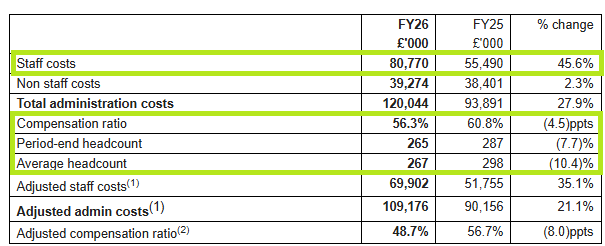

The upshot of the company’s involvement in fee-generating corporate activity was a 153% increase in investment banking fee income to £57.9m. Much of this appears to have cascaded through to bonus payments for employees, despite a reduction in headcount:

Execution Services: this business also performed well last year “despite ever-increasing competition”. Management says its focus is on using technology to strengthen connectivity and unlock incremental liquidity for clients.

Given that revenue from execution services rose by 41.9% last year, I am not sure this commentary really explains the full scale of the increase. I would hazard a guess that the macro backdrop and associated market volatility over the 12 months to 31 March also made a large contribution.

In FY25, for example, revenue from execution services only rose by 13.6% despite very similar management commentary.

Even so, it’s good to see Peel Hunt continuing to compete successfully in this market.

Research & Distribution:

Our business remained resilient in FY26, with moderately increased revenues. This is a good outcome given wider economic turbulence that included unpredictable US policies and market uncertainty in the run-up to the UK government's 2025 Autumn Budget.

A number of changes were made to Peel Hunt’s Research and Equities teams last year “including key internal leadership positions and a new management group”. These changes are said to have increased collaboration and also made it easier to retain “top talent”.

Peel Hunt opened a new office in Abu Dhabi in November to help expand its international distribution and liquidity reach. Commission revenue across its international offices is said to have risen last year, perhaps suggesting this is a more prospective area for growth than the mature UK market.

Strong relationships in Research and Distribution may also help Peel Hunt win other more lucrative business:

We saw this advantage in action in FY26, with the strength of our Research & Distribution division pivotal to us acting on the largest UK IPO of 2025. It also underpinned several capital markets transactions, including a significant capital raise for Coats Group plc.

Outlook

While markets remain supportive of high quality transactions, renewed global inflationary pressures, the volatile outlook for benchmark interest rates and increased domestic political uncertainty have all weighed on UK market confidence and therefore transactional activity since the start of our financial year. A sustained recovery in UK ECM, IPO and M&A activity will inevitably depend on greater macroeconomic stability and the pace at which confidence rebuilds.

Peel Hunt’s own broker is a subsidiary of Stifel and doesn’t make its coverage available on Research Tree. This means I don’t have access to any updated broker forecasts for Peel Hunt today.

However, the outlook commentary and the lack of market reaction today suggests to me that current expectations are largely unchanged.

On this basis, our consensus forecasts indicate earnings could fall sharply this year unless transactional activity improves:

FY26 actual EPS: 12.9p

FY27E adj EPS: 6.3p

These estimates leave Peel Hunt shares on a FY27E P/E of around 16x.

Roland’s view

Peel Hunt’s share price has not been very strong recently, perhaps reflecting subdued expectations for the year ahead. As I write, the stock is actually trading below the level at which Graham took a positive view on 31 March:

I think the outlook and valuation at this point are dependent on whether any of the momentum seen last year can be maintained.

Graham has rightly flagged up previously that broker forecasts were stale and too low. It’s possible that this is the case for our FY27 forecasts too, but I don’t see any way to evaluate this at present.

A look at Peel Hunt’s record since its 2021 IPO suggests the company has not yet managed to decouple its results from wider market conditions:

I think an AMBER/GREEN view could be more appropriate at this stage, to reflect the lack of earnings visibility and apparent double-digit valuation.

