Good morning, it's Paul here. Many thanks to Jack for giving me a day off yesterday, which was much appreciated.

In the usual way, this is a placeholder initially, i.e. a blank post, to enable readers to post comments from 7am, whilst I write up the article gradually throughout the morning & early afternoon, section by section. For newcomers, I report on the day's small cap trading updates & results statements, plus any other important news.

Please see the header for announcements I'll be reviewing today.

Today's report is now finished.

.

Stockopedia App

Just to flag up that I downloaded & used the Stockopedia app on my smartphone (a Samsung M31 - which is a fantastic phone for the relatively low price) last weekend, and I found it excellent. I'm a bit challenged with eyesight, hence prefer using a full-sized PC or laptop screen, as opposed to a mobile device. However, with the Stockopedia app, I could see everything clearly. It spaces out the usual StockReport into a longer, thinner version. Also, I found the news pages very easy to scroll through - better than the full webpage actually, because the left and right pane scroll independently, whereas they're locked together in the web version of Stockopedia.

Therefore, I shall be using the Stockopedia app in future when I'm out & about, to do a quick research job on a share that e.g. a friend might have recommended over lunch. Something that should hopefully be happening more often again, if restaurants remain open. I'm not sure how long that might be though, with all these second wave outbreaks popping up?

(NB. I have not been asked to post the above, it's my genuine personal opinion, and thought it might be useful to flag up to readers)

.

Norcros (LON:NXR)

Share price: 164p (up 9% today, at 08:12)

No. shares: 80.57m

Market cap: £132.1m

Norcros plc ("Norcros" or the "Group"), a market leading supplier of high quality and innovative bathroom and kitchen products, issues the following trading update for the 16 week period ended 26 July 2020 ahead of its Annual General Meeting which takes place at 11.00am today.

Note that, with a end March year end, the current financial year began shortly after lockdown restrictions were introduced in the UK, and were introduced earlier than that in some other countries. It's also worth noting that a lot of DIY shops continued trading throughout lockdown, due to bing classified as essential. Hence Norcros's customers were probably less impacted by lockdown than other sectors.

Here is the very clear table, showing how revenues have bounced back strongly in June, and more so in July, which is actually running ahead of last year. I'm not sure if this is LFL revenues, or if there have been any acquisitions which help these numbers, it isn't stated either way, which is a bit of an omission. Maybe the company and its advisers could bear that in mind with future disclosures? Actually, that is relevant to all companies which are making acquisitions.

.

.

As we can see, the business has recovered quickly & strongly from the covid crisis. There might perhaps be an element of catching up, or pent up demand, from the sales increase in July, maybe?

Profitability - more important than revenues, yet so many companies are not telling us how they're performing right now. I can't be the only investor who finds this frustrating. So a thumbs up here to Norcros, as it says;

Overall, the Group broke even at the underlying operating profit level in May with a return to profitability on the same basis in June resulting in a small underlying operating profit for the first quarter.

Reading between the lines, this suggests to me that April was probably loss-making.

We have to be careful with operating profit now, as IFRS 16 messed things up by moving some rental costs into finance charges, which is below the operating profit line on the P&L. Hence there is a danger that post-IFRS 16, operating profit now over-states true profitability, although this issue is probably not huge in £ terms, but that depends how many leasehold properties a company operates from.

Liquidity -

Strong balance sheet and liquidity

As outlined in our year end statement of 25 June, in response to the sharp impact of COVID-19 we took immediate action to preserve cashflow and reduce costs. Group net debt has reduced to £35.2m at the end of June compared with £36.4m at the year end.

Net Debt: LTM EBITDA at the end of June was 1 times compared to 0.9 times at the year end.

["LTM" I assume means Last Twelve Months?]. There should be a rule that all abbreviations are asterisked with an explanation of what they mean, for all companies. Sometimes the abbreviation may not be obvious to some readers, so it's always best to provide an explanation, rather than leaving people scratching their heads. Maybe I should start a consultancy business, to help improve the quality of trading updates? It's badly needed!

