Keir Starmer departure? The probability of Andy Burnham becoming PM this year has risen to 93% at Polymarket after a weekend which saw speculation intensify that Keir Starmer is going to announce plans for his departure. It is even possible that Starmer may make an announcement this morning. CONFIRMED (9:35): Keir Starmer announces that he will resign.

An example of the type of change that could be introduced by a Burnham premiership would be greater intervention in the utilities sector, i.e. water and energy.

Here’s the chart for the FTSE Gas Water & Multi-Utilities Index, which includes the likes of National Grid, United Utilities & Severn Trent. It has been under pressure since the Makerfield constituency was opened up for Burnham’s return to parliament in mid-May:

Iran talks: on Saturday, Iran said that it was closing the Strait of Hormuz after military action by Israel in Lebanon. But Indian tankers did make it through the Strait over the weekend. Negotiations between the US and Iran for a permanent peace deal continue, mediated by Qatar and Pakistan.

Overnight market movements:

The FTSE is set to open up 0.2% at 10,370

S&P 500 is unchanged at 7,478

Brent crude is down 3.4% at $78.70/bbl

Gold is up 1% at $4,195/oz

Bitcoin is up 0.5% at $64,190

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Babcock International (LON:BAB) (£5.13bn | SR22) | Revenue +8% organically. Underlying operating profit down 19% to £293.3m. Includes a £140m charge on a fixed-price contract (“Type 31 contract”). Outlook: For FY27 we expect another year of good progress, supported by strong revenue visibility with around 70% revenue under contract at 1 April 2026, a similar percentage to the prior year. We reaffirm our medium-term guidance… | ||

easyJet (LON:EZJ) (£3.82bn | SR42) | Castlelake offered 560p, then 600p, and 625p. “Following the rejection of three proposals by the easyJet Board, and given its unwillingness to engage meaningfully, Castlelake is announcing this Third Proposal to enable easyJet shareholders to consider its merits… “ | TAKEOVER (AMBER/GREEN =) (Graham) | |

Ocado (LON:OCDO) (£1.52bn | SR18) | “Ocado confirms that the CEO and the Board continually engage in long-term succession planning and regularly engage with potential candidates.” Sky News reported that Ocado was preparing to appoint a successor to Tim Steiner. | AMBER/RED = (Graham) [no section below] I'm surprised that Tim Steiner has remained as CEO for so long: he founded Ocado with two colleagues all the way back in 2000. Since then the business has been a puzzle: failing to generate much in terms of profits but always commanding a degree of respect from the financial markets. But over the past year, its usual underlying losses have continued and its ventures in North America have been scaled back by its partners Kroger and Sobeys. Overall, it's not a surprise that Steiner himself and/or the rest of the Board might be thinking about the future of the business under new leadership. | |

Great Portland Estates (LON:GPE) (£1.31bn | SR26) | GPE has completed the pre-letting campaign at 30 Duke Street St James's, SW1, following the exchange of a new retail lease with Australian menswear brand, M.J. Bale. | ||

Anglo Asian Mining (LON:AAZ) (£446m | SR57) | AAZ has appointed Worley Europe Limited as its contractor to complete the Xarxar and Garadag feasibility studies. The Company is planning a 90,000 metres core drill programme for 2026 and 2027. This comprises both exploration drilling of around 55,000 metres and drilling for the feasibility studies of around 35,000 metres. | ||

Avacta (LON:AVCT) (£344m | SR7) | "Avacta has continued its strong progress in the first half of 2026, initiating the clinical program with our Gen Two product AVA6103 and presenting updated data on the Gen One AVA6000, which further validate our unique pre|CISION® technology.” | ||

Empire Metals (LON:EEE) (£268m | SR8) | Exceptional drilling results confirm the scale and continuity of the high-grade weathered central core at Thomas. Final assays for Cosgrove Prospect and Exploration/Sterilisation remain pending, with further results expected late June and July 2026. These drill results will support a significant Mineral Resource Estimate upgrade which is targeted in Q3 2026 and provide the basis for future mine planning and engineering design studies. | ||