Mark's Section

Luceco (LON:LUCE)

For a share price to drop 11% on the planned departure of a CEO seems a little harsh:

…following 21 years of leading the business, John Hornby has decided to retire from the Group, with effect from 31 December 2026…John will be taking a sabbatical until late August 2026, and will remain as Chief Executive Officer and as a Board Director until 31 December, following which he will be available to the Group in an advisory capacity.

However, it is worth understanding that John Hornby has been a driving force behind Luceco over the years.

He originally joined British General as Operations Manager in 1997, before leading a MBO in 2000. He became group CEO in 2005 after a secondary buyout, with Luceco eventually listing in 2016. At IPO, he and his wife held a combined 20.8% of the equity, worth around £43m. Today that is around 15%, but he remains a multi-millionaire based on his successful running of the company.

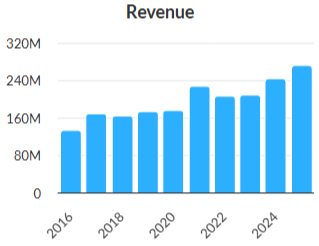

Since listing, the revenue has doubled:

However, the group has been highly acquisitive, so you would have expected it to grow.

It is the combination of an impressive 20% average ROCE, together with the ability to show positive operational gearing that marks this company out as having delivered great shareholder value during this period. With operating profit for FY26 confirmed in today’s update (and recently upgraded):

The trading momentum described in the Group's Q1 Trading Update published on 19 May 2026 has been sustained through Q2-to-date. The outlook for the year ending December 2026 remains consistent with the commentary provided in that announcement and accordingly, the Board continues to expect Adjusted Operating Profit to exceed £40m, with the potential for further significant outperformance dependent on Demand Flexibility.

This means that operating profit has grown by 4x since listing. Unlike many acquisitive companies, this hasn’t come at the cost of a greatly expanded share count:

Despite fairly consistent delivery, the share price has been on a volatile ride (not helped by COVID, Russia invading Ukraine and UK housing market challenges):

Hornby, together with other management stakeholders have not been shy to take advantage of excessive market enthusiasm or pessimism for the company.

Sizeable trades for Hornby include:

Selling at 235p in 2017

Buying at 40p in 2018

Selling at 300p in 2022

Selling at 269p last month

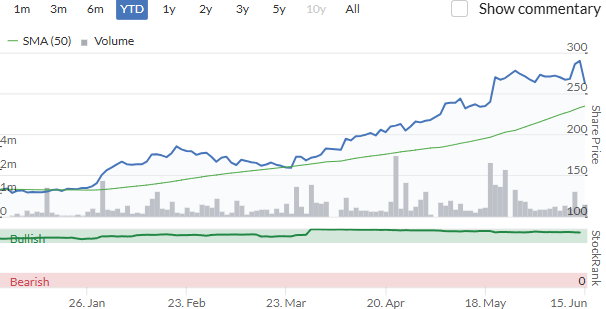

Zooming in to this year, the share price has doubled:

Driven by multiple upgrades in EPS:

However, it is worth noting that the actual increase in EPS forecasts is only around 20%, meaning that the Value Rank is now only 35. This remains a high flyer, given the recent trends, but remains vulnerable to any mean reversion is share price:

It is also worth noting that when I reviewed their FY25 trading update in January, all of the strength in trading was concentrated in the EV charging part of the business and their core RMI market sales appeared to be flat.

Mark’s view

I’m not generally a fan of investing (or selling) purely based on one’s view of management quality. However, Hornby has been a clear driving force behind Luceco (or its predecessor) for almost 30 years. His history of correctly calling the short term trajectory of the share price, combined with his recent sale of £3m worth of shares, makes me think that his resignation at this time is signalling something. Perhaps not that the share price is materially overvalued, but that it is at least now up with events.

