Good morning!

I'm back from a long weekend in Warsaw - it was really good to have a change of scene. All was great, apart from being ripped off by an illegal taxi driver, and a stag party on the plane back who made the flight a misery. The airlines really do need to do something about this increasing problem.

Mello Beckenham

A reminder that David Stredder's popular, and long-running monthly investor evening is happening today - click the blue link above for more details. The popular & very capable David Cicurel of Judges Scientific (LON:JDG) will be updating investors on progress this evening.

I probably won't be able to make it tonight, as I'm working in North London this afternoon, helping a private company. I'm taking on some NED roles in smaller, private companies with good growth potential, to help them with finances, and strategy/planning. All good fun, and it's enjoyable to do something a bit more hands on.

Sprue Aegis (LON:SPRP)

Share price: 142p (down 47% today)

No. shares: 45.9m

Market cap: £65.2m

Profit warning - you know straight away, when a share price is down 47%, that the profit warning is a bad one. Also, there has been no bounce in the share price yet, Such an initial bounce often happens for 2 reasons;

1) The early drop can be exaggerated by forced sellers at spread bet companies - whose positions are cut at any price, once the stop loss is triggered. It's important to remember that there can often be considerable "slippage" with stop losses - i.e. your spread bet can end up being closed at a far lower price than the stop loss you set. A stop loss is only a genuine stop loss if it's guaranteed, and you have to pay extra for that. Any share that gaps down at the open can make a mockery of a (say) 10-20% stop loss. The actual loss can be considerably more.

2) Existing holders are often anchored to the previous share price, and wrongly see the reduced price as a buying opportunity. This is down to psychological factors, and often an underlying desire to support the share price. This is due to the increasing pain of the losses on their existing shareholdings. It's nearly always a mistake to steam in and increase your existing holding on a profit warning - unless the profit warning is mild, and due to one-off, and easily fixed problems. Or, if the share price has wildly over-reacted, and fallen far more than it should have done.

In the case of SPRP, the company has a strong balance sheet, with net cash, so the 47% share price fall is really even worse than that, on an Enterprise Value basis. So things must be bad, and they are bad I'm afraid.

2015 results - warranty increase - a problem has emerged with batteries supplied by a third party:

...the Company has recently identified an issue in certain batteries supplied by a third party supplier that may cause a premature low battery warning chirp in certain of its smoke alarm models sold in the UK and in Continental Europe.

The Board is keen to stress that this is not a safety critical issue.

I don't really understand this problem. Surely the customer would just replace the battery, if it gives a warning chirp? Perhaps it's not as simple as that? Maybe it's a built-in rechargeable battery? I think the company could have explained this better, so that non-technical people like me could understand the issue properly.

EDIT: In the comments section below Biloseli reckons that this might relate to a "sealed for life" product, which is supposed to have a 10-year battery inside, which it now appears could fail after 3 years.

The financial upshot of this is quite considerable:

As a result, to support the Company's customer service obligations, the Board proposes to increase the Group's warranty provision as at 31 December 2015 by £5.5m to £6.8m (2014: £0.9m). Consequently, further to the Company's trading update released on 20 January 2016, the Board now expects the Company's operating profit* for the year ended 31 December 2015 to be approximately £7.3m compared to the previously announced expected operating profit* of £12.1m.

Well done to the company and its advisers for quantifying the impact, so that shareholders & commentators have accurate information to work on. All companies should do this, rather than the more usual vague wording without numbers.

One hopes that the company can sue its supplier, to recover some or all of these losses. This is not mentioned in the RNS. There is also reputational damage to think of - customers affected by this warranty issue might buy competitor products in future perhaps?

In itself though, the above is clearly not anywhere near enough to have triggered a 47% share price fall. There is also a warning for the current year, which looks a lot more serious.

2016 profit warning - this looks pretty dreadful:

Challenging trading conditions in France, principally due to overstocking, and weaker sales in Germany, due to product certification delays, are likely to significantly adversely impact the Group's expected results for this year. Consequently, the Board has revised its guidance for the full year 2016. Subject to no major changes in exchange rates, the Board now expects a first half operating loss* of approximately £1.9m (which includes a restructuring charge of £0.2m as a result of reducing certain fixed overheads), and an operating profit* in the second half of approximately £3.8m with sales and operating profit* in the full year of approximately £55.0m and £1.9m respectively. The estimated saving in 2017 from the fixed cost reduction is approximately £0.8m.

So loss-making in H1, and only a £1.9m profit anticipated for the full year. That's a long way below previous guidance of £8.3m given just over a month ago. Although as above, hats off to the company for giving profit guidance to the market - if some companies can give profit guidance to the market, why can't all companies?

Outlook - the company hopes to get things back on track by 2017:

We expect to rebuild trading momentum in the second half of 2016 with certified new products and enter 2017 with normal levels of trading.

Whilst regrettable, the overhead reductions will put the Group onto a lower cost base saving an estimated £0.8m in 2017 and keep the Group on the right course to deliver our longer term strategic objectives as set out last year by Neil Smith, the Group CEO.

Cash position - the company reports today that it had net cash of £22.4m at 31 Dec 2015, so that protects the downside risk - there's no danger of it going bust. Also the 2015 dividend is still going to be paid, but it doesn't say what amount.

My opinion - the product warranty issue is a nuisance, and probably deserves a say 10% fall in share price. The real damage though is the collapse in 2016 forecast profits. This really casts into doubt the whole business model of this company.

It looks as if the bumper profits of 2014-2015 were a bit of a one-off. We already knew that bumper sales in France were caused by a law requiring the fitting of smoke alarms. However, bulls in the stock hoped that new products would take up the slack. Clearly that has not happened.