Synthomer (LON:SYNT) (£188m | SR70) | On track to deliver strong H1 revenue, EBITDA and margin progress relative to prior year. Substantial liquidity and covenant headroom. | AMBER/RED = (Mark) This update is somewhat reassuring; Q2 is ahead of expectations, and they are reporting plenty of headroom against covenants. However, the Q2 strength appears to be largely pull-forward demand, and I wouldn’t expect them to have an issue with the newly increased covenants so soon. The medium-term covenants still look challenging given their recent trend of business performance. Hence I think we should maintain our broadly negative view, at least until there is evidence that the EPS trend has well and truly bottomed and is now back on the upgrade path. | |

Ondine Biomedical (LON:OBI) (£81.4m | SR16) | The Longstop Date for completion of the transaction has by mutual agreement been extended to 31 July 2026. | ||

Clean Power Hydrogen (LON:CPH2) (£68.3m | SR-) | Re: incident at test site. The detailed cause of the failure remains under investigation. CPH2 “does not currently have the financial and scaled-up engineering resources required to complete a full manufacturing and re-testing process to demonstrate commerciality for eventual MFE220 production.” Will adopt a more capital-light business model. In discussions re: potential equity raise. Current cash balance is sufficient through to mid-July. | (Shares suspended since 29th May 2026.) | |

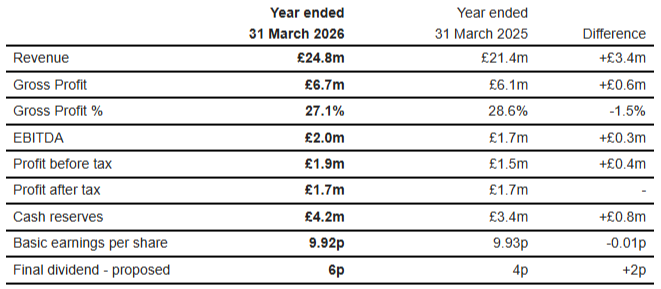

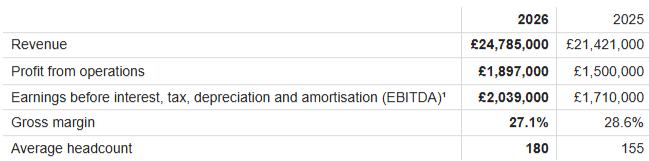

Triad (LON:TRD) (£49.7m | SR56) | Revenue +16% to £24.8m, EBITDA +18% to £2.0m, PAT flat at £1.7m, Cash £4.2m (FY25: £3.4m). “The outlook is very promising. Short-term, the new financial year has started well.” | AMBER/RED ↓ (Mark) These results are not bad, showing decent growth even though normalised tax rates mean this doesn’t drop through to rising EPS. The outlook is also positive. However, at the end of the day this is a small IT contractor with less-than-perfect corporate governance. A sector peer comparison suggests this company is likely to be at least two times overvalued at the current price. Given what I know from the history of the company and learnt by attending an AGM a few years ago, I hope readers will understand why I am a bit more negative than my colleagues. | |

Batm Advanced Communications (LON:BVC) (£48.6m | SR61) | Entered into a share purchase and loan assignment agreement to sell three out of four non-core activities, for a cash consideration of $13.3m. One of the Disposed Businesses has entered into an agreement for the sale of 96,794,500 shares in BATM at a price of 18.15p per share. | ||

80 Mile (LON:80M) (£46.2m | SR42) | Mobilisation activities underway at Disko-Nuussuaq nickel-copper-cobalt-PGE project in West Greenland for two diamond drill rigs. | ||

Cellbxhealth (LON:CLBX) (£19.9m | SR10) | Revenue -52% to £1.4m, Operating Loss £19.2m (FY24: £15.1m Loss), Cash £7.3m after £8.2m fundraise in period. FY 2026 revenues are expected to be at least £2.1 million. With a much-reduced cost base and more efficient operating model, the Company has a cash runway into Q2 2027. | ||

