Good morning. Apple increased the prices of its MacBook and iPad products by 20% yesterday, citing memory shortages caused by the AI boom.

While the US firm has held off from hiking iPhone prices so far, the decision sparked a 6% drop in Apple shares yesterday over concerns that consumers would be unable to absorb higher prices. This triggered a broader sell-off in Asian indices – the Nikkei closed down nearly 5%, while Korea’s chip-heavy Kospi index closed nearly 7% lower.

The AI boom has driven fantastic profits for many companies in the sector, but it is hardware intensive and global semiconductor manufacturing capacity is constrained and relatively inflexible. It may be worth watching for further company-specific impact from such shortages.

Elsewhere, a number of oil tankers attempting to exit the Strait of Hormuz turned round and paused their journeys after a ship was attacked on Thursday. The International Maritime Organization has paused its evacuation programme for ships bottled up in the Strait. However, the impact on oil prices has been very limited so far.

Finally, this week’s European heatwave is said to be the worst on record. It’s described by scientists as being impossible without climate change. With increasing health impacts and risks to key infrastructure, I wonder if this will become a greater area of focus for policymakers (and businesses) over the coming years.

On a related note, apologies if there is some disruption to service this morning - the thunderstorms here in the north east have triggered power cuts and my internet connection is intermittent.

Overnight market movements:

The FTSE is set to open down 0.6% at 10,470

S&P 500 is down 0.7% at 7,307

Brent crude (August) is down 1.2% at $74.55/bbl

Gold is down 0.5% at $4,013/oz

Bitcoin is down 2.9% at $59,767

Today's agenda is now complete.

Spreadsheet accompanying this report: link

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

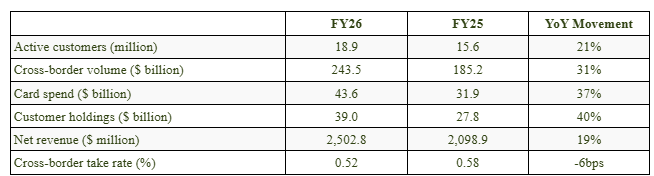

Wise (LON:WISE) (£10bn | SR53) | Net revenue +21%, with pre-tax profit down 8% to $660.4m. Take rate -6bps to 0.52% with cross-border volume +31% to $243.5bn. Active customers +21% to 18.9m. Outlook: expects FY27 net revenue growth in the middle of the 15-20% range, with pre-tax margin around the top of the 20-25% range. No change to medium-term targets. | GREEN = (Roland) I think these results show that Wise is continuing to execute on its long-term strategy of building market share by providing a high-quality and keenly-priced service. The falling take rate and decline in profits don’t concern me. Margins remain high and rapid volume growth means that management should be able to manage profitability as needed. While this business model does carry risks – as highlighted by the ongoing Belgian money-laundering investigation – I think the investment thesis remains attractive and am comfortable with the valuation. | |

Barratt Redrow (LON:BTRW) (£4.2bn | SR43) | New CEO Dean Banks will join on 21 September 2026. The current CEO will step down at that time but remain with the group until March 2027. | ||

Zegona Communications (LON:ZEG) (£3.8bn | SR96) | Completed refinancing of “all its existing senior secured notes and senior facilities”. Improved terms will deliver annual interest savings of c.€60m and extend the maturity of Zegona’s capital structure beyond five years. Annualised interest cost of the new debt structure is €170m. | ||

XPS Pensions (LON:XPS) (£627m | SR61) | Acquired Austin Professional Resourcing LLP, a UK-based actuarial consultancy working with insurers and financial sector clients. APR generated revenue of £10.7m last year. Cash consideration of £3.3m will be paid on completion, with £3m due in 2027 and further contingent payments totalling up to £10m in years two and three. | ||

Guardian Metal Resources (LON:GMET) (£429m | SR27) | The company will publish its pre-feasibility study for the Pilot Mountain Tungsten Project on 30 June 2026. | ||

