Good morning!

The Covid-19 outlook has not improved over the weekend - expectations for the duration of the 'lockdown' period are lengthening.

This report won't be locked down, however. Business as usual here.

At 7.30am, FTSE futures are trading almost unchanged at c. 5500.

Cheers

Graham

Agenda for today (COVID-19)

There are a vast number of RNS updates, again, as companies scramble to update investors in light of the Coronavirus situation.

I can't help the feeling that we are in some type of a "doomsday" scenario for many businesses. Even during wars and recessions, many businesses were still open and operational.

This virus (or the government's response to it, depending on your point of view) has completely shut down huge parts of the economy. It's an unthinkable scenario - who could ever have imagined it?

It's a punishing situation for people who are leveraged, in their portfolios or their personal lives.

I thought that I was sufficiently careful, only buying shares in financially strong corporates and using only a very modest degree of leverage in my trading account.

It turns out that I might not have been careful enough: even financially strong companies such as Next (LON:NXT) (in which I have long position) may struggle, if they are forced to stay shut for six months. And while I wasn't forced to close any positions (e.g. due to margin calls), March has been an uncomfortable month.

But again, who could have predicted a scenario in which vast swathes of the economy would be forced to shut down?

I am loath to get involved in a political debate on a financial blog, but I do feel compelled to share this article by Professor John Lee (retired).

While demonstrating some important ways to understand the statistics you see in the media, the article also strengthens my suspicion that government policies are being driven by fear, not by a calm understanding of the facts and the alternatives.

However, there is nothing that I can do to influence policy. The only thing I can do is manage my portfolio as best as I can, and try to share a few nuggets of wisdom with you.

Discussed today:

- Easyjet (LON:EZJ)

- Purplebricks (LON:PURP)

- National Milk Records (OFEX:NMRP)

- Alpha FX (LON:AFX)

- Audioboom (LON:BOOM)

- Finablr (LON:FIN)

- Ten Lifestyle (LON:TENG)

I failed to get to: Numis (LON:NUM), Somero Enterprises Inc (LON:SOM), United Carpets (LON:UCG), Macfarlane (LON:MACF), Franchise Brands (LON:FRAN).

Timings: Finished at 4.50pm.

Easyjet (LON:EZJ)

- Share cap: 551.2p (-7%)

- No. of shares: 397 million

- Market cap: £2.2 billion

Not a small-cap. However, since air travel is basic to the functioning of a modern economy, I think this is worth a mention.

Easyjet has "fully grounded its entire fleet of aircraft":

easyJet and Unite the union have collaboratively reached an agreement on furlough arrangements for its cabin crew. The agreement will be effective from 1 April 2020 for a period of two months and means that crew will be paid 80% of their average pay through the Government job retention scheme.

The company says it has no debt refinancings until 2022 - that's some comfort, I suppose. And with the job retention scheme in place, a great deal of the cost base will be covered.

As of year-end, EZJ had cash of £1.6 billion and borrowings of £1.9 billion, giving rise to a small net debt position of £0.3 billion.

That £1.6 billion warchest would, you'd think, give it plenty of flexibility to deal with serious problems in the short-term.

Ryanair Holdings (LON:RYA) is a much bigger company and yet it has a similar positioning: net debt of €460 million as of September 2019, and a huge cash pile of c. €4 billion.

Earlier this month, Michael O'Leary said:

Ryanair is a resilient airline group, with a very strong balance sheet, and substantial cash liquidity, and we can, and will, with appropriate and timely action, survive through a prolonged period of reduced or even zero flight schedules...

My view

I don't invest in airlines when times are good, and I can't see myself buying shares in them when their fleets are grounded. Maybe at a big discount to tangible book value, I could start to get a little bit interested?

Purplebricks (LON:PURP)

- Share price: 38.55p (+2%)

- No. of shares: 307 million

- Market cap: £118 million

As a "hybrid" estate agency, PURP should be better-prepared than most of its peers for the shift online.

There is nothing it can do, however, about the fact that house transactions are likely to collapse in the short-term.

Government advice is to delay house moves until the "stay-at-home" measures are ended (only vacant properties are excluded). PURP references this advice in today's RNS.

Company response: PURP is doing what all companies are doing now - preserving cash, examining its costs, reducing overheads. No more advertising, and the marketing budget has been slashed.

Cash balance - £35 million, and no debt. That's what you want to hear, in times like this.

Cash was £41.6 million at the end of October, so the burn has been c. £1.3 million per month.

My view - I never said much that was positive about this company.

My stance on it is now changing, because:

- it has given up on the disastrous expansion plan in the US, and in Australia

- it can probably make money in the UK, and is around breakeven in Canada

- the cash balance, mentioned already, can underwrite its valuation

- the share price is now much, much lower than before

At the current share price, cash accounts for c. 30% of its market cap.