Eenergy (LON:EAAS) (£19.7m | SR52) | Conducted a detailed review of the pipeline of potential sales opportunities. Now expects FY26 Revenue of circa £32.0m and Adj. EBITDA of £1.7m. Down from £38m & £4.5m, respectively. Expected to reduce annual operating costs by almost a third and generate annualised total savings of circa £2.0m in FY26. | BLACK (AMBER/RED) (Mark) | |

Europa Oil & Gas (Holdings) (LON:EOG) (£17.8m | SR15) | Longstop Date for completion of the transaction has by mutual agreement been extended to 31 July 2026. | ||

Oriole Resources (LON:ORR) (£17.6m | SR29) | A maiden drilling programme for 19 drill holes is now underway at its 85%-owned Wapouzé limestone project. | ||

Eco Buildings (LON:ECOB) (£16.6m | SR5) | First apartment block in Albania now completed to second floor level. | ||

Fusion Antibodies (LON:FAB) (£15.6m | SR4) | The Canadian Intellectual Property Office has issued a notice of allowance in respect of the Company's Canadian patent application. | ||

Lexington Gold (LON:LEX) (£15.4m | SR7) | Net Loss $0.83 (FY24: $1.4m), Net Cash $0.3m (FY24: £0.9m) after a £530k fundraise during the period. £1.2m fundraise post-period. “The Company will continue to evaluate potential project-level partnerships, strategic funding structures and other corporate opportunities that could assist in advancing its assets while preserving shareholder value.” | ||

Solvonis Therapeutics (LON:SVNS) (£12.9m | SR7) | A nonclinical study was designed to assess whether the intended combined sublingual-buccal administration of SVN-002 could generate systemic esketamine exposure supportive of a scientific bridge to the approved intranasal esketamine reference product delivered positive results. | ||

Kazera Global (LON:KZG) (£10.5m | SR3) | executed a definitive settlement agreement with Hebei Xinjian Construction in relation to the previously announced arbitration award concerning African Tantalum. Kazera will receive total consideration of US$10.5 million, payable over a structured period ending December 2029. | ||

| Transense Technologies (LON:TRT) (£8.6m | SR51) | Trading update | FY26: Revenue of not less than £4.6m, Adj. EBITDA of not less than £0.5m, Adj PBT break-even, modest reduction versus expectations. Net cash £0.71m (31 Dec: £0.92m. FY27 expectations are being moderated to reflect the timing of conversion of advanced commercial opportunities. | BLACK (RED ↓) (Mark) |

Graham's Section

easyJet (LON:EZJ)

Up 3% at 518p (£3.92bn) - Possible Offer for easyJet & Rejection of Possible Offer for easyJet - Graham - TAKEOVER (AMBER/GREEN =)

Castlelake’s interest in easyJet was announced and discussed here on 1st June. easyJet described the timing of the approach as “opportunistic”, given that their share price was “temporarily depressed due to the current situation in the Middle East and its impact on customer confidence and jet fuel prices”.

The easyJet share price has recovered by a further 19% since then:

Castlelake made a fresh announcement this morning, revealing the following:

12th June - they made a 560p proposal.

17th June - they made a 600p proposal.

20th June - they made a 625p proposal.

They note that their third proposal was at a 59% premium to the last price before their interest became public.

They also describe the price they've offered as follows:

· a price above any closing easyJet share price since 25 February 2022;

· a price above all research analyst price targets published since 16 April 2026; and

· a price to 2027E earnings per share multiple of 16.5x.

They argue that even if easyJet achieved its target of £1 billion PBT in the medium-term and traded between its 5-10 year average earnings multiple, 625p would still be a good price.

EU ownership: Castlelake say that they respect “the form, spirit and importance of the EU ownership requirements”.

They have found two Irish airline executives who will own and control an EU company that in turn “will hold a controlling shareholding in the overall structure”, thereby complying with EU ownership rules.

This proposed structure is consistent with structures adopted by a number of other European airlines that are subject to the same EU ownership rules as [easyJet].

Funding: Castlelake’s own funds and commitments from co-investors along with the new EU company will fund the equity, while Goldman Sachs will arrange the debt.

