Good morning, it's Paul here.

This is initially a placeholder article, for subscribers to leave your early comments on anything interesting on the RNS. I'll write up the main article throughout the morning, section by section.

Estimated timing - I'm aiming to finish before 3pm today.

Update at 14:45 - today's report is now finished.

.

Pubs re-opening

I ventured out into Bournemouth on Super Saturday , expecting to witness chaotic scenes of drunken Brits defying social distancing, and being rowdy. However, it was all rather calm & civilised from about 6-9pm when I was out & about.

Starting off in Holdenhurst Road (near the station), which is usually busy at that time, only 1 cafe was open - Sprinkles Gelato, a large, new ice cream parlour. It was almost empty. None of the other restaurants, or independent bars had opened. A reminder that whilst there are no business rates, and staff can be paid on furlough, the financial incentive is to remain closed, having a call option on whether to re-open at all. Hence the general approach by independents, seems to be wait & see, before deciding whether to struggle to re-open, or throw in the towel & hand back the keys to the landlord.

One pub was open, The Christopher Creek, which is a popular Wetherspoons. On arrival, I was greeted by a friendly staff member, who invited me to use the hand sanitiser, then explained that all service is now at table. So find a table, then order the drinks & food via the Wetherspoons app, which also takes payment by card through the app It worked great, and I sat outside, enjoying a couple of pints & a panini with chips, all good quality & cheap. Not having to rub shoulders with smelly people, which is an issue with some Wetherspoons, was a pleasing improvement.

Inside the pub, they had installed clear plastic screens between the tables, and I'm pretty sure there were fewer tables than before. It wasn't that busy. I talked to the security lady, and commented that it didn't seem very busy. Oh we've only just opened, there was a gas leak on the boiler, so that had to be fixed before we could re-open. A reminder that a lot of re-opening pubs are likely to have maintenance issues due to being closed for a while. The bar area is not to be used by customers at all. Customers walking into the pub looked delighted to be able to have a freshly poured pint again, and many seemed to be regulars, greeting the staff warmly.

Overall capacity of customer numbers must be way down (below half, I'd guess) on what would normally be allowed at peak times. Plus the number of staff is up, because they need extra people to meet & greet, control numbers coming in, and serve food/drinks to the tables. There was almost no "atmosphere" in the pub, just small groups of people sitting at tables, talking quietly.

Next stop was Old Christchurch Road, which is a tatty-looking, but busy road, full of takeaways, vaping shops, hairdressers & tattoo parlours. You can probably visualise the type of thing. I noticed that the takeaways were all open, but have been for some time, and are clearly busy, with groups of Deliveroo mopeds lined up. Restaurants have had to adapt, and the ones that have embraced takeaways are likely to survive, in my opinion. Others, probably not. One or two independent restaurants had opened, but in each case only had a handful of customers were inside, as I peered in the windows.

Revolution Bars, and all its nearby competitors are still shut for now. More maintenance issues, with minor vandalism evident on several shopfronts, and peeling paint, etc.

Next stop was a large pub called the George Tapps, or the George Tapas as I always read the sign. They don't serve tapas, which is a good thing, as I reckon that's a con - splitting the food into smaller plates, and then charging you more for it, as you have to order at least 5 plates to feel full. This pub is run by Stonegate. It also seemed very well organised, with a reception team of 2 staff also asking me to use the hand sanitiser, and then register my personal details through their app, called My Pub. They helped me navigate the app, and register my visit (for tracing purposes if an outbreak occurs), then allocated me a table - right in front of a huge screen with football showing, oh dear! Most tables were full of men in their 20s & 30s, bellowing at each other. Why is it that when people have had a few pints, they shout instead of speaking normally? Anyway, it was so noisy, I left after one pint. They had taped off half the urinals, for social distancing, which is marvellous - I hate having someone right next to me when relieving myself, so let's hope they keep this innovation permanently.