Beximco Pharmaceuticals (LON:BXP) (£385m | SR n/a) | Late results: FY25 net revenue +10.7%, with profit after tax +19.3% to BDT 6,999m (£42.1m). EPS of BDT 15.56, recommended dividend of BDT 4.75 per share. | Beximco shares have been suspended since 2 Jan 26 but will resume trading today. | |

Kistos Holdings (LON:KIST) (£191m | SR43) | Revenue -1.6%, adj EBITDA +1.3% to $96.6m. Net debt of $76m. Average production of 8,940 boepd. FY26 production guidance unchanged at 19,000 - 21,000 boepd. | Slow to publish FY25 results. | |

Aew UK Reit (LON:AEWU) (£165m | SR59) | NAV per share down 1.42% to 103.38p for y/e 31 March, with NAV total return of 5.7%. EPRA EPS down 11.3% to 7.98p, giving 99.8% dividend cover for the unchanged payout of 8p. EPRA vacancy rate of 9.4% at 31 March (FY25: 7.5%). | ||

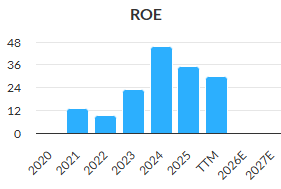

Distribution Finance Capital Holdings (LON:DFCH) (£99m | SR64) | H1 update: new loan origination expected to close at c.£1bn, +21% vs H1 25. Aggregate loan book is expected to close >£915m, +25% vs H1 25. Outlook: average loan book has exceeded expectations in H1, now expect to report full-year profit ahead of expectations, with pre-tax profit of at least £13m and ROE in excess of c.17%. | GREEN = (Roland) Another upgrade from this fast-growing specialist lender. Updated broker forecasts suggest encouraging earnings growth and the valuation remains very reasonable in my view, with a discount to book value despite last year’s 12%+ return on equity. Small lenders always carry some risk, but I’m happy to stay fully positive here given the strong fundamentals and good momentum. | |

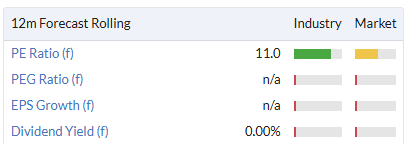

Devolver Digital (LON:DEVO) (£85m | SR55) | H1 performance ahead of expectations with revenue expected to be “at least 60% higher than 1H 2025” and adj EBITDA expected to reach “mid single-digit” $m. Strong start due in part to the Devolver Steam Publisher sale held in H1. However, sales of a recent major new game have been disappointing so far. No change to broker forecasts. | AMBER = (Roland) Devolver had a strong start to the year, but a recent game launch has been disappointing (so far). It’s too soon to know if the shortfall will be covered by the remaining slate of new games scheduled for H2 - the company has promised an update in September. Broker forecasts are unchanged today, but my number crunching suggests there could be some risk of a profit warning later this year, without a fairly strong H2 performance. Net cash of $37m underpins the market cap and a forward P/E of 11 isn’t unreasonable. But a lack of visibility or obvious bargain characteristics means that I’m leaving our neutral view unchanged today. | |

Clean Power Hydrogen (LON:CPH2) (£68m | SR n/a) | Agreed settlement with Lagan MEICA relating to the Northern Ireland Water 1MW MFE220. Contract will be terminated through the payment of a settlement sum, but the settlement is contingent on a fundraise by 31 July 26. | CPH2 shares have been suspended from trading since 29 May 2026. | |

Zephyr Energy (LON:ZPHR) (£67m | SR28) | Acquired 27,000 acres in Utah, “doubling the acreage footprint around Zephyr’s White Sands Unit” in the Paradox project. Funded from existing cash resources. | ||

