Good morning, it's Paul & Jack here, with the SCVR for Wednesday.

Timings - should mostly be done by official finish time of 1pm. Let's revise that to 5pm, there's a lot going on in the markets that is distracting me, sorry about that. Today's report is now finished.

Agenda - this is what has caught my/our eye(s) today. Jack has come up with an idea for he & I to collaborate on file sharing in google docs, so we can both contribute sections to the same article. We’re testing that out today, let’s see what happens!

Shoe Zone (LON:SHOE) - I hold - as discussed in the reader comments below, a full year trading update

Sylvania Platinum (LON:SLP) - this section written by Jack - Q1 Report

Tribal (LON:TRB) - Trading statement - looks positive

M&c Saatchi (LON:SAA) - Half year report

.

Shoe Zone (LON:SHOE)

Share price: 38p (down 16% at 10:36)

No. shares: 50.0m

Market cap: £19.0m

(I hold)

Shoe Zone PLC ("Shoe Zone") reports on trading for the 52-week period to 5 October 2020 ("FY20"), prior to entering its close period.

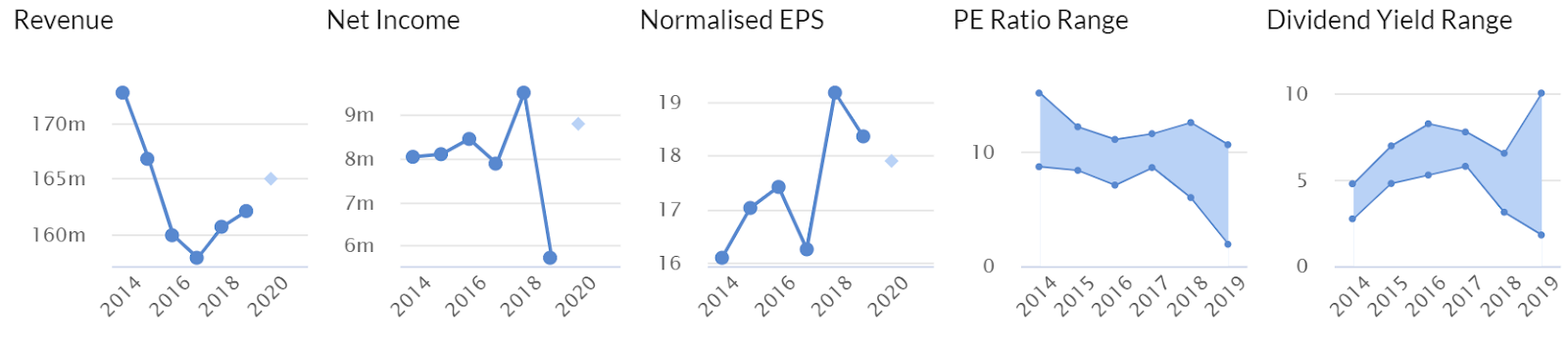

Preamble - It’s remarkable to see the market cap of Shoezone down to only £19m, given that this business used to consistently make £8m+ profit per year, and paid out generous divis. It has entrepreneurial management, Anthony & Charles Smith, who together own 50% of the business. Its leases are short, and fit-out costs are low, so it actively manages the store estate, avoiding the long tail of loss-making sites that plagues (and often destroys) other retailers. Product is cheap & cheerful, and is manufactured in China.

The light blue blobs below look outdated forecasts, so ignore those. Otherwise you can see that, in normal circumstances, this is a decently profitable business. The big question is, can it survive, and recover from covid/lockdown? IF it can, then buying now could lock in a wonderful future dividend yield, and capital appreciation too. If not, then the company could end up going bust, or being taken private for a song.

.

.

I’ve just re-read my notes from 23 June 2020, covering SHOE’s interim results to early April 2020. I concluded that liquidity looked OK, so insolvency risk seemed low back then. Lease liabilities on the balance sheet were higher than I’d imagined, which didn’t seem to tie in with management comments that leases are short term.

Shoe Zone PLC ("Shoe Zone") reports on trading for the 52-week period to 5 October 2020 ("FY20"), prior to entering its close period.