Everything seemed very well organised in both pubs visited so far. This must have taken a lot of organising, I commented to the slightly brusque security lady. "It's been like a military operation over the last fortnight", she confirmed.

Next up I headed further into town, to The Mary Shelley, a larger Wetherspoons. Same thing there - staff seemed on the ball, and were managing things very well. There was a short queue outside, then when tables became free, they were let in. I had a table of 4 for myself, which seems wasteful & damaging to revenues. I had a couple of pints & a cooked breakfast, which was OK, but cheap. The clientelle generally seemed quite tipsy (this was about 8pm), and I overhead doormen discussing people they had just thrown out. Also groups of screeching young women were completely flouting distancing rules, by hugging each other, etc.. Most people seemed to observe social distancing well, but if people see some friends out, then social distancing seems to go out of the window. Therefore, I imagine we're likely to see some new outbreaks linked to bars & restaurants. You can't completely socially distance indoors, especially when passing in corridors, or going to the loo.

In the centre of Bournemouth, the main drag for bars, called The Square (which is actually circular), was quiet, with just the usual skateboarders & tramps hanging around. Hardly any bars were open, just another Wetherspoons! That looked busy, with lots of people standing outside at the front, under a canopy, smoking & drinking.

I then tried to get into a Slug & Lettuce, but was turned away by 2 rather smug doormen. "Have you got a buggy?" they shouted to me from a distance, as I halted at the halt sign, halfway up an outside stepped pathway. How strange. They must think I'm a single Dad, and need some help with my pushchair. Why on earth would they think that? Where do they think I've left my baby? "No, I haven't got a buggy with me today", I replied. "A booking! Have you got a booking?!" Oh no, sorry I don't. Then you can't come in I'm afraid. That was that.

A similar thing happened at another large bar, an O'Neills. The burly but affable doorman explained to me very politely that his total capacity was now just 100 people, when it had previously been 800. "But your beer garden is practically empty, I just wanted to stand outside there". I know, but 100 capacity is for the whole pub. Again, with maximum capacity at peak times down from 800 to 100, and with more staff needed, I don't see how this pub could possibly be profitable until these restrictions are removed completely.

Overall here are my key impressions;

- Very much a soft start, with only a few pub/restaurant chains re-opening, independents generally not

- Wetherspoons & Stonegate seem to be managing their pubs very well, from my small sample, observing the Govt rules thoroughly.

- The beer tasted good, so they seem to have surmounted the supply chain issues well

- Limited customer numbers mean pubs won't now have busy, profitable, peak times any more. Therefore I don't see how the sector can be profitable at all in the current circumstances, especially with increased costs too

- You have to book a table beforehand, to be sure of gaining entry to popular pubs/restaurants (opportunity for booking apps?), which may improve loyalty to particular pubs where you get used to using their app

- Customer experience is fine - I actually much preferred having fewer people in pubs, and ordering/paying from the table.

- If you can't interact with other people, then why go to a pub at all? Sitting at home with beer from the supermarket makes a lot more sense to me

How long before things return to normal? - Who knows, but if we have a vaccine/treatment in 2021, as seems possible, then the hospitality businesses that survive this crisis should become more profitable again, and with less competition. Hence I think this sector is attractive for investors who are willing to look beyond the current crisis. But don't expect pubs to be profitable any time soon - which begs the question whether their balance sheets are strong enough? There might need to be more dilutive fundraisings for some, possibly?

.

Boohoo (LON:BOO)

331p (down 15% today) - mkt cap £4.1bn

Allegations have resurfaced in the Sunday Times about a third party BooHoo supplier apparently operating unsafe sweatshops in Leicester, flouting social distancing rules, and paying below minimum wage. This issue was flagged up some time ago, and it all blew over, but the same thing has cropped up again.

Garment making almost completely disappeared in the UK in the 1980-90s. However, it has come back in recent years, e.g. in Leicester, with authorities turning a blind eye to sweatshop conditions & illegally low pay, probably through fear of being accused of racism - which seems to dominate the PC world of local councils. Whereas applying the law evenly & fairly, to everyone, is what we actually need. Why bother having rules, if they're not going to be enforced?