Panther Securities (LON:PNS) (£49m | SR56) | Sold freehold warehouse property in Peterborough for c.£3.25m in cash. This is a £250k increase on the book value of £3m. Proceeds will be held for reinvestment. | ||

Character (LON:CCT) (£49m | SR77) | A party connected with the new occupier of Infinity House has exercised an option to purchase the property. A deposit of £980k has been received, with a further payment of £8.82m due on 23 July 2026. | ||

Zenith Energy (LON:ZEN) (£31m | SR24) | The International Centre for Settlement of Investment Disputes will accept post-hearing briefs on 31 July 26 and 30 Sept 26 and deliver its final reward in Q1 2027 (estimated), relating to the claims launched against the Republic of Tunisia by Zephyr in the amount of approximately US$572.65 million. | ||

Defence Holdings (LON:ALRT) (£30m | SR11) | Completed £4m fundraising at 1p per share. Placing was “significantly oversubscribed and scaled back”. | ||

Cirata (LON:CRTA) (£23m | SR10) | Completed fundraising to raise gross proceeds of c.£5.1m at 15p per share (an 18.9% discount). 34.2m new shares will be issued, increasing the existing share capital by 27%. | ||

Ampeak Energy (LON:AMP) (£21m | SR16) | 2025 revenue 4.2% to £15.0m with EBITDA -53% to £3.7m and a net loss of £13.9m. Net assets down 60.5% to £6.8m. | Slow to publish FY25 results. | |

Hercules (LON:HERC) (£18m | SR36) | Secured enhanced debt facilities with IGF, comprising an increased invoice discounting facility of £20m (previously £16m) and £5m of term loans, of which £4m will be used to settle the final earn-out payment for Advantage NRG. | ||

ARC Minerals (LON:ARCM) (£17m | SR10) | 2025 net loss of £9.1m (2024: £2.1m). Year-end cash of £635k. Recently began a geophysical programme at Virgo Point, targeting drilling in H2. | Slow to publish FY25 results. | |

Tap Global (LON:TAP) (£10m | SR5) | Tap customers will soon be able to receive their salary and third-party payments directly into their Tap account. Rollout for Euro area customers starts today, with GBP payments “expected to follow in due course”. |

Roland's Section

Distribution Finance Capital Holdings (LON:DFCH)

Up 9% at 65p (£m) - Trading Statement - Roland - GREEN =

DFCH is a specialist lender providing finance for caravan and motorhome manufacturers, dealers and more recently for individual buyers. Graham has been positive on this business for a while, most recently in April.

Today’s trading update is ahead of expectations and sounds fairly positive to me:

Full Year Profit expected to be materially ahead of market expectations driven by loan book performance and new product growth

Trading highlights:

New lending is running ahead of expectations and historic seasonality. New loan origination in H1 is expected to total c.£1bn, an increase of c.21% over H1 last year. The Q1 figure was £469m, suggesting a sequential Q2 growth rate of 13%.

The group’s loan book is expected to end the half year “in excess of £915m”, 25% ahead of the same point last year.

A new lending product aimed at consumers is seeing strong momentum, especially in the static caravan and holiday park sectors. The loan book is expected to reach £40m by the end of H1, a near-threefold increase from £15m at the end of 2025. Loans are originated through dealers who are already part of DFCH’s network. This product is also contributing to a longer average tenor for loans, which the company sees as a benefit.

Portfolio quality remains “exceptionally strong”, with the cost of credit risk remaining "well within" the group’s target of less than 1%.

Outlook

DFCH has provided explicit new guidance for 2026 today:

In light of the Group's average loan book exceeding expectations through the first half alone, coupled with continuing low arrears and impairments, the Group expects to report profit before tax of at least £13m for the period ending 30 June 2026, delivering an annualised return of required equity in excess of c.17%.

Broker Panmure Liberum has shared updated forecasts through Research Tree this morning. They’ve upgraded 2026 pre-tax profit forecasts by c.16% to £22.4m, citing the higher than expected average loan book (which improves interest income).