H2 “challenging”

Store trading since reopening in June has been broadly 20% down year on year with digital trading broadly 100% up year on year. While the latter is encouraging, it has not filled the deficit from store sales.

Recent Govt lockdown guidance, etc, is hurting sales, especially in tier 2 & 3 areas

FY 09/2020 is going to show a hefty loss. This is worse than I was expecting. Remember this would also be after receiving the benefit of furlough, and business rates relief in H2;

Shoe Zone generated revenues for the period of approximately £122.6 million (2019: £161.9m). As a result of the closure of its retail estate from 23 March 2020 to 15 June 2020 owing to the COVID-19 pandemic, Shoe Zone expects to report a loss before Tax for the period in the range of £10.0 million to £12.0 million.

Liquidity looks fine, because the company has a good sized Govt-guaranteed loan, hence the gross cash available would be a lot higher than the net cash below;

Notwithstanding the challenging trading conditions, Shoe Zone closed FY20 with a net cash balance of £6.3 million (2019: £11.3m). No dividend will be paid in relation to FY20 as debt repayment is now being prioritised by the Board… The Board does not anticipate Shoe Zone will be in a position to restart a dividend policy until at least the 2024/25 financial year.

This makes sense in the circumstances;

Shoe Zone ended the year with 460 stores, having opened 10 Big Box stores and closed 40 stores during the period. At the year-end 50 Big Box stores were trading. All future new openings are on hold until trading conditions improve whilst a small number of essential relocations will happen as needed.

Outlook - good to see management confirm the business is funded enough to survive.

"Shoe Zone has ended an incredibly challenging year with a robust plan and sufficient funding in place to ensure the future survival of the business. The exceptional growth in digital sales since the start of the COVID-19 pandemic demonstrates the flexibility of our operating model, and follows the decision to create an autonomous Digital department in 2019. However, it is very difficult at this stage to provide meaningful guidance on the future outlook, given the material uncertainty in the wider economy.

Business rates - the company makes the point that reintroduction of business rates from April 2021 will be devastating for the High Street. It would trigger SHOE closing a total of 90 shops by March 2022.

I think it’s absolutely right that retailers lobby the Govt hard over business rates. It would be counter-productive to re-introduce it, and I think the Govt should seriously look at abolishing it altogether, perhaps to be replaced with a hike in VAT that would be fairer being paid by physical and online retailers equally.

I can feel a letter to my MP coming on. I use a terrific platform called WriteToThem which makes it quick & easy to write to your elected representatives. We seem to have a particularly clueless/flexible (delete as you wish) Government, which seems to work on the basis of floating policy ideas through leaks, and then backing down or reversing strategy when there’s a public outcry. I quite like that, as nobody really knows what to do re covid, hence being flexible/pragmatic is surely the best approach? Also it means that writing to your MP is actually worthwhile, because they are listening, and you could help guide policy. I’ve written to my MP several times, about more support being needed for the arts, and for the beleaguered hospitality sector, and policy was changed to give both sectors more support. So plenty of other people must have done the same. They say that for every 1 person who bothers to write, 100 others agree but don't write. Hence one letter effectively magnifies your view/influence 100 fold.

My opinion - I agree with a reader comment below, that the trading since re-opening figures actually look quite good in the circumstances. Also I like the confirmation that liquidity is still adequate to ensure survival of the business. SHOE went into this crisis with a strong balance sheet, and plenty of cash. Therefore it should survive & recover, unlike many other retail/hospitality businesses which entered the crisis with existing debt, and no cash reserves. Nobody knows what the future holds, that’s why it is so important for companies (and households) to have some money tucked away for a rainy day. People used to scoff at such a notion being old-fashioned, or inefficient. They’re not scoffing now.

My one reservation with SHOE, is why the loss is going to be so large, at £10-12m. Although I wonder if that might include some non-cash write-offs (e.g. onerous lease provisions, writing off fixed assets, etc?). The update today is not clear on that.

