Good morning!

I'm starting to get nervous about the banking system again. That's partly because I've been reading Mervyn King's outstanding book, "The End of Alchemy" - highly recommended. It's also because there are persistent press reports concerning Deutsche Bank, and it's vast derivatives exposure.

So it seems as if we could be sleep-walking into another financial crisis. This has been worsened considerably by Angela Merkel ruling out a Government bailout for Deutsche Bank - probably the worst possible thing she could have said. Counter-parties will probably now be asking whether it's worth the risk to continue doing business with Deutsche.

All major banks are too big to fail - that's the big lesson from 2008. In extreme situations, they have to be rescued by the state, however unpalatable that may seem - as the alternative is unthinkable - a complete collapse of the financial system.

I think another crisis is actually necessary, as only then will Governments properly rein in the activities of banks. There needs to be much tighter regulation, to stop them creating vast risk, and eventual losses through derivatives. This could all get rather dangerous for the markets, so I'm considering my options at the moment - it might be time to take some cash off the table perhaps? And/or put a few large cap shorts in place as insurance against a market sell-off?

Boohoo.Com (LON:BOO)

Share price: 99.25p (up 1.5% today)

No. shares: 1,123.3m

Market cap: £1,114.9m

(at the time of writing, I hold a long position in this share)

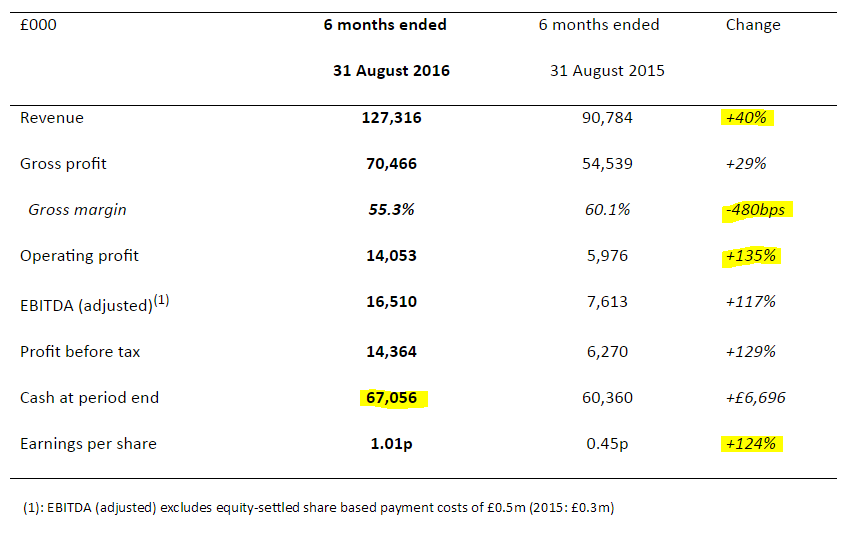

Interim results, 6m to 31 Aug 2016 - excellent reporting timeliness - publishing interim figures just 27 days after the period end is good stuff - clearly the FD and his team have good internal controls in place.

Why am I still reporting on this share, now it's over £1bn market cap? Well, partly to crow about one of my biggest successes in the last couple of years! Also because I know that a lot of readers followed me into this share after the market threw us a bargain in Jan 2015 at a quarter of the current price.

The interim figures today are excellent, and well ahead of forecasts. Brokers are upgrading full year forecasts as a result. Peel Hunt puts out the best research I've seen on BooHoo, so those are worth asking your broker to source for you. PH has raised this year (ending 28 Feb 2017) to EPS of 1.8p. Although personally I think 2p EPS could be on the cards.

In valuation terms, that gives a current year PER of about 50. So clearly this share is now expensive. The question is whether the growth & future potential of the business is worth paying up for. That's a decision each investor has to make for themself, based on their risk tolerance. Personally, I've top-sliced my holding on the way up, which is a nice compromise, as that way you've banked some of the profit, but still benefit from any further upside.

Market sentiment could change of course. We've seen lots of growth company shares go through the roof this year. So if something has gone from a PER of 20 to a PER of 50, then that's a bit of a one-off gain. It could of course quite easily reverse, if the market has a big correction.

Mind you, when you look at the highlights from today's figures (see below), there are some fantastic growth trends underway here. Remember this is all organic growth too, and it's international, not just UK;

Very strong top line growth, up 40% year on year.

