Next PM: there is the faint prospect of a leadership contest within Labour, but this seems to be primarily for the sake of having a leadership contest. There are no contenders with momentum and widespread support, other than Andy Burnham.

Tech sell-off: after its initial pop to $201 per share, Space Exploration Technologies (NSQ:SPCX) has been on the decline in recent trading sessions and fell 16% yesterday to $154.60 (still above its IPO price of $135). Elon Musk's net worth is bouncing around by hundreds of billions of dollars daily:

Alphabet (NSQ:GOOGL) also had a tough day yesterday, falling 5%.

Overall, the Nasdaq Composite Index fell 1.3%, and general weakness in the equity markets has continued overnight in emerging markets. The Korean Kospi index is down 8%.

Overnight market movements:

The FTSE is set to open down 1% at 10,335

S&P 500 is down 1% at 7,400

Brent crude is down 1.3% at $76.90/bbl

Gold is down 1.7% at $4,120/oz

Bitcoin is down 1.7% at $63,340

Today's Agenda is complete. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Bunzl (LON:BNZL) (£8.0bn | SR95) | H1 revenue expected to be +4% at constant rates, with growth supported by inflation. Volume growth driven by N.Am with good growth in Distribution. FY26 outlook upgraded: now expects revenue growth to be slightly stronger than previously. Operating margin guidance unchanged; “slightly down year-on-year”. | ||

Plus500 (LON:PLUS) (£3.3bn | SR85) | Has launched 24/5 CFD trading on “selected stocks and ETFs”, including SpaceX. | ||

Filtronic (LON:FTC) (£836m | SR58) | FY26 slightly ahead of expectations on adjusted EBITDA. Cavendish FY26 EPS upgraded to 3.3p (prev. 3.2p). Announces additional $0.5m contract with an existing customer. FY27 outlook: strong order book covers 90% of FY27 consensus revenue. | AMBER = (Roland) [no section below] For a company with a £800m+ market cap to announce a $0.5m (£370k) contract win seems a little promotional to me. In this case the issue is obvious. While Filtronic appears to be performing well, the reality is that profits have nearly halved from peak FY25 levels as the product mix has changed and costs have risen. While today’s guidance is marginally ahead of consensus, the 3% increase to EPS from broker Cavendish isn’t enough to justify a positive market reaction for a stock that’s trading on c.100x forward earnings. We were neutral on this business when its shares were trading at half this level earlier in the year. While I recognise the high level of excitement (and opportunity) in the space market, objectively I think Filtronic looks too expensive. I’m going to maintain our neutral view ahead of August’s results but I think it could pay to be cautious. I note that almost all of the company’s largest shareholders have been taking money off the table this year. | |

Telecom Plus (LON:TEP) (£766m | SR53) | Final Results for the year ended 31 Mar 26 & Strategy update and new five year plan | Revenue +5.6%, adj pre-tax profit +4.7% to £132.2m. Adj EPS +3% to 122.8p with total dividend of 50p (FY25: 94p) and £40m share buyback (equivalent to 50p per share). Total customers +23.3% to 1.43m with organic customers +10.3% to 1.26m. FY27/Strategy update: aiming to double multiservice customers from c.500k to 1m by FY31. Will require c.£55m of investment. FY27 adj pre-tax profit to be £80-90m. | |

Pantheon Infrastructure (LON:PINT) (£553m | SR67) | Q1 NAV total return of -2.6%, with trailing 12-month NAV total return of 12.1%. Q1 NAV per share -5.6p to 124.8p, post-dividend. Main contributor to decline was a -3.9p movement in the valuation of PINT’s investment in Constellation Energy Corporation. | ||

Big Technologies (LON:BIG) (£305m | SR54) | Various contract wins and renewals. Confident that 2026 trading will be in line with market expectations (adj EBITDA of £24.7m to £25.9m). | ||

B.P. Marsh & Partners (LON:BPM) (£252m | SR70) | Received the second tranche of deferred consideration of £5.1m relating to the sale of Aspira Corporate Solutions Limited. Total proceeds from Aspira are now £11m, with a further £5.1m payment expected in 2027 giving a total of £16.1m, in addition to a £3.3m loan repayment. | ||

Dialight (LON:DIA) (£149m | SR63) | Revenue -9% with adj operating profit up $6.1m to $10.3m. Net debt reduced to $1.9m. FY27 outlook: expect to achieve sales growth, profit growth and eliminate bank debt this year. | ||

Ramsdens Holdings (LON:RFX) (£146m | SR96) | Cash offer from US pawn operator FirstCash Holdings for up to 609p per share, comprising a payment of 600p per share plus dividends of up to 9p. | TAKEOVER (Roland) | |

Strategic Minerals (LON:SML) (£125m | SR44) | Additional samples from 2025 drilling have identified “tin-rich mineralised structures” and “tungesten enriched structures” to the north of the Redmoor deposit, outside the current modelled resource. | ||

EnSilica (LON:ENSI) (£118m | SR53) | FY26 revenue +51%, with adj EBITDA of £4.7m (FY25: £0m). FY27 expectations: revenue £32-34m & adj EBITDA £5.5-6.5m. PanLib FY27 forecasts unchanged. | ||