I agree with reader comments that this update seems to cut a deliberately negative stance. Maybe that is to help increase the company’s leverage in lease negotiations? Or maybe a precursor to a cheeky lowball takeover bid? I hope not. My feeling is that, once a company floats on the stock market, then management have a moral responsibility to stick at it, and work hard to recover things from any setback, not grab the future upside for themselves with a buyout at the lows. But we’re speculating there.

Overall, I’m happy to hold, and might top up on any further weakness, but I don’t see this becoming a large position in my portfolio. It’s small at the moment, and might become medium, but no more than that, as my conviction on it is not particularly strong.

Has the share price overshot to the downside? Quite possibly, in my view, given that trading should recover at least somewhat in 2021, and there doesn't appear to be any insolvency risk. Therefore as a recovery situation, I like the look of this, at 36p. I can foresee 100% upside on that price, once the market becomes more upbeat about covid/economic recovery. That's appealing, if I'm right. Maybe I should be buying more? Can't decide at the moment, I'll have a think about that.

.

.

** This next section written by Jack Brumby **

Sylvania Platinum (LON:SLP)

Share price: 68.33p (-2.11%)

Shares in issue: 271,476,690

Market cap: £185.5m

(Jack: I hold)

Sylvania Platinum (LON:SLP) is a low-cost producer of platinum group metals (PGMs) with dump operations and exploration assets in the South Africa Bushveld Igneous Complex. If you believe that PGM spot prices are set to appreciate, or are even just sustainable at current levels, then the company’s shares are cheap.

Sylvania understands this and has been diligently buying them back.

Today it reports its First Quarter results.

Running through the headline figures:

- Sylvania Dump Operations declared 17,972 4E PGM ounces in Q1 (Q1 FY2020: 20,797 ounces)

- $41.5m of net revenue (Q1 FY2020: $31.2m)

- Group cash costs per PGM ounce down to $652/ounce

- Net profit of $21.0m (Q1 FY2020: $12.5m)

- Cash balance of $60.9m, up $5m quarter-on-quarter

Operational challenges

The global COVID-19 pandemic is a concern but the country remains in Level-1 Lockdown which does not hinder production. This could always change though, as we’re seeing in the UK currently.

Reduced mining operations at some host mines due to the depressed chrome market are leading to lower PGM feed grades and recoveries. This was flagged in a previous update. That update did note some asset writedowns as well but there is no further mention of that in today’s RNS.

Opportunities

Risks remain, but SLP is in such a cash generative position that it has been able to progress its growth capex initiatives while buying back shares. In particular:

- The new Lannex mill and spiral upgrade project is ongoing;

- Design of Lesedi secondary milling and flotation module to is advancing;

- Mooinooi chrome processing modifications and optimisation project is in execution phase and expected to commission during Q3.

Commenting on the Q1 results, Sylvania's CEO, Jaco Prinsloo said:

We anticipate to reach our estimated production target of approximately 70,000 ounces of PGM's for the year. The Company continues to enjoy the benefits of the strong PGM price environment and the 31% increase in gross basket price from Q4 has assisted in boosting our financial performance and cash reserves. The Company remains in a robust financial position with sufficient cash reserves to fund capital projects which will help mitigate any rise in costs and the possible reduction in future cash inflows due to the ongoing uncertainty relating to COVID-19.

Conclusion

Sylvania remains debt free and continues to maintain strong cash reserves, which provides a decent margin of safety. The $60.9m of net cash equates to roughly £45m at current exchange rates, which is about 24% of the market cap.

The share price has recovered well from its last update, which ruffled some feathers due to a lower-than-expected dividend payment. I’m not here for the dividends though. If the share price really is as cheap as it looks then the company is right to be buying back shares instead.

And building up the cash cushion, now more than ever, seems prudent.

Risks remain. The reduced mining operations of certain host mines continues to impact on feed grades and Q1's PGM production decreased 14% year-on-year. This is something to monitor going forwards. There have also been issues with water access and energy supply to its sites in the past.

There is always the big unknown of the PGM spot prices. That’s probably the most important factor in the whole investment case, so you need to take a view here. Mine is that current prices will be at least maintained due to structural demand factors but others may disagree on this point.