In other words, there is no need for me to be uber-bearish on this stock anymore. It has fallen enough.

If it keeps falling, and approaches the value of its cash reserves, then I might even start to think that it is cheap.

Incidentally, that could be a great signal that the stock market is cheap - when there are large numbers of "net-nets" (stocks trading below the value of their net working capital).

National Milk Records (OFEX:NMRP)

- Share price: 109p (unch.)

- No. of shares: 21 million

- Market cap: £23 million

This is a niche company that provides data services to the cattle industry. Please note that it is listed on the NEX Exchange, not AIM.

NMR staff are considered "key workers", since they are part of the food supply chain. This helps, though NMR says childcare availability could be an issue (there is a question mark over whether schools will open during Easter, for the children of key workers).

Other issues:

- NMR's core milk testing service will be "largely uninterrupted"

- Farmers may need to collect their own samples and this may impact earnings while the Covid-19 outbreak is ongoing.

Balance sheet - at the end of H1, this company was not exactly groaning with cash. It had just £0.3 million, down £1 million from a year earlier.

It had been affected by some one-off factors, including an unusually large debtor balance which was expected to unwind.

Today, the Directors say they "remain assured that the Company has sufficient liquid funds and access to debt facilities for its current purposes. We are nevertheless acting prudently to preserve cash to ensure investment in new projects planned for 2020 can go ahead."

My view - this business might get through the crisis relatively unscathed. The demand for milk isn't going to change much, and farmers will still want the data that NMR provides. I also would tend to agree that the cash balance is likely to improve, as debts are collected.

The market shares my view - NMR's share price is virtually unchanged, year-to-date.

Alpha FX (LON:AFX)

- Share price: 382p (-41%)

- No. of shares: 37 million

- Market cap: £142 million

This update starts off with a sales and profit warning - no surprise, since we are clearly on course for a recession and international trade is taking a huge hit.

Then we get bombshell news:

- 223 clients faced margin calls as a consequence of the very sharp currency movements. That's a third of all clients.

- One client, a food exporter, "requires more time" to make £30.2 million in payments to AFX. A payment plan is being negotiated, so that AFX will get its money back by mid-2022.

- The delay "has created a temporary shortfall" in AFX's own cash, which it needs to use as collateral for the running of its own business.

For context, AFX's operating profit over the last two years adds up to £23 million - less than the amount owed by this single client.

For more context, AFX's adjusted net cash figure was £38.6 million at the end of 2019. The delay in payment by the client has, I guess, blown a huge hole in this number.

What were the signs?

Not many people (myself included) though that this sort of blow-up was possible.

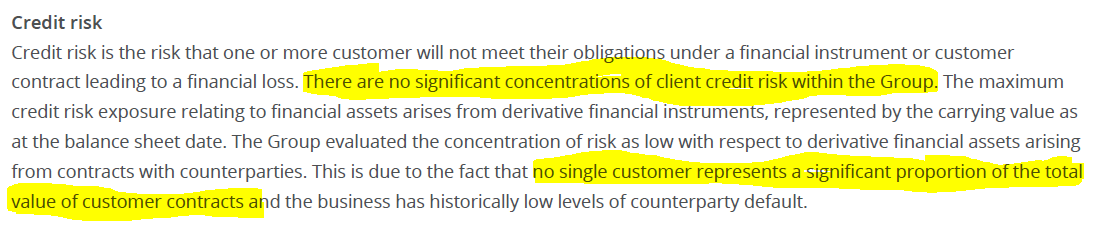

I've dug up the 2018 Annual Report, and found this in the Risk Management section:

This should be a calming paragraph. In hindsight, it's quite alarming!

If it's still true that "no single customer represents a significant proportion of the total value of customer contracts", then the food exporter currently in default must not be particularly large, relative to other credit risks at AFX and the total credit risk it faces. There must be many other large risks on AFX's books.

However, today's announcement also states that the defaulting client was previously responsible for 15% of AFX's forward book. In that case, how can the statement from 2018 regarding credit risk be true? Perhaps this client did not become particularly important until 2019?

That might be the explanation which makes the most sense, based on AFX's disclosures.

It also says today:

Outside of this, Alpha's next largest position is a Dollar-Polish Zloty exposure split across two separate clients, representing c. 1% of the total forward book

So the most likely scenario, to me, is that the AFX customer base used to be well-diversified, but then one client become extremely large during 2019.

Unfortunately, this does not reflect well on the quality of the revenue growth that was recently reported for 2019.

Underlying leverage

In Note 14 of the 2018 Annual Report, AFX reported derivative assets with notional principal of £1.05 billion and derivate liabilities with notional principal of £0.7 billion. Most of these deals are with customers, not with banks.

These big numbers represent the underlying amounts being hedged by currency deals.

The same numbers for 2019 will have been significantly larger.

Up until now, the associated risks have been well-managed at AFX.