Note there's a sharp fall in gross margin. The company has been rather clever here. What they've done is to deliberately plan for lower selling prices (which were already under-cutting most of the High Street). At the same time, they reduced marketing spend (which was enormous, at over 10% of turnover). This makes complete sense to me - after all, there are only so many ads which customers will respond to - the law of diminishing returns kicks in beyond a certain point. Much better to lower prices, and drive growth that way, as obviously if customers see bargains, they buy more.

Hence the profit line and EPS are up triple digit percentages, proving that accepting a lower gross margin results in a better overall result in profit terms.

Growth in overseas territories is encouraging, particularly 93% growth in the USA. That would be a rather good market to crack, given its size.

Balance sheet is excellent, with £67.1m of net cash (rising). Note that continuous capex is needed, to increase warehouse capacity. Some quite chunky forex derivatives losses have popped up.

Outlook - this is all self-explanatory;

As a result of our continued momentum in the UK and encouraging growth in selected overseas markets, we now expect revenue growth for the full year of between 30% and 35%, reflecting tougher second half comparatives.

Following the success in the first half of the year we will continue to look for opportunities to invest in marketing campaigns and our customer proposition to drive future sales growth and improve customer lifetime value. We will also be making significant investments in our IT systems and Ecommerce platforms. Consequently EBITDA margin for the full year is expected to be around 11%.

My opinion - this is a fantastic company. I've been saying for a while that it's actually better than Asos - because it's delivering strong growth, and decent profitability. Whereas Asos has seen its profit margin relentlessly falling, and is really now very low.

On conventional valuation grounds, BOO may look expensive now. However, PER is not a good valuation method to use for rapid growth companies. Also note that BOO has seen earnings expectations constantly rising - e.g. a year ago it was expected to do 1.35p EPS this year. I reckon the final outcome is probably more likely to be about 50% higher than that, around the 2p EPS level. This is why people have been buying the shares - they've worked out that the company is on a roll.

Online is doing serious damage to the High Street retailers now. Companies like BOO have cut out the middlemen. The people behind BooHoo used to be the biggest supplier to my old employer, Pilot - we had a chain of about 150 shops mostly in the UK, which we built up in the 1990s. Sadly, Pilot is no more, in terms of a High Street presence anyway, but our former supplier has now morphed into BooHoo, and supplies the young female end customers direct, via their smartphones & tablets. The product is so cheap that it's almost disposable fashion, to wear once or twice, then throw away. It's really difficult to see how High Street competitors, with their enormous overheads of a large branch network, can compete at the cheap end of the market.

As regards BOO, yes the shares look pricey now. However, I think the growth, and international potential, means this valuation of almost 100p per share can be justified. Providing nothing goes wrong of course.

In my view, management here are exceptionally talented, experienced, ambitious & hard-working. So that also justifies something of a premium. So it remains one of my favourite shares, although I'm mindful that the price is looking a bit on the high side now.

Also, note that the company appears to be inching towards doing a deal to integrate PrettyLittleThing.com which is operated by one of the sons of BooHoo's founder. It's always been an uncomfortable conflict of interest, so I feel that BooHoo really has to exercise its £5m Call Option. Peel Hunt says it's "fairly certain" that BOO will indeed decide to acquire PLT before the Mar 2017 deadline.

Longer term, I believe that BOO is likely to create new brands, and standalone websites, targeting different demographics. So the growth could continue for the foreseeable future.

Time for lunch now, then later this afternoon I'll be adding sections on;

Pennant International (LON:PEN)

Premier Technical Services (LON:PTSG)

Share price: 74.75p (up 1.7% today)

No. shares: 88.1m

Market cap: £65.9m

(at the time of writing, I hold a long position in this company)

Interim results, 6m to 30 Jun 2016 - it seems a sluggish reporting cycle, to be reporting June half year figures now, almost 3 months later.