Response from easyJet

The response from easyJet is an emphatic No:

The Board of easyJet carefully considered the Third Proposal with its advisers and concluded that it is highly opportunistic, delivered against the backdrop of easyJet’s temporarily depressed share price, and still fundamentally undervalues easyJet and its prospects.

The premium, multiple and future share price analyses presented by Castlelake are based primarily on Middle East conflict-affected share prices, short term earnings and analyst reports. They fail to reflect easyJet’s medium-term prospects, its strong balance sheet and capital structure and still less provide an adequate control premium thereto.

On top of that, “the envisaged ownership structure is opaque and does not present any basis for assessing the deliverability of the Third Proposal”.

In summary, easyJet says that this is “an opportunistic attempt to acquire easyJet “on the cheap””.

Graham’s view

I still don’t think that this takeover is very likely, although Castlelake’s proposal to have an EU company partner with them on it does at least show us how they think it could happen.

At the end of the day, it’s a question for easyJet’s shareholders: how do they feel about selling the company at 625p? How does the Haji-Ioannou family, owning 15%, feel about it?

Where I think Castlelake may have missed a trick is that they have failed to explain why they are willing to make such an allegedly generous offer to easyJet’s shareholders.

They’ve gone to great lengths to demonstrate how attractive their offer is.

But they should also tell easyJet shareholders why they are willing to make such an offer - it’s not out of the goodness of their hearts! Buyers normally offer some sort of rationale in this regard, as to why they are best-suited to own the business. This is the closest they come:

Castlelake's ambition is to support easyJet as a stronger, more resilient European airline under European control, respecting easyJet's valuable airline assets and continuing to sustain its network, serve the passengers who depend on them and enable future growth. Castlelake is committed to working constructively with employees, regulators and government, and to being transparent about its intentions throughout this process.

In the absence of a clear rationale as to why they are willing to offer easyJet shareholders such an allegedly generous offer, we are left to conclude that the offer is not all that generous in reality, compared to easyJet’s prospects.

Castlelake themselves, as we noted last time, have an intimate understanding of easyJet. They are an aviation specialist, and I believe they manage some of the airline's current leases. Therefore, if they are willing in theory to pay 625p per share, there is a very good chance that the company is worth at least that amount, if not substantially more.

Or, as I said last time, they might also want to highlight to the wider financial world the cheapness of easyJet shares. They already own 2.1% of the company, an investment that is currently worth over £80m. If another party is prompted to make a higher takeover offer by this affair, that won’t be a terrible outcome for them.

I’m going to keep us AMBER/GREEN on this today. The P/E multiple is expensive in the near-term, but earnings are expected to rebound sharply in the next few years. On forecast FY 2028 earnings, for example, the P/E multiple may only be in the region of 8.5x. This fact alone would go a long way towards explaining Castlelake's rationale.

Mark's Section

Synthomer (LON:SYNT)

Up 5% at 120p (£188m) - AGM trading statement - Mark - AMBER/RED =

I wrote a StockPitch on Synthomer back in August 2025, when it appeared on a 52-week low screen. With the share price around 60p, it looked like an interesting opportunity, as it was a very large business available for a sub-£100m market cap. I said that if investors accept that this is a cyclical business where trading will reflect global market conditions, there are signs that the company may now be undervalued. However, it was also highly risky, with excessive leverage that could have easily led to a debt-for-equity swap, or worse. So it was a value opportunity that I decided not to avail myself of. For a while, this looked smart, as the share price fell to a low of around 17p.

However, the share price has since made a huge recovery:

What caused the fall was fairly obvious. In February, the company confirmed media reports that it was considering a capital raise to support debt refinancing due next year. Roland downgraded this to RED to reflect those risks.

What appears to have triggered the recovery was the news in March that they did not intend to issue new equity as part of the refinancing. However, we remained sceptical, noting that in December, their largest shareholder had to step in with additional off-balance sheet receivables financing to make sure they were compliant with their covenants, and this is not included in these debt figures.

The recovery in share price continued after they announced a debt refinancing at the end of April, with relaxed covenants on net debt to EBITDA for 2026, 2027, and 2028 of not more than 6.25x, 5.25x, and 4.25x, respectively.