In my view the valuation continues to compensate for the risks involved and I’m holding for a sustained rerating.

The near-return to historic levels of production is a creditable performance in light of the COVID disruption and government-imposed industry shutdown faced by this miner earlier in the year. The brokers are targeting 100p+ and, given the low valuation metrics, that doesn’t seem unreasonable to me assuming spot prices are at least maintained and there are no further operational disruptions.

.

Tribal (LON:TRB)

Share price: 70p (up 8% today, at 12:20)

No. shares: 205.7m

Market cap: £144.0m

Tribal (AIM: TRB), a leading provider of software and services to the international education market, today provides an update on trading for the year ending 31 December 2020 ("the Year") and information regarding the reinstatement of the dividend.

As a result of the uplift in revenue from the two new contracts, the ongoing benefit of cost reduction measures introduced at the start of the COVID-19 pandemic, the increased efficiency of the remote delivery of Professional Services and Education Services, and the strength of the Group's recurring revenue model, the Board now anticipates reporting profits for the Year comfortably ahead of current market expectations(1), at approximately £14.8m adjusted EBITDA(2) and £11.5m adjusted EBITA. Total revenue is expected to be in the region of £72m. Annual Recurring Revenue has increased to £44.5m.

(1) In so far as the Board is aware, prior to this announcement, market expectations for the year ending 31 December 2020 were for revenue of £72.1m, adjusted EBITDA of £13.7m and adjusted EBITA of £10.5m.

(2) Adjusted EBITDA is in respect of continuing operations excluding restructuring costs, share based payments and amortisation of acquired (IFRS3) intangibles.

Thank you to the company & its advisers for the footnotes, informing us what market expectations are. This is incredibly helpful, and everyone should be doing it. I’m told that some old-fashioned brokers push back against doing this, which is harming their clients’ interests. Transparency helps us understand the company, and makes us more likely to buy its shares. Why do I need to explain that, it should be obvious?!

Personally, I find EBITDA meaningless for software companies, due to internal development costs being capitalised. TRB capitalised £3.2m development costs in H1 alone, so very material. That’s fine to capitalise development costs, but we have to reflect those costs somewhere when we value the company. EBITDA ignores both current & historic development costs altogether! Which clearly is nonsense.

Therefore I use adj EPS instead, a much more meaningful figure to use in valuing software companies. My thanks go to N+1 Singer, which has kindly made available an update note today on Research Tree. This reflects today’s positive update, with FY 12/2020 EPS forecast now at 4.6p (up from 4.3p in 2019) - not many companies are growing 2020 earnings over 2019, so that’s impressive.

The PER is 70p/4.6p = 15.2 - that’s not expensive at all these days, for a software company with strong recurring revenues. Also the broker indicates further upgrades could be in the pipeline if trading momentum continues.

Balance sheet - is actually quite weak, with negative NTAV. However, like a lot of other software companies, it has a favourable working capital setup, where customers typically pay up-front, therefore it can operate with a decent cash pile, despite having negative tangible assets overall.

There is an argument for regarding software development costs as a genuine asset. We were discussing this the other day. Conventional businesses buy machines which are long-use assets, and capitalise them. Whereas IT companies spend on intangibles by paying developers to produce code, which they then sell as a service, so these costs are capitalised. That’s one way of looking at it.

I understand that point of view, but to my mind, anyone who is on the payroll, should have their salary expensed through the P&L, whatever they’re doing! Also, I see development costs as an ongoing cost of running an IT business. If you stop product development, then the company will go into run-off, and slowly die as competitors overtake.

Current liabilities exceed current assets, for example, so people need to be aware of that too - i.e. even if you want to keep some intangibles on the balance sheet, which would make NAV positive, there’s still a shortfall on working capital, with the net current liabilities position. It’s OK, not a problem, I’m just pointing out that by several different measures, this is not a strong balance sheet.

So instead of claiming to have a strong balance sheet, the company could be more accurate perhaps by saying we know we’ve got a weakish balance sheet, but it doesn’t matter because of inherently favourable working capital flows. That’s nearer to the truth, in my opinion.