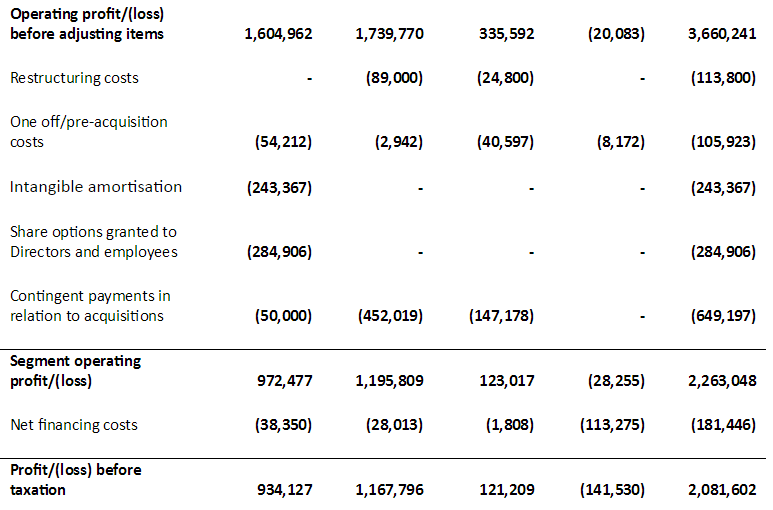

The P&L figures look good, with strong growth reported - both organic, and from acquisitions made in 2015. However, I have 2 reservations about these figures;

1) In both H1 2015 and 2016, adjusting items contribute materially to profits. The table below shows how statutory profit of £2.08m is boosted to £3.66m by various adjustments.

2) The other issue with the accounts is that debtors (sometimes called receivables) seem excessive.

The balance sheet shows £17.2m in receivables within current assets. This figure measures the amount of unpaid invoices which PTSG has sent to its clients, but hasn't yet been paid for. I would expect this to be about the equivalent of 60 days' sales.

Sales were £18.5m for the entire 6 month period. So the £17.2m receivables figure is way more than 60 days. It's not far off the entire 6 months' turnover! This suggests that PTSG's customers have hardly paid it anything for the services it performed for them in the 6m to 30 Jun 2016.

Now, as a UK business, PTSG's receivables figures will be inclusive of 20% VAT. So we can reverse that out, and receivables excl.VAT drops to £14.3m. Divide that into £18.5m turnover (which is always stated excl.VAT), and it's equivalent to 77.3% of 6 months, which I make 141 days. That's way, way too high. So it's a red flag for me, and I'll ask the company why its receivables figure is so excessive.

Balance sheet - overall it's not strong, with £11.0m NAV dropping to only £0.4m NTAV once intangibles are written off. The level of debt looks reasonable, given decent profitability.

Outlook comments sound fine.

My opinion - I hold a small long position in this share, but don't feel confident enough to want to increase it. I like the niche markets, with recurring revenues, which PTSG addresses. Management seem impressive, with a strong focus on efficiency & using their in-house designed software to sweat assets & staff hard.

On the downside, the excessive debtor days bothers me a lot. Also I feel the company has been excessively generous with share options. The shareholding structure is not ideal either, with Directors owning most of the company, but with a stated intention to dribble out stock to Institutions over time, as demand crops up. That could limit the upside for other investors, as it's effectively a large overhang which the market knows about - hence institutions won't need to chase the share price higher.

Overall then, I'm probably neutral at the moment on this one. I'll keep my little scrap of stock, to keep me interested, but have no desire to buy any more right now.

A few quick comments to round off with;

Alternative Networks (LON:AN.) - There's a fair bit of detail in this trading update, but it seems to be a mild profit warning;

The Board now expect an Adjusted EBITDA* for the year ending 30 September 2016 somewhat below management's previous expectations.

This company is a cash cow in terms of divis, but I reported in Feb 2016 my concerns about how sustainable its profits are?

FinnCap has today lowered EPS estimate for y/e 09/2016 a fair bit - from 28.3p to 24.4p EPS. This is on the back of previous downgrades. So EPS forecast is now down almost a third from where it was a year ago. I don't like that at all. This is why the share price has almost halved in the last year. I think the big divi yield here could be a bit of a value trap - an apparently cheap business, but one which is going downhill.

Universe (LON:UNG) - interim figures out today look OK, although it seems to have a heavy H2-weighting to performance, judging by the prior year comparatives.

There's a mild profit warning for the full year, due to some project delays, but it doesn't sound too bad;

The first six months of this year saw steady progress in piloting new products in the new customer estates. We confidently expect full-scale deployments of these to begin shortly. However the delayed start means that we will be slightly below management expectations for turnover and profitability for this year. Nonetheless, we still believe that prospects for continuing growth remain encouraging.

The shares are down 14.5% today to 9.3p. It doesn't interest me.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.