The shares are supported by the cash pile, but I think for the time being the bull case has really gone out of the window. It's difficult to know what level of sustainable profits the company can generate, which is key to valuing the shares.

So for now, I can only really put a question mark next to valuation. As the shares are illiquid, then who knows where the share price might settle? I'm inclined to sit on the sidelines for a few weeks/months, and see what happens. That also gives time to watch the RNS to see what "holding in company" statements are issued - giving an idea what the big institutional holders are doing. Ideally, I look for the big holders to buy, in support of the company & share price. If they are selling, then I think it's usually best to wait until they've finished selling, before considering a purchase.

Bad luck to holders here - I know quite a few friends hold this stock.

People's Operator (LON:TPOP)

Share price: 30p (down 14.3% today)

Share price: 77.1m

Market cap: £23.1m

2015 results - these numbers are a joke, and the least time spent on it, the better.

The company is generating a gross loss - i.e. it's selling telephony services at a lower price than it has to pay to provide the service. That's just plain bonkers.

Sure there's plenty of top line growth (from a low base) - I'm sure customers are happy to use services that are provided at below cost price.

The company managed to generate a £10.4m operating loss, on £2.1m turnover.

There's only £8m cash left, so the begging bowl is likely to be out fairly soon, for more cash. I'm not sure whether investors will be quite so wowed by Jimmy Wales' name, after seeing such diabolical trading figures.

The company says it has very low cost customer acquisition. So the big question is this - where's all the money going then? There must be a large central overhead.

My opinion - after a few bad experiences, I try to avoid blue sky, heavily loss-making companies like the plague. They nearly all go wrong - taking far longer, and costing far more than originally planned. Early shareholders are the mugs who get diluted down to nothing, when the discounted placings are done later to keep things going.

Why take the risk, when hardly any companies like this actually deliver what they say they're going to deliver?

I put this share on the Bargepole List less than 4 months ago, and it's already down about 64%. The thing is, you can spot things like this a mile off. So I continue to be amazed that brokers can find institutional punters who are prepared to chuck other peoples' money into such questionable & unproven business models.

I hope TPOP works, because it supports charities. However, to date it's shareholders who have provided the charity.

From what I've observed, you have to be so careful with loss-making tech companies. There is a Silicon Valley mentality in a lot of them - where management and staff are convinced of their collective genius. Losses and cash burn are regarded as of negligible importance. The assumption is that each round of funding will be easy to secure, and at incrementally higher share prices.

In a bull market, shareholders can become caught up in this madness, and end up hugely over-paying for companies which don't have any commercial viability. However, the bubble has already burst for some such companies. Shareholders now want to see real progress, and a road map towards profitability. This is a rude awakening for some smaller tech companies, which are forced to slash costs, and race for breakeven (as has happened with Synety (LON:SNTY) for example).

So for TPOP, I think they may well find that the mood for another fundraising is very different to when they floated. So I imagine a deeply discounted placing is probably on the cards. However, the growth might be enough to excite investors - as we saw recently with Koovs (LON:KOOV) - an apparent basket case, but generating enough growth to swing the pendulum of investor mindset from gloom to excitement again.

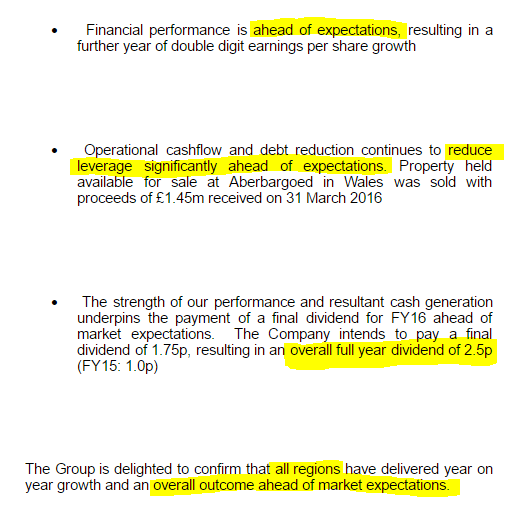

International Greetings (LON:IGR)

Share price: 175p (up 12.2%)

No. shares: 59.3m

Market cap: £103.8m

(at the time of writing, I hold a long position in this share)

Trading update - relating to the y/e 31 Mar 2016. This looks to be a business that is firing on all cylinders:

I like big increases in divis, as it demonstrates confidence, and a positive trajectory in what might initially be a modest dividend yield. However, increasing the divi by 150% means this could become a decent yielding share in the future.

My opinion - I've held this share for a while. Although there were some balance sheet issues, these are being sorted out well. Also, a series of upbeat trading statements, gives the impression of a company that is really going places.

Gervais Williams of Miton Group was raving about this company and its management at an investor event last year. I'm a great believer that when good stockpickers meet management, and come away impressed, then it's worth including that ingredient in your overall investing hot pot.

The forecast PER is still reasonable, something like 12-13, after today's share price movement, and also allowing for forecasts to probably rise a bit. Given that the valuation appears reasonable, and the Directors sound confident, then I'm happy to continue holding.

Lakehouse (LON:LAKE)

(at the time of writing, I hold a long position in this share)

Many thanks to reader Imranawan, who flagged up in the comments section below, that the Board of Lakehouse seems to have have reached agreement with the EGM requisitionists (Slater Investments, and the founder Steve Rawlings) as to the future Board composition.

I'm very glad that agreement has been reached, as public mud-slinging between the parties can only damage the business.

Right, I have to dash now. See you tomorrow!

Regards, Paul.

(usual disclaimers apply)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.