But the recent volatility has truly been extraordinary, and not just in the equity market (where the VIX reached an all-time high this month).

We have seen crazy swings in the currency market too, where the perceived safe haven of the dollar in a crisis has resulted in the value of other currencies dropping dramatically.

The sharp drop in the Norwegian Krone (NOK) is what caused the problem for AFX's client. According to AFX, the recent weekly move in NOK was "nearly three times its previous largest fall", which was during the 2008 crisis.

Hedges are supposed to reduce risk for AFX's clients. What we've just seen is an example of what happens when hedges go wrong, and increase risk, by creating cash flow problems that can't be solved.

My view

If the client fails to make the repayments, that will clearly be a huge blow. On the basis that the client will make the repayments, then there are further grounds for optimism:

- the remaining customer base is said to be well-diversified

- international trade is currently at a low, but will presumably recover and the recent volatility will help to justify the use of hedging strategies

- the cancellation of the dividend will provide AFX with some extra cash to use as collateral (£2 million)

- £9 million of collateral has been released from the ex-client's account, and can be used as collateral for other clients

AFX will have to rebuild trust among its investors, and probably won't enjoy the very high multiple that it did before, for some time.

If it is as well-capitalised as it says it is, and the shortfall it is currently experiencing is truly temporary, then it may offer long-term value at the current level.

Not something I would have the conviction to bet on personally.

Audioboom (LON:BOOM)

- Share price: 150p (-4%)

- No. of shares: 14 million

- Market cap: £21 million

This podcasting company has been burning cash for years. 2019 is no exception.

The main event in 2019 was that the long-standing CEO decided to call it a day.

Farcically, he said on the day of his resignation that:

The business is now entering a more mature phase and I believe that the time is now right for me to pursue more entrepreneurial opportunities.

There is little evidence of maturity as far as the share price is concerned.

The new Board is trying to sell the company, but admits that this could be difficult in the current environment:

A number of interested parties are actively engaged in the process, but it is possible that Covid-19 could impact the planned timeline. At this point, potential buyer interest in the Company suggests the process will stay the course, but we will continue to evaluate the impact of Covid-19 over the coming weeks.

Even if the natural demand for podcasting content remains high while people are locked indoors, the rout in equities means that valuations generally are lower - and a lower price can be expected for BOOM's disposal, all else being equal.

I would steer clear of this. If a generous takeover fails to materialise, the cash-guzzling is likely to continue. $47 million in cumulative losses so far, and counting.

Finablr (LON:FIN)

- Share price: 11p (suspended)

- No. of shares: 700 million

- Market cap: £77 million

Auditor Resignation and Board Changes

This company has been suspended under the stench of corruption. It is closely related to NMC Health (LON:NMC), having the same shareholders who appear to have engaged in dodgy dealings.

Both companies had liabilities which weren't disclosed and which "may" have benefited third-parties.

On 12th March, it said:

...the Board has been reassured that the Company has no undisclosed related-party transactions or unrecorded on or off-balance-sheet financing arrangements.

On 16th March, it said:

the Board has been informed of the presence of cheques (written by Group companies and dating back to before the IPO), which may have been used as security for financing arrangements for the benefit of third parties. A preliminary view is that the amount of these cheques totals approximately US$100 million. The existence of these cheques has only recently been brought to the attention of the Board and urgent investigations are ongoing.

And now the auditors have had enough:

The Company announces that it has been notified by Ernst & Young LLP ("EY") of their resignation as auditor of the Company. In their letter of resignation, EY cited "concerns arising out of recent events at the Company and NMC Health plc…the composition of the Board of the Company, the adequacy of corporate governance concerns and the recent issues that have caused the Company to commission an independent review of the Company's financial arrangements, including of related party transactions and on and off- balance-sheet debt".

It's hard enough to make money when companies are honest. When they are corrupt, it's simply impossible.

Not all foreign companies which list in the UK are fraudulent, but enough of them are. Avoiding all of them is a sensible decision.

Unless there is a very good reason to list in the UK, rather than somewhere else, it is safer to assume that it's a fraud.

Ten Lifestyle (LON:TENG)

- Share price: 46.15p (-5%)

- No. of shares: 80.7 million

- Market cap: £37 million

Covid-19 update and cost-saving initiatives

This provides a high-class concierge service. It has been hit hard by the slowdown in travel bookings and expects the a reduction in restaurant and entertainment-related services.

In more positive news, it had net cash of £9.6 million at the end of February, and no debt - excellent.

And 150 employees and contractors have backed it by taking options priced at 70p, exercisable for three years, in lieu of their normal salary payments. This saves the company £0.8 million in cash.

That's an excellent sign of conviction by insiders, who are cleverly taking advantage of the reduced share price. They clearly think that this can recover to its former highs, around 120p.

Out of time for today. Paul will be back tomorrow.

Cheers

Graham

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.