In January with a share price of 148p, I was happy to keep our broadly positive view based on the undoubted quality of the business and modest rating. However, following a material re-rating, driven by upgrades in only one very specific part of the business, it is hard to argue that the shares are cheap. The algorithms still rate this as a High Flyer. However, this is exactly the sort of designation that investors will usually benefit from exiting on any sign of Momentum reversal. I’m not certain that Hornby’s resignation will be that trigger. However, there is enough uncertainty (as reflected by the share price drop today) that I think we should take a more neutral view of AMBER.

Mission (LON:TMG)

Up 3% at 19p (£16m) - AGM Trading Update - Mark - AMBER/RED ↓

This is a fairly short update, but may be re-assuring, given that they warned in January for their results that were announced in March:

Trading in the current financial year remains in line with the Board's expectations. Against an ongoing backdrop of wider macroeconomic uncertainty this has been driven by continued strong Client retention, new Client wins and the benefits of the strategic actions completed earlier in the year to simplify and strengthen the Group's operating platform.

It is pretty bad form, in my opinion, to warn by a material amount after the period has ended. It suggests to me either a lack of management access to the numbers, or an unwillingness to share them in a timely manner. So this makes me a little wary at taking today’s statement at face value.

We didn’t get a chance to look at the FY numbers on the DSMR, so I’ve taken the opportunity to review the figures today. Headline EPS came in at 2.0p, but printing the historical StockReport suggests that around 3p was forecast, with over 5p forecast before the January profits warning. So that was a material miss in my book.

Not only that, but there was a huge difference between statutory and adjusted figures. The bulk of these were non-cash intangible write downs, but few of the rest look like they are one-off:

Then we get to the supposed good news, that net bank debt was down £0.5m to £9.0m. This is a key figure as high debt levels have been a major concern in the past. However, again I have to question how much the figures at the balance sheet date reflect economic reality. Payables increased by almost £8m with flat receivables. Seeing these figures rise on heavily declining revenue is particularly worrying:

A more normalised working capital profile would see net debt significantly higher than the reported figure. Today’s update doesn’t contain any update on financial position.

It is not surprising that the market didn’t like these results. However, the share price seems to have inexplicably recovered recently, perhaps as investors look to the future. The rating here looks very cheap at a forward P/E of around 3 (presumably for the 18 month period following a change of accounting reference date), if you believe that they are trading in line, the adjustments reflect economic reality, and the debt is under control. Sadly, the recent results make me doubt all of those.

Mark’s view

Graham downgraded this to AMBER following the January profits warning. Having now reviewed the FY numbers, I don’t think he has gone far enough. An EPS miss, even on very heavily adjusted figures, and worrying working capital movements, leave me with little confidence that today’s in line statement will reflect underlying economic reality when the true figures are revealed. AMBER/RED

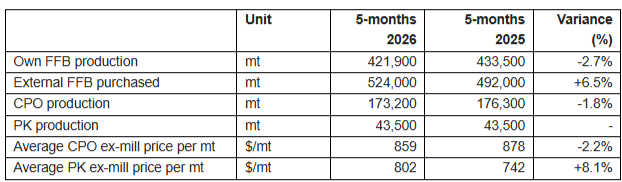

AEP Plantations (LON:AEP)

Up 2% at 1684p (£631m) - AGM Trading Update - Mark - AMBER ↓

AEP report a similar 5 month update to MP Evans did last week, and to me the recent story is remarkably similar. First they address the recent proposed changes impacting the industry:

Following the Indonesian Government's May 2026 announcement to centralise strategic commodity exports under PT Danantara Sumberdaya Indonesia ("DSI"), subsequent statements and a phased transition period have provided greater clarity. Exporters may continue direct overseas sales during the transition while meeting new reporting requirements to DSI, with full implementation expected from 1 January 2027. It is reported that DSI will serve as an intermediary facilitating and overseeing exports rather than acting as a trader; and that its mandate is to strengthen data-based supervision, not disrupt normal trading activities.

This policy does not directly impact the Group's business as the Group sells its CPO only to domestic refineries.

Again, minimal expected impact.