Recent trading:

Today’s AGM update has been well received, with the share price rising modestly. They say:

Synthomer achieved strong growth in Continuing Group volume, revenue, EBITDA and EBITDA margin in the first five months of 2026 compared with the equivalent prior year period.

Q1 has been in line with expectations and ahead of the prior year. Even better news: Q2 is ahead, with them saying “period-on-period volume, margin and EBITDA growth in Q2 has been ahead of our expectations.” However, many of the factors they list for the better-than-expected performance appear to be due to timing factors pulling forward demand.

It is also worth zooming out and putting that improvement in context. Here, there has been an almost continuous decline in broker forecasts over the last 18 months, with a further large lurch down recently:

In this context, it is hard to get excited about a strong couple of months, driven mostly by a pull-forward of demand.

Financing:

On the important financing side, they say:

Following the successful bank debt refinancing and maturity extension announced in April 2026, the Group has substantial liquidity and covenant headroom. This is notwithstanding the unwind as expected of the £50m receivables purchasing arrangement with KLK and the typical seasonal build-up in working capital in the first half of the year, reflecting the Group's usual H1-weighted activity levels and the recent higher pricing and volumes.

The good news is that the extraordinary receivables financing from the largest shareholder appears to be winding down. However, they don’t actually give us any figures to back up their statement of substantial headroom. I also wouldn’t expect them to have an issue so soon after refinancing and with a 6.25x net debt to EBITDA covenant. The issues, if they arise, will be in future years, as the covenants reduce by 1xEBITDA each year. They would either have to put all their EBITDA into repaying net debt (i.e., zero capex, not even a new pencil sharpener) or, more realistically, grow EBITDA significantly. Something for which the recent trend has not been promising.

What will help is their continued divestment program. For example, the recent sale of Acrylate Monomers reduces EBITDA losses by €10m, even though they receive no upfront consideration for exiting this, and appear to have to contribute €5m to working capital. The downside of transactions such as this, is that they limit the upside in their business when the recovery comes.

Mark’s view

This update is somewhat reassuring; Q2 is ahead of expectations, and they are reporting plenty of headroom against covenants. However, the Q2 strength appears to be largely pull-forward demand, and I wouldn’t expect them to have an issue with the newly increased covenants so soon. The medium-term reductions in covenants look challenging given their recent trend of business performance. They appear to require a recovery in EBITDA, as well as very limited Capex, and the continued divestment of non-core businesses.

While they were understandably reluctant to raise fresh equity when the share price was 17p, with the share now trading at 120p, the attraction of raising fresh capital with the narrative of investing for recovery growth becomes much higher. Despite the reassuring noises recently, raising fresh capital today rather than having the next three years of minimal capex and a firesale of anything they can get a bid for, looks like an attractive option. Perhaps I am reading this wrong, and they will surprise me with a big recovery in EBITDA that puts this uncomfortable period behind them. However, recent EPS forecast trends are not particularly encouraging. Hence I think we should maintain our broadly negative view, at least until there is evidence that the EPS trend has well and truly bottomed and is now back on the upgrade path. AMBER/RED

Eenergy (LON:EAAS)

Down 38% at 3.15p (£19.7m) - Trading Update - Mark - BLACK (AMBER/RED)

eEnergy has undergone a significant management overhaul recently. Three non-execs decided not to seek re-election at today’s AGM, including the Chairman. It is expected that another non-exec John Samuel will be appointed as the new Chairman at the AGM. Last month, CEO Harvey Sinclair stepped down by mutual agreement with the board. CFO John Gahan takes the reins on an interim basis.

Investors often have a love-hate relationship with management changes. When a company has been struggling, they can often signal a much-needed change of direction. It is no coincidence that activist fund managers, such as Rockwood Strategic, often seek to refresh a company’s board when they aim to drive a turnaround in prospects. However, in the short term, management changes come with a reset of expectations. The so-called “kitchen-sinking”.