Another glaring omission, is that we're not given any figures on stretched creditors. It's easy to report lower net debt, if you're not paying VAT or payroll taxes temporarily. Companies must disclose these figures, otherwise the positive cashflow is misleading, as it's benefiting from one-off concessions from Govts. All those tax creditors will be cash going out of the door in the coming months, and before end March 2021 at the latest - coincidentally that's Norcros's next year end date, so the year end balance sheet might not look so good for net debt as today's update.

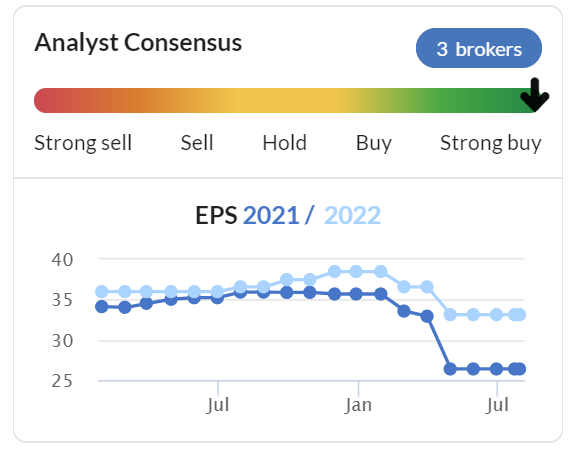

My opinion - Norcros always looks cheap, because it has a large pension fund in deficit, and is materially exposed to South Africa, with the consequent economic & political risk. Media reports suggest S.Africa is in poor shape, with massive problems, including widespread poverty, still having economic apartheid effectively, and horrendous levels of crime & drugs. Therefore I can see why Norcros shares always look cheap.

I always check the broker forecasts graph on the StockReport, to see if forecasts have come down significantly since March. IF they have, then this is a good indication that covid has been baked into the forecasts. If they're a horizontal line, then this indicates the forecasts are almost certainly out of date, hence need to be ignored. This tracks through to the valuation table & StockRanks on the StockReport too. Hence we need to be particularly careful at the moment, to double check everything.

.

.

As you can see above, forecast EPS came down a lot in March, so it looks as if the broker forecasts have indeed factored in some impact from covid.

The only thing I would question is whether Norcros might want to suspend, or reduce divis for a while? I would prefer it to preserve cash, by withholding divis, in order to de-gear, even if that means management taking some flak from income-seeking shareholders.

My opinion - I think this RNS is partially misleading, given that it doesn't say how much the company has benefited from stretching tax creditors. Also, it doesn't say whether revenue growth is organic or not?

However, now that we know it's trading profitably again, with a strong recovery in June & July, then debt is less important than previously.

Bear in mind that the pension schemes are likely to be a bigger problem, due to the effect of zero interest rates - these cause pension scheme liabilities to balloon. Although with equity & bond markets strong, then the pension scheme assets should have risen in value too.

The exposure to South Africa worries me.

I don't expect the bank to get difficult, seeing as current trading is strong.

You can buy it now on a PER of about 6, and the likelihood is that any future lockdowns would be far less broad in scale than the recent one. Hence future earnings should be able to rise. Overall, despite the issues flagged above, it still looks good value to me. DIY has apparently been doing well throughout lockdown, as people can always order stuff online. Being stuck at home twiddling our thumbs, there must be millions of people who decided it was time to revamp their homes, which should benefit Norcros.

.

.

Scs (LON:SCS)

Share price: 191.5p (up c.20% at 09:49)

No. shares: 38.0m

Market cap: £72.8m

ScS, one of the UK's largest retailers of upholstered furniture and floorings, today issues the following trading update for the 52 weeks ended 25 July 2020, ahead of announcing its preliminary results on 29 September 2020.

How about this for clarity? This table below is the best way of presenting revenue that I've seen so far, from all companies I've looked at. Simple and clear, to split the revenues into the 3 logical categories of pre-lockdown, lockdown, and post-lockdown. Please can all companies use this format for your announcements.

.

.