BooHoo has responded. It claims to not have had knowledge that some of its products were being made in a sweatshop. Whilst people might be cynical about this, there is actually some credibility to this. My experience in the sector is that orders placed with one supplier are very often outsourced to another factory, usually via family connections. Sometimes retailers are unaware of even what country their products are made in. Audit trails are a waste of time, because I found that suppliers will just sign anything. The only way to properly audit where & how garments are made, is to have physical boots on the ground, inspecting factories in person. With hundreds of suppliers, scattered around in multiple countries, that's complex & very expensive, hence why so many retailers don't do it.

BooHoo says it's working to raise standards, and details what is going to be done. The danger is that these repeated allegations may damage its brands, and lead to customer boycotts. Although in the past, the public have shown a very short attention span, with boycotts quickly fizzling out.

A dose of reality here - if you buy a garment at a remarkably cheap price, then the person making it is being paid very little - whether that's in the UK, or abroad. However, the person making it clearly needs the money, or they wouldn't be working for a low wage, and doesn't have an alternative, better paid, source of work. Therefore I always tell everyone who virtue signals about boycotting a particular shop, to make sure they donate money to a charity which will feed & house the people who are now unemployed because of their boycott.

Clearly BooHoo has to deny these allegations, and also has to take decisive action to sort out its supply chain. That's bound to hit its margins somewhat. Social media means that bad news travels further, and faster, than in the past. But with such a short attention span, the public quickly forget. Is this likely to damage BOO badly? I doubt it, once the dust has settled. It really is long overdue for sweatshops, and breaches of minimum wage regulations, to be properly punished. That is going to be tricky though, as sweatshops are adept at disappearing, then popping up again somewhere else, with the same people, but a new limited company. Sometimes retailers turn a blind eye, but sometimes they're unaware that orders have been subcontracted out to an unknown factory, that's the way this sector works. The rules have to be enforced, otherwise nothing will ever change. I expect customers might forward some outraged opinions, sign a petition online, and then carry on an usual after a few weeks. Hence I'd be more inclined to buy on today's drop, than to sell.

EDIT: I'm quite surprised to see BOO shares continue falling today, now down c.23% at c.300p. This is looking increasingly tempting as a buying opportunity. Unless there's been some further negative news out? End of edit.

.

Up Global Sourcing Holdings (LON:UPGS)

76p (up 13% today) - market cap £62.5m

Trading Update - the previous trading update from 8 June was surprisingly good, for background here is my article on that - with underlying EBITDA (not my measure of choice) would be above market expectations. Although a soft order book was mentioned.

Ultimate Products, the owner, manager, designer and developer of an extensive range of value-focused consumer goods brands, announces the following unscheduled trading update.

Today's update - this reads very positively to me, and it's good to have some specific figures;

Since the Group provided its previous update on 8 June, the invoicing and delivery of its order book has continued to progress at a good pace, driven in particular by a strong performance in Online.

As a result, we now anticipate that revenue for the year ending 31 July 2020 will be above £111.0m, Underlying EBITDA* will be above £9.6m, and Underlying PBT will be above £7.4m - all of which are above the market's current expectations.

Those figures are way above the (possibly old) forecasts shown on the StockReport.

My opinion - I'm very impressed indeed with how UPGS has managed to trade so well through such a difficult period. These results are tremendously impressive. I'm not looking to open any new positions at the moment, but UPGS is certainly going on my watch list of possible future purchases. There could be further upside on the share price, given this strong performance, maybe?

Divis may be back on the cards soon too. Overall, I like this share, it gets a thumbs up from me. Note the high StockRank over the last 2 years;

.

.

Macfarlane (LON:MACF)

76p (up 8% today) - mkt cap £120m

I last looked at this packaging group here on 27 Feb 2020, when it published quite good results for 2019.