Earnings forecasts have been upgraded across the board:

FY26E adj EPS: 9.4p (previously 8.1p)

FY27E adj EPS: 10.6p (previously 10.0p)

FY28E adj EPS: 11.7p (previously 11.5p)

These estimates price the shares on FY26E P/E of 7x after this morning’s gains.

Roland’s view

This morning’s upgrade continues a run of upgrades for DFCH, highlighting the strong momentum in the business at the moment:

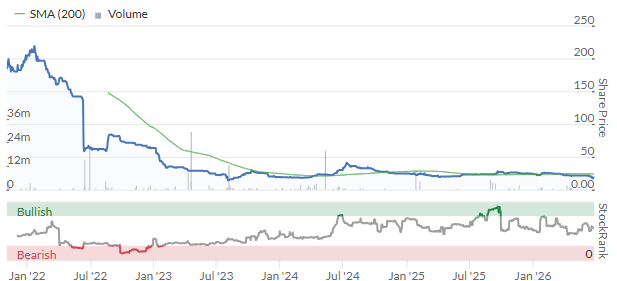

The valuation also remains potentially attractive, in my view. At 66p, the stock continues to trade at a discount to last year’s book value of 76p per share.

When paired with double-digit returns on equity, this seems fairly undemanding to me:

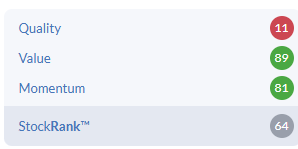

While the quality score remains low, the main metric I look for in businesses of this type is return on equity (paired with a healthy balance sheet). I think DFCH ticks both boxes and expect profitability to improve if growth continues and bad debt remains manageable.

Small lenders are always quite risky, so I wouldn’t make DFCH a large part of my portfolio. But I’m quite comfortable maintaining our positive view on this business today. GREEN

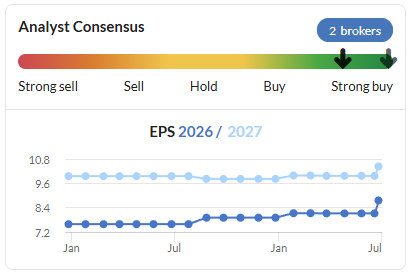

Wise (LON:WISE)

Up 6% at 878p (£9.0bn) - FY26 Results - Roland - GREEN =

Thank you to subscriber David Holdsworth for providing some early analysis on today’s results in the comments.

Money transfer group Wise moved its primary stock market listing to the US in May, but has maintained a secondary listing in the UK. So I think it’s fair to maintain some coverage here in this (UK-focused) report.

For some backdrop on recent share price movements, it’s worth remembering the stock fell by around 20% at the start of June. This was prompted by the news that Wise is being investigated by Belgium authorities, in relation to possible money laundering offences relating to c.€500m of transfers. There’s no update on this issue in these results.

Wise’s FY26 results showcase the characteristics I’ve come to expect from this business: rapid growth in usage with more measured growth in revenue, as Wise continues to focus on keeping it pricing ("take rate") as low as possible.

For some context on the company’s aggressive pursuit of low pricing, Wise’s take rate has now fallen from 0.64% in April 2024 to 0.51% in the three months to 31 March 2026. That’s a 20% cut in two years!

Financial performance: Wise’s profit performance is complicated by the fact that as a non-bank it’s ability to pay interest on customer deposits is strictly restricted. Even though it would like to be more generous with customers.

Graham’s covered this previously, but today’s commentary highlights the boost this provides to the group’s margins:

[We maintain our medium-term target for an] Income before tax margin of 15-20%, including 20% of interest income above the first 1% yield retained. However, until we are substantially able to pay out additional interest to customers, we expect to report an above-target income before tax margin of 20-25%.