Taylor Maritime (LON:TMI) (£85m | SR94) | Sold a vessel generating net proceeds of $11.4m. Also agreed sale of a 50% JV vessel, generating net proceeds of $16.6m. Both are expected to complete in June, following which the company expects to make a minimum $45m return of capital in July by redemption of ordinary shares. | ||

Severfield (LON:SFR) (£82m | SR69) | FY26 revenue +1%, adj pre-tax profit -42% to £10.5m. Adj EPS -37% to 2.7p, in line with expectations. UK/Eur order book of £507m. Headwind from lower-margin projects expected to roll off in FY27. FY27 pre-tax profit expected to be in line with previous guidance of £12-15m. | ||

Journeo (LON:JNEO) (£77m | SR56) | Purchase orders totalling £1.3m for the provision of its on-board bus safety systems and high-security cloud-based SaaS services for Metroline Manchester. No reference to any impact on forecasts. | ||

Intercede (LON:IGP) (£73m | SR34) | Revenue down 2.8% (or down 0.5% at constant currencies). PBT £3.7m (FY25: £4.6m). Given the strength of delivered contracts year to date, the Company has started FY27 in line with the Board's expectations. | ||

Hardide (LON:HDD) (£58m | SR57) | Proposed cancellation of both the share premium account and a separate capitalised non-statutory reserve, generating c. £3.2m of distributable reserves. The goal is to enable share buybacks to fund executive share option awards, and to make distributions to shareholders possible. | ||

Gear4music (HOLDINGS) (LON:G4M) (£54m | SR85) | Revenue +30%. PBT £10.3m (FY25: £1.6m). FY27 trading to date in line with board expectations and on track to deliver FY27 consensus market expectations. | ||

Character (LON:CCT) (£51m | SR78) | “Enterprise Management Incentive” share option scheme. Substantially similar in structure and in operation to the 2017 Plan. | ||

Symphony Environmental Technologies (LON:SYM) (£21m | SR13) | Revenue down 13%. Operating loss £2.1m due to Middle East operations and one-off strategic costs. Net profit achieved in the first five months of 2026. | ||

iomart (LON:IOM) (£20m | SR65) | Results in line with revised market expectations. Adjusted pre-tax loss £4m. Outlook: “While a modest decline in full year revenue is expected, the Board expects the benefits of cost base actions and an increased focus on higher-value, strategically aligned services to support an improved profit profile during the second half of FY27.” | ||

Hercules (LON:HERC) (£20m | SR36) | “The acquired businesses are performing as hoped and while there have been some delays in the commencement of some key projects across the business, we are confident that we are well positioned for the future…” | BLACK (RED ↓) (Graham) [no section below] Roland downgraded our stance on this in May as accounting irregularities were brought to light. This problem was combined with the absence of forecasts for FY September 2026, although forecasts from SP Angel have subsequently been reinstated. Today’s AGM statement reads like a profit warning to me, with delays to key projects, although the company doesn’t quantify the financial effects that these delays might have. And I can’t see any broker update yet: the most recent forecast I can find is for a small operating loss this year (<£200k). I can only conclude that this loss might turn out to be wider than previously expected. I also note that the company’s gross cash balance (c. £7m) is funded by loans and an invoice discounting facility. Given all of the above, I think that a further downgrade is needed and that this must be a RED for us today. | |

Kelso group (LON:KLSO) (£14m | SR36) | As set out in the most recent portfolio update, NAV increased by 35% in the first five months of the year to 3p. | ||

Angus Energy (LON:ANGS) (£12m | SR n/a) | Revenue £9.5m, operating profit £1.5m (H1 2025: £3.4m). “...immediate priority remains the completion of the restructuring process and the restoration of trading in the Company's shares.” Material uncertainty arising from “dependence on continued gas production, compliance with the terms of its financing arrangements and the successful completion of the restructuring”. | (Shares suspended since 19 May 2025) | |

Arkle Resources (LON:ARK) (£12m | SR18) | €225k operating loss, no revenues. Arkle continued its strategy as a gold, zinc and lithium explorer, working in Ireland and Botswana. Shortly after the year-end, in January 2026, we announced a transformational acquisition that repositions the Company as an energy metals explorer with uranium at its centre. |

Roland's Section

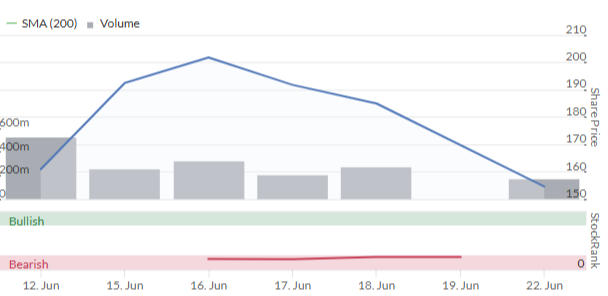

Ramsdens Holdings (LON:RFX)

Up 30% at 590p (£192m) - Recommended Cash Acquisition - Roland - TAKEOVER

We’ve been consistently positive on pawnbroking, gold and jewellery retailer Ramsdens, most recently here. The company has proved an excellent way to play the gold price and – in our view – is a great example of a well-run, good quality AIM business.