The Group retains a strong balance sheet, with a net cash position as at 23 October 2020 of £11.2m. The positive trading has enabled the Group to repay all furlough benefits received (approximately £80k) and all temporary tax deferrals.

So liquidity is fine.

I’m labouring the point here, let’s move on!

Dividends - Tribal is reinstating the divis, with a flat against last year interim divi of 1.1p - not earth-shattering, but it’s an important signal of confidence, and that there’s cash available.

Outlook - I like the sound of this;

"Our priorities for the remainder of 2020 are to continue to protect the business from the impact of COVID-19, win new customers, retain and grow existing customer relationships, and deliver on the Tribal Edge strategy.

"Never has the need for cloud-based solutions for the Education market been more pressing. The investments we have made position us at the forefront of this evolution in our industry, providing for an exciting future for Tribal."

.

My opinion - this is a very good update, considering how covid has impacted the education sector.

I think the valuation looks reasonable, cheap even, if good momentum continues.

This company has never really caught my imagination before, because performance was patchy, and it seemed accident-prone, e.g. that big legal action it ended up with not long ago.

However, today’s update sounds like something more positive is going on under the surface. Winning new customers, offering a cloud product, developing ways of installing it remotely, etc, this all sounds very impressive, and very relevant to the modern world. That you can buy the share on a PER of about 15 now, seems a good deal. Somebody might bid for it.

I’d prefer a stronger balance sheet, but am prepared to ignore that, given that the company is trading well, and has a good outlook.

Therefore I can feel myself turning positive on this share, because the fundamentals and outlook are now looking a lot better than when I’ve looked at it in the past. For that to be happening during covid, is impressive.

Therefore Tribal gets a thumbs up from me. Not a recommendation, as always, just my personal opinion. Over to you, to do your own research on it.

.

M&c Saatchi (LON:SAA)

Share price: 58p (suspended since 1 Oct 2020 due to late accounts)

No. shares: 115.4m

Market cap: £66.9m

This is a very unusual situation, in that the company is publishing its 2020 interim results, but hasn’t yet published its audited 2019 results, due to problems with the audit. It said 2019 accounts would be published “within weeks” on 30 Sept 2020, so hopefully these will be imminent.

I’m struggling to understand how they can publish 2020 interims before they’ve agreed the starting balance sheet with the auditors from the previous accounts. I’m very wary of all situations where something has gone wrong with the accounts, because often it can be a lot worse than originally disclosed (Staffline, Patisserie Valerie, Conviviality, and many others, especially overseas companies on AIM, although the UK ones are often not much better!)

I last covered SAA here on 27 Aug 2020, where I thought it looks potentially interesting, based on a small underlying profit for H1 being in the pipeline, new business wins strong, and a comfortable liquidity position with net cash of £20.0m.

Interim results for the 6 months to 30 June 2020 - clearly this covers the worst of the original covid lockdown, so figures are likely to be poor.

These look OK in the circumstances;

- Revenue down 13% to £103.4m

- Headline profit before tax of £2m before exceptional costs, down 59%

- Costs cut - being a people business, it should have a fairly flexible cost basis - although expensive London offices might be a problem now?

- Current cash position looks healthy;

- £28m at 20 October 2020

- No divi

Outlook comments - very clear guidance here;

Current trading and outlook

· Positive trends have continued into H2, although there remains considerable uncertainty due to the ongoing Covid-19 pandemic

· The Group's clients and revenue are heavily weighted towards resilient industry sectors, such as government, e-commerce and financial services

· Revenues expected to be marginally stronger in H2 than H1 with 2020 full year headline PBT, excluding exceptional items, expected to be at least £4m

· 2020 year end net cash expected to be at least £10m

· Full year operating costs expected to be approximately £30m lower than 2019 as a result of restructuring, the majority of which are expected to be ongoing cost savings

· The Group is in the process of exiting from companies that are expected to generate combined losses of £5m in 2020, with divestment or closure expected to be completed before the year end

