Hi, it's Paul here.

Loungers (LON:LGRS)

I have just published part 2 of my video review of the Loungers AIM Admission Document. Thank you for the kind comments on part 1.

Here is the link to part 2. It is 27 minutes long. I hope you find it useful/interesting. Please don't share that link publicly, as it's intended for Stockopedia subscribers, you after all are paying my (modest) fees.

Good news, it has recorded in high definition this time. So you can read everything clearly. If it's not clear, then go into settings, and you can increase the definition right up to 1080, how exciting! Then full screen it, and all is clear. The idea is you can then pause the video at any time, to inspect my notes on screen.

If people like my videos, then I'll make some more. If people like them, it's appreciated when people leave a thumbs up, as it indicates to me that it was worth the effort.

7-8 am quick views

Just realised I've got the hygienist, then the main man, so the morning will mainly be dentistry.

Good luck with everything, I hope there aren't any profit warnings.

Main report, after 8am

Loungers (LON:LGRS)

Share price: 226p (up 2.5% today, at 11:19)

No. shares: 92.5m

Market cap: £209.1m

Loungers, the operator of 148 café / bar / restaurants across England and Wales which trade under the Lounge and Cosy Club brands, announces a trading update for the 52 weeks ended 21 April 2019.

As mentioned above, I recorded a video review of this company's AIM Admission Document, for Stockopedia readers only (please don't post the links anywhere else);

Part 1 (37 minutes, medium definition)

Part 2 (27 minutes, high definition)

My main findings from reviewing the Admission Document, are that;

- It's a good business, growing strongly both in LFL sales, and from new site openings

- This is a great time to be doing a roll-out, as there are plenty of good sites available at modest rents & with incentives (e.g. long rent-free period, and/or landlords contribution to fit-out costs, called a reverse premium)

- However, it has far too much debt - the IPO only raised enough to clear about a third of the debt - this makes it too high risk

- Another placing will be necessary to reduce debt, and allow the private equity firm to exit fully. So the enterprise value is substantially larger than the market cap

- Taking into account the debt, shares look over-priced

Trading update - today the company reports;

Total revenue for the year was £153.0 million, representing total revenue growth of 26.4% over the prior year (2018: £121.1 million), and like for like sales growth of 6.9%.

The results for the year are anticipated to be in line with market expectations.

That's outstanding LFL sales growth, but not a surprise - it's consistent with the 5-7% LFL annual revenue growth over the last 3 years, disclosed in the admission document. How long the business can keep up that rate of growth, I'm not sure. Clearly the format is appealing to its customers - what do readers think, if you've visited one or more of their sites?

25 new site openings - as planned, and that number of new sites will be opened each year going forwards

146 sites in total - so plenty of scope for growth in the UK - "some fantastic sites in the pipeline"

My opinion - lovely business, but over-geared, and its shares look over-priced to me.

It makes Revolution Bars (LON:RBG) (in which I have a long position) look stunningly cheap, but that's because RBG is not delivering LFL sales growth (yet), and has paused its roll-out whilst it puts its house in order.

They're not direct competitors though - LGRS is an all-day concept, whereas RBG is really a late night venue. However, the financials are quite similar in some ways. RBG would make an excellent acquisition for LGRS actually - which could re-brand some of RBG's sites as Cosy Clubs perhaps?

It certainly gives an idea of the huge upside possible on RBG shares, if it gets its house in order, and is able to perform as well as LGRS. The jury's out on that at the moment, with new management at RBG yet to deliver a convincing turnaround.

When time is available, I'll write a report comparing the financials & valuations of LGRS and RBG.

Amino Technologies (LON:AMO)

Share price: 102p (up 10% today, at 13:17)

No. shares: 72.8m

Market cap: £74.3m

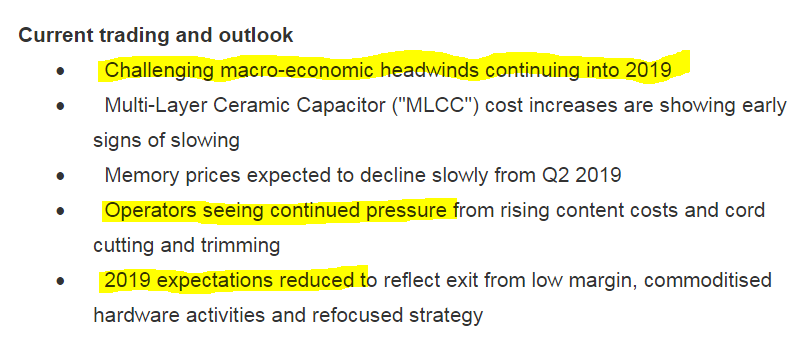

Amino, the global provider of media and entertainment technology solutions to network operators, announces a trading update for the six months ended 31 May 2019 ("H1 2019").

The share price is up 10% today, which surprises me, as the company is only confirming that it's trading in line with full year expectations;

We have made good progress with the transformation programme announced in February 2019, which will support an acceleration of our focus on value-added software, services and hardware. The programme was completed on schedule in April 2019 and is expected to deliver annualised cost savings of $5m as planned. The Board's expectations for the full year therefore remain unchanged.

Outlook comments don't sound madly exciting either.

The last point below almost sounds like a profit warning. I think it must be referring to a previous reduction in forecasts?

Revenues in H1 fell 15% vs LY H1, to $35m. The full year forecast shown on its StockReport is $84.1m, so that's implying a hefty 40% step up in sales from H1 to H2. I've checked on Research Tree, and it looks like the latest broker note from FinnCap is forecasting $69.9m revenues, a flat from H1 to H2. Some difference! Unfortunately Thomson Reuters data for small caps is not always bang up to date, so it's always wise to check back to broker notes if you can get hold of them. If I spot something that doesn't look right, I always raise a ticket using that green blob on the bottom RHS of each page here, to alert the team at HQ, who get Thomson Reuters to correct any errors.

The forecast of $0.14 EPS is also too high. The latest broker note forecasts $0.129, or 10.2p. Therefore the PER for the current year is actually 10.0 - which looks good value.

Dividends - Amino has been a generous divi payer for some years now, and it said this back in Feb 2019 with the last full year accounts;

"The Board remains confident in the strength and strategic direction of the Company and has committed to continue its dividend policy for this financial year and maintain this dividend level for at least two years thereafter...

[NB. above extracted from Feb 2019 results].

It's forecast to pay $0.093 this year, which is 7.3p. Therefore over the next 3 years shareholders should be paid 21.9p in divis. Not bad when the share price is 102p. Therefore this share has attractions for income seekers.

Cash - it reports net cash of $19.3m, up on a year earlier, but down a little from $20.3m at last results date of 30 Nov 2018. That looks to be down to the final divi being paid on 26 April 2019.

My opinion - I don't know anything about its sector, hence cannot form an informed view on the company's prospects. That said, the update today sounds reassuring. The PER is low, divi yield high, and the balance sheet is strong, with plenty of cash.

Altogether then, it looks a good value share. If the revised strategy delivers results, and profits start rising again, then this share could re-rate. Quite interesting at this level, in my opinion.

All done for today.

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.