I had to look twice, are they really saying revenues are up 92.2% above last year, or are 92.2% of last year's numbers? This paragraph confirms, they are genuinely 92.2% up, on top of last year's numbers. We can reasonableness check this by looking at the full year figure of -5.9% down. That's only slightly down on the -4.2% down for the 34 weeks prior to covid. Therefore, this confirms that the post-lockdown period almost fully recouped the lost sales during lockdown. This is tremendously impressive.

Encouragingly, post-lockdown trading has been very strong both in-store and online, with Group order intake increasing 92.2% when compared to the same period in the prior year. This reflects pent up demand, which has been supported by our well executed re-opening plans, our continued focus on value and customer service, and our increased investment in targeted marketing over the last two months.

I can see why the share price is up 20% today, that looks fully justified by this outstanding update.

It reminds us that there is a time lag of orders received. Therefore the profit for FY 06/2020 is likely to be worse than the order intake table suggests. However, that benefits FY 06/2021, which gets off to a flying start. Therefore expect strong interim results for H1 12/2020.

Liquidity - strikingly good figures here, and a good explanation of its negative working capital model (being paid up-front, before product has been made to order).

Sadly, there is one glaring omission - no figures are given on the short term benefit of stretching creditors (VAT & payroll taxes). We must insist on companies providing this essential information please. As I keep pointing out, if sretched creditors information is withheld, then the cash/debt figures are misleading.

On 17 March 2020, the Group drew down £12m from its revolving credit facility ('RCF'). As noted in our trading update on 26 May 2020, including the £12m RCF, the Group held £48.3m in cash.

Since the end of May, the £12m borrowed under the RCF has been repaid and cash on the balance sheet has grown to £82.3m. This compares to £57.7m of cash at the end of July 2019. The increase has been driven by the Group's negative working capital model, benefiting from the order intake over the past few weeks, coupled with effective cash management actions that the Group has undertaken in response to the COVID-19 outbreak.

I think companies also need to think about the wider issue to society of holding back taxes, when they don't need to. ScS is clearly rolling in cash, which earns next to nothing on deposit. Hence why would they hold back payments to creditors? Companies which are cash-rich, should pay creditors on time, or even early (to e.g. help support small suppliers), even if they don't have to. Then trumpet why they've paid creditors quickly, to be socially responsible. Maybe ScS and other cash rich companies, are missing a trick here?

Outlook - too vague to give us anything useful. But I think it's safe to assume that +92% sales performance against last year is very unlikely to continue for long, since that must include a lot of pent-up demand from lockdown. Maybe ScS should raise its prices, if demand is that strong?

I think investors should ask for more clarity from companies. After all, companies are sector experts, so should have a good handle on what the future holds, even if it giving us a range of possible outcomes. Refusing to give any indication of the outlook, is not good enough.

Whilst it is too early to provide clarity on the outlook for the weeks and months ahead, the Group is encouraged with its trading performance since re-opening on 23 May 2020. The Board would again like to thank our colleagues for their ongoing dedication and professionalism during this time, as well as our customers, shareholders, and wider stakeholders for their continued support.

ScS is a resilient business, with a strong balance sheet, coupled with a flexible cost base, and is well positioned to navigate these difficult circumstances and maximise opportunities as and when they arise.

My opinion - I've been positive about ScS for a while, flagging it here as a good opportunity for recovery. So I hope some readers have benefited from today's share price rebound. It operates from retail parks, which are much better placed to recover, since they're big stores, with social distancing easy to do, and footfall figures show that customers have returned in greater numbers than to traditional, more cramped High Streets.

Also, as I've flagged before, ScS prices are low, hence I don't think its sofas & beds should be seen as big ticket items any more. All those millions of people locked down this year, would be more likely to replace worn out sofas, carpets, etc, than before. Hence lockdown may ultimately prove to be an overall benefit to ScS, depending on when the sales spike eases off.

.

.