Hence, that this AGM update is a negative one should perhaps not come as a huge surprise:

Following the detailed review and significant reduction in pipeline revenue, the Board now expects FY26 Revenue to be circa £32.0m (previously £38.0m; FY25: £19.0m) with FY26 Adjusted EBITDA of £1.7m* (previously £4.5m*; FY25: £2.2m*).

However, the scale of the disappointment is perhaps surprising, with full-year revenue expectations cut by 16% and EBITDA by 62% half way through the year. This is despite a recent cost-cutting exercise:

John Gahan was appointed as the Interim CEO in May 2026 and commenced a restructuring and cost saving exercise to simplify the reporting structure and right size the cost base. In total, this exercise is expected to reduce annual operating costs by almost a third and generate annualised total savings of circa £2.0m in FY26 (FY25 operating costs of circa £6.3m). The cost reduction exercise is expected to improve H2-26 Adjusted EBITDA by circa £1.0m. H1-26 will include an exceptional restructuring charge of circa £0.5m in respect of the restructuring exercise implemented in June 2026.

Without this, adj. EBITDA would be just £0.7m. The overall pipeline of opportunities is also reduced:

Following the appointment of John Gahan as Interim CEO, we have conducted a detailed review of the pipeline of potential sales opportunities. Consequently, the Board now believes that investment grade opportunities equivalent to £66m more fairly reflect the level of live opportunities that the business could potentially convert into revenue in the short to medium term.

The way this is phrased makes it sound like a new CEO has come in and found the skeletons of the previous team in the closet. However, Gahan has been CFO since October 2024. Are we really to believe that he had no hand in setting which opportunities would be in this pipeline, nor which would be delivered in this financial year? It looks like these are his closet and his skeletons.

It is not the first time that expectations have had to be reset during his tenure, either:

This is despite an accounting change in the FY25 results that shifted revenue into FY26:

As part of the ongoing review of its accounting policies, the Board has decided to adopt a more conservative revenue recognition policy. Consequently, revenue recognised on contract signing has been reduced from 30% to 5% for Solar PV and Batteries and from 30% to 0% on LED and EV contracts. This policy has been applied retrospectively from FY24. By refining the revenue recognition policy to better reflect the progress of projects throughout their installation, the Group has recognised a deferral of revenue from FY25 to FY26.

There are no updated forecasts from their broker that I can see, but with £1m of D&A last year, together with £600k+ of interest paid, FY26 is likely to be another loss-making period.

One has to ask questions about their financial strength. At 31 December, they had £6.4m of current assets, including £0.921m cash, but £8.6m current liabilities. They have a history of running things close to the wire, too. The company uses Luceco as its primary technology provider. In November 2023, Luceco injected £1.75 million in cash into eEnergy by subscribing for 35m new shares. However, this cash was used to pay the outstanding supplier debt to Luceco. This was obviously a clever move that proved to be a win-win. eEnergy appears to have avoided being unable to pay a supplier, and Luceco appears to have avoided having to report a bad debt. John Hornby (recently retiring CEO of Luceco) joined the eEnergy board as a non-exec to guide strategy until Luceco's stake was sold to Harwood in October last year.

To keep the business afloat, the board also had to execute a messy, long-winded divestment of its Energy Management division to Flogas in early 2024 for £29.1 million to wipe out high-interest debts.

It is clear that Harwood are supportive of the company, having lent them £1.5m and have the financial firepower to back them if further equity funding is required following this reset of expectations. However, that doesn’t mean that Harwood won’t extract their pound of flesh if it comes to this.

Strategy:

On the surface, this is a good business model. eEnergy provides upfront energy infrastructure, such as smart LED lighting or solar panels, to public and commercial organisations, including schools and healthcare facilities, which pay for it through the energy savings they generate. They rely on major long-term funding partners (such as NatWest and Redaptive) to fund the initial purchase of hardware and installation costs.

The problem appears to be that they aggressively scaled their cost base to support what leadership believed was a massive backlog of commercial opportunities. Today’s update shows the folly of that, and hence the recently announced cost-cutting.

The other issue is that the contracts they sign are based on certain assumptions, for energy prices, savings levels, and, as they are debt-funded, interest rates. The movement of any of these can significantly change the outlook for the business, making cash flow forecasting difficult.