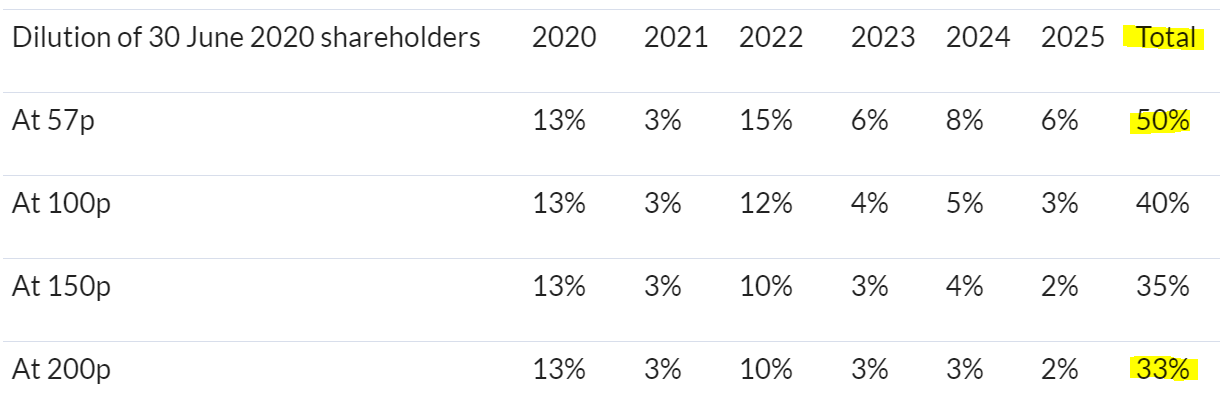

Put Options scheme - this is rather confusing, but it seems to be a form of bonus/deferred consideration, payable in shares, which now looks potentially problematic.

There’s an explanation in note 13;

The Company has experienced a significant decline in its share price since 2019, from a peak of 394p per share in March 2019. In many of the share schemes, the consideration is calculated at a fixed multiple of the relevant subsidiary Company's profits - this is effectively a deferred consideration model used by the Company for acquisitions. The consideration is typically paid in shares of the Company, with the result that as the Company's share price has fallen a greater number of shares are needed to be issued as consideration under the schemes. This has a very significant dilutive effect. It is important to note that no transactions have been structured in this manner for several years and no transactions will be structured in this way in future.

OK, I’ve got my head round this issue now. This table below is the base case scenario, and shows the % dilution of existing shareholders, from the issue of shares that the company is committed to, as reward schemes for management relating to acquired subsidiaries.

As you can see, the dilution is very substantial, even if the share price were to recover strongly from its current 57p level.

Another table is provided, which shows a mitigated case, where the company is negotiating with holders of these put options, to try to get them to move to cash bonuses instead.

.

.

This looks a bit of a disaster for existing shareholders, who look set to be substantially diluted. The table doesn’t show the worst case scenario either. If the share price really collapses, then the dilution could become ruinous. I note their table assumes that the share price won’t go any lower than the current (suspended) level.

Balance sheet - some quite large numbers in here. NAV is £57.1m, less intangibles of £38.7m, gives NTAV of £18.4m.

The minority shareholder put option liabilities seem to have greatly reduced on the latest balance sheet, compared with last year, which I don’t understand given the large dilution that seems to be in the pipeline from these liabilities (payable in shares).

My opinion - definitely too complicated for me to want to get involved.

Whoever dreamed up & agreed to the put option schemes clearly didn’t think it through, and it’s now blown up to be a major problem - with potentially large dilution of existing holders.

If there was no put option problem, then this share would look quite interesting. However, the numbers in note 13 of large dilution in the pipeline, is a major worry, and justifies a big share price discount.

Therefore when looking at this share, it’s vital that people include the dilutive impact of these new shares which could see the share count rise by c.50%, or even more, if the share price falls a lot lower.

It all looks a mess, and puts me off wanting to buy any SAA shares, once it comes back from suspension. Maybe they’ll get it all sorted, but that might involve having to make substantial cash payments instead, to persuade holders of the put options to give them up?

.I've run out of time for today, so sorry I didn't get round to looking at Redde Northgate (LON:REDD)

See you tomorrow!

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.