With no immediate prospect of this situation changing, I think it’s easiest to follow the statutory accounts. These show a slight decline in profits last year, as expected:

Pre-tax profit down 8% to $660.4m;

After-tax profit down 9.4% to $498.7m;

Diluted earnings per share down 8% to 48.43c.

Applying today’s exchange rate gives me an earnings figure of 37.7p per share, which is very close to the consensus figure of 37.3p shown on the StockReport. So my conclusion is that these results are largely in line with expectations.

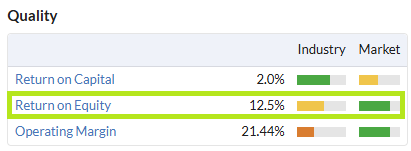

Profitability: these results give Wise a FY26 pre-tax profit margin of 26% and a return on equity of 25.9% – both excellent figures, albeit ROE is (intentionally) below last year:

Capital allocation strategy - buybacks

Wise spend $470m buying back 35.9m shares last year for its Employee Share Trust – effectively a remuneration cost, in my view. This equates to an average price paid of c.990p, slightly above the current share price.

For 2027, the company has announced a new $500m buyback of which c.40% will be allocated to the EST, with the remainder presumably used to reduce the group’s share count. I don't have a problem with this in the scheme of things; it looks affordable to me.

FY27 Guidance

Today’s results included clear guidance for the current year:

Net revenue growth “around the middle” of the 15-20% medium-term target range;

A pre-tax profit margin “around the top” of the 20-25% range.

Applying this guidance to today’s FY26 results gives me the following estimates:

Net revenue of $2,940m;

Pre-tax profit of c.$720m;

Diluted earnings of around 57 cents per share (c.43p), assuming unchanged tax rates etc

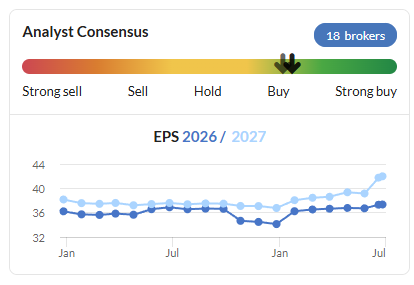

As far as I can tell, today’s guidance is slightly ahead of previous consensus for FY27, but not massively so. Even so, this seems likely to extend the recent positive trend in earnings forecasts:

Roland’s view

By continually cutting its “take rate” [fees] to reflect growing economies of scale, Wise’s services become more competitive and attractive for a wider number of users. It’s a land grab strategy similar to that pursued by Amazon in the past.

I think this is a smart approach. This is a business where strong volumes and deep liquidity provide a competitive advantage and help to support further expansion. While Wise probably could make more money in the short term by maintaining its take rate on higher volumes, I think doing so might make it harder for the business to achieve it’s long-term strategy of becoming a dominant player in its markets.

After all, $43 trillion is moved across borders by people and businesses every year (according to Wise). The company’s share of this last year was just $243.5bn, or just 0.6%. Aiming big seems sensible to me.

My estimate of 2027 earnings suggests Wise is trading on a forward P/E of c.20. For a business with strong quality metrics and double-digit revenue growth, I don’t think this is unreasonable.

I am in the camp that believes Wise has a long growth runway and the potential to become a much larger and more profitable business.

The Belgian investigation remains a risk and is perhaps a reminder of the pitfalls that can befall fast-growing fintechs. Even so, I think the long-term investment thesis here remains very positive and am happy to maintain our GREEN view today.

Devolver Digital (LON:DEVO)

Up 8.5% at 19p (£93m) - Trading Statement - Roland - AMBER =

Today’s update from this publisher and developer of indie video games has received a warm reception, but to my mind it’s broadly neutral overall. What the update gives with one hand, it appears to take away with the other.

H1 ahead of expectations

The good news is that Devolver has had a strong start to the year, with H1 performance “ahead of expectations”.