Trading Update - summarising it;

- Previous guidance was that Q1 was good, and Q2 sales expected to be down 20-25% below 2019, due to lockdown

- Actual Q2 performance has been better than expected, with sales down only 7%

- Weak sectors partly offset by growth in others (e.g. online, medical, food, etc)

- H1 sales will be down 3% on LY, but includes benefit of acquisitions. Organic growth not stated, but will obviously be worse than 3% down

- All sites continued operating throughout lockdown

- Furlough - bringing back staff (30% furloughed originally), and will seek to repay sums already claimed. Not explained why

- Liquidity - tons of headroom (£30m facility), net bank debt reduced to only £2.0m - helped by Govt schemes

Guidance - still too uncertain to give specific guidance (a bit lame, as we're now in H2), but this reassures;

... based on ongoing actions and current levels of trading, we expect the business to remain profitable in 2020 and to operate well within the current borrowing facility

Divis - intention to reinstate them once there is more clarity

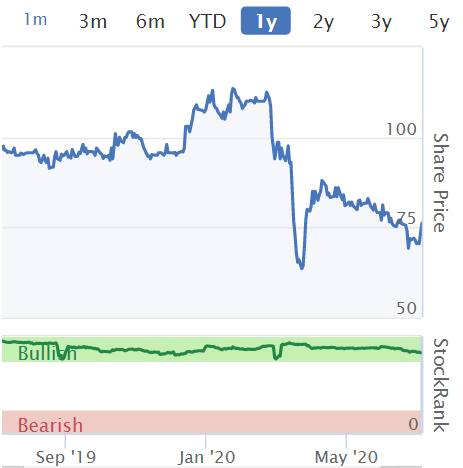

My opinion - this is clearly a good update. Shareholders can sleep more soundly now. Given that it's had a fairly good crisis, then this chart looks as if there could be some more recovery potential maybe? Note the consistently high (green) StockRank in the last year.

I think we could see nice upside from companies which reinstate divis, and this might be one that applies to.

.

.

Bigdish (LON:DISH)

2.3p (down 14% today) - mkt cap £8.0m

(I have a long position)

This is a tiny, highly speculative company that operates a dining app which allows restaurants to use dynamic pricing (i.e. discounts with half hour slots) to attract more business at times when they would otherwise be empty/quiet. Clearly this is highly relevant to the situation now restaurants are re-opening.

There's a rather long-winded strategic update out today. It doesn't seem to have impressed the market, with the share price down 14% today, but it's a highly volatile share, and had been rising in anticipation of a resumption of trading.

It's a big change to the business model, with the company expanding its offering to become a SaaS provider for restaurants, to replace the current small fee per transaction. I really like the concept of disrupting the deliveries market (basically by undercutting Deliveroo), and encouraging restaurants to promote BigDish, which removes the need for a huge marketing budget.

The Manchester based telesales team proved highly effective just before lockdown brought down the shutters.

DISH needs to raise more money, which is already known. I'm relaxed about that, as there's pots of money swilling about for dining tech companies. The last fundraise was from a US family office, at 7.2p. I imagine the next funding round is likely to come from something similar, rather than a stock markt fundraise (it's fully listed by the way, not on AIM, so more expensive to raise money from the stock market).

This share will not appeal to anyone here, so I'm not really interested in discussing it. I'm fully aware of all the negatives, but think it has interesting speculative upside. Very high risk.

My RNS - it's a long time since I've had to issue one of these, but my total DISH holding has gone over 3%. Because most of the position is on a spread bet through Spreadex, I didn't think it needed an RNS (because spread bets don't usually include voting rights). But the company told me that they wanted a TR-1 to be issued, which they have now released, after I filled it in over the weekend. Section 11 Additional Information - this explains things in full. Since my economic interest in the company is 11,529,620 shares (3.166% of the company) we thought it best to publicly declare it, as I don't want to fall foul of the FCA. Better to err on the side of declaring too much, than too little, in my view.

.

That's me done for today. See you tomorrow!

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.