Mark’s view

The cost-saving actions and reduction in the pipeline to reflect more realistic assumptions look to be the right move. However, the interim CEO can’t exactly claim he is clearing up the mess of the previous team. Many of the previous assumptions were from a time he was CFO!

We’ve not given a recent view on this company on the DSMR, but the scale of today’s downgrade in expectations, lack of financial robustness, and history of running things close to the wire mean we should probably be mostly negative. Perhaps only the support of well-known turnaround investor Harwood Capital stops me from being completely negative here. AMBER/RED.

Triad (LON:TRD)

Up 3% at 297p (£49.7m) - Final Results - Mark - AMBER/RED ↓

The history: This is a company where I have some history. I got interested in it when it looked very cheap prior to the COVID Pandemic. The market at the time was concerned about a large share overhang from the former CEO Mira Makar following her dispute with the Executive Chairman John Rigg.

As far as I can tell from press reports, in February 2005, Triad’s Executive Chairman, John Rigg, interrupted a meeting Makar was holding with the firm's stockbrokers. Makar was detailing financial and corporate governance concerns she had. At this point, Rigg immediately suspended Makar and he was formally sacked in December 2005. Makar took the company to an employment tribunal, claiming she was ousted for whistleblowing. In November 2006, Triad settled out of court, paying Makar an undisclosed sum and admitting that her corporate governance concerns were entirely reasonable. Makar retained her stake of around 24.7% of the company's shares.

The professional animosity resurfaced years later in 2018, Triad Group Plc and its directors launched legal action against Makar accusing her of conducting a prolonged campaign of libel and harassment against its leadership. In February 2019, the High Court handed down a default judgment against Makar and by February 2020, the court ordered funds to be seized from the Court Funds Office to pay Triad's legal costs and awarded damages. This involved selling a portion of her Triad shares. She still holds around 20% of the company according to the Stock Report.

This led me to attending the company’s AGM, where I learnt that:

It appeared that John Rigg was probably too infirm to play a very active role as Executive Chairman.

The MD Adrian Leer was probably the driving force behind the day-to-day running and did a good job. However, the vast majority of his shareholding comes from options exercise.

The board were very welcoming to external shareholders but appeared to consider it their personal fiefdom when it comes to decision-making. A view that is backed up by the subsequent appointment of John Rigg’s daughter, Charlotte Rigg, as Executive Deputy Chair. In my personal opinion, this is a role for which she had little to no relevant experience.

The board’s strategy aim of returning to the glory days of Y2K work which led to them delivering around £36m of revenue in 1998 looked totally achievable.

In summary, this is a reasonably well-run IT contractor to government projects, but one with some corporate governance concerns and that should be priced accordingly.

The reality:

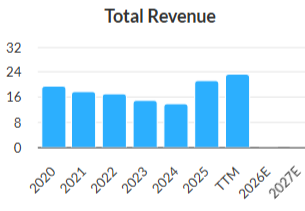

The initial share price recovery was a surprise to me as it appeared to be due to the announcement of a Blockchain collaboration at a time when the market was excited about such things. As far as I could tell, this may not have gone much beyond hiring a person who had written the word “Blockchain” on their CV! Whichever way, it didn’t seem to make much impact on revenue which declined continuously from 2020 to 2024:

This doesn’t appear to have worried investors, as the share price never gave back the gains from its blockchain induced excitement. After a strong recovery in trading 2025, the share price briefly hit £4 before retracing back to today’s level.

The results:

Today’s results show a continued improvement in that revenue trend:

EBITDA also shows a nice increase, but normalising tax rates see EPS flat on the prior year.

Outlook:

There is no broker coverage here, so we are reliant on the company outlook statement:

The outlook is very promising. Short-term, the new financial year has started well. The Company is growing steadily, and we have made significant changes to our work-winning approach to secure the platform for future growth. Secured work is at levels higher than previous years, and we continue to be enthusiastic about our prospects to win more work in our core and emerging markets.