The favourable year-on-year comparison is in part due to the Devolver Steam Publisher sale being held in 1H 2026, in addition to a positive start to the year with 3 Top 10 Global Best Sellers on Steam in January.

We’ve commented on Devolver’s confusing update style before and today is now exception. Rather than providing explicit figures, management have provided percentage changes and vague suggestions.

Revenue

H1 revenue is expected to be “at least 60% higher than 1H2025”;

Based on last year’s results, this implies H1 revenue of at least $62m

Underlying adjusted EBITDA

Leaving aside the absurd double level of adjustment being applied here, it looks like profits are going to bounce back from last year - when Devolver generated just $0.1m of EBITDA in H1:

H1 “underlying adjusted EBITDA” is “projected to reach mid single-digit US$ millions”.

My guess is that this means a range of $5-7m of adjusted EBITDA.

STARSEEKER release has “been disappointing”

The strong H1 performance may not continue into H2. Early sales of a (presumably) important new game are said to have been disappointing:

In June, Devolver's subsidiary System Era released STARSEEKER: Astroneer Expeditions into Early Access with a significant platform deal accompanying the launch. Unit sales have been disappointing so far but review scores are improving and there are regular content updates planned for August and through to the end of 2026 which the Board believes can re-energise the game.

END QUOTE

Investors with an interest in this sector will probably know more about this than me – as Ed has highlighted previously, it’s possible to mine publicly-available data to get an insight on new game sales before companies report to the financial markets.

I’d certainly recommend this kind of supplementary research for anyone considering an investment in games publishers.

Outlook & Broker Estimates

Devolver has a number of other new games slated for the second half of the year and remains positive about their prospects:

Subsidiary studio Firefly enjoyed a very positive response to its announcement of Stronghold 4, building 250,000 wishlists in just two weeks. Equally encouraging is the interest in other games slated for 2H 2026, Warhammer 40,000: Boltgun 2 (c. 260,000 wishlists) and Shroom and Gloom (c. 220,000 wishlists).

However, the disappointing launch of STARSEEKER does seem at risk of putting a dampener on the full-year outlook. Today’s full-year guidance is noncommittal, with a further update promised in September:

The strong 1H 2026 performance and the positive response to pending games are expected to combine to build a profitable cushion although this will be offset by the slower than expected initial launch of STARSEEKER. We will provide further details on 1H 2026 performance and guidance for the full year 2026 at the time of the Company's half-year results in late September 2026.

Brokers Panmure Liberum and Zeus have both published updates today. Both brokers have left their FY26 estimates unchanged, but I’m surprised at the wide variance between each company’s estimate:

PanLib FY26E adj dil EPS 1.4 cents

Zeus FY26E adj dil EPS: 2.4 cents

These figures average to give the 2 cent consensus estimate shown on the StockReport. But in my view, the variation between these forecasts highlights the lack of visibility on sales for the remainder of the year.

Roland’s view

This business floated opportunistically during the pandemic video game boom and has disappointed investors ever since:

While broker forecasts are unchanged today, I think they do provide some useful context for today’s H1 guidance.

PanLib’s forecasts suggest full-year adjusted EBITDA of $12.8m, while Zeus comes in at $14.6m due to slightly higher revenue assumptions.

Today’s guidance for "mid single-digit" H1 EBITDA suggests to me that Devolver could easily miss full-year expectations if H2 is not as strong as H1.

Based on today’s commentary, I would suggest there is some risk of a profit warning later this year, unless other new games perform well.

While Devolver’s $37m net cash position helps underpin the market cap and provide a margin of safety, I can’t get very excited about this business. Devolver has operated at a loss in each of the last four years. Based on today’s update, I’d argue that the outlook for this year also carries some uncertainty.

We’ve been neutral on this business previously. I’m going to leave that view unchanged today to reflect unchanged forecasts and the reasonable valuation:

However, while in-depth sector research might unearth an opportunity here, I am inclined to think there are more tempting choices elsewhere.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.