Then we get an update on production and pricing:

This includes a month of the Pinago acquisition, where they paid $162m for a 98.3% share.

This complicates matters slightly but I can make a guesstimate based on these trends to forecast the full year.

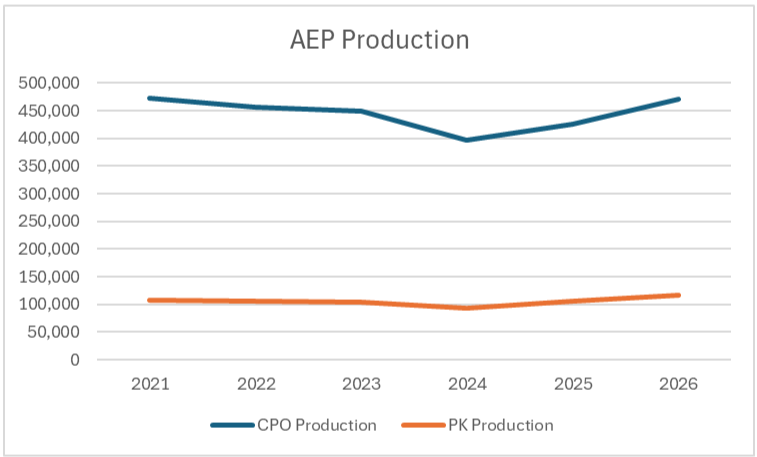

Like MP Evans, we are really seeing recent production growth as a recovery from a recent dip and the effect of the Pinago acquisition:

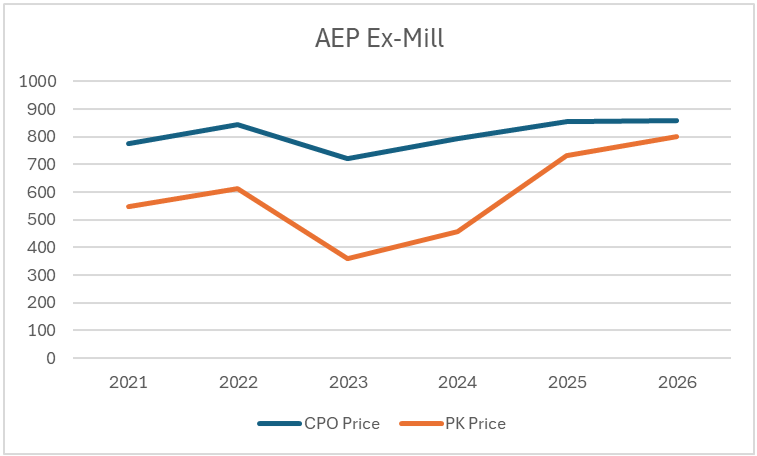

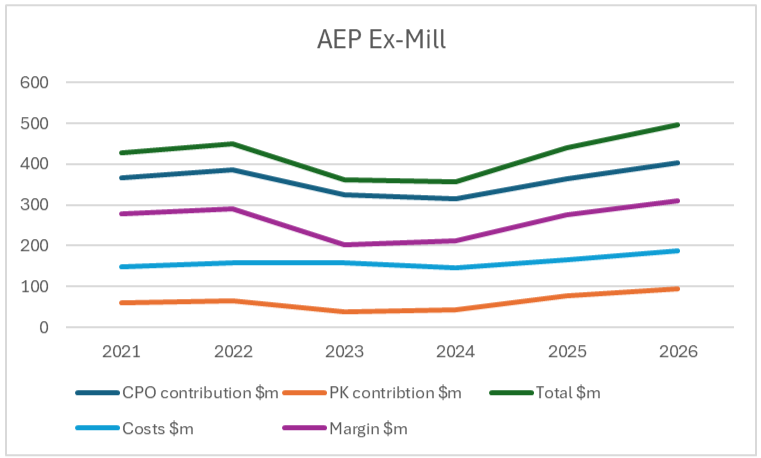

The recent strength in financials is mainly due to stronger pricing, particularly amongst the more volatile Palm Kernels:

[Note: AEP report Ex-Mill Prices versus MPE who report Mill-gate, the difference being who pays for transport.]