This is not bad, but we have to remember this is an IT contractor, not a software business. There is little to no operational gearing, above the improved coverage of admin costs. More workload requires hiring more IT staff; as the relatively low gross margin, and increasing headcount last year attest:

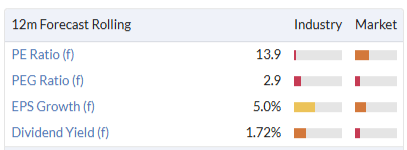

Valuation:

The P/E here remains around 30. This is frankly bonkers for a small IT consultant, with a patchy history and some ongoing corporate governance concerns. Even on a EV/EBITDA basis, accounting for the net cash, we have a 23x EV/EBITDA multiple.

The closest listed competitors are TP Impact holdings and Madetech. These are both businesses that have performed very strongly recently due to good corporate performance and contract wins. Yet both businesses trade on half the P/S and EV/EBITDA of Triad.

Mark’s view

These results are not bad, showing decent growth even though normalised tax rates mean this doesn’t drop through to rising EPS. The outlook is also positive. However, at the end of the day this is a small IT contractor with less-than-perfect corporate governance. A sector peer comparison suggests this company is likely to be at least two times overvalued at the current price. Given what I know from the history of the company and learnt by attending an AGM a few years ago, I hope readers will understand why I am a bit more negative than my colleagues. AMBER/RED ↓

Transense Technologies (LON:TRT)

Down 15% at 48p (£8.6m) - Trading update - Mark - BLACK/RED ↓

This falls below our normal market cap level. However, we have commented here in the past, so it is probably worth a brief review.

It is a bit of a meh update on every front:

FY26: Revenue £4.6m, PBT breakeven versus £5.2m previously expected. Lower than anticipated sales from global tyre manufacturers within Translogik is blamed.

FY27: expectations are being moderated to reflect timing of conversion of advanced commercial opportunities.

Net Cash: down a bit to £0.71m from £0.92m at 31 December. They say internal cash generation is sufficient to fund working capital and further investment in new products and componentry.

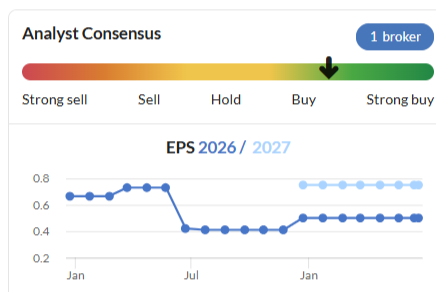

Broker’s forecasts:

While the impact from the company’s update seems relatively minor, I can’t help being a little concerned by the impact on broker forecasts. It makes sense that Cavendish’s FY26 EPS estimates go to zero. However, FY27 EPS goes from 8.7p to 0.8p, a cut of over 90%.

Equally worrying, FY27 net cash forecast goes from £2.0m to £0.1m. At this level of market cap, the cash impact alone is material.

Given that Cavendish aren’t willing to make an FY28 forecast at this time, then keeping their rather aggressive 251p Price Target based on a pipeline of “conversion of advanced opportunities into contracted revenues” looks a little daft to me.

Mark’s view

It is not surprising that the share price is down today. What is surprising is that it has only fallen 15% on an update that takes 22% of the market cap out of net cash estimates, let alone the 90% drop in EPS estimates.

When I reviewed this in February I kept our broadly negative view of AMBER/RED. As I said:

“…the risk of further bad news following a profits warning is too high to consider investing for a recovery now. However, a look at the balance sheet here suggests that they do have some time to turn things around. As such, I keep our broadly negative view…until there are some signs that the 2027 estimates are achievable and/or the Momentum Rank returns to a more reasonable level.”

Strangely, the Momentum Rank had increased slightly prior to today’s update

However, I foresee all the Ranks taking a major hit when the 2026 numbers end up assessed by the algorithms.

This update increases the risk here and the need for new contract wins sooner rather than later, plus it is now hard to argue that this is cheap if it hits future forecasts. With the share price reaction not yet fully reflecting these new realities, it makes sense to go fully RED, until it is clear that they can win those commercial opportunities that are sorely needed.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.