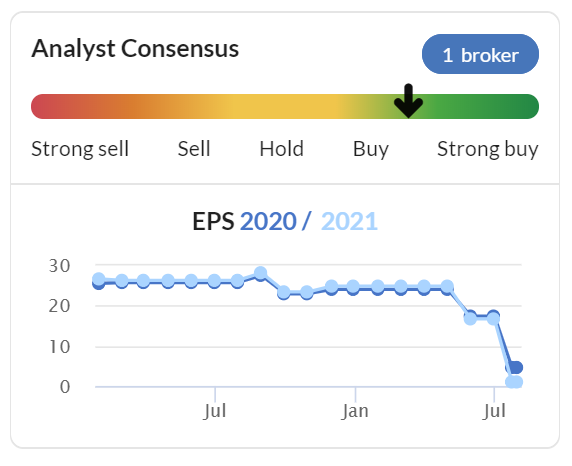

Reading today's update, it seems to me that FY 06/2021 forecasts are likely to be substantially raised (the lighter line above, for colour-challenged readers). Together with a balance sheet groaning with customers' cash, the valuation could be a bargain, even after today's 20% rise, perhaps?

.

Intercede (LON:IGP)

Share price: 75p (up 7% today, at 11:06)

No. shares: 50.5m

Market cap: £37.9m

(I'm long)

I don't normally comment on contract wins, unless it's something major, but in this case I've got a couple of broader points to make, so thank you for your indulgence.

Intercede already has a highly impressive client list (one of the main reasons I bought this share in 2018), including various branches of the USA Govt. These are long-term contracts, so very sticky, some having been running 10-15 years, or even longer. Plus there are some very big corporate clients, including 5 of the world's 6 largest aerospace companies. Therefore most of the cost base is covered by sticky, long-term recurring revenues. The company is now in year 3 of a 3-year turnaround under new management. The hope is that this should be the year that new clients kick in, with additional high margin contracts, once the product, processes, people, and finances were fixed in years 1-2.

Therefore it's encouraging to see a contract win announced today;

Intercede, the leading specialist in digital identity, credential management and secure mobility, is pleased to announce its involvement in a successful bid for a ten-year contract with the U.S. Department of State (DoS) to create an innovative Identity Management System and Credential Management System (IDMS) solution compliant with Homeland Security Presidential Directive 12 (HSPD-12) for the DoS and its customers.

Note that Intercede's main strategy is to sell through 3rd party systems integrators, with the Intercede software being a component within a bigger IT system. Here is the link to the overall project announcement, from a company called Guidepoint. I like that Guidepoint name checks Intercede's MyID product in the second paragraph - which is the new, mid-market product, designed to greatly widen Intercede's total addressable market, and MyID is quick & easy to set up, being standardised. Previously Intercede just went for the top end, high security market, with bespoke products. Hence this announcement is reassuring, that the MyID product is generating a contract win with another big part of the USA Govt. I know some people had concerns that IGP was perhaps legacy software, dining out on long-term contracts which were stimulated by a security push after 9/11. It's reassuring to see that it is still relevant for new systems today.

Guidehouse sounds like a substantial business. It was spun out of PriceWaterhouseCoopers, being their public sector division.

Headquartered in Washington, D.C., the company has more than 7,000 professionals in more than 50 locations.

The beauty of selling through third party systems integrators, is that if a project goes well, it is likely to lead to more business following on. Also as a small UK company, IGP couldn't possibly finance a worldwide sales team alone. In my various meetings with IGP management, and their RNS statements, they have stressed the importance of the partner sales channel like this. Hence it's a positive development to see this beginning to bear fruit. I'm hoping this might develop into a multibagger share, if sales really start to take off. But of course that can never be guaranteed, it's just a wish, supported by a good strategy, now it's all about execution.

A cautionary word - although this contract is pleasing, we're not given any financial details, and it was already budgeted for. Hence it shouldn't be particularly price sensitive;

Intercede expects to receive orders for software licenses and associated development, professional services and support & maintenance within the next few months; a portion of which will be recognised in the current financial year ending 31 March 2021.

The contract was included within the directors' expectations for the current financial year ending 31 March 2021.