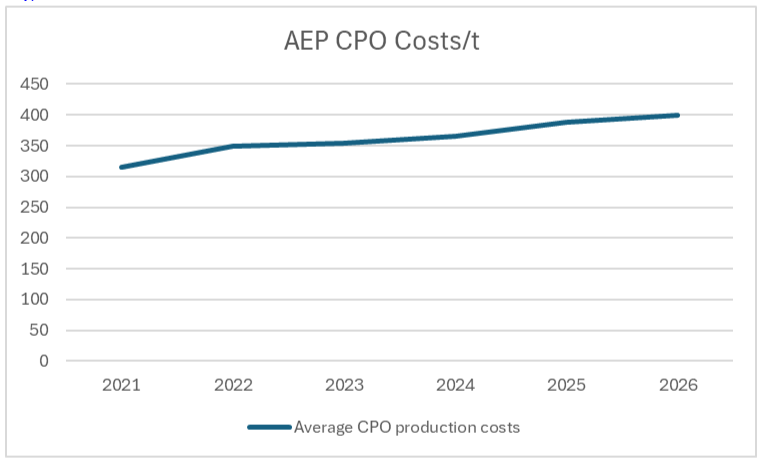

Costs continue to rise as you’d expect due to inflation. They don’t report separate PK costs but treat it like a by-product:

They don’t give us cost figures in today’s AGM update, so I’ve had to estimate based on an inflationary rise, offset by some scale advantages from the acquisition.

This still enables us to calculate an effective contribution and margin (a sort of operating profit without central costs):

So again, we see the margin recovering strongly, but only really back to 2022 levels, despite an acquisition this year.

However, the share price is now double where it was at the start of 2022, making the recent rise largely a re-rating by the market rather than a fundamental change in prospects:

There are some reasons to think that this isn’t entirely irrational. The company has become more shareholder friendly in recent years, with increasing dividends and an ongoing share buyback. Plus they have forecasts in the market, which they never used to. However, I would prefer if they’d been buying back their shares at £6 not £16. After all, the operational fundamentals of the business don’t appear to have changed much during this time.

This is an in-line update from the company, which means that the rating remains modest with a forward P/E of around 8. However, like MP Evans, analysts are expecting profitability to decline in future years based on lower commodity pricing. I’ve no idea if that is realistic or not, but there are good reasons to think commodity pricing for Palm Oil will always be cyclical.

Mark’s view

The similarities to MP Evans are striking. Investors have enjoyed strong gains here recently, but these are almost entirely down to positive moves in commodity prices, particularly the volatile PK pricing. While there are reasons for the AEP re-rating beyond simply commodity pricing - they have become more shareholder friendly of late - there is no escaping that future returns will almost entirely be dependent on where Palm Oil pricing goes from here. Personally, I have no idea whether Palm Oil prices will rise, fall or stay the same over the long term, so I just think we have to take a neutral view of AMBER.

We’ve been positive here most recently, so this feels like a big downgrade. However, that view has largely been driven by the algorithmic Stock Rank and recent upgrades. The Stock Rank remains high, but the last EPS forecast move was down, but a in many ways it feels like I should be positive on a 97 StockRank company:

However, I don’t think the StockRank can predict commodity pricing, and with the Momentum Rank starting to fall, the reasons for the commodity-agnostic investor to stay on board for purely technical reasons are starting to wane. I think consistency with MP Evans is also important as both companies are valued on similar multiples with similar outlooks. Palm oil bulls will want to own both for diversification; Palm oil bears, neither.

Of course, if any readers have done a detailed analysis of the global supply and demand characteristics of Palm Oil and feel they have a more informed view into where we are in the commodity cycle, I’d love to hear it.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.