Good afternoon!

I spent yesterday afternoon catching up on the backlog from Friday, and ended up digging into an AIM-listed Barbados hotel chain called Elegant Hotels (LON:EHG) . What an interesting company. I was tempted at one point to buy a few shares in it, but overall was put off by 2 specific factors - click here for that report. It's one for the watch list anyway, but I'm expecting profit warnings to come in 2017.

Bioventix (LON:BVXP)

Share price: 1485p (up 2.4% today)

No. shares: 5.1m

Market cap: £75.7m

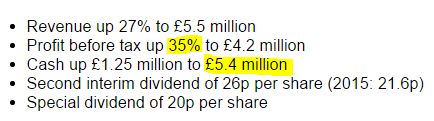

Results, y/e 30 Jun 2016 - this is a terrific set of results. The headlines section is most impressive;

This company operates in an astonishingly profitable niche, with one of the highest net profit margins we'll ever see - profit before tax is 76.5% of turnover. I've wondered in the past if that would be sustainable, but so far, so good.

The barriers to entry seem to be that each new product takes years to develop & test. Also, the volumes are possibly too small to attract any serious competitors. Although such high profit margins do make me nervous, hence why I don't hold this share.

Well done to people that do, as its track record is absolutely superb, and shareholders must be delighted with today's figures. It's good to see some surplus cash being paid out in divis too.

Diluted EPS has risen strongly from just under 50p, to just under 68p - again, tremendously impressive. That gives a PER of 21.8 - a rich rating, but fully justified by these numbers I feel.

Balance sheet - is very strong. Although debtors looks too high at £2.7m. Considering the full year's turnover was only £5.5m, its customers seem to be very slow in paying.

I've just found an explanation for the large debtor balance in the narrative;

Approximately three quarters of Bioventix sales are generated from customer royalties. These are based on our customers’ global sales which are then factored by a royalty percentage and then sent to Bioventix around 2 months after the end of each half year.

In the first half of 2016, this mechanism resulted in $ based and Euro based royalties being converted into sterling around August at post Brexit exchange rates of approximately 1.3$/£ and 1.2Euro/£. As no hedging mechanisms are employed, this provided an additional uplift in reported sterling revenues compared to previous periods.

So the depreciation of sterling has been a help in boosting profits.

Outlook - it sounds like growth will slow in the new year.

We are delighted to be able to report such positive news for the current year. Furthermore, we remain optimistic that further modest growth next year will come from additional vitamin D antibody sales and royalties.

Beyond that, growth in the period 2017 2020 will be linked to our troponin project and the success of Siemens in their product launches around the world.

We continue our research activities as we look to seed additional projects that will germinate in the period 2020 2030 creating additional shareholder value.

My opinion - so far so good. It all hinges on whether profitability is sustainable, and what levels of growth will be achieved in future. A recent spike in share price was apparently caused by it being tipped in a tip sheet. Sometimes those spikes can wear off, as people get bored and drift on to the next hot tip.

Overall though, it's difficult to fault Bioventix, having a superb track record of profit and divi growth in recent years. The shares are illiquid, so there can be large & rapid moves in share price.

Zytronic (LON:ZYT)

Share price: 386.5p (up 1.7% today)

No. shares: 15.4m

Market cap: £59.5m

(at the time of writing, I hold a long position in this share)

Trading update - for the year ended 30 Sep 2016.

Underlying trading looks good;

Reported profit before tax for the full year will reflect the impact of a c. £0.9m non-cash provision arising from the Group's foreign exchange policy; however, the Group's underlying profit (before this non-cash item) is expected to be significantly ahead of last year and at least in line with market expectations.

Zytronic is a UK producer of bespoke touch screens. It exports practically all of its production, so should be a big beneficiary of the recent plunge in sterling. However, in the short term it looks as if the company's currency hedges have backfired. Still, that's what happens with currency hedging - sometimes it's profitable, sometimes costly.

Looking through the 2015 Annual Report, it says this about foreign currency hedging arrangements;

Risks associated with currency movements: A large proportion of the Group’s sales are denominated in US Dollars and Euros, so the Group is subject to risks associated with currency movements. It is the Group’s policy to manage these risks and provide a degree of certainty for cashflows into the UK without taking the risks of speculative positions.

Natural hedging is adopted to manage currency risk, whereby goods and services are sourced from Europe and the USA and the liability arises in the respective currencies. Surplus currency is then protected through the use of forward foreign exchange contracts for a period of twelve to 18 months ahead. This ensures the business knows its position around FX in the current year.

If my understanding is correct, it sounds as if the company must have forward sold its net dollar & Euro receipts, into sterling at less favourable rates than would now be the case.

This is just a transitory factor. Obviously it would have been much better if the company had not entered into hedging arrangements - indeed as Bioventix (above) showed, not using hedging has boosted its profits considerably. Whereas Zytronic took a more prudent view, but it has backfired this time. Such is life.

The important thing is that underlying trading at Zytronic is good, and is likely to continue to be strong, given that it now has the benefit of weak sterling making its products much more competitive in export markets.

My opinion - I remain positive about this share - it's good value, pays decent divis, and has a smashing balance sheet with plenty of net cash. Plus it should now be a big beneficiary from weak sterling. Plenty to like then. The £0.9m hit from currency hedging this year is by the by really, nothing to worry about - more bad luck than anything, that exchange rates happened to move against their hedges. They will more than recoup that cost from improved profits going forwards, as a UK exported.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.