The most recent information the company gave, was that the sales pipeline was up 40%, but Intercede does not disclose the actual amount of the sales pipeline. Hence I am hoping to see it beat expectations for FY 03/2021, which is only 6% forecast revenue growth on last year. On the downside, the covid crisis is bound to have delayed conversion of sales pipeline into sales.

My opinion - this is one of my top 3 personal holdings, because I can see the growth potential from the turnaround strategy under newish management. With such an amazing client list, offering numerous reference sites, and long-term customer stickiness, then the potential growth seems credible. Management were very cautious to begin with, but seem much more confident in the future in the most recent RNSs.

I was invited to join a Zoom company presentation for analysts & brokers recently. It was superb, and focused on introducing more members of the senior team, not just the CEO & CFO, and explaining the product. Cloudcall (LON:CALL) followed the same format recently in their webinar, and it works tremendously well, so I hope more companies adopt this format with online presentations. After the IGP Zoom call, I messaged the company to suggest it repeats the same format, and throw it open to all investors, so people can better understand what the company does, as it's not always obvious from RNSs. This included screen shots of the product itself, and the technical chap (whose name eludes me) gave a particularly clear explanation of the products. The slides were easy to follow too, so it definitely deserves a wider distribution.

The shares are horribly illiquid, so I've found that buying tends to require patience, on the dips. I recently bought some more for my SIPP, and the market makers took full advantage of me, increasing the price for any size, so think I had to pay about 5p over the market offer price, to get a decent quantity. Frustrating, but long-term, if things pan out as I hope, then paying 75p or 80p won't make any significant difference. It may not pan out as hoped though, I can't predict the future with certainty, nor can anyone else.

The issue with the convertible loans should sort itself out in about 18 months, as the company has enough cash to pay them off. Although apparently it will just be a negotiation between the company and the loan note holders (which includes Directors) as to who wants the cash, and who wants to take shares. The dilution would be unfortunate, but isn't huge, and would bring the benefit of a completely ungeared balance sheet.

So far, so good;

.

Volex (LON:VLX)

Share price: 143.7p (up 4% today, at 13:11)

No. shares: 152.25m

Market cap: £218.8m

Volex plc (AIM:VLX), the global supplier of integrated manufacturing services and power products, is today holding its Annual General Meeting, during which the Executive Chairman, Nat Rothschild, will make the following statement on trading for the three months ended June 2020...

Recap - I briefly reviewed Volex's FY 03/2020 preliminary results here. The brief version is that I like the excellent turnaround progress, like the strong balance sheet, but thought the outlook comments were a bit mixed.

Q1 update today - very good in the circumstances, I'd say;

Unaudited revenue for the three months ended June 2020 was $96 million, which was flat on the same period a year earlier. Given the disruption caused by the global coronavirus pandemic, we are very pleased with this result.

Operating profit remains at a similar level to the prior year, and our cash balance as at 24 July was $30 million. Our $30 million revolving credit facility remains available and undrawn.

This shows a really resilient business, that (for many companies) the worst period in memory, due to covid, has seen revenue & profit flat against last year. Very impressive, I think.

Outlook - same points made as last time, but good to see things are improving;

As noted in our results statement on 18 June 2020, we continue to see weakness primarily in the medical installation sector, as hospitals around the world remain closed for non-critical medical procedures. In our electric vehicle business, demand is approaching pre-crisis levels as customers re-open their factories and consumer preference continues to shift towards electric vehicles. We continue to see resilient demand in our consumer electronics and data centre businesses.

Dividends - shareholders approved the 2p final dividend today. I agree with reader comments that paying divis at this time of crisis, is a very strong signal. That's another benefit of investing in companies with strong balance sheets - they can usually keep paying divis even in times of uncertainty.

My opinion - I'm tremendously impressed with how well Volex has performed. A few years ago it looked a bit of a mess. Not many turnaround situations do actually turnaround convincingly, but this one very definitely has done so, so kudos to management.