Ramsdens’ reputation has clearly spread across the pond as the company has now become the latest British firm to succumb to an offer from a deep-pocketed US buyer.

In this case, it’s a trade sale rather than a private equity bid – Ramsdens board has recommended a cash offer from NASDAQ-listed US pawnbroking group Firstcash Holdings (NSQ:FCFS), which is coming back for seconds after buying the UK’s largest pawnbroker, H&T, last year.

FirstCash operates over 3,300 shops in the US, Latin America and the UK and has a market cap of c.$10bn. So today’s £203m offer for Ramsdens is probably small enough to qualify as a bolt-on acquisition.

Here are the details of FirstCash’s offer:

Total consideration: up to 609p per share in cash or up to £206m, including dividends.

600p for each Ramsdens share from FirstCash

Up to 9p in dividends reflecting the interim payout of 6p and special dividend of 3p that were declared with the company’s recent half-year results.

The offer represents a fairly healthy premium across all recent timeframes:

33% premium to yesterday’s closing price of 453p

46% premium to the volume-weighted average price of 412p over the last three months

22% premium to Ramsdens’ all-time closing high of 493p on 3 June 2026

The offer is comfortably above Ramsdens’ all-time high, so this guarantees that any current shareholder will receive a profit from the takeover.

Longer-term shareholders have done much better, of course. Investors who bought Ramsdens’ following its 2017 IPO could be in for a 500% profit, plus dividends:

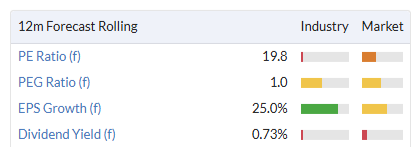

Valuation: the latest forecasts from house broker Cavendish show Ramsdens generating earnings of 67p per share this year and 45.5p in FY27.

This means the FirstCash offer is equivalent to a FY26E P/E of 9x and a FY27E P/E of 13.

However, as Graham has pointed out previously, the FY27 forecasts are based on an average 9-carat gold price of £32/g, below the current level of c.£35/g. So there may be in-built scope for upgrades if gold remains stable at current levels.

Of course, there could also be significant downside if the gold price continues to decline, but I imagine some commodity price risk has been factored into the offer.

Valuation

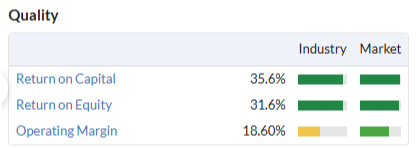

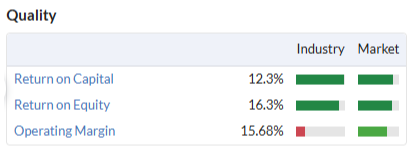

Overall, I think it’s fair to suggest FirstCash is not paying more than c.10x near-term earnings for Ramsdens, which has minimal debt and enviable quality metrics:

The attraction for FirstCash is not hard to see.

FirstCash shares trade on P/E of 20 – double my 10x P/E estimate for its acquisition of Ramsdens:

In theory, this means that Ramsdens’ earnings will be valued at 20x when added to FirstCash’s results. That should effectively give a c.£400m boost to the US group’s valuation, double the cost of the acquired UK earnings.

Ramsdens is also a higher-margin business than FirstCash, so this acquisition should be margin-accretive for the buyer:

Competition approval?

H&T and Ramsdens are the UK’s largest pawnbrokers by some margin. According to some brief research, I believe they control around 65-75% of the pawnbroking market in the UK, based on pledge book data.

The completion of this acquisition is dependent on the approval of the Competition and Markets Authority. Presumably FirstCash is reasonably confident this will be possible despite the market consolidation that will result.

I would guess that one factor in favour of the deal being approved is that H&T has historically been stronger in the south of England, while Ramsdens has more of a skew to the North/Wales, limiting direct overlap. Even so, I think there’s some possibility that regulatory risk could hold up this deal.

Roland’s view

Ramsdens’ chairman Simon Herrick appears to blame UK investors for not being bullish enough to protect Ramsdens from a takeover offer:

Unfortunately, the share price has not fully kept pace with the Group's positive profit and earnings per share growth and FirstCash has made a cash offer for the Group which represents a 35% premium to the current share price. The Board, following independent advice from Cavendish as to the financial terms of the Acquisition, considers the Acquisition to be recommendable to our shareholders.

A counterpoint to this argument might be that UK investors were recognising the commodity price risk in this situation.

Ramsdens’ recent half-year results showed that gold trading generated the same gross profit as jewellery and pawnbroking combined, but the price of gold has fallen by c.20% since the end of that reporting period.

This offer means that Ramsdens’ shareholders are getting a fixed premium in exchange for losing their exposure to the gold price and the potential risks and benefits of Ramsden’s continued expansion.

Based on what we know today, I think it’s probably a reasonably fair offer for both parties, but only time will tell whether FirstCash has secured a bargain.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.