I watched an excellent documentary over the weekend, about the manufacturing process for London cabs, now made in a state of the art £500m factory in the midlands. The key electric/hybrid version was fascinating. It really struck me how complex all the electronics are, with lots of heavy-duty cabling to cope with the high power required to move a heavy vehicle. It only has a range of 80 miles on battery only, so they've bolted on a 1.5 litre petrol engine to produce extra electricity, which extends the range greatly, to about 380 miles from memory. Although the concept of a hybrid vehicle is somewhat baffling, since there's little cost or emissions benefit from lugging around all that extra weight, whether on battery or electric power.

Anyway, the point I'm making is that this documentary made me join up the dots with Volex - i.e. it could be on the cusp of a big increase in demand from electric vehicles, once they become more widespread. I imagine the medical devices softness would sort itself out in time. After all, given the critical importance of having decent quality wiring in electrical vehicles, I imagine manufacturers wouldn't necessarily risk putting in sub-standard wiring, as it could result in breakdowns, or even fires, if short circuits arise.

Overall then, I'm inching closer to buying some Volex shares, when I have some spare cash. I'm thinking in terms of maybe buying a small or medium-sized position, not going crazy with it.

.

.

Lastly, I'll do some quick reviews of micro caps. These are thinly traded, so I'm putting less focus on the tiddlers, unless there's something really special;

Airea (LON:AIEA)

27.5p - mkt cap c.£11m

Interims for H1, 6m to 30 June 2020. I've gone through the figures, here are my brief notes;

- Pre-lockdown sales were in line with LY

- Apr & May 2020 sales down 51% vs LY

- June much better, down 9% on LY

- 6 year CBILS loan of £2.75m drawn

- VAT deferred - but doesn't say how much, and I can't find it on the balance sheet. "Deferred tax" is usually other stuff, and there aren't proper notes to the balance sheet categories

- Hoarding cash, now has pile of £6.5m, or £3.7m if we offset the CBILS debt - looks fine, but bear in mind that cash will reduce as the business expands again, due to the build up of inventories & receivables, so I think this should be seen as a bit of a one-off, artificially high cash figure

- Pension deficit has risen from £3.6m to £4.9m - consuming £400k p.a. of cashflow, as deficit recovery payments

- Outlook - H2 should produce a "modest profit"

- No interim divis - makes sense

- Balance sheet - looks fine to me. Very healthy working capital position (i.e. net current assets). Also has a £3.6m investment property, which could be sold if they ever get into difficulties - always good to have some property down the back of the sofa. Overall, I don't have any concerns re solvency risk

My opinion - looks cheap, and fairly low risk recovery play. Lack of market liquidity could be frustrating. Not the sort of thing to trade, but I think it could be a reasonable long-term recovery share. I could see say 50% upside, if recovery continues, with a maybe 1-2 year view, so quite good possibly.

.

Belvoir (LON:BLV)

145p (up 11%) - mkt cap £53.8m

Thank you to readers who flagged up this positive trading update in the comments below.

I've had a look, and agree with you! The key bit says;

The Board is delighted to report that trading during the first half of 2020 has delivered continued growth due to the success of its strategy, despite the UK-wide lockdown.

Both revenue and operating profit is comfortably ahead of 2019 with net profit in line with management's pre-Covid expectations, as set at the start of the year.

Providing there's nothing unusual in the figures, then it strikes me as very impressive that the company is now saying profits are in line with pre-Covid expectations. The hit from lockdown saw a good recovery, due to pent-up demand once lockdown ended. Similar to what ScS was saying above, so this could develop into an interesting investment theme.

Nice to see it clearly disclose deferred VAT;

The Group has continued to generate cash from operations with net debt at 30 June 2020 standing at £5.7m (31 December 2019: £6.9m) having deployed £2.0m of cash in January to acquire the Lovelle network and deferred payment of £0.5m VAT until Q1 2021.

No divi, but hoping to reinstate. I'd prefer them to strengthen the balance sheet.

Nice outlook comments.

My opinion - looks good, although my balance sheet concerns still exist. Maybe a resilient business like this can operate OK with a weak balance sheet? So my concerns might be misplaced in this case?

I've run out of time for today, so will see you in the morning.

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.